Abbott Laboratories Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

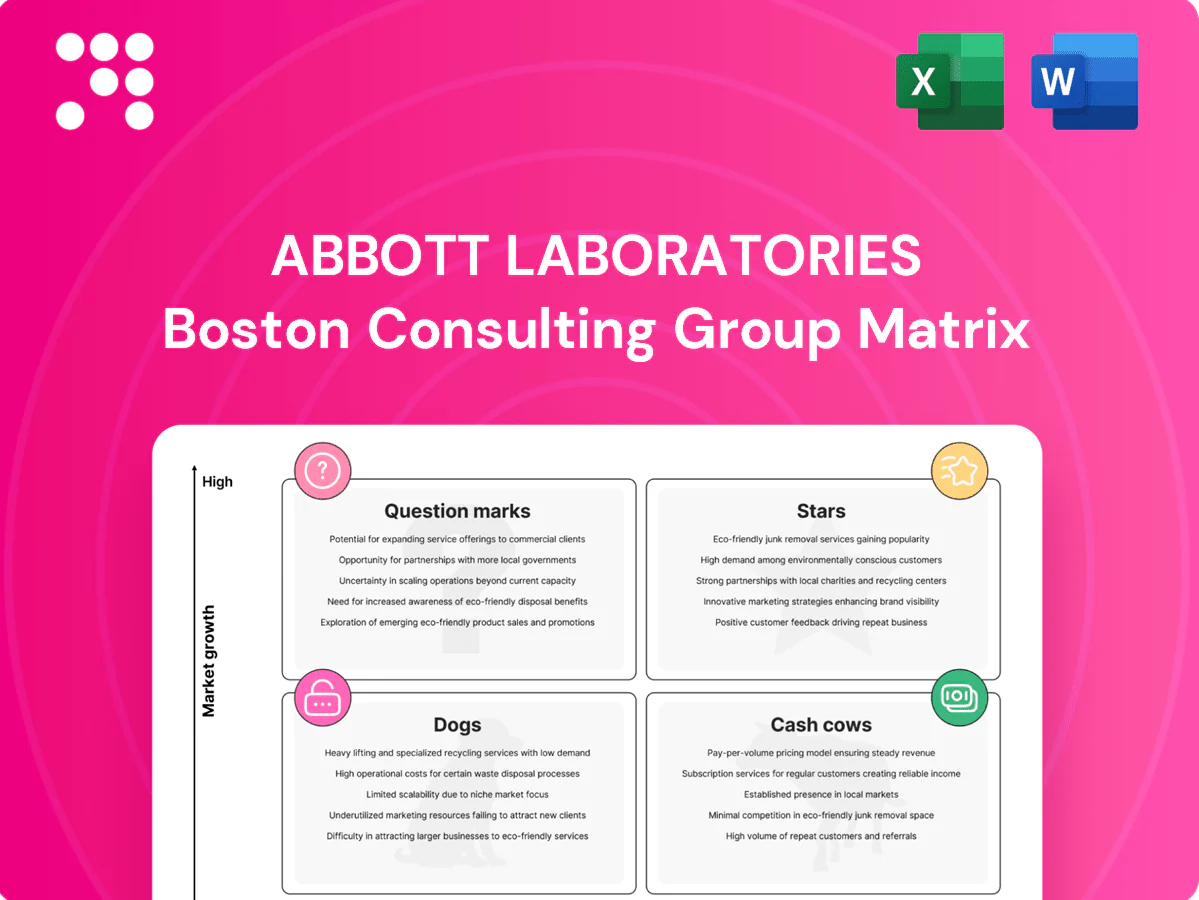

Abbott Laboratories’ BCG Matrix snapshot shows where flagship diagnostics and nutrition products sit—some are clear Stars driving growth, others steady Cash Cows funding R&D, and a few niche lines that need a rethink. Want the whole picture with quadrant-by-quadrant placements, revenue shares, and action-ready moves? Purchase the full BCG Matrix for a detailed Word report plus an Excel summary—insights you can present, decide on, and act on fast.

Stars

FreeStyle Libre CGM

FreeStyle Libre is the global leader in CGM with roughly 6 million users by 2024 and dominates a CGM market estimated near $10 billion in 2024, showing rapid adoption. High-growth diabetes demand plus strong share and continuous product iteration keep the growth flywheel spinning. Continued heavy investment in sensors, software and reimbursement expansion is required. If Abbott holds share, Libre can mature into a large cash-generating franchise.

Alinity lab diagnostics

Alinity lab diagnostics sits in BCG Stars: integrated Alinity platforms offer sticky placements and a rising test menu (over 100 assays by 2024), driving hospital lock‑in via high throughput and consistent cross‑analyte workflows. Growth remains robust as labs standardize; continue investing in installed base, connectivity, and menu breadth to sustain momentum.

Structural heart (e.g., MitraClip/TriClip)

Transcatheter mitral/tricuspid repair is scaling fast as populations age—UN data show the 65+ share rising from about 9% in 2020 toward ~16% by 2050—driving procedure demand. Abbott’s MitraClip/TriClip is the market-leading platform with strong clinician loyalty, supported by pivotal trials such as COAPT. Training, registries and access programs require sustained funding to protect share and convert this growing category into a long-term annuity.

Rapid diagnostics (ID NOW, Panbio)

Rapid diagnostics ID NOW and Panbio sit as Stars: point-of-care molecular and antigen platforms have shifted from episodic COVID use to embedded workflows across respiratory, STI, and urgent care settings, driving high utilization and recurring test revenue that fuels momentum; Abbott continues expanding menus and partnering with decentralized care networks to broaden adoption.

- Embedded POCT expansion

- Respiratory, STI, urgent care growth

- High utilization + recurring revenue

- Menu expansion & decentralized partnerships

Cardiac rhythm management/heart failure monitoring

Cardiac rhythm management and heart-failure monitoring are Stars for Abbott, driven by connected devices with peer-reviewed clinical data such as the CHAMPION trial showing a 37 percent reduction in HF hospitalizations with pulmonary artery pressure monitoring and growing payer demand for reduced admissions and cleaner remote data workflows.

The category continues expanding with digital overlays and telemonitoring; sustaining R&D spend and tighter ecosystem integrations is critical to protect share as providers and payers push value-based outcomes.

- Clinical impact: CHAMPION trial 37% HF hospitalization reduction

- Payer focus: lower admissions, cleaner real-world data

- Market trend: expanding digital overlays and remote workflows

- Strategic priority: sustain R&D and ecosystem integrations

6M CGM users, $10B market; 100+ assays, mitral clips and HF monitoring need investment

Abbott Stars: FreeStyle Libre—~6M users by 2024, CGM market ≈$10B (2024); Alinity—>100 assays by 2024 driving lab lock‑in; MitraClip/TriClip scaling with aging populations and COAPT-backed clinical momentum; ID NOW/Panbio and CRM/HF monitoring (CHAMPION: 37% HF hospitalization reduction) require sustained investment to convert growth into long-term cash flow.

| Asset | 2024 KPI | Strategic Need |

|---|---|---|

| Libre | 6M users; $10B CGM | R&D, reimbursement |

| Alinity | 100+ assays | Installed base |

What is included in the product

Comprehensive BCG analysis of Abbott's product units, identifying Stars, Cash Cows, Question Marks, Dogs and strategic moves.

One-page Abbott BCG Matrix placing each business unit in a quadrant to quickly spot underperformers and growth opportunities.

Cash Cows

Ensure & Pediasure nutrition

Household brands Ensure and Pediasure deliver scale with dominant shelf presence and loyal prescribers, forming Abbott’s multibillion-dollar nutrition franchise; combined annual sales exceeded US$3bn in 2024. They operate in mature categories with steady volumes and reliable margins, supporting predictable cash flow. Incremental promotional spend remains low versus historical sunk brand equity. Optimize manufacturing footprint and portfolio mix to sustain cash generation.

Core blood screening

Core blood screening benefits from a large installed base and multiyear service contracts that drive predictable reagent pull-through; Abbott participates in the $87 billion global in vitro diagnostics market (2024). Market growth is stable with incremental innovation; service uptime and maintenance, not headline launches, drive renewal behavior in institutional labs. Focus on milking efficiencies while preserving gold-standard reliability and uptime.

Point-of-care glucose meters (legacy)

Abbott’s legacy point-of-care glucose meters are mass-distributed in 120+ countries with entrenched channels outside the U.S., delivering a profitable installed base even as growth is low-single-digit annually. Minimal marketing is required; emphasis is on price and supply discipline to protect margins (~20% operating on legacy devices). Harvest cash flows here while CGM (FreeStyle Libre) captures growth.

Established pharmaceuticals (branded generics, EM)

Established pharmaceuticals (branded generics, EM) deliver durable demand across a diverse emerging-markets portfolio; 2024 saw mid-single-digit revenue growth but high cash conversion, with cash conversion >25% and operating margins north of 20% in core EM franchises. Local brands and integrated supply chains keep churn low, so Abbott prioritizes operational excellence and selective SKU pruning to protect cash flow.

- EM diversification

- Low growth, high cash conversion (>25% in 2024)

- Local brands/supply chains = low churn

- Focus: operational excellence & SKU pruning

Vascular closure & mature coronary devices

Vascular closure and mature coronary devices are Abbott cash cows: trusted, widely used tools with strong clinician familiarity and baked-in hospital purchasing; market growth in 2024 is modest while margins remain healthy due to recurring disposables and service contracts. Innovation is incremental and capital-light, letting Abbott use scale to compress costs and defend pricing.

- Trusted tools

- Wide clinician familiarity

- Baked-in purchasing

- Modest market expansion (2024)

- High margins, capital-light innovation

- Scale to squeeze costs & stabilize pricing

Diversified health: nutrition >US$3bn, IVD pull-through in US$87bn market, legacy margins ~20%

Household nutrition (Ensure/Pediasure) >US$3bn sales (2024) with stable margins and low promo spend. Core blood screening in a US$87bn IVD market (2024) yields predictable reagent pull-through. Legacy glucose meters (~120+ countries) and EM pharmaceuticals deliver high cash conversion (>25% in 2024) and margins ~20% on legacy devices.

| Segment | 2024 Sales | Margins | Cash Conv. |

|---|---|---|---|

| Nutrition | >US$3bn | Stable | High |

| IVD | — (US$87bn market) | Predictable | Stable |

| Legacy devices/EM pharma | Regional | ~20% | >25% |

Full Transparency, Always

Abbott Laboratories BCG Matrix

The file you're previewing is the exact Abbott Laboratories BCG Matrix report you'll receive after purchase. No watermarks or demo content—just a fully formatted, analysis-ready document built for strategic clarity. Once bought, the full file is immediately downloadable and editable for presentations, planning, or board packs. Designed by strategy professionals, it’s ready to slot into your workflow with no surprises.

Visual. Strategic. Downloadable.

Abbott Laboratories’ BCG Matrix snapshot shows where flagship diagnostics and nutrition products sit—some are clear Stars driving growth, others steady Cash Cows funding R&D, and a few niche lines that need a rethink. Want the whole picture with quadrant-by-quadrant placements, revenue shares, and action-ready moves? Purchase the full BCG Matrix for a detailed Word report plus an Excel summary—insights you can present, decide on, and act on fast.

Stars

FreeStyle Libre CGM

FreeStyle Libre is the global leader in CGM with roughly 6 million users by 2024 and dominates a CGM market estimated near $10 billion in 2024, showing rapid adoption. High-growth diabetes demand plus strong share and continuous product iteration keep the growth flywheel spinning. Continued heavy investment in sensors, software and reimbursement expansion is required. If Abbott holds share, Libre can mature into a large cash-generating franchise.

Alinity lab diagnostics

Alinity lab diagnostics sits in BCG Stars: integrated Alinity platforms offer sticky placements and a rising test menu (over 100 assays by 2024), driving hospital lock‑in via high throughput and consistent cross‑analyte workflows. Growth remains robust as labs standardize; continue investing in installed base, connectivity, and menu breadth to sustain momentum.

Structural heart (e.g., MitraClip/TriClip)

Transcatheter mitral/tricuspid repair is scaling fast as populations age—UN data show the 65+ share rising from about 9% in 2020 toward ~16% by 2050—driving procedure demand. Abbott’s MitraClip/TriClip is the market-leading platform with strong clinician loyalty, supported by pivotal trials such as COAPT. Training, registries and access programs require sustained funding to protect share and convert this growing category into a long-term annuity.

Rapid diagnostics (ID NOW, Panbio)

Rapid diagnostics ID NOW and Panbio sit as Stars: point-of-care molecular and antigen platforms have shifted from episodic COVID use to embedded workflows across respiratory, STI, and urgent care settings, driving high utilization and recurring test revenue that fuels momentum; Abbott continues expanding menus and partnering with decentralized care networks to broaden adoption.

- Embedded POCT expansion

- Respiratory, STI, urgent care growth

- High utilization + recurring revenue

- Menu expansion & decentralized partnerships

Cardiac rhythm management/heart failure monitoring

Cardiac rhythm management and heart-failure monitoring are Stars for Abbott, driven by connected devices with peer-reviewed clinical data such as the CHAMPION trial showing a 37 percent reduction in HF hospitalizations with pulmonary artery pressure monitoring and growing payer demand for reduced admissions and cleaner remote data workflows.

The category continues expanding with digital overlays and telemonitoring; sustaining R&D spend and tighter ecosystem integrations is critical to protect share as providers and payers push value-based outcomes.

- Clinical impact: CHAMPION trial 37% HF hospitalization reduction

- Payer focus: lower admissions, cleaner real-world data

- Market trend: expanding digital overlays and remote workflows

- Strategic priority: sustain R&D and ecosystem integrations

6M CGM users, $10B market; 100+ assays, mitral clips and HF monitoring need investment

Abbott Stars: FreeStyle Libre—~6M users by 2024, CGM market ≈$10B (2024); Alinity—>100 assays by 2024 driving lab lock‑in; MitraClip/TriClip scaling with aging populations and COAPT-backed clinical momentum; ID NOW/Panbio and CRM/HF monitoring (CHAMPION: 37% HF hospitalization reduction) require sustained investment to convert growth into long-term cash flow.

| Asset | 2024 KPI | Strategic Need |

|---|---|---|

| Libre | 6M users; $10B CGM | R&D, reimbursement |

| Alinity | 100+ assays | Installed base |

What is included in the product

Comprehensive BCG analysis of Abbott's product units, identifying Stars, Cash Cows, Question Marks, Dogs and strategic moves.

One-page Abbott BCG Matrix placing each business unit in a quadrant to quickly spot underperformers and growth opportunities.

Cash Cows

Ensure & Pediasure nutrition

Household brands Ensure and Pediasure deliver scale with dominant shelf presence and loyal prescribers, forming Abbott’s multibillion-dollar nutrition franchise; combined annual sales exceeded US$3bn in 2024. They operate in mature categories with steady volumes and reliable margins, supporting predictable cash flow. Incremental promotional spend remains low versus historical sunk brand equity. Optimize manufacturing footprint and portfolio mix to sustain cash generation.

Core blood screening

Core blood screening benefits from a large installed base and multiyear service contracts that drive predictable reagent pull-through; Abbott participates in the $87 billion global in vitro diagnostics market (2024). Market growth is stable with incremental innovation; service uptime and maintenance, not headline launches, drive renewal behavior in institutional labs. Focus on milking efficiencies while preserving gold-standard reliability and uptime.

Point-of-care glucose meters (legacy)

Abbott’s legacy point-of-care glucose meters are mass-distributed in 120+ countries with entrenched channels outside the U.S., delivering a profitable installed base even as growth is low-single-digit annually. Minimal marketing is required; emphasis is on price and supply discipline to protect margins (~20% operating on legacy devices). Harvest cash flows here while CGM (FreeStyle Libre) captures growth.

Established pharmaceuticals (branded generics, EM)

Established pharmaceuticals (branded generics, EM) deliver durable demand across a diverse emerging-markets portfolio; 2024 saw mid-single-digit revenue growth but high cash conversion, with cash conversion >25% and operating margins north of 20% in core EM franchises. Local brands and integrated supply chains keep churn low, so Abbott prioritizes operational excellence and selective SKU pruning to protect cash flow.

- EM diversification

- Low growth, high cash conversion (>25% in 2024)

- Local brands/supply chains = low churn

- Focus: operational excellence & SKU pruning

Vascular closure & mature coronary devices

Vascular closure and mature coronary devices are Abbott cash cows: trusted, widely used tools with strong clinician familiarity and baked-in hospital purchasing; market growth in 2024 is modest while margins remain healthy due to recurring disposables and service contracts. Innovation is incremental and capital-light, letting Abbott use scale to compress costs and defend pricing.

- Trusted tools

- Wide clinician familiarity

- Baked-in purchasing

- Modest market expansion (2024)

- High margins, capital-light innovation

- Scale to squeeze costs & stabilize pricing

Diversified health: nutrition >US$3bn, IVD pull-through in US$87bn market, legacy margins ~20%

Household nutrition (Ensure/Pediasure) >US$3bn sales (2024) with stable margins and low promo spend. Core blood screening in a US$87bn IVD market (2024) yields predictable reagent pull-through. Legacy glucose meters (~120+ countries) and EM pharmaceuticals deliver high cash conversion (>25% in 2024) and margins ~20% on legacy devices.

| Segment | 2024 Sales | Margins | Cash Conv. |

|---|---|---|---|

| Nutrition | >US$3bn | Stable | High |

| IVD | — (US$87bn market) | Predictable | Stable |

| Legacy devices/EM pharma | Regional | ~20% | >25% |

Full Transparency, Always

Abbott Laboratories BCG Matrix

The file you're previewing is the exact Abbott Laboratories BCG Matrix report you'll receive after purchase. No watermarks or demo content—just a fully formatted, analysis-ready document built for strategic clarity. Once bought, the full file is immediately downloadable and editable for presentations, planning, or board packs. Designed by strategy professionals, it’s ready to slot into your workflow with no surprises.

Description

Visual. Strategic. Downloadable.

Abbott Laboratories’ BCG Matrix snapshot shows where flagship diagnostics and nutrition products sit—some are clear Stars driving growth, others steady Cash Cows funding R&D, and a few niche lines that need a rethink. Want the whole picture with quadrant-by-quadrant placements, revenue shares, and action-ready moves? Purchase the full BCG Matrix for a detailed Word report plus an Excel summary—insights you can present, decide on, and act on fast.

Stars

FreeStyle Libre CGM

FreeStyle Libre is the global leader in CGM with roughly 6 million users by 2024 and dominates a CGM market estimated near $10 billion in 2024, showing rapid adoption. High-growth diabetes demand plus strong share and continuous product iteration keep the growth flywheel spinning. Continued heavy investment in sensors, software and reimbursement expansion is required. If Abbott holds share, Libre can mature into a large cash-generating franchise.

Alinity lab diagnostics

Alinity lab diagnostics sits in BCG Stars: integrated Alinity platforms offer sticky placements and a rising test menu (over 100 assays by 2024), driving hospital lock‑in via high throughput and consistent cross‑analyte workflows. Growth remains robust as labs standardize; continue investing in installed base, connectivity, and menu breadth to sustain momentum.

Structural heart (e.g., MitraClip/TriClip)

Transcatheter mitral/tricuspid repair is scaling fast as populations age—UN data show the 65+ share rising from about 9% in 2020 toward ~16% by 2050—driving procedure demand. Abbott’s MitraClip/TriClip is the market-leading platform with strong clinician loyalty, supported by pivotal trials such as COAPT. Training, registries and access programs require sustained funding to protect share and convert this growing category into a long-term annuity.

Rapid diagnostics (ID NOW, Panbio)

Rapid diagnostics ID NOW and Panbio sit as Stars: point-of-care molecular and antigen platforms have shifted from episodic COVID use to embedded workflows across respiratory, STI, and urgent care settings, driving high utilization and recurring test revenue that fuels momentum; Abbott continues expanding menus and partnering with decentralized care networks to broaden adoption.

- Embedded POCT expansion

- Respiratory, STI, urgent care growth

- High utilization + recurring revenue

- Menu expansion & decentralized partnerships

Cardiac rhythm management/heart failure monitoring

Cardiac rhythm management and heart-failure monitoring are Stars for Abbott, driven by connected devices with peer-reviewed clinical data such as the CHAMPION trial showing a 37 percent reduction in HF hospitalizations with pulmonary artery pressure monitoring and growing payer demand for reduced admissions and cleaner remote data workflows.

The category continues expanding with digital overlays and telemonitoring; sustaining R&D spend and tighter ecosystem integrations is critical to protect share as providers and payers push value-based outcomes.

- Clinical impact: CHAMPION trial 37% HF hospitalization reduction

- Payer focus: lower admissions, cleaner real-world data

- Market trend: expanding digital overlays and remote workflows

- Strategic priority: sustain R&D and ecosystem integrations

6M CGM users, $10B market; 100+ assays, mitral clips and HF monitoring need investment

Abbott Stars: FreeStyle Libre—~6M users by 2024, CGM market ≈$10B (2024); Alinity—>100 assays by 2024 driving lab lock‑in; MitraClip/TriClip scaling with aging populations and COAPT-backed clinical momentum; ID NOW/Panbio and CRM/HF monitoring (CHAMPION: 37% HF hospitalization reduction) require sustained investment to convert growth into long-term cash flow.

| Asset | 2024 KPI | Strategic Need |

|---|---|---|

| Libre | 6M users; $10B CGM | R&D, reimbursement |

| Alinity | 100+ assays | Installed base |

What is included in the product

Comprehensive BCG analysis of Abbott's product units, identifying Stars, Cash Cows, Question Marks, Dogs and strategic moves.

One-page Abbott BCG Matrix placing each business unit in a quadrant to quickly spot underperformers and growth opportunities.

Cash Cows

Ensure & Pediasure nutrition

Household brands Ensure and Pediasure deliver scale with dominant shelf presence and loyal prescribers, forming Abbott’s multibillion-dollar nutrition franchise; combined annual sales exceeded US$3bn in 2024. They operate in mature categories with steady volumes and reliable margins, supporting predictable cash flow. Incremental promotional spend remains low versus historical sunk brand equity. Optimize manufacturing footprint and portfolio mix to sustain cash generation.

Core blood screening

Core blood screening benefits from a large installed base and multiyear service contracts that drive predictable reagent pull-through; Abbott participates in the $87 billion global in vitro diagnostics market (2024). Market growth is stable with incremental innovation; service uptime and maintenance, not headline launches, drive renewal behavior in institutional labs. Focus on milking efficiencies while preserving gold-standard reliability and uptime.

Point-of-care glucose meters (legacy)

Abbott’s legacy point-of-care glucose meters are mass-distributed in 120+ countries with entrenched channels outside the U.S., delivering a profitable installed base even as growth is low-single-digit annually. Minimal marketing is required; emphasis is on price and supply discipline to protect margins (~20% operating on legacy devices). Harvest cash flows here while CGM (FreeStyle Libre) captures growth.

Established pharmaceuticals (branded generics, EM)

Established pharmaceuticals (branded generics, EM) deliver durable demand across a diverse emerging-markets portfolio; 2024 saw mid-single-digit revenue growth but high cash conversion, with cash conversion >25% and operating margins north of 20% in core EM franchises. Local brands and integrated supply chains keep churn low, so Abbott prioritizes operational excellence and selective SKU pruning to protect cash flow.

- EM diversification

- Low growth, high cash conversion (>25% in 2024)

- Local brands/supply chains = low churn

- Focus: operational excellence & SKU pruning

Vascular closure & mature coronary devices

Vascular closure and mature coronary devices are Abbott cash cows: trusted, widely used tools with strong clinician familiarity and baked-in hospital purchasing; market growth in 2024 is modest while margins remain healthy due to recurring disposables and service contracts. Innovation is incremental and capital-light, letting Abbott use scale to compress costs and defend pricing.

- Trusted tools

- Wide clinician familiarity

- Baked-in purchasing

- Modest market expansion (2024)

- High margins, capital-light innovation

- Scale to squeeze costs & stabilize pricing

Diversified health: nutrition >US$3bn, IVD pull-through in US$87bn market, legacy margins ~20%

Household nutrition (Ensure/Pediasure) >US$3bn sales (2024) with stable margins and low promo spend. Core blood screening in a US$87bn IVD market (2024) yields predictable reagent pull-through. Legacy glucose meters (~120+ countries) and EM pharmaceuticals deliver high cash conversion (>25% in 2024) and margins ~20% on legacy devices.

| Segment | 2024 Sales | Margins | Cash Conv. |

|---|---|---|---|

| Nutrition | >US$3bn | Stable | High |

| IVD | — (US$87bn market) | Predictable | Stable |

| Legacy devices/EM pharma | Regional | ~20% | >25% |

Full Transparency, Always

Abbott Laboratories BCG Matrix

The file you're previewing is the exact Abbott Laboratories BCG Matrix report you'll receive after purchase. No watermarks or demo content—just a fully formatted, analysis-ready document built for strategic clarity. Once bought, the full file is immediately downloadable and editable for presentations, planning, or board packs. Designed by strategy professionals, it’s ready to slot into your workflow with no surprises.