abrdn Porter's Five Forces Analysis

From Overview to Strategy Blueprint

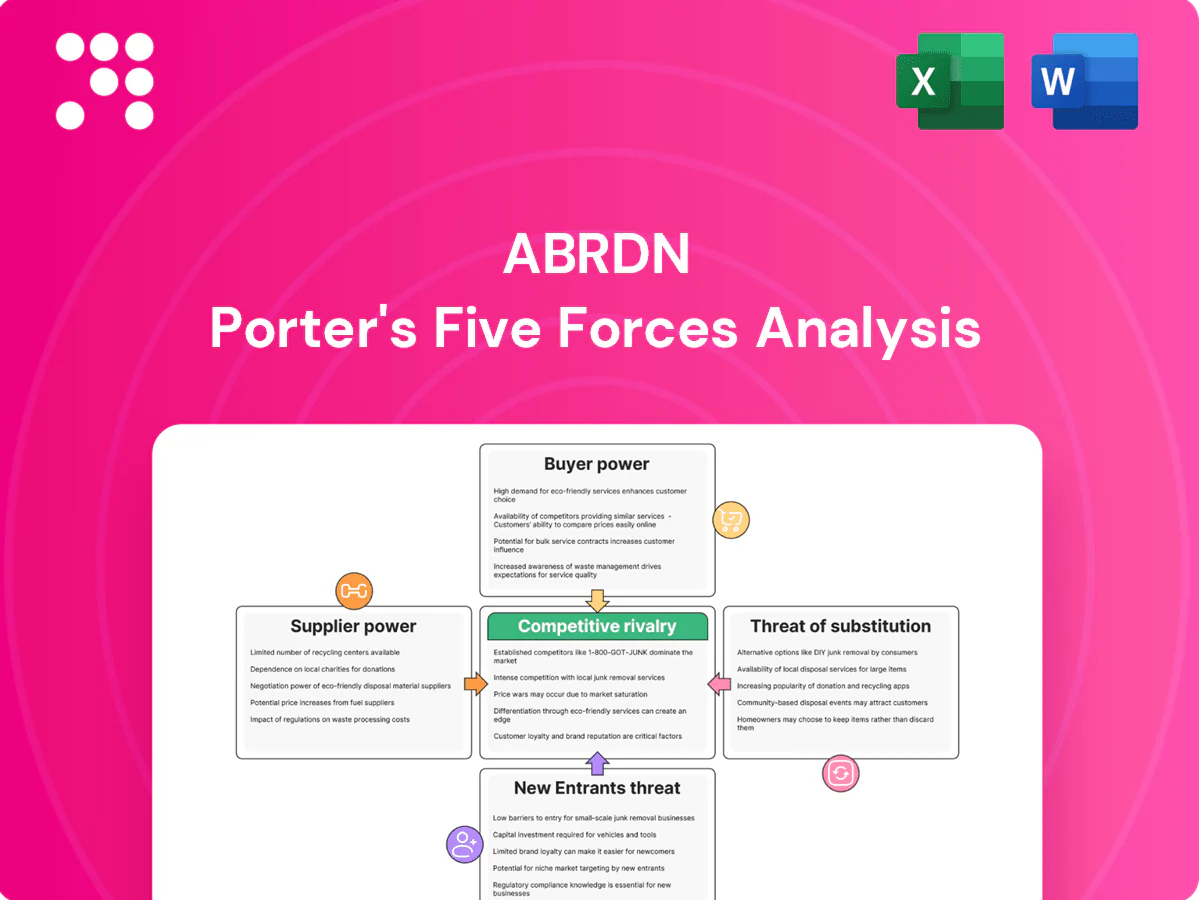

Abrdn faces moderate buyer power, concentrated institutional clients, fee pressure and digital disruption that intensify competition; supplier relationships and regulatory scrutiny further shape strategic options. This snapshot highlights key tensions but scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Dependence on talent and star PMs

Portfolio managers, analysts and distribution leaders are scarce, credentialed suppliers whose mobility drives wage inflation; abrdn reported c.£360bn AUM in 2024, so loss of star PMs can risk meaningful fee revenue and client redemptions. abrdn must offer competitive pay, culture and clear career paths to retain alpha-generators and limit mandate churn. Long-term incentives and team-based investment processes reduce concentration risk by aligning pay and distributing client relationships.

Concentrated market data and index vendors

Essential inputs from Bloomberg (Terminal ~USD24,000/yr), Refinitiv (Eikon ~USD22,000/yr), MSCI and FTSE Russell give vendors clear pricing power with few substitutes and entrenched workflows. Rising data, benchmark and ESG fees—often up low-double digits annually—squeeze margins. Multi-year contracts (typically 3–5 years) and switching frictions reinforce vendor leverage. abrdn can negotiate enterprise bundles and adopt open-source/alternative data to reduce dependency.

Custody, fund admin, and transfer agents

Global custodians and administrators are few—BNY Mellon, State Street, JP Morgan, Citi, Northern Trust, BNP Paribas and HSBC dominate custody and fund administration—making scale and standardisation critical. Service quality and operational resilience are non-negotiable, giving providers leverage on terms and SLAs. Competition among top-tier firms enables abrdn to dual-source and embed KPI-driven contracts to manage cost and service.

Cloud, fintech, and tech stack providers

Reliance on major cloud and software vendors (AWS ~33% share, Microsoft Azure ~23% in 2024) creates switching costs and potential lock-in for abrdn; security, latency, and integration SLAs further heighten supplier influence. Large-volume commitments can secure discounts but raise dependency and concentration risk. abrdn can mitigate this by adopting modular architectures and enforcing interoperability standards.

- Concentration: AWS/Azure ~56% combined (2024)

- Risk: vendor lock-in increases migration cost and time

- Mitigation: modular APIs, multi-cloud, open standards

- Trade-off: volume discounts vs dependency

Distribution platforms and intermediaries

Third-party platforms, advisors and wealth networks control end-client access in key markets, with top UK and European platforms still concentrating a majority of retail flows in 2024. Shelf space, marketing support and platform fees directly shape fund flows and net pricing, giving large platforms clear negotiating leverage. abrdn’s owned platforms partially offset this by internalising distribution economics and retaining client relationships.

- Top platforms dominate retail distribution in 2024

- Platform fees and shelf placement drive flows

- abrdn platforms reduce external dependence

Asset manager hit by strong supplier power: scarce PMs, expensive data and cloud lock-in

abrdn faces high supplier power: scarce PMs (c.£360bn AUM in 2024) and concentrated custodians raise retention and fee risks. Data vendors (Bloomberg ~USD24,000; Refinitiv ~USD22,000) and benchmarks exert pricing power via entrenched workflows. Cloud concentration (AWS ~33%, Azure ~23% in 2024) creates lock-in; multi-year contracts and platform gatekeepers further reinforce leverage.

| Supplier | 2024 metric |

|---|---|

| abrdn AUM | c.£360bn |

| Bloomberg price | ~USD24,000/yr |

| Refinitiv price | ~USD22,000/yr |

| AWS/Azure share | ~33% / 23% |

What is included in the product

Tailored Porter's Five Forces analysis for abrdn that uncovers key competitive drivers, customer bargaining power, supplier influence, and barriers to entry shaping its market position. Identifies emerging substitutes, disruptive threats, and strategic levers affecting pricing, profitability, and long-term resilience.

abrdn Porter's Five Forces Analysis delivers a clear one-sheet summary of competitive pressures and an interactive radar view, letting teams instantly spot threats/opportunities and copy-ready visuals for decks—no complex tools required.

Customers Bargaining Power

Fee compression from institutions and wealth

Large pension funds, insurers and wealth networks — part of the roughly USD 60 trillion in global pension assets in 2024 — push fee compression and stricter performance hurdles, forcing abrdn to defend net-of-fee outcomes and bespoke mandates.

Transparent benchmarking and PRIIP-like reporting intensify negotiations; institutional clients expect tiered pricing, scale discounts and fees often negotiated below industry averages.

Low switching costs for many mandates

Low switching costs—mandates can be re-tendered and funds redeemed—drive client mobility, with performance dips or team changes frequently prompting reviews. abrdn mitigates churn through service quality, consistent processes and multi-year track records; its scale (c.£300bn AUM in 2024) underpins client servicing. Sticky platform relationships and model portfolios further raise retention.

High due diligence and custom requirements

Institutions increasingly demand detailed ESG, risk and operational transparency, driven by frameworks such as the EU SFDR (in force since 2021) and over 5,000 PRI signatories globally, raising due diligence standards. Custom guidelines, bespoke reporting and factor tilts increase operational complexity and cost for managers. abrdn can convert this into differentiation through data-rich reporting and active stewardship; failure to meet mandates risks loss of institutional clients.

Demand shift to passive and low-cost beta

Clients shift to ETFs and index strategies, anchoring fee expectations as global ETF/ETP assets reached about US$12.0 trillion in 2024; active funds face direct price benchmarking to passive alternatives. abrdn must demonstrate persistent alpha or pivot to outcome-focused, private markets and multi-asset solutions, while blended fee models and performance fees can better align incentives.

- Passive anchors pricing

- Need for persistent alpha

- Push to private/outcome solutions

- Blended/performance fees align payoffs

Cross-selling potential on platforms

Clients on abrdn’s administration and platforms exhibit higher lifetime value and greater integration stickiness, making cross-selling a key lever to reduce churn; bundled services lower perceived switching benefits, but sophisticated institutional and advisory buyers will still unbundle to source best-in-class capabilities, so clear value articulation across the stack is crucial.

- Higher LTV and stickiness

- Bundling reduces switching

- Sophisticated buyers unbundle

- Need clear cross-stack value

USD60tn pensions, ETF growth press fees; c.£300bn manager backs scale

Large institutional clients (part of ~USD60tn pension assets in 2024) compress fees and demand bespoke reporting; low switching costs and ETF growth (USD12.0tn ETPs 2024) increase bargaining power. abrdn (c.£300bn AUM 2024) counters via scale, bundled platform services and private/outcome solutions to protect margins.

| Metric | 2024 |

|---|---|

| Pension pool | USD60tn |

| ETF/ETP assets | USD12.0tn |

| abrdn AUM | £300bn |

What You See Is What You Get

abrdn Porter's Five Forces Analysis

This preview shows the exact abrdn Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is precisely the document you'll get, with no surprises.

From Overview to Strategy Blueprint

Abrdn faces moderate buyer power, concentrated institutional clients, fee pressure and digital disruption that intensify competition; supplier relationships and regulatory scrutiny further shape strategic options. This snapshot highlights key tensions but scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Dependence on talent and star PMs

Portfolio managers, analysts and distribution leaders are scarce, credentialed suppliers whose mobility drives wage inflation; abrdn reported c.£360bn AUM in 2024, so loss of star PMs can risk meaningful fee revenue and client redemptions. abrdn must offer competitive pay, culture and clear career paths to retain alpha-generators and limit mandate churn. Long-term incentives and team-based investment processes reduce concentration risk by aligning pay and distributing client relationships.

Concentrated market data and index vendors

Essential inputs from Bloomberg (Terminal ~USD24,000/yr), Refinitiv (Eikon ~USD22,000/yr), MSCI and FTSE Russell give vendors clear pricing power with few substitutes and entrenched workflows. Rising data, benchmark and ESG fees—often up low-double digits annually—squeeze margins. Multi-year contracts (typically 3–5 years) and switching frictions reinforce vendor leverage. abrdn can negotiate enterprise bundles and adopt open-source/alternative data to reduce dependency.

Custody, fund admin, and transfer agents

Global custodians and administrators are few—BNY Mellon, State Street, JP Morgan, Citi, Northern Trust, BNP Paribas and HSBC dominate custody and fund administration—making scale and standardisation critical. Service quality and operational resilience are non-negotiable, giving providers leverage on terms and SLAs. Competition among top-tier firms enables abrdn to dual-source and embed KPI-driven contracts to manage cost and service.

Cloud, fintech, and tech stack providers

Reliance on major cloud and software vendors (AWS ~33% share, Microsoft Azure ~23% in 2024) creates switching costs and potential lock-in for abrdn; security, latency, and integration SLAs further heighten supplier influence. Large-volume commitments can secure discounts but raise dependency and concentration risk. abrdn can mitigate this by adopting modular architectures and enforcing interoperability standards.

- Concentration: AWS/Azure ~56% combined (2024)

- Risk: vendor lock-in increases migration cost and time

- Mitigation: modular APIs, multi-cloud, open standards

- Trade-off: volume discounts vs dependency

Distribution platforms and intermediaries

Third-party platforms, advisors and wealth networks control end-client access in key markets, with top UK and European platforms still concentrating a majority of retail flows in 2024. Shelf space, marketing support and platform fees directly shape fund flows and net pricing, giving large platforms clear negotiating leverage. abrdn’s owned platforms partially offset this by internalising distribution economics and retaining client relationships.

- Top platforms dominate retail distribution in 2024

- Platform fees and shelf placement drive flows

- abrdn platforms reduce external dependence

Asset manager hit by strong supplier power: scarce PMs, expensive data and cloud lock-in

abrdn faces high supplier power: scarce PMs (c.£360bn AUM in 2024) and concentrated custodians raise retention and fee risks. Data vendors (Bloomberg ~USD24,000; Refinitiv ~USD22,000) and benchmarks exert pricing power via entrenched workflows. Cloud concentration (AWS ~33%, Azure ~23% in 2024) creates lock-in; multi-year contracts and platform gatekeepers further reinforce leverage.

| Supplier | 2024 metric |

|---|---|

| abrdn AUM | c.£360bn |

| Bloomberg price | ~USD24,000/yr |

| Refinitiv price | ~USD22,000/yr |

| AWS/Azure share | ~33% / 23% |

What is included in the product

Tailored Porter's Five Forces analysis for abrdn that uncovers key competitive drivers, customer bargaining power, supplier influence, and barriers to entry shaping its market position. Identifies emerging substitutes, disruptive threats, and strategic levers affecting pricing, profitability, and long-term resilience.

abrdn Porter's Five Forces Analysis delivers a clear one-sheet summary of competitive pressures and an interactive radar view, letting teams instantly spot threats/opportunities and copy-ready visuals for decks—no complex tools required.

Customers Bargaining Power

Fee compression from institutions and wealth

Large pension funds, insurers and wealth networks — part of the roughly USD 60 trillion in global pension assets in 2024 — push fee compression and stricter performance hurdles, forcing abrdn to defend net-of-fee outcomes and bespoke mandates.

Transparent benchmarking and PRIIP-like reporting intensify negotiations; institutional clients expect tiered pricing, scale discounts and fees often negotiated below industry averages.

Low switching costs for many mandates

Low switching costs—mandates can be re-tendered and funds redeemed—drive client mobility, with performance dips or team changes frequently prompting reviews. abrdn mitigates churn through service quality, consistent processes and multi-year track records; its scale (c.£300bn AUM in 2024) underpins client servicing. Sticky platform relationships and model portfolios further raise retention.

High due diligence and custom requirements

Institutions increasingly demand detailed ESG, risk and operational transparency, driven by frameworks such as the EU SFDR (in force since 2021) and over 5,000 PRI signatories globally, raising due diligence standards. Custom guidelines, bespoke reporting and factor tilts increase operational complexity and cost for managers. abrdn can convert this into differentiation through data-rich reporting and active stewardship; failure to meet mandates risks loss of institutional clients.

Demand shift to passive and low-cost beta

Clients shift to ETFs and index strategies, anchoring fee expectations as global ETF/ETP assets reached about US$12.0 trillion in 2024; active funds face direct price benchmarking to passive alternatives. abrdn must demonstrate persistent alpha or pivot to outcome-focused, private markets and multi-asset solutions, while blended fee models and performance fees can better align incentives.

- Passive anchors pricing

- Need for persistent alpha

- Push to private/outcome solutions

- Blended/performance fees align payoffs

Cross-selling potential on platforms

Clients on abrdn’s administration and platforms exhibit higher lifetime value and greater integration stickiness, making cross-selling a key lever to reduce churn; bundled services lower perceived switching benefits, but sophisticated institutional and advisory buyers will still unbundle to source best-in-class capabilities, so clear value articulation across the stack is crucial.

- Higher LTV and stickiness

- Bundling reduces switching

- Sophisticated buyers unbundle

- Need clear cross-stack value

USD60tn pensions, ETF growth press fees; c.£300bn manager backs scale

Large institutional clients (part of ~USD60tn pension assets in 2024) compress fees and demand bespoke reporting; low switching costs and ETF growth (USD12.0tn ETPs 2024) increase bargaining power. abrdn (c.£300bn AUM 2024) counters via scale, bundled platform services and private/outcome solutions to protect margins.

| Metric | 2024 |

|---|---|

| Pension pool | USD60tn |

| ETF/ETP assets | USD12.0tn |

| abrdn AUM | £300bn |

What You See Is What You Get

abrdn Porter's Five Forces Analysis

This preview shows the exact abrdn Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is precisely the document you'll get, with no surprises.

Description

From Overview to Strategy Blueprint

Abrdn faces moderate buyer power, concentrated institutional clients, fee pressure and digital disruption that intensify competition; supplier relationships and regulatory scrutiny further shape strategic options. This snapshot highlights key tensions but scratches the surface. Unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights for investment or strategy decisions.

Suppliers Bargaining Power

Dependence on talent and star PMs

Portfolio managers, analysts and distribution leaders are scarce, credentialed suppliers whose mobility drives wage inflation; abrdn reported c.£360bn AUM in 2024, so loss of star PMs can risk meaningful fee revenue and client redemptions. abrdn must offer competitive pay, culture and clear career paths to retain alpha-generators and limit mandate churn. Long-term incentives and team-based investment processes reduce concentration risk by aligning pay and distributing client relationships.

Concentrated market data and index vendors

Essential inputs from Bloomberg (Terminal ~USD24,000/yr), Refinitiv (Eikon ~USD22,000/yr), MSCI and FTSE Russell give vendors clear pricing power with few substitutes and entrenched workflows. Rising data, benchmark and ESG fees—often up low-double digits annually—squeeze margins. Multi-year contracts (typically 3–5 years) and switching frictions reinforce vendor leverage. abrdn can negotiate enterprise bundles and adopt open-source/alternative data to reduce dependency.

Custody, fund admin, and transfer agents

Global custodians and administrators are few—BNY Mellon, State Street, JP Morgan, Citi, Northern Trust, BNP Paribas and HSBC dominate custody and fund administration—making scale and standardisation critical. Service quality and operational resilience are non-negotiable, giving providers leverage on terms and SLAs. Competition among top-tier firms enables abrdn to dual-source and embed KPI-driven contracts to manage cost and service.

Cloud, fintech, and tech stack providers

Reliance on major cloud and software vendors (AWS ~33% share, Microsoft Azure ~23% in 2024) creates switching costs and potential lock-in for abrdn; security, latency, and integration SLAs further heighten supplier influence. Large-volume commitments can secure discounts but raise dependency and concentration risk. abrdn can mitigate this by adopting modular architectures and enforcing interoperability standards.

- Concentration: AWS/Azure ~56% combined (2024)

- Risk: vendor lock-in increases migration cost and time

- Mitigation: modular APIs, multi-cloud, open standards

- Trade-off: volume discounts vs dependency

Distribution platforms and intermediaries

Third-party platforms, advisors and wealth networks control end-client access in key markets, with top UK and European platforms still concentrating a majority of retail flows in 2024. Shelf space, marketing support and platform fees directly shape fund flows and net pricing, giving large platforms clear negotiating leverage. abrdn’s owned platforms partially offset this by internalising distribution economics and retaining client relationships.

- Top platforms dominate retail distribution in 2024

- Platform fees and shelf placement drive flows

- abrdn platforms reduce external dependence

Asset manager hit by strong supplier power: scarce PMs, expensive data and cloud lock-in

abrdn faces high supplier power: scarce PMs (c.£360bn AUM in 2024) and concentrated custodians raise retention and fee risks. Data vendors (Bloomberg ~USD24,000; Refinitiv ~USD22,000) and benchmarks exert pricing power via entrenched workflows. Cloud concentration (AWS ~33%, Azure ~23% in 2024) creates lock-in; multi-year contracts and platform gatekeepers further reinforce leverage.

| Supplier | 2024 metric |

|---|---|

| abrdn AUM | c.£360bn |

| Bloomberg price | ~USD24,000/yr |

| Refinitiv price | ~USD22,000/yr |

| AWS/Azure share | ~33% / 23% |

What is included in the product

Tailored Porter's Five Forces analysis for abrdn that uncovers key competitive drivers, customer bargaining power, supplier influence, and barriers to entry shaping its market position. Identifies emerging substitutes, disruptive threats, and strategic levers affecting pricing, profitability, and long-term resilience.

abrdn Porter's Five Forces Analysis delivers a clear one-sheet summary of competitive pressures and an interactive radar view, letting teams instantly spot threats/opportunities and copy-ready visuals for decks—no complex tools required.

Customers Bargaining Power

Fee compression from institutions and wealth

Large pension funds, insurers and wealth networks — part of the roughly USD 60 trillion in global pension assets in 2024 — push fee compression and stricter performance hurdles, forcing abrdn to defend net-of-fee outcomes and bespoke mandates.

Transparent benchmarking and PRIIP-like reporting intensify negotiations; institutional clients expect tiered pricing, scale discounts and fees often negotiated below industry averages.

Low switching costs for many mandates

Low switching costs—mandates can be re-tendered and funds redeemed—drive client mobility, with performance dips or team changes frequently prompting reviews. abrdn mitigates churn through service quality, consistent processes and multi-year track records; its scale (c.£300bn AUM in 2024) underpins client servicing. Sticky platform relationships and model portfolios further raise retention.

High due diligence and custom requirements

Institutions increasingly demand detailed ESG, risk and operational transparency, driven by frameworks such as the EU SFDR (in force since 2021) and over 5,000 PRI signatories globally, raising due diligence standards. Custom guidelines, bespoke reporting and factor tilts increase operational complexity and cost for managers. abrdn can convert this into differentiation through data-rich reporting and active stewardship; failure to meet mandates risks loss of institutional clients.

Demand shift to passive and low-cost beta

Clients shift to ETFs and index strategies, anchoring fee expectations as global ETF/ETP assets reached about US$12.0 trillion in 2024; active funds face direct price benchmarking to passive alternatives. abrdn must demonstrate persistent alpha or pivot to outcome-focused, private markets and multi-asset solutions, while blended fee models and performance fees can better align incentives.

- Passive anchors pricing

- Need for persistent alpha

- Push to private/outcome solutions

- Blended/performance fees align payoffs

Cross-selling potential on platforms

Clients on abrdn’s administration and platforms exhibit higher lifetime value and greater integration stickiness, making cross-selling a key lever to reduce churn; bundled services lower perceived switching benefits, but sophisticated institutional and advisory buyers will still unbundle to source best-in-class capabilities, so clear value articulation across the stack is crucial.

- Higher LTV and stickiness

- Bundling reduces switching

- Sophisticated buyers unbundle

- Need clear cross-stack value

USD60tn pensions, ETF growth press fees; c.£300bn manager backs scale

Large institutional clients (part of ~USD60tn pension assets in 2024) compress fees and demand bespoke reporting; low switching costs and ETF growth (USD12.0tn ETPs 2024) increase bargaining power. abrdn (c.£300bn AUM 2024) counters via scale, bundled platform services and private/outcome solutions to protect margins.

| Metric | 2024 |

|---|---|

| Pension pool | USD60tn |

| ETF/ETP assets | USD12.0tn |

| abrdn AUM | £300bn |

What You See Is What You Get

abrdn Porter's Five Forces Analysis

This preview shows the exact abrdn Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The file is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is precisely the document you'll get, with no surprises.