Abercrombie & Fitch Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

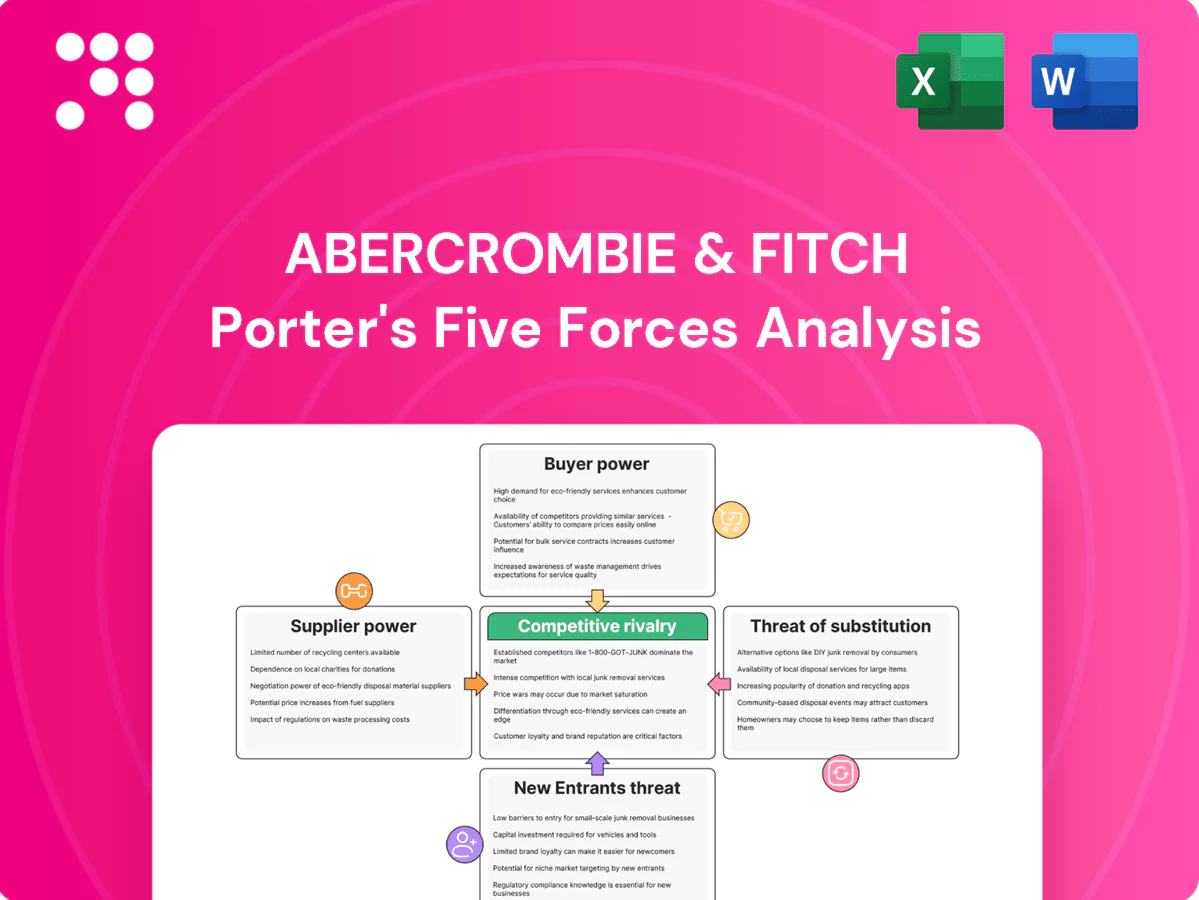

Abercrombie & Fitch faces intense retail rivalry, shifting buyer preferences toward value and digital channels, moderate supplier leverage, and a rising threat from fast-fashion substitutes that pressure margins. Brand equity offers resilience but requires strategic agility. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and actionable insights.

Suppliers Bargaining Power

Diversified sourcing base

Abercrombie & Fitch sources finished goods from a broad network of third‑party manufacturers in Asia, Europe and the Americas (2024 Form 10‑K), reducing single‑supplier dependence and moderating individual supplier leverage. Regional disruptions can still cascade through supplier clusters, so multi‑sourcing and dual‑vendor strategies preserve negotiating flexibility.

Commodity cost exposure

Inputs such as cotton, dyes and energy are volatile, occasionally strengthening supplier bargaining power and pressuring Abercrombie & Fitch margins; cost spikes have forced periodic price adjustments. Hedging and fabric substitution strategies reduce but do not eliminate exposure, while multi-year supplier agreements can stabilize input pricing at the expense of sourcing flexibility.

Quality, compliance, and ESG requirements

Stringent labor and sustainability standards narrow Abercrombie & Fitch’s approved vendor pool, increasing leverage for compliant suppliers and raising input bargaining power.

Auditing, traceability, and certifications create switching friction and higher onboarding costs for alternatives.

Forced exits of non‑compliant vendors can temporarily compress production capacity and lead times.

Preferred supplier programs tie assured volume to compliance—supporting supply continuity for a company with $3.56B net sales in fiscal 2023.

Lead times and design complexity

Suppliers' bargaining power rises as 2024 fashion cycles and capsule drops force Abercrombie & Fitch to rely on agile makers; shorter lead times and smaller batches let capable vendors command premiums. Nearshoring and strict calendar discipline in 2024 have reduced reliance on long‑lead suppliers, while vendor‑managed sampling and PLM systems compress development timelines.

- Agility = premium

- Shorter lead times ↑ bargaining

- Nearshoring reduces risk

- PLM/sampling compress timelines

Logistics and capacity constraints

Port congestion, volatile freight rates, and capacity shortages shift bargaining toward logistics partners and factory groups; peak-season prioritization favors higher-volume buyers and raises landed costs, and A&F’s scale typically secures allocation but can be undermined by sudden chokepoints.

- Peak-season leverage: favors large buyers

- Cost impact: higher freight and surcharges

- Risk mitigation: multi-port and blended air/ocean

Global apparel sourcing balances supplier leverage amid input volatility; nearshoring eases pressure

Abercrombie & Fitch sources finished goods from a broad network across Asia, Europe and the Americas (2024 Form 10‑K), limiting single‑supplier risk but keeping supplier leverage during regional disruption. Volatile inputs (cotton, dyes, freight) and compliance requirements elevate supplier bargaining power, while nearshoring, preferred‑supplier programs and A&F scale partially mitigate pricing pressure.

| Metric | Value |

|---|---|

| Net sales (FY2023) | $3.56B |

| Supplier regions | Asia/Europe/Americas (2024 10‑K) |

| 2024 trend | Nearshoring ↑, agility premiums |

What is included in the product

Tailored Porter's Five Forces analysis for Abercrombie & Fitch uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitutes, highlighting disruptive threats and strategic levers for pricing, positioning, and growth.

A concise, one-sheet Porter's Five Forces for Abercrombie & Fitch—instantly reveal supplier, buyer, rivalry and entrant pressures with customizable scores and a radar chart, ready to drop into pitch decks or boardroom slides for faster strategic decisions.

Customers Bargaining Power

Price-sensitive youth segments

Hollister and Abercrombie concentrate on teens and young adults, cohorts with high price elasticity that react strongly to promotions; Abercrombie & Fitch Co. reported roughly $3.7 billion in net sales in FY2023, underscoring scale where pricing drives traffic. Frequent markdowns and promotions materially influence conversion and amplify buyer power in downturns. Tiered pricing and value basics (offering lower-priced essentials) help preserve store traffic without broadly diluting the premium image.

Low switching costs

Low switching costs let consumers move easily to rivals with similar aesthetics, intensifying pressure on Abercrombie & Fitch, which reported fiscal 2024 net sales of about $4.7 billion. Ubiquitous online options and comparison tools—ecommerce accounting for roughly one‑third of apparel sales in 2024—increase buyer price sensitivity. Minimal contractual lock‑in elevates buyer leverage. Abercrombie’s focus on differentiated fits and fabric quality seeks to raise perceived switching costs.

Omnichannel expectations

Shoppers now expect seamless store, app and web experiences with fast fulfillment and easy returns—McKinsey 2024 found about 75% of consumers prefer retailers offering unified omnichannel service—failure on convenience quickly drives churn and raises customer bargaining power. Operational bar empowers buyers to demand more for less; investments in OMS, BOPIS and flexible returns reduce that leverage.

Influence of reviews and social media

User content now rapidly shapes Abercrombie & Fitchs momentum and sell-through; 79% of consumers say online reviews influence purchases, so viral trends can reprice demand overnight and force markdowns or premiuming within days. This collective voice raises customer bargaining power by rewarding perceived value or punishing missteps, while always-on creative plus influencer seeding help stabilize demand and recover sell-through.

- Reviews drive purchase intent: 79% trust online reviews

- Viral trends can shift pricing and sell-through within days

- Collective voice increases leverage on promotions and assortment

- Continuous influencer seeding mitigates sudden drops

Loyalty and personalization

Loyalty programs and curated recommendations increase stickiness for Abercrombie & Fitch by converting casual buyers into repeat customers, softening buyer bargaining power. First-party data from memberships and app interactions enables targeted offers rather than blanket promotions, raising relevance and lowering effective price sensitivity. However, inconsistent personalization or frequent broad discounts can train shoppers to wait for sales, eroding this advantage.

- Rewards programs boost retention

- First-party data -> targeted offers

- Higher relevance reduces price sensitivity

- Poor execution retrains discount-seeking

Price-sensitive youth, promotions and low switching costs boost bargaining power

Young, price‑sensitive core customers give high bargaining power; A&F net sales ~$4.7B FY2024 and frequent promotions drive traffic. Low switching costs and ~33% apparel ecommerce share in 2024 raise price sensitivity. Loyalty and first‑party data temper but don't eliminate leverage.

| Metric | Value |

|---|---|

| FY2024 net sales | $4.7B |

| Ecommerce share 2024 | ~33% |

Preview Before You Purchase

Abercrombie & Fitch Porter's Five Forces Analysis

This preview is the exact Abercrombie & Fitch Porter’s Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready to use. It contains the full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. No samples or placeholders: buy and download this same file instantly.

A Must-Have Tool for Decision-Makers

Abercrombie & Fitch faces intense retail rivalry, shifting buyer preferences toward value and digital channels, moderate supplier leverage, and a rising threat from fast-fashion substitutes that pressure margins. Brand equity offers resilience but requires strategic agility. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and actionable insights.

Suppliers Bargaining Power

Diversified sourcing base

Abercrombie & Fitch sources finished goods from a broad network of third‑party manufacturers in Asia, Europe and the Americas (2024 Form 10‑K), reducing single‑supplier dependence and moderating individual supplier leverage. Regional disruptions can still cascade through supplier clusters, so multi‑sourcing and dual‑vendor strategies preserve negotiating flexibility.

Commodity cost exposure

Inputs such as cotton, dyes and energy are volatile, occasionally strengthening supplier bargaining power and pressuring Abercrombie & Fitch margins; cost spikes have forced periodic price adjustments. Hedging and fabric substitution strategies reduce but do not eliminate exposure, while multi-year supplier agreements can stabilize input pricing at the expense of sourcing flexibility.

Quality, compliance, and ESG requirements

Stringent labor and sustainability standards narrow Abercrombie & Fitch’s approved vendor pool, increasing leverage for compliant suppliers and raising input bargaining power.

Auditing, traceability, and certifications create switching friction and higher onboarding costs for alternatives.

Forced exits of non‑compliant vendors can temporarily compress production capacity and lead times.

Preferred supplier programs tie assured volume to compliance—supporting supply continuity for a company with $3.56B net sales in fiscal 2023.

Lead times and design complexity

Suppliers' bargaining power rises as 2024 fashion cycles and capsule drops force Abercrombie & Fitch to rely on agile makers; shorter lead times and smaller batches let capable vendors command premiums. Nearshoring and strict calendar discipline in 2024 have reduced reliance on long‑lead suppliers, while vendor‑managed sampling and PLM systems compress development timelines.

- Agility = premium

- Shorter lead times ↑ bargaining

- Nearshoring reduces risk

- PLM/sampling compress timelines

Logistics and capacity constraints

Port congestion, volatile freight rates, and capacity shortages shift bargaining toward logistics partners and factory groups; peak-season prioritization favors higher-volume buyers and raises landed costs, and A&F’s scale typically secures allocation but can be undermined by sudden chokepoints.

- Peak-season leverage: favors large buyers

- Cost impact: higher freight and surcharges

- Risk mitigation: multi-port and blended air/ocean

Global apparel sourcing balances supplier leverage amid input volatility; nearshoring eases pressure

Abercrombie & Fitch sources finished goods from a broad network across Asia, Europe and the Americas (2024 Form 10‑K), limiting single‑supplier risk but keeping supplier leverage during regional disruption. Volatile inputs (cotton, dyes, freight) and compliance requirements elevate supplier bargaining power, while nearshoring, preferred‑supplier programs and A&F scale partially mitigate pricing pressure.

| Metric | Value |

|---|---|

| Net sales (FY2023) | $3.56B |

| Supplier regions | Asia/Europe/Americas (2024 10‑K) |

| 2024 trend | Nearshoring ↑, agility premiums |

What is included in the product

Tailored Porter's Five Forces analysis for Abercrombie & Fitch uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitutes, highlighting disruptive threats and strategic levers for pricing, positioning, and growth.

A concise, one-sheet Porter's Five Forces for Abercrombie & Fitch—instantly reveal supplier, buyer, rivalry and entrant pressures with customizable scores and a radar chart, ready to drop into pitch decks or boardroom slides for faster strategic decisions.

Customers Bargaining Power

Price-sensitive youth segments

Hollister and Abercrombie concentrate on teens and young adults, cohorts with high price elasticity that react strongly to promotions; Abercrombie & Fitch Co. reported roughly $3.7 billion in net sales in FY2023, underscoring scale where pricing drives traffic. Frequent markdowns and promotions materially influence conversion and amplify buyer power in downturns. Tiered pricing and value basics (offering lower-priced essentials) help preserve store traffic without broadly diluting the premium image.

Low switching costs

Low switching costs let consumers move easily to rivals with similar aesthetics, intensifying pressure on Abercrombie & Fitch, which reported fiscal 2024 net sales of about $4.7 billion. Ubiquitous online options and comparison tools—ecommerce accounting for roughly one‑third of apparel sales in 2024—increase buyer price sensitivity. Minimal contractual lock‑in elevates buyer leverage. Abercrombie’s focus on differentiated fits and fabric quality seeks to raise perceived switching costs.

Omnichannel expectations

Shoppers now expect seamless store, app and web experiences with fast fulfillment and easy returns—McKinsey 2024 found about 75% of consumers prefer retailers offering unified omnichannel service—failure on convenience quickly drives churn and raises customer bargaining power. Operational bar empowers buyers to demand more for less; investments in OMS, BOPIS and flexible returns reduce that leverage.

Influence of reviews and social media

User content now rapidly shapes Abercrombie & Fitchs momentum and sell-through; 79% of consumers say online reviews influence purchases, so viral trends can reprice demand overnight and force markdowns or premiuming within days. This collective voice raises customer bargaining power by rewarding perceived value or punishing missteps, while always-on creative plus influencer seeding help stabilize demand and recover sell-through.

- Reviews drive purchase intent: 79% trust online reviews

- Viral trends can shift pricing and sell-through within days

- Collective voice increases leverage on promotions and assortment

- Continuous influencer seeding mitigates sudden drops

Loyalty and personalization

Loyalty programs and curated recommendations increase stickiness for Abercrombie & Fitch by converting casual buyers into repeat customers, softening buyer bargaining power. First-party data from memberships and app interactions enables targeted offers rather than blanket promotions, raising relevance and lowering effective price sensitivity. However, inconsistent personalization or frequent broad discounts can train shoppers to wait for sales, eroding this advantage.

- Rewards programs boost retention

- First-party data -> targeted offers

- Higher relevance reduces price sensitivity

- Poor execution retrains discount-seeking

Price-sensitive youth, promotions and low switching costs boost bargaining power

Young, price‑sensitive core customers give high bargaining power; A&F net sales ~$4.7B FY2024 and frequent promotions drive traffic. Low switching costs and ~33% apparel ecommerce share in 2024 raise price sensitivity. Loyalty and first‑party data temper but don't eliminate leverage.

| Metric | Value |

|---|---|

| FY2024 net sales | $4.7B |

| Ecommerce share 2024 | ~33% |

Preview Before You Purchase

Abercrombie & Fitch Porter's Five Forces Analysis

This preview is the exact Abercrombie & Fitch Porter’s Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready to use. It contains the full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. No samples or placeholders: buy and download this same file instantly.

Description

A Must-Have Tool for Decision-Makers

Abercrombie & Fitch faces intense retail rivalry, shifting buyer preferences toward value and digital channels, moderate supplier leverage, and a rising threat from fast-fashion substitutes that pressure margins. Brand equity offers resilience but requires strategic agility. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and actionable insights.

Suppliers Bargaining Power

Diversified sourcing base

Abercrombie & Fitch sources finished goods from a broad network of third‑party manufacturers in Asia, Europe and the Americas (2024 Form 10‑K), reducing single‑supplier dependence and moderating individual supplier leverage. Regional disruptions can still cascade through supplier clusters, so multi‑sourcing and dual‑vendor strategies preserve negotiating flexibility.

Commodity cost exposure

Inputs such as cotton, dyes and energy are volatile, occasionally strengthening supplier bargaining power and pressuring Abercrombie & Fitch margins; cost spikes have forced periodic price adjustments. Hedging and fabric substitution strategies reduce but do not eliminate exposure, while multi-year supplier agreements can stabilize input pricing at the expense of sourcing flexibility.

Quality, compliance, and ESG requirements

Stringent labor and sustainability standards narrow Abercrombie & Fitch’s approved vendor pool, increasing leverage for compliant suppliers and raising input bargaining power.

Auditing, traceability, and certifications create switching friction and higher onboarding costs for alternatives.

Forced exits of non‑compliant vendors can temporarily compress production capacity and lead times.

Preferred supplier programs tie assured volume to compliance—supporting supply continuity for a company with $3.56B net sales in fiscal 2023.

Lead times and design complexity

Suppliers' bargaining power rises as 2024 fashion cycles and capsule drops force Abercrombie & Fitch to rely on agile makers; shorter lead times and smaller batches let capable vendors command premiums. Nearshoring and strict calendar discipline in 2024 have reduced reliance on long‑lead suppliers, while vendor‑managed sampling and PLM systems compress development timelines.

- Agility = premium

- Shorter lead times ↑ bargaining

- Nearshoring reduces risk

- PLM/sampling compress timelines

Logistics and capacity constraints

Port congestion, volatile freight rates, and capacity shortages shift bargaining toward logistics partners and factory groups; peak-season prioritization favors higher-volume buyers and raises landed costs, and A&F’s scale typically secures allocation but can be undermined by sudden chokepoints.

- Peak-season leverage: favors large buyers

- Cost impact: higher freight and surcharges

- Risk mitigation: multi-port and blended air/ocean

Global apparel sourcing balances supplier leverage amid input volatility; nearshoring eases pressure

Abercrombie & Fitch sources finished goods from a broad network across Asia, Europe and the Americas (2024 Form 10‑K), limiting single‑supplier risk but keeping supplier leverage during regional disruption. Volatile inputs (cotton, dyes, freight) and compliance requirements elevate supplier bargaining power, while nearshoring, preferred‑supplier programs and A&F scale partially mitigate pricing pressure.

| Metric | Value |

|---|---|

| Net sales (FY2023) | $3.56B |

| Supplier regions | Asia/Europe/Americas (2024 10‑K) |

| 2024 trend | Nearshoring ↑, agility premiums |

What is included in the product

Tailored Porter's Five Forces analysis for Abercrombie & Fitch uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitutes, highlighting disruptive threats and strategic levers for pricing, positioning, and growth.

A concise, one-sheet Porter's Five Forces for Abercrombie & Fitch—instantly reveal supplier, buyer, rivalry and entrant pressures with customizable scores and a radar chart, ready to drop into pitch decks or boardroom slides for faster strategic decisions.

Customers Bargaining Power

Price-sensitive youth segments

Hollister and Abercrombie concentrate on teens and young adults, cohorts with high price elasticity that react strongly to promotions; Abercrombie & Fitch Co. reported roughly $3.7 billion in net sales in FY2023, underscoring scale where pricing drives traffic. Frequent markdowns and promotions materially influence conversion and amplify buyer power in downturns. Tiered pricing and value basics (offering lower-priced essentials) help preserve store traffic without broadly diluting the premium image.

Low switching costs

Low switching costs let consumers move easily to rivals with similar aesthetics, intensifying pressure on Abercrombie & Fitch, which reported fiscal 2024 net sales of about $4.7 billion. Ubiquitous online options and comparison tools—ecommerce accounting for roughly one‑third of apparel sales in 2024—increase buyer price sensitivity. Minimal contractual lock‑in elevates buyer leverage. Abercrombie’s focus on differentiated fits and fabric quality seeks to raise perceived switching costs.

Omnichannel expectations

Shoppers now expect seamless store, app and web experiences with fast fulfillment and easy returns—McKinsey 2024 found about 75% of consumers prefer retailers offering unified omnichannel service—failure on convenience quickly drives churn and raises customer bargaining power. Operational bar empowers buyers to demand more for less; investments in OMS, BOPIS and flexible returns reduce that leverage.

Influence of reviews and social media

User content now rapidly shapes Abercrombie & Fitchs momentum and sell-through; 79% of consumers say online reviews influence purchases, so viral trends can reprice demand overnight and force markdowns or premiuming within days. This collective voice raises customer bargaining power by rewarding perceived value or punishing missteps, while always-on creative plus influencer seeding help stabilize demand and recover sell-through.

- Reviews drive purchase intent: 79% trust online reviews

- Viral trends can shift pricing and sell-through within days

- Collective voice increases leverage on promotions and assortment

- Continuous influencer seeding mitigates sudden drops

Loyalty and personalization

Loyalty programs and curated recommendations increase stickiness for Abercrombie & Fitch by converting casual buyers into repeat customers, softening buyer bargaining power. First-party data from memberships and app interactions enables targeted offers rather than blanket promotions, raising relevance and lowering effective price sensitivity. However, inconsistent personalization or frequent broad discounts can train shoppers to wait for sales, eroding this advantage.

- Rewards programs boost retention

- First-party data -> targeted offers

- Higher relevance reduces price sensitivity

- Poor execution retrains discount-seeking

Price-sensitive youth, promotions and low switching costs boost bargaining power

Young, price‑sensitive core customers give high bargaining power; A&F net sales ~$4.7B FY2024 and frequent promotions drive traffic. Low switching costs and ~33% apparel ecommerce share in 2024 raise price sensitivity. Loyalty and first‑party data temper but don't eliminate leverage.

| Metric | Value |

|---|---|

| FY2024 net sales | $4.7B |

| Ecommerce share 2024 | ~33% |

Preview Before You Purchase

Abercrombie & Fitch Porter's Five Forces Analysis

This preview is the exact Abercrombie & Fitch Porter’s Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready to use. It contains the full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications. No samples or placeholders: buy and download this same file instantly.