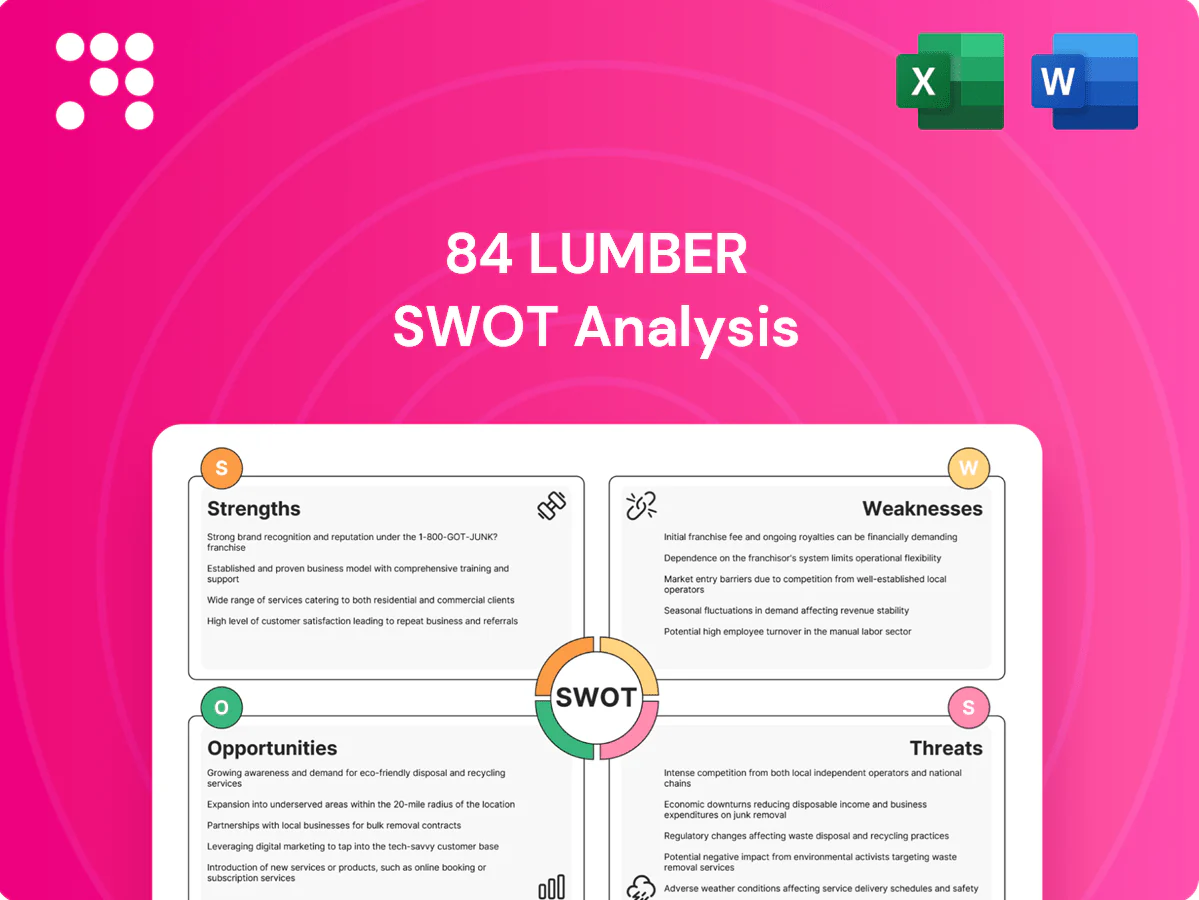

84 Lumber SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

84 Lumber's SWOT highlights a strong regional brand, integrated supply chain and construction tailwinds, offset by margin pressure, intense competition, and regulatory exposure. Our full SWOT unpacks market drivers, financial context, and strategic options with editable Word and Excel deliverables. Purchase the complete report to plan, pitch, or invest with confidence.

Strengths

National branch network

84 Lumber operates more than 250 locations across the U.S., enabling proximity to jobsites and faster fulfillment for builders and contractors. Localized inventories cut lead times and shipping costs by concentrating SKU availability regionally. Network density supports route optimization and consistent on-site service. Scale improves supplier leverage and national brand visibility.

Integrated components capacity

84 Lumber’s in-house truss, wall panel and millwork plants enable vertical integration and value-add through controlled quality and inventory. Offsite manufacturing—shown in industry studies to cut waste by ~30% and shorten cycle times 20–50%—improves yield and speed. Custom shops deliver tailored solutions for complex projects, differentiating 84 Lumber from pure commodity lumber sellers.

Pro-focused relationships

84 Lumber’s core customer base—professional builders and contractors—drives recurring demand, supported by the company’s network of more than 250 branches and dedicated account management teams. Dedicated credit programs and jobsite delivery deepen loyalty and raise effective switching costs by embedding operations into customers’ workflows. Knowledgeable staff and in-house takeoff and estimating services improve project accuracy and reduce procurement friction.

Broad product portfolio

84 Lumber’s broad product portfolio covers lumber, windows, doors, roofing, siding and millwork, enabling end-to-end supply for residential and commercial builds. One-stop solutions simplify procurement and on-site coordination, reducing vendor management complexity and shortening project timelines. A wide vendor base supports competitive pricing and product availability, while cross-selling increases wallet share per project.

- End-to-end product range

- Streamlined procurement

- Vendor diversity = better pricing

- Cross-selling boosts revenue per project

Operational agility, private

Privately held and family-owned since 1956, 84 Lumber leverages freedom from quarterly public-market pressures to make multi-year investments and act faster on strategic moves; lean governance enables quick local-market responses and regionally tailored assortments and service models, while cultural cohesion sustains a consistent customer experience.

- Founded: 1956

- Privately held — long-term decision-making

- 250+ locations — regional assortment

- Lean governance — faster execution

250+ locations and vertical integration enable pro-builder one-stop supply

84 Lumber operates 250+ locations (2024), enabling local fulfillment, lower shipping costs and route optimization. Vertical integration with in-house truss, wall-panel and millwork plants supports offsite manufacturing (industry: ~30% waste reduction; 20–50% faster cycles). Core professional-builder customer base, dedicated credit and jobsite delivery drive recurring demand and high switching costs. Broad product range enables one-stop procurement and cross-selling.

| Metric | Value |

|---|---|

| Founded | 1956 |

| Locations (2024) | 250+ |

| Ownership | Privately held |

| Offsite Mfg impact | ~30% waste ↓; 20–50% cycle time ↓ |

| Core customers | Professional builders/contractors |

What is included in the product

Delivers a strategic overview of 84 Lumber’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to map growth drivers, operational gaps, and market risks.

Provides a concise SWOT matrix tailored to 84 Lumber for fast, visual strategy alignment, helping relieve pain points around supply-chain resilience and competitive differentiation.

Weaknesses

Housing-cycle exposure

Revenue is tightly linked to residential starts and contractor activity, with single-family homes accounting for roughly 60% of U.S. starts; elevated mortgage rates (30-year fixed above ~6.5% since 2023) and consumer uncertainty can quickly damp demand. Fixed costs in branches and plants magnify volume swings, and diversification into counter-cyclical lines remains limited for 84 Lumber.

Commodity price volatility

Spot lumber and panel pricing is highly volatile—Random Lengths framing lumber peaked near $1,600/Mbf in 2021 and fell roughly 75% to below $400/Mbf by 2023, with OSB sliding ~60% from peak—creating material margin compression risk. Timing mismatches between procurement and selling can erase margins as monthly price swings often exceed 20%. Customers frequently delay purchases in falling markets, pressuring revenue. Hedging and strict pricing discipline are required but remain imperfect and costly.

Digital maturity gap

84 Lumber’s digital maturity gap shows as weaker e-commerce, real-time inventory visibility and pro portals compared with big-box rivals, which is notable for a retailer with over 250 locations and roughly 6,000 employees; industry B2B e-commerce penetration reached about 10% in 2024, raising competitive pressure. Manual quoting and takeoffs slow bid responsiveness versus automated competitors. Limited data integration impedes predictive demand planning and SKU optimization. Ongoing digital transformation demands capital-intensive investments in systems and talent.

Labor and skills intensity

Skilled drivers, truss assemblers, and yard staff are hard to recruit and retain, raising recruitment and training burdens; training and OSHA-driven safety requirements further lift operating costs. High turnover disrupts service quality and throughput, prolonging job cycles and increasing overtime. Tight labor markets push wages higher, squeezing margins on volume-sensitive building-supply operations.

- Recruitment difficulty — skilled drivers/truss assemblers/yard staff

- Higher operating costs — training and safety compliance

- Service risk — turnover reduces throughput and quality

- Margin pressure — tight labor markets increase wages

Geographic concentration risk

84 Lumber remains U.S.-centric with 250+ locations (2024), concentrating exposure to regional housing cycles. Local housing downturns or catastrophic weather can sharply reduce volumes in affected MSAs. Entering new MSAs requires material capital and multi-year ramp, and market share varies widely by region.

- 250+ locations (2024)

- High exposure to local housing/weather shocks

- Capital- and time-intensive MSA expansion

Revenue cyclical, high fixed costs and lumber volatility strain margins amid weak housing demand

Revenue highly cyclical—~60% exposure to single-family starts and 250+ locations (2024) concentrates risk; 30-year mortgage >6.5% since 2023 weakens demand.

Spot lumber volatility (framing lumber fell ~75% from 2021 peak to 2023) and procurement timing compress margins.

Digital gaps, labor shortages (~6,000 employees) and high fixed branch costs raise operating risk and capital needs.

| Metric | Value |

|---|---|

| Locations (2024) | 250+ |

| Employees | ~6,000 |

| Single-family exposure | ~60% |

| 30yr mortgage | >6.5% |

Same Document Delivered

84 Lumber SWOT Analysis

This is the actual 84 Lumber SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is not a sample but the real, editable analysis ready for download after checkout.

Elevate Your Analysis with the Complete SWOT Report

84 Lumber's SWOT highlights a strong regional brand, integrated supply chain and construction tailwinds, offset by margin pressure, intense competition, and regulatory exposure. Our full SWOT unpacks market drivers, financial context, and strategic options with editable Word and Excel deliverables. Purchase the complete report to plan, pitch, or invest with confidence.

Strengths

National branch network

84 Lumber operates more than 250 locations across the U.S., enabling proximity to jobsites and faster fulfillment for builders and contractors. Localized inventories cut lead times and shipping costs by concentrating SKU availability regionally. Network density supports route optimization and consistent on-site service. Scale improves supplier leverage and national brand visibility.

Integrated components capacity

84 Lumber’s in-house truss, wall panel and millwork plants enable vertical integration and value-add through controlled quality and inventory. Offsite manufacturing—shown in industry studies to cut waste by ~30% and shorten cycle times 20–50%—improves yield and speed. Custom shops deliver tailored solutions for complex projects, differentiating 84 Lumber from pure commodity lumber sellers.

Pro-focused relationships

84 Lumber’s core customer base—professional builders and contractors—drives recurring demand, supported by the company’s network of more than 250 branches and dedicated account management teams. Dedicated credit programs and jobsite delivery deepen loyalty and raise effective switching costs by embedding operations into customers’ workflows. Knowledgeable staff and in-house takeoff and estimating services improve project accuracy and reduce procurement friction.

Broad product portfolio

84 Lumber’s broad product portfolio covers lumber, windows, doors, roofing, siding and millwork, enabling end-to-end supply for residential and commercial builds. One-stop solutions simplify procurement and on-site coordination, reducing vendor management complexity and shortening project timelines. A wide vendor base supports competitive pricing and product availability, while cross-selling increases wallet share per project.

- End-to-end product range

- Streamlined procurement

- Vendor diversity = better pricing

- Cross-selling boosts revenue per project

Operational agility, private

Privately held and family-owned since 1956, 84 Lumber leverages freedom from quarterly public-market pressures to make multi-year investments and act faster on strategic moves; lean governance enables quick local-market responses and regionally tailored assortments and service models, while cultural cohesion sustains a consistent customer experience.

- Founded: 1956

- Privately held — long-term decision-making

- 250+ locations — regional assortment

- Lean governance — faster execution

250+ locations and vertical integration enable pro-builder one-stop supply

84 Lumber operates 250+ locations (2024), enabling local fulfillment, lower shipping costs and route optimization. Vertical integration with in-house truss, wall-panel and millwork plants supports offsite manufacturing (industry: ~30% waste reduction; 20–50% faster cycles). Core professional-builder customer base, dedicated credit and jobsite delivery drive recurring demand and high switching costs. Broad product range enables one-stop procurement and cross-selling.

| Metric | Value |

|---|---|

| Founded | 1956 |

| Locations (2024) | 250+ |

| Ownership | Privately held |

| Offsite Mfg impact | ~30% waste ↓; 20–50% cycle time ↓ |

| Core customers | Professional builders/contractors |

What is included in the product

Delivers a strategic overview of 84 Lumber’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to map growth drivers, operational gaps, and market risks.

Provides a concise SWOT matrix tailored to 84 Lumber for fast, visual strategy alignment, helping relieve pain points around supply-chain resilience and competitive differentiation.

Weaknesses

Housing-cycle exposure

Revenue is tightly linked to residential starts and contractor activity, with single-family homes accounting for roughly 60% of U.S. starts; elevated mortgage rates (30-year fixed above ~6.5% since 2023) and consumer uncertainty can quickly damp demand. Fixed costs in branches and plants magnify volume swings, and diversification into counter-cyclical lines remains limited for 84 Lumber.

Commodity price volatility

Spot lumber and panel pricing is highly volatile—Random Lengths framing lumber peaked near $1,600/Mbf in 2021 and fell roughly 75% to below $400/Mbf by 2023, with OSB sliding ~60% from peak—creating material margin compression risk. Timing mismatches between procurement and selling can erase margins as monthly price swings often exceed 20%. Customers frequently delay purchases in falling markets, pressuring revenue. Hedging and strict pricing discipline are required but remain imperfect and costly.

Digital maturity gap

84 Lumber’s digital maturity gap shows as weaker e-commerce, real-time inventory visibility and pro portals compared with big-box rivals, which is notable for a retailer with over 250 locations and roughly 6,000 employees; industry B2B e-commerce penetration reached about 10% in 2024, raising competitive pressure. Manual quoting and takeoffs slow bid responsiveness versus automated competitors. Limited data integration impedes predictive demand planning and SKU optimization. Ongoing digital transformation demands capital-intensive investments in systems and talent.

Labor and skills intensity

Skilled drivers, truss assemblers, and yard staff are hard to recruit and retain, raising recruitment and training burdens; training and OSHA-driven safety requirements further lift operating costs. High turnover disrupts service quality and throughput, prolonging job cycles and increasing overtime. Tight labor markets push wages higher, squeezing margins on volume-sensitive building-supply operations.

- Recruitment difficulty — skilled drivers/truss assemblers/yard staff

- Higher operating costs — training and safety compliance

- Service risk — turnover reduces throughput and quality

- Margin pressure — tight labor markets increase wages

Geographic concentration risk

84 Lumber remains U.S.-centric with 250+ locations (2024), concentrating exposure to regional housing cycles. Local housing downturns or catastrophic weather can sharply reduce volumes in affected MSAs. Entering new MSAs requires material capital and multi-year ramp, and market share varies widely by region.

- 250+ locations (2024)

- High exposure to local housing/weather shocks

- Capital- and time-intensive MSA expansion

Revenue cyclical, high fixed costs and lumber volatility strain margins amid weak housing demand

Revenue highly cyclical—~60% exposure to single-family starts and 250+ locations (2024) concentrates risk; 30-year mortgage >6.5% since 2023 weakens demand.

Spot lumber volatility (framing lumber fell ~75% from 2021 peak to 2023) and procurement timing compress margins.

Digital gaps, labor shortages (~6,000 employees) and high fixed branch costs raise operating risk and capital needs.

| Metric | Value |

|---|---|

| Locations (2024) | 250+ |

| Employees | ~6,000 |

| Single-family exposure | ~60% |

| 30yr mortgage | >6.5% |

Same Document Delivered

84 Lumber SWOT Analysis

This is the actual 84 Lumber SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is not a sample but the real, editable analysis ready for download after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

84 Lumber's SWOT highlights a strong regional brand, integrated supply chain and construction tailwinds, offset by margin pressure, intense competition, and regulatory exposure. Our full SWOT unpacks market drivers, financial context, and strategic options with editable Word and Excel deliverables. Purchase the complete report to plan, pitch, or invest with confidence.

Strengths

National branch network

84 Lumber operates more than 250 locations across the U.S., enabling proximity to jobsites and faster fulfillment for builders and contractors. Localized inventories cut lead times and shipping costs by concentrating SKU availability regionally. Network density supports route optimization and consistent on-site service. Scale improves supplier leverage and national brand visibility.

Integrated components capacity

84 Lumber’s in-house truss, wall panel and millwork plants enable vertical integration and value-add through controlled quality and inventory. Offsite manufacturing—shown in industry studies to cut waste by ~30% and shorten cycle times 20–50%—improves yield and speed. Custom shops deliver tailored solutions for complex projects, differentiating 84 Lumber from pure commodity lumber sellers.

Pro-focused relationships

84 Lumber’s core customer base—professional builders and contractors—drives recurring demand, supported by the company’s network of more than 250 branches and dedicated account management teams. Dedicated credit programs and jobsite delivery deepen loyalty and raise effective switching costs by embedding operations into customers’ workflows. Knowledgeable staff and in-house takeoff and estimating services improve project accuracy and reduce procurement friction.

Broad product portfolio

84 Lumber’s broad product portfolio covers lumber, windows, doors, roofing, siding and millwork, enabling end-to-end supply for residential and commercial builds. One-stop solutions simplify procurement and on-site coordination, reducing vendor management complexity and shortening project timelines. A wide vendor base supports competitive pricing and product availability, while cross-selling increases wallet share per project.

- End-to-end product range

- Streamlined procurement

- Vendor diversity = better pricing

- Cross-selling boosts revenue per project

Operational agility, private

Privately held and family-owned since 1956, 84 Lumber leverages freedom from quarterly public-market pressures to make multi-year investments and act faster on strategic moves; lean governance enables quick local-market responses and regionally tailored assortments and service models, while cultural cohesion sustains a consistent customer experience.

- Founded: 1956

- Privately held — long-term decision-making

- 250+ locations — regional assortment

- Lean governance — faster execution

250+ locations and vertical integration enable pro-builder one-stop supply

84 Lumber operates 250+ locations (2024), enabling local fulfillment, lower shipping costs and route optimization. Vertical integration with in-house truss, wall-panel and millwork plants supports offsite manufacturing (industry: ~30% waste reduction; 20–50% faster cycles). Core professional-builder customer base, dedicated credit and jobsite delivery drive recurring demand and high switching costs. Broad product range enables one-stop procurement and cross-selling.

| Metric | Value |

|---|---|

| Founded | 1956 |

| Locations (2024) | 250+ |

| Ownership | Privately held |

| Offsite Mfg impact | ~30% waste ↓; 20–50% cycle time ↓ |

| Core customers | Professional builders/contractors |

What is included in the product

Delivers a strategic overview of 84 Lumber’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to map growth drivers, operational gaps, and market risks.

Provides a concise SWOT matrix tailored to 84 Lumber for fast, visual strategy alignment, helping relieve pain points around supply-chain resilience and competitive differentiation.

Weaknesses

Housing-cycle exposure

Revenue is tightly linked to residential starts and contractor activity, with single-family homes accounting for roughly 60% of U.S. starts; elevated mortgage rates (30-year fixed above ~6.5% since 2023) and consumer uncertainty can quickly damp demand. Fixed costs in branches and plants magnify volume swings, and diversification into counter-cyclical lines remains limited for 84 Lumber.

Commodity price volatility

Spot lumber and panel pricing is highly volatile—Random Lengths framing lumber peaked near $1,600/Mbf in 2021 and fell roughly 75% to below $400/Mbf by 2023, with OSB sliding ~60% from peak—creating material margin compression risk. Timing mismatches between procurement and selling can erase margins as monthly price swings often exceed 20%. Customers frequently delay purchases in falling markets, pressuring revenue. Hedging and strict pricing discipline are required but remain imperfect and costly.

Digital maturity gap

84 Lumber’s digital maturity gap shows as weaker e-commerce, real-time inventory visibility and pro portals compared with big-box rivals, which is notable for a retailer with over 250 locations and roughly 6,000 employees; industry B2B e-commerce penetration reached about 10% in 2024, raising competitive pressure. Manual quoting and takeoffs slow bid responsiveness versus automated competitors. Limited data integration impedes predictive demand planning and SKU optimization. Ongoing digital transformation demands capital-intensive investments in systems and talent.

Labor and skills intensity

Skilled drivers, truss assemblers, and yard staff are hard to recruit and retain, raising recruitment and training burdens; training and OSHA-driven safety requirements further lift operating costs. High turnover disrupts service quality and throughput, prolonging job cycles and increasing overtime. Tight labor markets push wages higher, squeezing margins on volume-sensitive building-supply operations.

- Recruitment difficulty — skilled drivers/truss assemblers/yard staff

- Higher operating costs — training and safety compliance

- Service risk — turnover reduces throughput and quality

- Margin pressure — tight labor markets increase wages

Geographic concentration risk

84 Lumber remains U.S.-centric with 250+ locations (2024), concentrating exposure to regional housing cycles. Local housing downturns or catastrophic weather can sharply reduce volumes in affected MSAs. Entering new MSAs requires material capital and multi-year ramp, and market share varies widely by region.

- 250+ locations (2024)

- High exposure to local housing/weather shocks

- Capital- and time-intensive MSA expansion

Revenue cyclical, high fixed costs and lumber volatility strain margins amid weak housing demand

Revenue highly cyclical—~60% exposure to single-family starts and 250+ locations (2024) concentrates risk; 30-year mortgage >6.5% since 2023 weakens demand.

Spot lumber volatility (framing lumber fell ~75% from 2021 peak to 2023) and procurement timing compress margins.

Digital gaps, labor shortages (~6,000 employees) and high fixed branch costs raise operating risk and capital needs.

| Metric | Value |

|---|---|

| Locations (2024) | 250+ |

| Employees | ~6,000 |

| Single-family exposure | ~60% |

| 30yr mortgage | >6.5% |

Same Document Delivered

84 Lumber SWOT Analysis

This is the actual 84 Lumber SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is not a sample but the real, editable analysis ready for download after checkout.