Aareal Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Aareal Bank faces moderate buyer power, concentrated commercial real estate clients, regulatory tailwinds, and niche specialization that limit substitutes but keep threat of new entrants low; digital disruption raises operational pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aareal Bank’s competitive dynamics in detail.

Suppliers Bargaining Power

Wholesale funding dependency

As a specialized commercial real estate lender, Aareal in 2024 continued to depend heavily on wholesale markets, Pfandbrief issuance and institutional deposits for funding, concentrating exposure in a few counterparties and instruments. This concentration raises supplier pricing power in stress, with market volatility widening bond and repo spreads and tightening funding covenants. Central bank liquidity lines, such as ECB facilities available in 2024, partially offset that supplier leverage but do not eliminate higher market funding costs.

Capital adequacy and regulators

Regulators act as the supplier of permissible risk capacity for Aareal Bank: ECB Pillar 1 requires CET1 of 4.5% plus a 2.5% conservation buffer (7.0% minimum), while SREP add-ons and stress tests set institution‑specific uplifts that raise capital costs and loan pricing. Tightening rules increases the price of risk and reduces margin on leveraged CRE lending. Supervisory expectations limit product flexibility and capital allocation choices.

Core IT and data vendors

Core IT and data vendors exert strong bargaining power over Aareal Bank through specialised risk, treasury and compliance platforms that create vendor lock-in and high switching costs, driven by integration complexity and certification demands. Security and uptime SLAs in 2024 tightened pricing leverage for suppliers as ECB outsourcing guidance reinforced strict oversight. Multi-vendor strategies reduce but do not remove dependence.

Talent in structured real estate

Experienced originators, underwriters and workout specialists for structured real estate are scarce, pushing competitive hiring cycles that elevate compensation and retention costs and concentrate critical knowledge in few individuals, raising operational risk for Aareal Bank.

- Talent scarcity

- Higher pay/retention costs

- Concentration risk

- Employer brand mitigates leverage

Rating agencies and auditors

Rating agencies and auditors wield soft power over Aareal by shaping market access and funding costs through published credit opinions; methodological changes can abruptly reprice liabilities and wholesale spreads. Audit and model-validation obligations create recurring fixed costs and compliance overhead, while transparent governance and timely disclosure reduce asymmetry and strengthen negotiation positions with agencies and auditors.

- Agencies affect funding access

- Methodology shifts reprice liabilities

- Audit/validation = fixed compliance cost

- Transparent governance tempers asymmetry

Concentrated funding and Pfandbrief reliance raise repricing risk despite ECB 2024 backstop

Supplier power is elevated: concentrated wholesale funding and Pfandbrief reliance increase repricing risk in stress, ECB facilities in 2024 mitigate but do not remove spread sensitivity. Regulatory supply of risk capacity requires CET1 minimum 7.0% (4.5% Pillar 1 + 2.5% buffer) plus SREP add‑ons, raising capital costs. Specialized IT, talent and rating firms create lock‑in and fixed compliance expense, limiting flexibility.

| Metric | 2024 value |

|---|---|

| Regulatory CET1 minimum | 7.0% |

| ECB liquidity available | Yes (2024 facilities) |

What is included in the product

Tailored Porter's Five Forces analysis for Aareal Bank uncovering competitive drivers, customer and supplier influence, entry barriers and substitute threats; identifies disruptive trends and pricing pressures that shape profitability and market position, ready to incorporate into investor materials or strategy decks.

A clear one-sheet Porter's Five Forces for Aareal Bank—fast insight into competitive pressures and profitability levers to speed strategic decisions. Clean layout, editable force levels and radar visualization make it easy to tailor scenarios, copy into decks, or integrate with broader financial dashboards.

Customers Bargaining Power

Large sponsor negotiation

Top-tier real estate sponsors and funds extract better pricing and terms from Aareal, leveraging scale and repeat mandates to compress spreads and negotiate covenant-lite structures.

Their multi-bank relationships intensify auction dynamics, driving faster decision timelines and pricing competition that erodes lender margins.

Mandates increasingly hinge on speed and certainty, pressuring Aareal’s margins, while targeted cross-selling of banking and advisory services helps rebalance value capture.

Institutional investor demands

Institutional depositors and investors seek yield, liquidity and ESG alignment, and with global assets under management topping roughly $110 trillion in 2023 they can reallocate rapidly, impacting Aareal's funding mix and cost; ECB policy rates around 4% in mid‑2024 heightened sensitivity to yield. Transparent reporting and formal sustainable frameworks lower investor flight risk, while a diversified investor base reduces concentration vulnerability.

Software and platform clients

Property managers and corporates routinely benchmark Aareal’s platform against competing proptech suites, driving transparent price comparisons; enterprise SaaS renewal rates remain high (around 90%+ in 2024) which boosts renewal leverage at term. Deep integrations create switching frictions and migration costs, yet procurement-driven price pressure (often 10–20% concessions) persists. Continuous monthly/weekly feature delivery sustains customer stickiness and upsell potential.

Price transparency in CRE debt

Market comps, brokered deals and debt advisors have increased price visibility in CRE debt, narrowing information asymmetry and pressuring margins.

Tight spreads in benign cycles compress take rates as competing lenders match pricing; bespoke structuring and ancillary services help defend margins by creating fee income and differentiation.

Long-standing relationship lending still influences outcomes, with repeat borrowers often securing preferred pricing and terms.

- price visibility: market comps + brokered deals + advisors

- margin pressure: tight spreads compress take rates

- defense: bespoke structuring & ancillary services

- relationship lending: preferential pricing/terms

Global alternatives access

Clients increasingly access insurers (European insurers hold ~€10.6tn in investable assets), private debt (private debt AUM reached about $1.6tn in 2024) and CMBS markets, expanding alternatives to Aareal and raising buyer leverage; alternative lenders offer faster, flexible structures but at higher spreads, compressing Aareal’s pricing power especially in late-cycle repricing phases. Multi-product offers (loan + servicing + treasury) shift negotiations from pure price to bundled value.

- Insurers: €10.6tn (Europe, 2024)

- Private debt AUM: $1.6tn (2024)

- CMBS: growing share in CRE finance, raising competitive pressure

- Bundled solutions reduce pure price sensitivity

Speed and bundling compress spreads amid higher funding costs and stronger investor leverage

Large sponsors, insurers and private debt funds exert strong leverage on pricing and terms, accelerating auction dynamics and compressing Aareal’s spreads. Speed, certainty and bundled offers shift negotiations from price to service, while diversified investor pools (global AUM ~$110tn in 2023) and ECB rates (~4% mid‑2024) raise funding sensitivity.

| Metric | Value |

|---|---|

| Global AUM (2023) | $110tn |

| EU insurers (2024) | €10.6tn |

| Private debt AUM (2024) | $1.6tn |

| ECB rate (mid‑2024) | ~4% |

What You See Is What You Get

Aareal Bank Porter's Five Forces Analysis

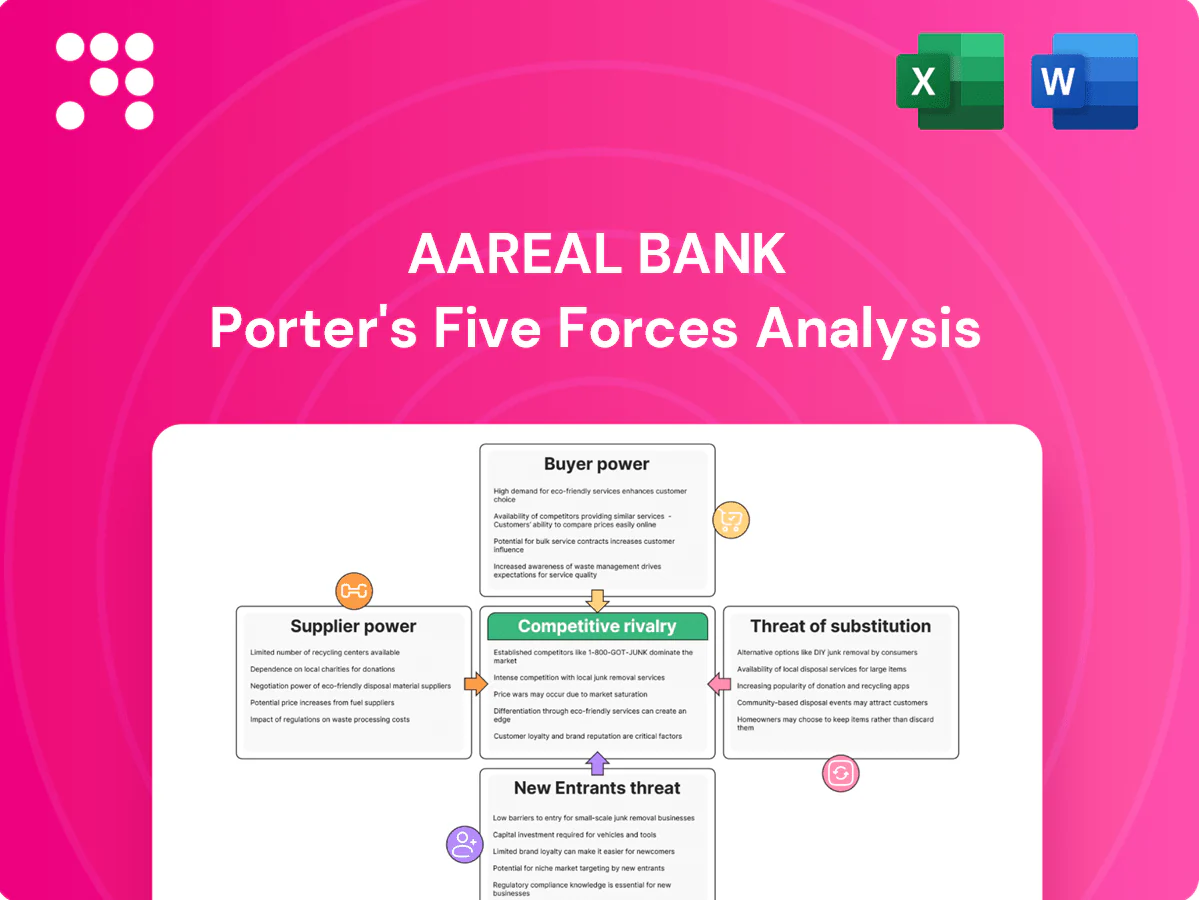

This preview shows the full Porter's Five Forces analysis of Aareal Bank—covering competitive rivalry, supplier and buyer power, and threats of substitutes and new entrants. The document displayed is the exact file you’ll receive instantly after purchase—fully formatted and ready to use. No placeholders, no excerpts—what you see is what you download.

A Must-Have Tool for Decision-Makers

Aareal Bank faces moderate buyer power, concentrated commercial real estate clients, regulatory tailwinds, and niche specialization that limit substitutes but keep threat of new entrants low; digital disruption raises operational pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aareal Bank’s competitive dynamics in detail.

Suppliers Bargaining Power

Wholesale funding dependency

As a specialized commercial real estate lender, Aareal in 2024 continued to depend heavily on wholesale markets, Pfandbrief issuance and institutional deposits for funding, concentrating exposure in a few counterparties and instruments. This concentration raises supplier pricing power in stress, with market volatility widening bond and repo spreads and tightening funding covenants. Central bank liquidity lines, such as ECB facilities available in 2024, partially offset that supplier leverage but do not eliminate higher market funding costs.

Capital adequacy and regulators

Regulators act as the supplier of permissible risk capacity for Aareal Bank: ECB Pillar 1 requires CET1 of 4.5% plus a 2.5% conservation buffer (7.0% minimum), while SREP add-ons and stress tests set institution‑specific uplifts that raise capital costs and loan pricing. Tightening rules increases the price of risk and reduces margin on leveraged CRE lending. Supervisory expectations limit product flexibility and capital allocation choices.

Core IT and data vendors

Core IT and data vendors exert strong bargaining power over Aareal Bank through specialised risk, treasury and compliance platforms that create vendor lock-in and high switching costs, driven by integration complexity and certification demands. Security and uptime SLAs in 2024 tightened pricing leverage for suppliers as ECB outsourcing guidance reinforced strict oversight. Multi-vendor strategies reduce but do not remove dependence.

Talent in structured real estate

Experienced originators, underwriters and workout specialists for structured real estate are scarce, pushing competitive hiring cycles that elevate compensation and retention costs and concentrate critical knowledge in few individuals, raising operational risk for Aareal Bank.

- Talent scarcity

- Higher pay/retention costs

- Concentration risk

- Employer brand mitigates leverage

Rating agencies and auditors

Rating agencies and auditors wield soft power over Aareal by shaping market access and funding costs through published credit opinions; methodological changes can abruptly reprice liabilities and wholesale spreads. Audit and model-validation obligations create recurring fixed costs and compliance overhead, while transparent governance and timely disclosure reduce asymmetry and strengthen negotiation positions with agencies and auditors.

- Agencies affect funding access

- Methodology shifts reprice liabilities

- Audit/validation = fixed compliance cost

- Transparent governance tempers asymmetry

Concentrated funding and Pfandbrief reliance raise repricing risk despite ECB 2024 backstop

Supplier power is elevated: concentrated wholesale funding and Pfandbrief reliance increase repricing risk in stress, ECB facilities in 2024 mitigate but do not remove spread sensitivity. Regulatory supply of risk capacity requires CET1 minimum 7.0% (4.5% Pillar 1 + 2.5% buffer) plus SREP add‑ons, raising capital costs. Specialized IT, talent and rating firms create lock‑in and fixed compliance expense, limiting flexibility.

| Metric | 2024 value |

|---|---|

| Regulatory CET1 minimum | 7.0% |

| ECB liquidity available | Yes (2024 facilities) |

What is included in the product

Tailored Porter's Five Forces analysis for Aareal Bank uncovering competitive drivers, customer and supplier influence, entry barriers and substitute threats; identifies disruptive trends and pricing pressures that shape profitability and market position, ready to incorporate into investor materials or strategy decks.

A clear one-sheet Porter's Five Forces for Aareal Bank—fast insight into competitive pressures and profitability levers to speed strategic decisions. Clean layout, editable force levels and radar visualization make it easy to tailor scenarios, copy into decks, or integrate with broader financial dashboards.

Customers Bargaining Power

Large sponsor negotiation

Top-tier real estate sponsors and funds extract better pricing and terms from Aareal, leveraging scale and repeat mandates to compress spreads and negotiate covenant-lite structures.

Their multi-bank relationships intensify auction dynamics, driving faster decision timelines and pricing competition that erodes lender margins.

Mandates increasingly hinge on speed and certainty, pressuring Aareal’s margins, while targeted cross-selling of banking and advisory services helps rebalance value capture.

Institutional investor demands

Institutional depositors and investors seek yield, liquidity and ESG alignment, and with global assets under management topping roughly $110 trillion in 2023 they can reallocate rapidly, impacting Aareal's funding mix and cost; ECB policy rates around 4% in mid‑2024 heightened sensitivity to yield. Transparent reporting and formal sustainable frameworks lower investor flight risk, while a diversified investor base reduces concentration vulnerability.

Software and platform clients

Property managers and corporates routinely benchmark Aareal’s platform against competing proptech suites, driving transparent price comparisons; enterprise SaaS renewal rates remain high (around 90%+ in 2024) which boosts renewal leverage at term. Deep integrations create switching frictions and migration costs, yet procurement-driven price pressure (often 10–20% concessions) persists. Continuous monthly/weekly feature delivery sustains customer stickiness and upsell potential.

Price transparency in CRE debt

Market comps, brokered deals and debt advisors have increased price visibility in CRE debt, narrowing information asymmetry and pressuring margins.

Tight spreads in benign cycles compress take rates as competing lenders match pricing; bespoke structuring and ancillary services help defend margins by creating fee income and differentiation.

Long-standing relationship lending still influences outcomes, with repeat borrowers often securing preferred pricing and terms.

- price visibility: market comps + brokered deals + advisors

- margin pressure: tight spreads compress take rates

- defense: bespoke structuring & ancillary services

- relationship lending: preferential pricing/terms

Global alternatives access

Clients increasingly access insurers (European insurers hold ~€10.6tn in investable assets), private debt (private debt AUM reached about $1.6tn in 2024) and CMBS markets, expanding alternatives to Aareal and raising buyer leverage; alternative lenders offer faster, flexible structures but at higher spreads, compressing Aareal’s pricing power especially in late-cycle repricing phases. Multi-product offers (loan + servicing + treasury) shift negotiations from pure price to bundled value.

- Insurers: €10.6tn (Europe, 2024)

- Private debt AUM: $1.6tn (2024)

- CMBS: growing share in CRE finance, raising competitive pressure

- Bundled solutions reduce pure price sensitivity

Speed and bundling compress spreads amid higher funding costs and stronger investor leverage

Large sponsors, insurers and private debt funds exert strong leverage on pricing and terms, accelerating auction dynamics and compressing Aareal’s spreads. Speed, certainty and bundled offers shift negotiations from price to service, while diversified investor pools (global AUM ~$110tn in 2023) and ECB rates (~4% mid‑2024) raise funding sensitivity.

| Metric | Value |

|---|---|

| Global AUM (2023) | $110tn |

| EU insurers (2024) | €10.6tn |

| Private debt AUM (2024) | $1.6tn |

| ECB rate (mid‑2024) | ~4% |

What You See Is What You Get

Aareal Bank Porter's Five Forces Analysis

This preview shows the full Porter's Five Forces analysis of Aareal Bank—covering competitive rivalry, supplier and buyer power, and threats of substitutes and new entrants. The document displayed is the exact file you’ll receive instantly after purchase—fully formatted and ready to use. No placeholders, no excerpts—what you see is what you download.

Description

A Must-Have Tool for Decision-Makers

Aareal Bank faces moderate buyer power, concentrated commercial real estate clients, regulatory tailwinds, and niche specialization that limit substitutes but keep threat of new entrants low; digital disruption raises operational pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aareal Bank’s competitive dynamics in detail.

Suppliers Bargaining Power

Wholesale funding dependency

As a specialized commercial real estate lender, Aareal in 2024 continued to depend heavily on wholesale markets, Pfandbrief issuance and institutional deposits for funding, concentrating exposure in a few counterparties and instruments. This concentration raises supplier pricing power in stress, with market volatility widening bond and repo spreads and tightening funding covenants. Central bank liquidity lines, such as ECB facilities available in 2024, partially offset that supplier leverage but do not eliminate higher market funding costs.

Capital adequacy and regulators

Regulators act as the supplier of permissible risk capacity for Aareal Bank: ECB Pillar 1 requires CET1 of 4.5% plus a 2.5% conservation buffer (7.0% minimum), while SREP add-ons and stress tests set institution‑specific uplifts that raise capital costs and loan pricing. Tightening rules increases the price of risk and reduces margin on leveraged CRE lending. Supervisory expectations limit product flexibility and capital allocation choices.

Core IT and data vendors

Core IT and data vendors exert strong bargaining power over Aareal Bank through specialised risk, treasury and compliance platforms that create vendor lock-in and high switching costs, driven by integration complexity and certification demands. Security and uptime SLAs in 2024 tightened pricing leverage for suppliers as ECB outsourcing guidance reinforced strict oversight. Multi-vendor strategies reduce but do not remove dependence.

Talent in structured real estate

Experienced originators, underwriters and workout specialists for structured real estate are scarce, pushing competitive hiring cycles that elevate compensation and retention costs and concentrate critical knowledge in few individuals, raising operational risk for Aareal Bank.

- Talent scarcity

- Higher pay/retention costs

- Concentration risk

- Employer brand mitigates leverage

Rating agencies and auditors

Rating agencies and auditors wield soft power over Aareal by shaping market access and funding costs through published credit opinions; methodological changes can abruptly reprice liabilities and wholesale spreads. Audit and model-validation obligations create recurring fixed costs and compliance overhead, while transparent governance and timely disclosure reduce asymmetry and strengthen negotiation positions with agencies and auditors.

- Agencies affect funding access

- Methodology shifts reprice liabilities

- Audit/validation = fixed compliance cost

- Transparent governance tempers asymmetry

Concentrated funding and Pfandbrief reliance raise repricing risk despite ECB 2024 backstop

Supplier power is elevated: concentrated wholesale funding and Pfandbrief reliance increase repricing risk in stress, ECB facilities in 2024 mitigate but do not remove spread sensitivity. Regulatory supply of risk capacity requires CET1 minimum 7.0% (4.5% Pillar 1 + 2.5% buffer) plus SREP add‑ons, raising capital costs. Specialized IT, talent and rating firms create lock‑in and fixed compliance expense, limiting flexibility.

| Metric | 2024 value |

|---|---|

| Regulatory CET1 minimum | 7.0% |

| ECB liquidity available | Yes (2024 facilities) |

What is included in the product

Tailored Porter's Five Forces analysis for Aareal Bank uncovering competitive drivers, customer and supplier influence, entry barriers and substitute threats; identifies disruptive trends and pricing pressures that shape profitability and market position, ready to incorporate into investor materials or strategy decks.

A clear one-sheet Porter's Five Forces for Aareal Bank—fast insight into competitive pressures and profitability levers to speed strategic decisions. Clean layout, editable force levels and radar visualization make it easy to tailor scenarios, copy into decks, or integrate with broader financial dashboards.

Customers Bargaining Power

Large sponsor negotiation

Top-tier real estate sponsors and funds extract better pricing and terms from Aareal, leveraging scale and repeat mandates to compress spreads and negotiate covenant-lite structures.

Their multi-bank relationships intensify auction dynamics, driving faster decision timelines and pricing competition that erodes lender margins.

Mandates increasingly hinge on speed and certainty, pressuring Aareal’s margins, while targeted cross-selling of banking and advisory services helps rebalance value capture.

Institutional investor demands

Institutional depositors and investors seek yield, liquidity and ESG alignment, and with global assets under management topping roughly $110 trillion in 2023 they can reallocate rapidly, impacting Aareal's funding mix and cost; ECB policy rates around 4% in mid‑2024 heightened sensitivity to yield. Transparent reporting and formal sustainable frameworks lower investor flight risk, while a diversified investor base reduces concentration vulnerability.

Software and platform clients

Property managers and corporates routinely benchmark Aareal’s platform against competing proptech suites, driving transparent price comparisons; enterprise SaaS renewal rates remain high (around 90%+ in 2024) which boosts renewal leverage at term. Deep integrations create switching frictions and migration costs, yet procurement-driven price pressure (often 10–20% concessions) persists. Continuous monthly/weekly feature delivery sustains customer stickiness and upsell potential.

Price transparency in CRE debt

Market comps, brokered deals and debt advisors have increased price visibility in CRE debt, narrowing information asymmetry and pressuring margins.

Tight spreads in benign cycles compress take rates as competing lenders match pricing; bespoke structuring and ancillary services help defend margins by creating fee income and differentiation.

Long-standing relationship lending still influences outcomes, with repeat borrowers often securing preferred pricing and terms.

- price visibility: market comps + brokered deals + advisors

- margin pressure: tight spreads compress take rates

- defense: bespoke structuring & ancillary services

- relationship lending: preferential pricing/terms

Global alternatives access

Clients increasingly access insurers (European insurers hold ~€10.6tn in investable assets), private debt (private debt AUM reached about $1.6tn in 2024) and CMBS markets, expanding alternatives to Aareal and raising buyer leverage; alternative lenders offer faster, flexible structures but at higher spreads, compressing Aareal’s pricing power especially in late-cycle repricing phases. Multi-product offers (loan + servicing + treasury) shift negotiations from pure price to bundled value.

- Insurers: €10.6tn (Europe, 2024)

- Private debt AUM: $1.6tn (2024)

- CMBS: growing share in CRE finance, raising competitive pressure

- Bundled solutions reduce pure price sensitivity

Speed and bundling compress spreads amid higher funding costs and stronger investor leverage

Large sponsors, insurers and private debt funds exert strong leverage on pricing and terms, accelerating auction dynamics and compressing Aareal’s spreads. Speed, certainty and bundled offers shift negotiations from price to service, while diversified investor pools (global AUM ~$110tn in 2023) and ECB rates (~4% mid‑2024) raise funding sensitivity.

| Metric | Value |

|---|---|

| Global AUM (2023) | $110tn |

| EU insurers (2024) | €10.6tn |

| Private debt AUM (2024) | $1.6tn |

| ECB rate (mid‑2024) | ~4% |

What You See Is What You Get

Aareal Bank Porter's Five Forces Analysis

This preview shows the full Porter's Five Forces analysis of Aareal Bank—covering competitive rivalry, supplier and buyer power, and threats of substitutes and new entrants. The document displayed is the exact file you’ll receive instantly after purchase—fully formatted and ready to use. No placeholders, no excerpts—what you see is what you download.