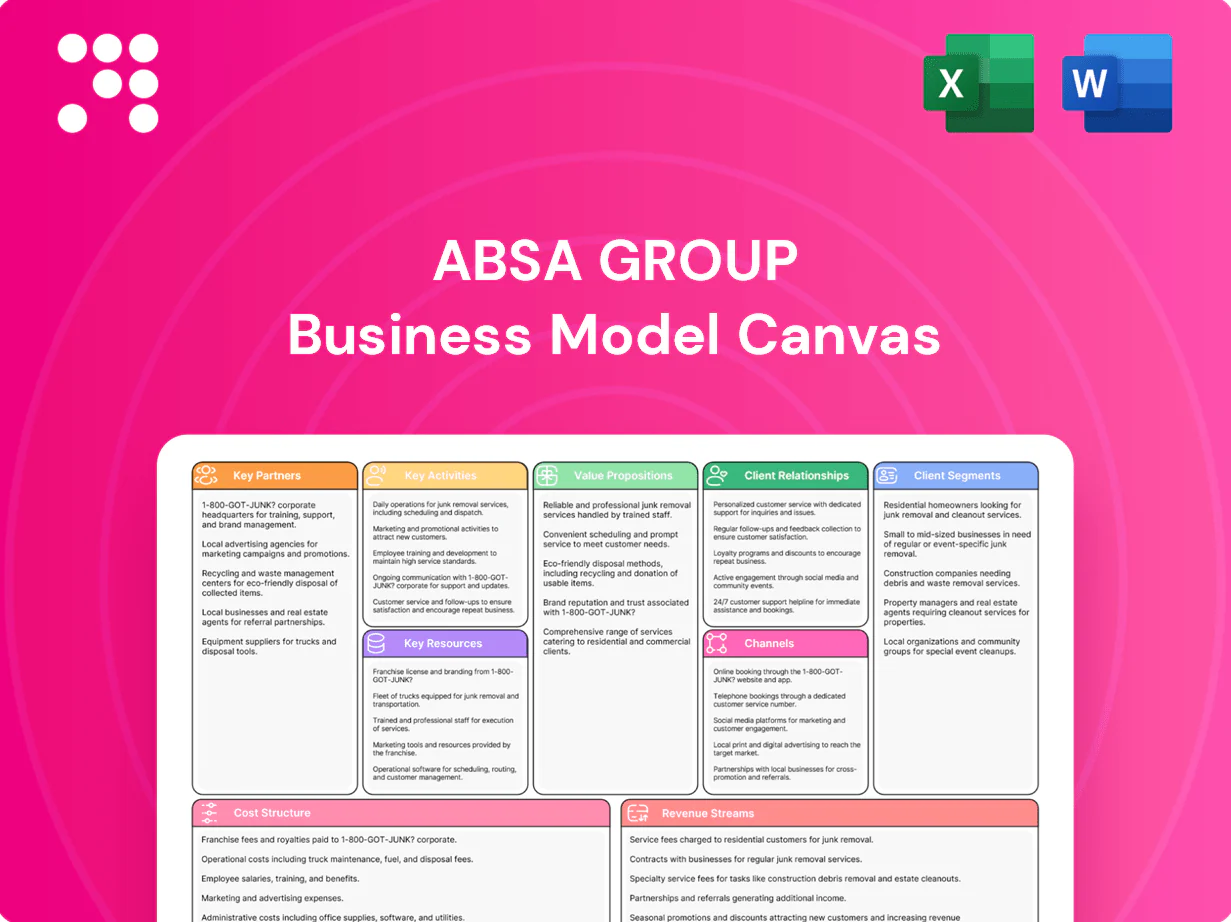

Absa Group Business Model Canvas

Unlock the strategic blueprint of a leading bank Business Model Canvas

Unlock the full strategic blueprint behind Absa Group’s Business Model Canvas—3–5 sentence preview that reveals how Absa creates value, scales across markets, and sustains competitive advantage. Purchase the complete Canvas for a section-by-section breakdown, editable Word/Excel files, and actionable insights for investors, consultants, and founders.

Partnerships

Fintech and payment networks

Collaborations with fintechs and card schemes enable Absa to deliver faster, lower-cost payments and new digital features, leveraging partners that collectively process scale—Visa handles ~500 million transactions daily—expanding acceptance, wallets and merchant services. Co-innovation with these partners accelerates time-to-market and scalability, while joint risk and fraud tools strengthen transaction security and reduce chargeback exposure.

Telecoms and mobile operators

Partnerships with telcos extend Absa’s mobile money, data-bundle offers and zero-rated banking access, leveraging a global mobile money base of over 1 billion accounts (GSMA 2024). Co-distribution with operators strengthens agent networks and rural reach via telco retail footprints. SIM-enabled KYC and bulk messaging accelerate onboarding and engagement, while shared analytics between banks and telcos improves customer targeting and reduces churn.

Cloud and core-banking technology providers

Alliances with cloud, core and cybersecurity vendors deliver industry-standard 99.9% uptime SLAs, boosting Agility and cost-efficiency across Absa in 2024. Managed services enable on-demand scaling to handle over 2x peak loads, reducing capital spend. APIs and microservices cut time-to-market by about 30%, accelerating product launches. Robust security certifications such as ISO 27001 support regulatory compliance.

Regulators and industry bodies

Close engagement with regulators and industry bodies ensures Absa meets banking, AML/CFT and data-privacy requirements while aligning with Basel III minima (CET1 4.5% plus 2.5% conservation buffer as of 2024); participation in payments councils advances standards and interoperability; regulatory sandboxes enable controlled innovation; prudential coordination supports stability and consumer protection.

- Regulatory compliance: CET1 4.5% + 2.5% buffer (2024)

- Payments engagement: standards & interoperability

- Sandboxes: controlled innovation pathways

- Prudential coordination: stability & consumer protection

Correspondent banks and insurers

Global correspondent relationships enable cross-border payments and trade finance, supporting Absa's footprint across 12 African countries and SWIFT-based corridors in 2024. Insurance underwriters and bancassurance partners expanded fee-generating product distribution, while reinsurers reduced balance-sheet risk on large commercial portfolios. Joint propositions deepen corporate and retail value through bundled lending, payments and insurance solutions.

- correspondent corridors: pan-African + global SWIFT links

- bancassurance: expanded fee income in 2024

- reinsurance: risk-transfer for large exposures

Alliances with card schemes, telcos and cloud vendors accelerate compliant cross-border payments

Strategic alliances with card schemes and fintechs (Visa ~500M tx/day) speed payments and expand merchant/wallet reach; telco tie-ups leverage GSMA 2024 ~1B mobile-money accounts for mass onboarding; cloud/cyber vendors deliver ~99.9% uptime and API-driven ~30% faster launches; regulators (CET1 4.5%+2.5% buffer) and correspondents across 12 African markets secure compliance and cross-border capability.

| Partner type | Key metric 2024 | Impact |

|---|---|---|

| Card/fintech | Visa ~500M tx/day | Faster, lower-cost payments |

| Telcos | ~1B mobile-money accounts | Mass mobile reach |

| Cloud/vendors | ~99.9% uptime | Scalability |

| Regulators | CET1 4.5%+2.5% | Compliance |

| Correspondents | 12 African markets | Cross-border |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Absa Group that maps customer segments, value propositions, channels, revenue streams and cost structure across the 9 BMC blocks. Includes competitive advantages, linked SWOT analysis and practical insights for presentations, investor discussions and strategic validation.

High-level, shareable Absa Group Business Model Canvas that condenses strategy into a clean, editable one-page snapshot — saves hours formatting and fast-tracks boardroom-ready reviews.

Activities

Lending and deposit gathering

Originating retail, SME and corporate loans (group gross loans ~ZAR 610bn in FY2024) while attracting stable deposits (customer deposits ~ZAR 900bn) drives Absa’s balance-sheet growth.

Pricing and risk-based underwriting balance growth with asset quality through targeted spreads and sector limits to keep impairment ratios controlled.

Active portfolio monitoring, collections and recovery processes limit delinquencies; deposit products are designed to optimize funding cost and liquidity across tenors.

Payments and cash management

Absa operates payments and cash management across 12 African countries, running card issuing, acquiring, EFT, RTGS and instant payments to support retail and corporate flows. The bank provides liquidity, collections and payroll services for businesses while boosting merchant acceptance and value-added services such as tokenisation and analytics. Operations prioritise high availability, real-time fraud monitoring and multi-channel dispute resolution.

Risk, compliance, and capital management

Credit, market and operational risk frameworks protect Absa's franchise through limits, models and monitoring. Robust regulatory reporting and AML/KYC controls preserve licenses and meet 2024 FATF and SARB expectations. Capital planning aligns with Basel III minima (CET1 4.5% plus 2.5% conservation buffer = 7.0%) and LCR >=100% liquidity standards. Regular stress testing and ICAAP outcomes steer strategic capital and portfolio decisions.

Digital product development

Digital product development focuses on mobile-first experiences and API-led services, delivering continuous delivery through agile, data-driven iteration while integrating identity, authentication, and personalization to boost security and engagement; Absa reported rising digital adoption in 2024 with digital sessions and mobile transactions proportionally increasing year-over-year.

- Mobile-first UX

- API-led services

- Agile continuous delivery

- Identity + personalization

- Analytics-driven cross-sell

Wealth and investment services

- Advisory, brokerage, discretionary mandates

- Structured products & multi-asset portfolios

- Fiduciary, trust & estate solutions

- Research & CIO views (weekly/quarterly)

Balance-sheet growth: ZAR 610bn loans, ZAR 900bn deposits, digital payments

Originating retail, SME and corporate loans (group gross loans ~ZAR 610bn in FY2024) while attracting stable deposits (~ZAR 900bn) drives balance-sheet growth.

Risk-based pricing, underwriting, monitoring and collections control impairments; capital planning aligns with CET1 7.0% target and LCR ≥100%.

Payments, cash management and mobile-first digital services across 12 countries enable transaction volumes and fee income growth.

| Metric | 2024 |

|---|---|

| Gross loans | ZAR 610bn |

| Customer deposits | ZAR 900bn |

What You See Is What You Get

Business Model Canvas

The Absa Group Business Model Canvas shown here is the actual deliverable, not a mockup. This preview is a direct snapshot of the full document you will receive upon purchase. After checkout you’ll get the complete, editable file formatted exactly as shown (Word and Excel), ready to present or adapt.

Unlock the strategic blueprint of a leading bank Business Model Canvas

Unlock the full strategic blueprint behind Absa Group’s Business Model Canvas—3–5 sentence preview that reveals how Absa creates value, scales across markets, and sustains competitive advantage. Purchase the complete Canvas for a section-by-section breakdown, editable Word/Excel files, and actionable insights for investors, consultants, and founders.

Partnerships

Fintech and payment networks

Collaborations with fintechs and card schemes enable Absa to deliver faster, lower-cost payments and new digital features, leveraging partners that collectively process scale—Visa handles ~500 million transactions daily—expanding acceptance, wallets and merchant services. Co-innovation with these partners accelerates time-to-market and scalability, while joint risk and fraud tools strengthen transaction security and reduce chargeback exposure.

Telecoms and mobile operators

Partnerships with telcos extend Absa’s mobile money, data-bundle offers and zero-rated banking access, leveraging a global mobile money base of over 1 billion accounts (GSMA 2024). Co-distribution with operators strengthens agent networks and rural reach via telco retail footprints. SIM-enabled KYC and bulk messaging accelerate onboarding and engagement, while shared analytics between banks and telcos improves customer targeting and reduces churn.

Cloud and core-banking technology providers

Alliances with cloud, core and cybersecurity vendors deliver industry-standard 99.9% uptime SLAs, boosting Agility and cost-efficiency across Absa in 2024. Managed services enable on-demand scaling to handle over 2x peak loads, reducing capital spend. APIs and microservices cut time-to-market by about 30%, accelerating product launches. Robust security certifications such as ISO 27001 support regulatory compliance.

Regulators and industry bodies

Close engagement with regulators and industry bodies ensures Absa meets banking, AML/CFT and data-privacy requirements while aligning with Basel III minima (CET1 4.5% plus 2.5% conservation buffer as of 2024); participation in payments councils advances standards and interoperability; regulatory sandboxes enable controlled innovation; prudential coordination supports stability and consumer protection.

- Regulatory compliance: CET1 4.5% + 2.5% buffer (2024)

- Payments engagement: standards & interoperability

- Sandboxes: controlled innovation pathways

- Prudential coordination: stability & consumer protection

Correspondent banks and insurers

Global correspondent relationships enable cross-border payments and trade finance, supporting Absa's footprint across 12 African countries and SWIFT-based corridors in 2024. Insurance underwriters and bancassurance partners expanded fee-generating product distribution, while reinsurers reduced balance-sheet risk on large commercial portfolios. Joint propositions deepen corporate and retail value through bundled lending, payments and insurance solutions.

- correspondent corridors: pan-African + global SWIFT links

- bancassurance: expanded fee income in 2024

- reinsurance: risk-transfer for large exposures

Alliances with card schemes, telcos and cloud vendors accelerate compliant cross-border payments

Strategic alliances with card schemes and fintechs (Visa ~500M tx/day) speed payments and expand merchant/wallet reach; telco tie-ups leverage GSMA 2024 ~1B mobile-money accounts for mass onboarding; cloud/cyber vendors deliver ~99.9% uptime and API-driven ~30% faster launches; regulators (CET1 4.5%+2.5% buffer) and correspondents across 12 African markets secure compliance and cross-border capability.

| Partner type | Key metric 2024 | Impact |

|---|---|---|

| Card/fintech | Visa ~500M tx/day | Faster, lower-cost payments |

| Telcos | ~1B mobile-money accounts | Mass mobile reach |

| Cloud/vendors | ~99.9% uptime | Scalability |

| Regulators | CET1 4.5%+2.5% | Compliance |

| Correspondents | 12 African markets | Cross-border |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Absa Group that maps customer segments, value propositions, channels, revenue streams and cost structure across the 9 BMC blocks. Includes competitive advantages, linked SWOT analysis and practical insights for presentations, investor discussions and strategic validation.

High-level, shareable Absa Group Business Model Canvas that condenses strategy into a clean, editable one-page snapshot — saves hours formatting and fast-tracks boardroom-ready reviews.

Activities

Lending and deposit gathering

Originating retail, SME and corporate loans (group gross loans ~ZAR 610bn in FY2024) while attracting stable deposits (customer deposits ~ZAR 900bn) drives Absa’s balance-sheet growth.

Pricing and risk-based underwriting balance growth with asset quality through targeted spreads and sector limits to keep impairment ratios controlled.

Active portfolio monitoring, collections and recovery processes limit delinquencies; deposit products are designed to optimize funding cost and liquidity across tenors.

Payments and cash management

Absa operates payments and cash management across 12 African countries, running card issuing, acquiring, EFT, RTGS and instant payments to support retail and corporate flows. The bank provides liquidity, collections and payroll services for businesses while boosting merchant acceptance and value-added services such as tokenisation and analytics. Operations prioritise high availability, real-time fraud monitoring and multi-channel dispute resolution.

Risk, compliance, and capital management

Credit, market and operational risk frameworks protect Absa's franchise through limits, models and monitoring. Robust regulatory reporting and AML/KYC controls preserve licenses and meet 2024 FATF and SARB expectations. Capital planning aligns with Basel III minima (CET1 4.5% plus 2.5% conservation buffer = 7.0%) and LCR >=100% liquidity standards. Regular stress testing and ICAAP outcomes steer strategic capital and portfolio decisions.

Digital product development

Digital product development focuses on mobile-first experiences and API-led services, delivering continuous delivery through agile, data-driven iteration while integrating identity, authentication, and personalization to boost security and engagement; Absa reported rising digital adoption in 2024 with digital sessions and mobile transactions proportionally increasing year-over-year.

- Mobile-first UX

- API-led services

- Agile continuous delivery

- Identity + personalization

- Analytics-driven cross-sell

Wealth and investment services

- Advisory, brokerage, discretionary mandates

- Structured products & multi-asset portfolios

- Fiduciary, trust & estate solutions

- Research & CIO views (weekly/quarterly)

Balance-sheet growth: ZAR 610bn loans, ZAR 900bn deposits, digital payments

Originating retail, SME and corporate loans (group gross loans ~ZAR 610bn in FY2024) while attracting stable deposits (~ZAR 900bn) drives balance-sheet growth.

Risk-based pricing, underwriting, monitoring and collections control impairments; capital planning aligns with CET1 7.0% target and LCR ≥100%.

Payments, cash management and mobile-first digital services across 12 countries enable transaction volumes and fee income growth.

| Metric | 2024 |

|---|---|

| Gross loans | ZAR 610bn |

| Customer deposits | ZAR 900bn |

What You See Is What You Get

Business Model Canvas

The Absa Group Business Model Canvas shown here is the actual deliverable, not a mockup. This preview is a direct snapshot of the full document you will receive upon purchase. After checkout you’ll get the complete, editable file formatted exactly as shown (Word and Excel), ready to present or adapt.

Description

Unlock the strategic blueprint of a leading bank Business Model Canvas

Unlock the full strategic blueprint behind Absa Group’s Business Model Canvas—3–5 sentence preview that reveals how Absa creates value, scales across markets, and sustains competitive advantage. Purchase the complete Canvas for a section-by-section breakdown, editable Word/Excel files, and actionable insights for investors, consultants, and founders.

Partnerships

Fintech and payment networks

Collaborations with fintechs and card schemes enable Absa to deliver faster, lower-cost payments and new digital features, leveraging partners that collectively process scale—Visa handles ~500 million transactions daily—expanding acceptance, wallets and merchant services. Co-innovation with these partners accelerates time-to-market and scalability, while joint risk and fraud tools strengthen transaction security and reduce chargeback exposure.

Telecoms and mobile operators

Partnerships with telcos extend Absa’s mobile money, data-bundle offers and zero-rated banking access, leveraging a global mobile money base of over 1 billion accounts (GSMA 2024). Co-distribution with operators strengthens agent networks and rural reach via telco retail footprints. SIM-enabled KYC and bulk messaging accelerate onboarding and engagement, while shared analytics between banks and telcos improves customer targeting and reduces churn.

Cloud and core-banking technology providers

Alliances with cloud, core and cybersecurity vendors deliver industry-standard 99.9% uptime SLAs, boosting Agility and cost-efficiency across Absa in 2024. Managed services enable on-demand scaling to handle over 2x peak loads, reducing capital spend. APIs and microservices cut time-to-market by about 30%, accelerating product launches. Robust security certifications such as ISO 27001 support regulatory compliance.

Regulators and industry bodies

Close engagement with regulators and industry bodies ensures Absa meets banking, AML/CFT and data-privacy requirements while aligning with Basel III minima (CET1 4.5% plus 2.5% conservation buffer as of 2024); participation in payments councils advances standards and interoperability; regulatory sandboxes enable controlled innovation; prudential coordination supports stability and consumer protection.

- Regulatory compliance: CET1 4.5% + 2.5% buffer (2024)

- Payments engagement: standards & interoperability

- Sandboxes: controlled innovation pathways

- Prudential coordination: stability & consumer protection

Correspondent banks and insurers

Global correspondent relationships enable cross-border payments and trade finance, supporting Absa's footprint across 12 African countries and SWIFT-based corridors in 2024. Insurance underwriters and bancassurance partners expanded fee-generating product distribution, while reinsurers reduced balance-sheet risk on large commercial portfolios. Joint propositions deepen corporate and retail value through bundled lending, payments and insurance solutions.

- correspondent corridors: pan-African + global SWIFT links

- bancassurance: expanded fee income in 2024

- reinsurance: risk-transfer for large exposures

Alliances with card schemes, telcos and cloud vendors accelerate compliant cross-border payments

Strategic alliances with card schemes and fintechs (Visa ~500M tx/day) speed payments and expand merchant/wallet reach; telco tie-ups leverage GSMA 2024 ~1B mobile-money accounts for mass onboarding; cloud/cyber vendors deliver ~99.9% uptime and API-driven ~30% faster launches; regulators (CET1 4.5%+2.5% buffer) and correspondents across 12 African markets secure compliance and cross-border capability.

| Partner type | Key metric 2024 | Impact |

|---|---|---|

| Card/fintech | Visa ~500M tx/day | Faster, lower-cost payments |

| Telcos | ~1B mobile-money accounts | Mass mobile reach |

| Cloud/vendors | ~99.9% uptime | Scalability |

| Regulators | CET1 4.5%+2.5% | Compliance |

| Correspondents | 12 African markets | Cross-border |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Absa Group that maps customer segments, value propositions, channels, revenue streams and cost structure across the 9 BMC blocks. Includes competitive advantages, linked SWOT analysis and practical insights for presentations, investor discussions and strategic validation.

High-level, shareable Absa Group Business Model Canvas that condenses strategy into a clean, editable one-page snapshot — saves hours formatting and fast-tracks boardroom-ready reviews.

Activities

Lending and deposit gathering

Originating retail, SME and corporate loans (group gross loans ~ZAR 610bn in FY2024) while attracting stable deposits (customer deposits ~ZAR 900bn) drives Absa’s balance-sheet growth.

Pricing and risk-based underwriting balance growth with asset quality through targeted spreads and sector limits to keep impairment ratios controlled.

Active portfolio monitoring, collections and recovery processes limit delinquencies; deposit products are designed to optimize funding cost and liquidity across tenors.

Payments and cash management

Absa operates payments and cash management across 12 African countries, running card issuing, acquiring, EFT, RTGS and instant payments to support retail and corporate flows. The bank provides liquidity, collections and payroll services for businesses while boosting merchant acceptance and value-added services such as tokenisation and analytics. Operations prioritise high availability, real-time fraud monitoring and multi-channel dispute resolution.

Risk, compliance, and capital management

Credit, market and operational risk frameworks protect Absa's franchise through limits, models and monitoring. Robust regulatory reporting and AML/KYC controls preserve licenses and meet 2024 FATF and SARB expectations. Capital planning aligns with Basel III minima (CET1 4.5% plus 2.5% conservation buffer = 7.0%) and LCR >=100% liquidity standards. Regular stress testing and ICAAP outcomes steer strategic capital and portfolio decisions.

Digital product development

Digital product development focuses on mobile-first experiences and API-led services, delivering continuous delivery through agile, data-driven iteration while integrating identity, authentication, and personalization to boost security and engagement; Absa reported rising digital adoption in 2024 with digital sessions and mobile transactions proportionally increasing year-over-year.

- Mobile-first UX

- API-led services

- Agile continuous delivery

- Identity + personalization

- Analytics-driven cross-sell

Wealth and investment services

- Advisory, brokerage, discretionary mandates

- Structured products & multi-asset portfolios

- Fiduciary, trust & estate solutions

- Research & CIO views (weekly/quarterly)

Balance-sheet growth: ZAR 610bn loans, ZAR 900bn deposits, digital payments

Originating retail, SME and corporate loans (group gross loans ~ZAR 610bn in FY2024) while attracting stable deposits (~ZAR 900bn) drives balance-sheet growth.

Risk-based pricing, underwriting, monitoring and collections control impairments; capital planning aligns with CET1 7.0% target and LCR ≥100%.

Payments, cash management and mobile-first digital services across 12 countries enable transaction volumes and fee income growth.

| Metric | 2024 |

|---|---|

| Gross loans | ZAR 610bn |

| Customer deposits | ZAR 900bn |

What You See Is What You Get

Business Model Canvas

The Absa Group Business Model Canvas shown here is the actual deliverable, not a mockup. This preview is a direct snapshot of the full document you will receive upon purchase. After checkout you’ll get the complete, editable file formatted exactly as shown (Word and Excel), ready to present or adapt.