Seven & I Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Seven & I Holdings faces intense retail rivalry, moderate supplier leverage, evolving buyer preferences and digital substitutes, plus regulatory and scale barriers that shape its margins and growth prospects. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore detailed force ratings, strategic implications, and actionable insights.

Suppliers Bargaining Power

Scale-driven supplier leverage

Seven & i’s vast 7-Eleven network—over 70,000 stores globally—plus a multi-format portfolio concentrates purchasing volumes, diluting individual supplier power. Global aggregation across FMCG, beverages and tobacco secures tougher terms and slotting control, supported by multi-year frameworks that stabilize pricing and supply continuity. Category captives like tobacco retain influence due to regulation and inelastic demand.

Private label and assortment control

Seven & i’s strong private‑label programs act as substitutes for national brands, reducing supplier leverage, while assortment optimization and strict planogram control across its network of over 21,000 stores in 2024 dictate shelf access and velocity, squeezing trade spend. Data‑driven category management using POS and loyalty data gives the group pricing and promotional leverage in negotiations. Specialty and premium niches with limited substitutes keep select suppliers relatively stronger.

Fresh, logistics, and perishables dependence

For fresh foods and daily prepared items, switching costs and coordination complexity raise supplier power as Seven & I serves over 20,000 domestic stores, requiring synchronized deliveries and strict shelf-life control. Temperature-controlled logistics and central kitchens create mutual dependence between retailer and vendors. Backward integration and multi-sourcing reduce exposure but do not eliminate reliance on specialized cold-chain providers. Strict local procurement and food-safety approvals further concentrate qualified suppliers in 2024.

Energy, payments, and tech vendors

Utilities, payment networks and POS/IT vendors hold leverage over Seven & i due to few alternatives and high integration/upgrade costs; long upgrade cycles and EMV/security compliance further entrench suppliers. Seven & i uses scale — about 24,000 stores and roughly 4 trillion JPY revenue (FY2023/24) — to secure multi-year contracts and volume discounts, while shifting to cashless partners and energy-efficiency projects to cut exposure.

- Limited alternatives: high switching costs

- Compliance lock‑in: EMV/security mandates

- Negotiation power: scale ~24,000 stores, ~4T JPY revenue (FY2023/24)

- Mitigation: cashless partnerships, energy efficiency

Geopolitical and commodity volatility

- Import dependence: Japan ~100% crude oil

- Freight: 2024 rates below 2021 peaks but volatile

- Mitigation: hedging + regional sourcing

- Pass-through: tied to category elasticity

70,000+ stores, ¥4T cuts supplier power; tobacco/fresh/IT keep leverage

Seven & i’s scale (70,000+ global stores; ~24,000 domestic; ~4T JPY revenue FY2023/24) compresses supplier power via volume buying and private‑label leverage, but tobacco, fresh/chilled and IT/utility vendors retain high bargaining power due to regulation, cold‑chain complexity and integration costs. FX/freight shocks in 2024 temporarily raised supplier leverage.

| Category | Supplier power | Metric |

|---|---|---|

| Tobacco | High | Regulated, inelastic |

| Fresh/chilled | High | 20,000 domestic stores logistics |

| FMCG/Brands | Low | Private label, volume |

What is included in the product

Concise Porter's Five Forces assessment of Seven & I Holdings highlighting intense retail rivalry, moderate buyer power, fragmented supplier influence, low entry barriers for niche formats, and threats from omnichannel substitutes.

One-sheet Porter’s Five Forces for Seven & I Holdings—quickly visualize competitive pressure with a spider chart, customize force levels for changing retail trends, and drop into decks or Excel dashboards for fast, board-ready strategic decisions.

Customers Bargaining Power

Low switching costs for convenience shoppers

Convenience shoppers face very low switching costs and routinely move among 7-Eleven, FamilyMart, Lawson, supermarkets and QSRs, eroding differentiation on staples given widespread product overlap. The Japanese convenience market tops 10 trillion yen annually and 7-Eleven Japan operates roughly 21,000 stores, intensifying proximity-driven competition. Loyalty programs and private-label ranges boost retention but do not fully lock in customers; price-matching and frequent promotions remain key to sustaining traffic.

Price sensitivity amid inflation

Macroeconomic pressure (Japan CPI around 3.0% in 2024) pushes customers toward value, multipacks and ready-to-eat price points, strengthening demand for visible affordability and portion-right sizing. Buyers increasingly choose private-label options, which raises direct comparisons with discounters on price and quality. Price elasticity is mission-dependent: urgent trips show low elasticity, planned purchases remain highly elastic.

Digital expectations and omnichannel

Customers now expect mobile ordering, delivery, and frictionless payments, driving higher app engagement and deal-seeking through app-based promotions that increase price transparency. Ratings and social feedback magnify buyer voice, accelerating shifts in footfall and SKU demand. Seven & i’s integration of fintech services and loyalty into its ecosystem helps partially lock in users, modering but not eliminating customer bargaining power.

Urban density and location convenience

High urban density and over 21,000 Seven-Eleven stores in Japan (2024) lower travel costs and strengthen buyer choice; micro-market overlap drives demand for highly localized assortments. Convenience and late-night access reduce price sensitivity for urgent missions, while clear mission segmentation (quick grab vs planned shop) is essential to balance margin and retention.

- High density: >21,000 stores (Japan, 2024)

- Micro-markets: overlap raises local SKU tailoring

- Urgent missions: lower price elasticity due to convenience

- Segmentation: key to margin vs retention

Corporate and B2B micro-accounts

Corporate and B2B micro-accounts negotiate services across office supplies, logistics, catering and financial products; bundled solutions introduced in 2024 reduced churn and weakened buyer leverage. Large accounts still extract volume discounts and service SLAs, particularly for regional rollouts. Cross-selling between retail and financial arms in 2024 increased client stickiness and recurring revenue.

- Bundling lowers bargaining power

- Large accounts demand discounts/SLAs

- Cross-selling boosts retention (2024)

Japanese convenience shoppers gain leverage: >10T yen market, CPI ~3% raises price sensitivity

Customers wield strong bargaining power due to very low switching costs and dense competition; Japan convenience market >10 trillion yen (2024) and Seven‑Eleven Japan >21,000 stores raise buyer choice. CPI ~3.0% (2024) shifts demand to value/private‑label, increasing price sensitivity on planned trips. Digital apps and fintech loyalty raise transparency and retention, moderating but not nullifying customer leverage.

| Metric | Value (2024) |

|---|---|

| Seven‑Eleven Japan stores | >21,000 |

| Japan convenience market | >10 trillion yen |

| Japan CPI | ~3.0% |

What You See Is What You Get

Seven & I Holdings Porter's Five Forces Analysis

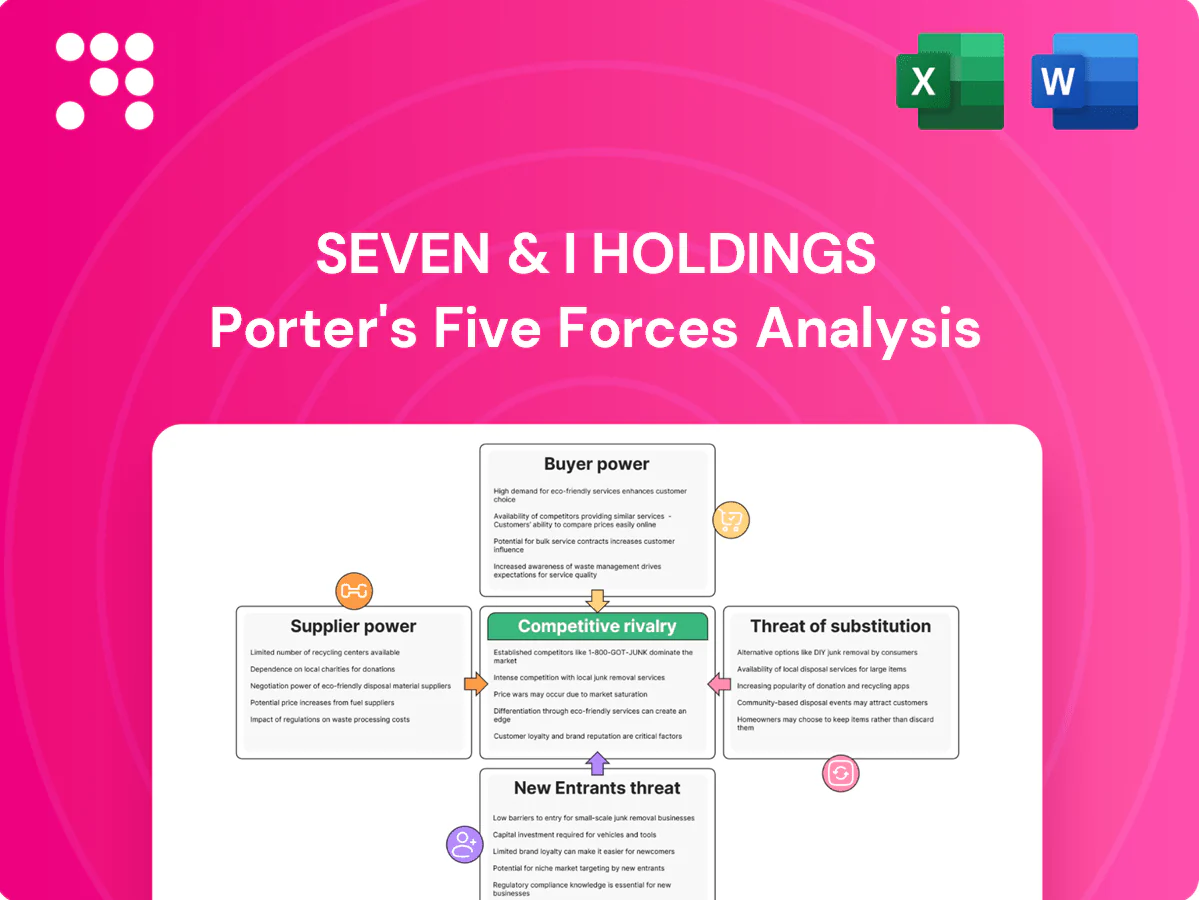

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Seven & I Holdings Porter's Five Forces Analysis evaluates supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, highlighting implications for convenience-store scale, private-label strategy, omnichannel competition, and regulatory risk. The file is fully formatted and ready for download and use the moment you buy.

From Overview to Strategy Blueprint

Seven & I Holdings faces intense retail rivalry, moderate supplier leverage, evolving buyer preferences and digital substitutes, plus regulatory and scale barriers that shape its margins and growth prospects. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore detailed force ratings, strategic implications, and actionable insights.

Suppliers Bargaining Power

Scale-driven supplier leverage

Seven & i’s vast 7-Eleven network—over 70,000 stores globally—plus a multi-format portfolio concentrates purchasing volumes, diluting individual supplier power. Global aggregation across FMCG, beverages and tobacco secures tougher terms and slotting control, supported by multi-year frameworks that stabilize pricing and supply continuity. Category captives like tobacco retain influence due to regulation and inelastic demand.

Private label and assortment control

Seven & i’s strong private‑label programs act as substitutes for national brands, reducing supplier leverage, while assortment optimization and strict planogram control across its network of over 21,000 stores in 2024 dictate shelf access and velocity, squeezing trade spend. Data‑driven category management using POS and loyalty data gives the group pricing and promotional leverage in negotiations. Specialty and premium niches with limited substitutes keep select suppliers relatively stronger.

Fresh, logistics, and perishables dependence

For fresh foods and daily prepared items, switching costs and coordination complexity raise supplier power as Seven & I serves over 20,000 domestic stores, requiring synchronized deliveries and strict shelf-life control. Temperature-controlled logistics and central kitchens create mutual dependence between retailer and vendors. Backward integration and multi-sourcing reduce exposure but do not eliminate reliance on specialized cold-chain providers. Strict local procurement and food-safety approvals further concentrate qualified suppliers in 2024.

Energy, payments, and tech vendors

Utilities, payment networks and POS/IT vendors hold leverage over Seven & i due to few alternatives and high integration/upgrade costs; long upgrade cycles and EMV/security compliance further entrench suppliers. Seven & i uses scale — about 24,000 stores and roughly 4 trillion JPY revenue (FY2023/24) — to secure multi-year contracts and volume discounts, while shifting to cashless partners and energy-efficiency projects to cut exposure.

- Limited alternatives: high switching costs

- Compliance lock‑in: EMV/security mandates

- Negotiation power: scale ~24,000 stores, ~4T JPY revenue (FY2023/24)

- Mitigation: cashless partnerships, energy efficiency

Geopolitical and commodity volatility

- Import dependence: Japan ~100% crude oil

- Freight: 2024 rates below 2021 peaks but volatile

- Mitigation: hedging + regional sourcing

- Pass-through: tied to category elasticity

70,000+ stores, ¥4T cuts supplier power; tobacco/fresh/IT keep leverage

Seven & i’s scale (70,000+ global stores; ~24,000 domestic; ~4T JPY revenue FY2023/24) compresses supplier power via volume buying and private‑label leverage, but tobacco, fresh/chilled and IT/utility vendors retain high bargaining power due to regulation, cold‑chain complexity and integration costs. FX/freight shocks in 2024 temporarily raised supplier leverage.

| Category | Supplier power | Metric |

|---|---|---|

| Tobacco | High | Regulated, inelastic |

| Fresh/chilled | High | 20,000 domestic stores logistics |

| FMCG/Brands | Low | Private label, volume |

What is included in the product

Concise Porter's Five Forces assessment of Seven & I Holdings highlighting intense retail rivalry, moderate buyer power, fragmented supplier influence, low entry barriers for niche formats, and threats from omnichannel substitutes.

One-sheet Porter’s Five Forces for Seven & I Holdings—quickly visualize competitive pressure with a spider chart, customize force levels for changing retail trends, and drop into decks or Excel dashboards for fast, board-ready strategic decisions.

Customers Bargaining Power

Low switching costs for convenience shoppers

Convenience shoppers face very low switching costs and routinely move among 7-Eleven, FamilyMart, Lawson, supermarkets and QSRs, eroding differentiation on staples given widespread product overlap. The Japanese convenience market tops 10 trillion yen annually and 7-Eleven Japan operates roughly 21,000 stores, intensifying proximity-driven competition. Loyalty programs and private-label ranges boost retention but do not fully lock in customers; price-matching and frequent promotions remain key to sustaining traffic.

Price sensitivity amid inflation

Macroeconomic pressure (Japan CPI around 3.0% in 2024) pushes customers toward value, multipacks and ready-to-eat price points, strengthening demand for visible affordability and portion-right sizing. Buyers increasingly choose private-label options, which raises direct comparisons with discounters on price and quality. Price elasticity is mission-dependent: urgent trips show low elasticity, planned purchases remain highly elastic.

Digital expectations and omnichannel

Customers now expect mobile ordering, delivery, and frictionless payments, driving higher app engagement and deal-seeking through app-based promotions that increase price transparency. Ratings and social feedback magnify buyer voice, accelerating shifts in footfall and SKU demand. Seven & i’s integration of fintech services and loyalty into its ecosystem helps partially lock in users, modering but not eliminating customer bargaining power.

Urban density and location convenience

High urban density and over 21,000 Seven-Eleven stores in Japan (2024) lower travel costs and strengthen buyer choice; micro-market overlap drives demand for highly localized assortments. Convenience and late-night access reduce price sensitivity for urgent missions, while clear mission segmentation (quick grab vs planned shop) is essential to balance margin and retention.

- High density: >21,000 stores (Japan, 2024)

- Micro-markets: overlap raises local SKU tailoring

- Urgent missions: lower price elasticity due to convenience

- Segmentation: key to margin vs retention

Corporate and B2B micro-accounts

Corporate and B2B micro-accounts negotiate services across office supplies, logistics, catering and financial products; bundled solutions introduced in 2024 reduced churn and weakened buyer leverage. Large accounts still extract volume discounts and service SLAs, particularly for regional rollouts. Cross-selling between retail and financial arms in 2024 increased client stickiness and recurring revenue.

- Bundling lowers bargaining power

- Large accounts demand discounts/SLAs

- Cross-selling boosts retention (2024)

Japanese convenience shoppers gain leverage: >10T yen market, CPI ~3% raises price sensitivity

Customers wield strong bargaining power due to very low switching costs and dense competition; Japan convenience market >10 trillion yen (2024) and Seven‑Eleven Japan >21,000 stores raise buyer choice. CPI ~3.0% (2024) shifts demand to value/private‑label, increasing price sensitivity on planned trips. Digital apps and fintech loyalty raise transparency and retention, moderating but not nullifying customer leverage.

| Metric | Value (2024) |

|---|---|

| Seven‑Eleven Japan stores | >21,000 |

| Japan convenience market | >10 trillion yen |

| Japan CPI | ~3.0% |

What You See Is What You Get

Seven & I Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Seven & I Holdings Porter's Five Forces Analysis evaluates supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, highlighting implications for convenience-store scale, private-label strategy, omnichannel competition, and regulatory risk. The file is fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Seven & I Holdings faces intense retail rivalry, moderate supplier leverage, evolving buyer preferences and digital substitutes, plus regulatory and scale barriers that shape its margins and growth prospects. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore detailed force ratings, strategic implications, and actionable insights.

Suppliers Bargaining Power

Scale-driven supplier leverage

Seven & i’s vast 7-Eleven network—over 70,000 stores globally—plus a multi-format portfolio concentrates purchasing volumes, diluting individual supplier power. Global aggregation across FMCG, beverages and tobacco secures tougher terms and slotting control, supported by multi-year frameworks that stabilize pricing and supply continuity. Category captives like tobacco retain influence due to regulation and inelastic demand.

Private label and assortment control

Seven & i’s strong private‑label programs act as substitutes for national brands, reducing supplier leverage, while assortment optimization and strict planogram control across its network of over 21,000 stores in 2024 dictate shelf access and velocity, squeezing trade spend. Data‑driven category management using POS and loyalty data gives the group pricing and promotional leverage in negotiations. Specialty and premium niches with limited substitutes keep select suppliers relatively stronger.

Fresh, logistics, and perishables dependence

For fresh foods and daily prepared items, switching costs and coordination complexity raise supplier power as Seven & I serves over 20,000 domestic stores, requiring synchronized deliveries and strict shelf-life control. Temperature-controlled logistics and central kitchens create mutual dependence between retailer and vendors. Backward integration and multi-sourcing reduce exposure but do not eliminate reliance on specialized cold-chain providers. Strict local procurement and food-safety approvals further concentrate qualified suppliers in 2024.

Energy, payments, and tech vendors

Utilities, payment networks and POS/IT vendors hold leverage over Seven & i due to few alternatives and high integration/upgrade costs; long upgrade cycles and EMV/security compliance further entrench suppliers. Seven & i uses scale — about 24,000 stores and roughly 4 trillion JPY revenue (FY2023/24) — to secure multi-year contracts and volume discounts, while shifting to cashless partners and energy-efficiency projects to cut exposure.

- Limited alternatives: high switching costs

- Compliance lock‑in: EMV/security mandates

- Negotiation power: scale ~24,000 stores, ~4T JPY revenue (FY2023/24)

- Mitigation: cashless partnerships, energy efficiency

Geopolitical and commodity volatility

- Import dependence: Japan ~100% crude oil

- Freight: 2024 rates below 2021 peaks but volatile

- Mitigation: hedging + regional sourcing

- Pass-through: tied to category elasticity

70,000+ stores, ¥4T cuts supplier power; tobacco/fresh/IT keep leverage

Seven & i’s scale (70,000+ global stores; ~24,000 domestic; ~4T JPY revenue FY2023/24) compresses supplier power via volume buying and private‑label leverage, but tobacco, fresh/chilled and IT/utility vendors retain high bargaining power due to regulation, cold‑chain complexity and integration costs. FX/freight shocks in 2024 temporarily raised supplier leverage.

| Category | Supplier power | Metric |

|---|---|---|

| Tobacco | High | Regulated, inelastic |

| Fresh/chilled | High | 20,000 domestic stores logistics |

| FMCG/Brands | Low | Private label, volume |

What is included in the product

Concise Porter's Five Forces assessment of Seven & I Holdings highlighting intense retail rivalry, moderate buyer power, fragmented supplier influence, low entry barriers for niche formats, and threats from omnichannel substitutes.

One-sheet Porter’s Five Forces for Seven & I Holdings—quickly visualize competitive pressure with a spider chart, customize force levels for changing retail trends, and drop into decks or Excel dashboards for fast, board-ready strategic decisions.

Customers Bargaining Power

Low switching costs for convenience shoppers

Convenience shoppers face very low switching costs and routinely move among 7-Eleven, FamilyMart, Lawson, supermarkets and QSRs, eroding differentiation on staples given widespread product overlap. The Japanese convenience market tops 10 trillion yen annually and 7-Eleven Japan operates roughly 21,000 stores, intensifying proximity-driven competition. Loyalty programs and private-label ranges boost retention but do not fully lock in customers; price-matching and frequent promotions remain key to sustaining traffic.

Price sensitivity amid inflation

Macroeconomic pressure (Japan CPI around 3.0% in 2024) pushes customers toward value, multipacks and ready-to-eat price points, strengthening demand for visible affordability and portion-right sizing. Buyers increasingly choose private-label options, which raises direct comparisons with discounters on price and quality. Price elasticity is mission-dependent: urgent trips show low elasticity, planned purchases remain highly elastic.

Digital expectations and omnichannel

Customers now expect mobile ordering, delivery, and frictionless payments, driving higher app engagement and deal-seeking through app-based promotions that increase price transparency. Ratings and social feedback magnify buyer voice, accelerating shifts in footfall and SKU demand. Seven & i’s integration of fintech services and loyalty into its ecosystem helps partially lock in users, modering but not eliminating customer bargaining power.

Urban density and location convenience

High urban density and over 21,000 Seven-Eleven stores in Japan (2024) lower travel costs and strengthen buyer choice; micro-market overlap drives demand for highly localized assortments. Convenience and late-night access reduce price sensitivity for urgent missions, while clear mission segmentation (quick grab vs planned shop) is essential to balance margin and retention.

- High density: >21,000 stores (Japan, 2024)

- Micro-markets: overlap raises local SKU tailoring

- Urgent missions: lower price elasticity due to convenience

- Segmentation: key to margin vs retention

Corporate and B2B micro-accounts

Corporate and B2B micro-accounts negotiate services across office supplies, logistics, catering and financial products; bundled solutions introduced in 2024 reduced churn and weakened buyer leverage. Large accounts still extract volume discounts and service SLAs, particularly for regional rollouts. Cross-selling between retail and financial arms in 2024 increased client stickiness and recurring revenue.

- Bundling lowers bargaining power

- Large accounts demand discounts/SLAs

- Cross-selling boosts retention (2024)

Japanese convenience shoppers gain leverage: >10T yen market, CPI ~3% raises price sensitivity

Customers wield strong bargaining power due to very low switching costs and dense competition; Japan convenience market >10 trillion yen (2024) and Seven‑Eleven Japan >21,000 stores raise buyer choice. CPI ~3.0% (2024) shifts demand to value/private‑label, increasing price sensitivity on planned trips. Digital apps and fintech loyalty raise transparency and retention, moderating but not nullifying customer leverage.

| Metric | Value (2024) |

|---|---|

| Seven‑Eleven Japan stores | >21,000 |

| Japan convenience market | >10 trillion yen |

| Japan CPI | ~3.0% |

What You See Is What You Get

Seven & I Holdings Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Seven & I Holdings Porter's Five Forces Analysis evaluates supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry, highlighting implications for convenience-store scale, private-label strategy, omnichannel competition, and regulatory risk. The file is fully formatted and ready for download and use the moment you buy.