Acadia PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Acadia—three to five expert-level insights into the political, economic, social, technological, legal and environmental forces shaping its outlook. Ready-to-use and fully sourced, this report helps investors and strategists act with confidence; buy the full version for the complete deep dive and editable files.

Political factors

Medicaid/Medicare reimbursement priorities

Federal and state funding priorities drive behavioral health reimbursement—Medicaid covers about 85 million Americans and Medicare about 66 million (CMS 2024), so shifts in these programs materially affect volumes and margins. Changes in Medicaid expansion, IMD waivers and evolving Medicare behavioral health coverage have recently expanded provider eligibility and revenue opportunities. Election cycles and budget pressures can quickly expand or constrain services and rate-setting. Acadia must actively engage policymakers and model reimbursement variability in financial forecasts.

Mental health parity enforcement

Stronger federal and state enforcement of mental health parity can boost commercial reimbursement and utilization, important given roughly 1 in 5 US adults experience mental illness annually. Uneven enforcement drives geographic revenue variance and payer-specific authorization hurdles that affect length-of-stay approvals. Consistent enforcement favors Acadia, though the company must adapt to varied payer behavior and claims practices.

State regulatory regimes and CON rules

Thirty-five states plus Washington, DC maintain certificate-of-need programs as of 2024, and CON/licensing rules directly shape market entry and capacity. States differ on bed-expansion approvals and service-line restrictions, with CON reviews commonly taking 6–18 months and altering timing of capital deployments. Political leadership shifts frequently tighten or loosen these constraints, so strategic growth requires tailored, state-level regulatory navigation.

Public health and opioid response funding

- Grants/appropriations influence service demand and partnerships

- ~110,000 provisional US overdose deaths in 2023 keep funding prioritized

- Shift toward outpatient/community care reallocates funding opportunities

- Acadia should optimize grant-ready outpatient and crisis-stabilization offerings

Puerto Rico territorial policy dynamics

Puerto Rico territorial funding formulas and distinct healthcare policy, given a resident population of about 3.2 million, materially affect Acadia operations and reimbursement rates; federal Medicaid for territories is capped, creating revenue uncertainty. Federal disaster recovery support — including roughly $42.5 billion in HUD CDBG-DR allocations after Hurricane Maria — and FEMA responses influence infrastructure resilience and cost. Political shifts on-island and in Washington can change funding flows and regulatory support, so tailored advocacy and contingency planning are essential.

- Population ~3.2M impacts service demand

- $42.5B HUD CDBG-DR shows disaster funding scale

- Medicaid caps = reimbursement uncertainty

- Advocacy + contingency planning required

Medicaid/Medicare shifts, CON limits and rising overdoses reshape SUD care and funding

Federal/state program changes (Medicaid ~85M, Medicare ~66M in 2024) and parity enforcement drive volumes and reimbursement; election cycles affect budgets. 35 states+DC have CONs, slowing capacity expansion. ~110,000 provisional overdose deaths in 2023 focus SUD funding toward community care. Puerto Rico (pop ~3.2M) faces capped Medicaid and disaster funding exposure.

| Factor | Key Data |

|---|---|

| Medicaid/Medicare | Medicaid ~85M; Medicare ~66M (CMS 2024) |

| CONs | 35 states + DC |

| Overdose deaths | ~110,000 (2023 provisional) |

| Puerto Rico | Pop ~3.2M; capped Medicaid; $42.5B HUD CDBG-DR |

What is included in the product

Explores how macro-environmental factors uniquely affect Acadia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples; designed to help executives and investors identify risks, opportunities, and actionable strategies for planning and funding.

A concise, visually segmented PESTLE summary for Acadia that’s easily dropped into presentations, editable for local context or business lines, and shareable to align teams quickly during strategy and risk discussions.

Economic factors

Labor availability and wage inflation

Shortages of psychiatrists, nurses, and therapists—with RN turnover near 27% (NSI 2023) and behavioral‑health provider shortfalls estimated in the low tens of thousands—drive higher wages and staffing costs for Acadia. Overtime, contract labor (often 20–40% premium) and retention incentives compress margins. Economic cycles affect turnover and recruitment pipelines, while efficient staffing models and in‑house training programs reduce volatility and curb agency reliance.

Payer mix and consumer affordability

Revenue hinges on the payer mix between Medicaid, Medicare, commercial and self-pay; Medicaid/CHIP covers roughly one-quarter of Americans (~80–90 million, KFF 2024) while Medicare enrolls about 65 million beneficiaries (CMS 2024), shaping reimbursement levels. Macroeconomic stress tends to boost Medicaid enrollment and increases bad debt and charity care as patient affordability falls. Benefit design shifts alter patient share and access, changing case mix and margins. Optimizing network participation and proactive financial counseling stabilizes cash flow and reduces receivable days.

Interest rates and capital intensity

Inpatient facilities require significant capital for builds, expansions, and upgrades; US hospital construction averages roughly $1.2–1.8 million per bed, raising project costs for Acadia. Higher interest rates (Fed funds ~5.25–5.50% in 2024–2025) increase borrowing costs and hurdle rates, compressing valuations and delaying M&A. Rate environment influences deal timing and multiples; disciplined capex and financing structures are critical.

Utilization trends and occupancy

Economic uncertainty has pushed behavioral health demand higher—about 1 in 5 US adults (≈20%) experience mental illness—while strained payer budgets compress reimbursements and margins. Seasonal and regional census swings alter case mix, length-of-stay management directly influences throughput and revenue, and data-driven scheduling plus referral management stabilize occupancy and reduce idle capacity.

- Demand: 20% prevalence

- Payer pressure: lower reimbursement risk

- Seasonality: regional census swings

- Ops: LOS drives throughput

- Tools: analytics for scheduling/referrals

M&A landscape and competition

Private equity and health systems remain highly active in behavioral health roll-ups, increasing competitive bidding for assets and accelerating consolidation.

Valuation cycle swings influence timing of acquisitions and divestitures, creating windows for strategic buys when multiples compress and for exits when they expand.

Scale advantages in contracting and overhead management can lift margins, and Acadia’s robust pipeline and proven integration capabilities are key drivers of its organic and M&A growth.

- PE and health systems: heightened roll-up activity

- Valuation cycles: dictate buy/sell timing

- Scale: contracting and overhead leverage

- Acadia: pipeline + integration = growth

Medicaid/Medicare shifts, CON limits and rising overdoses reshape SUD care and funding

Staff shortages (RN turnover ~27% NSI 2023; behavioral‑health shortfall low tens of thousands) drive wage inflation and agency spend, while payer mix (Medicaid ~80–90M KFF 2024; Medicare ~65M CMS 2024) and Fed funds (~5.25–5.50% 2024–25) compress margins and slow deals; scale and analytics mitigate volatility.

| Metric | Value |

|---|---|

| RN turnover | ~27% |

| BH provider gap | 20–30k |

| Medicaid | 80–90M |

| Medicare | ~65M |

| Fed funds | 5.25–5.50% |

| Constr. cost/bed | $1.2–1.8M |

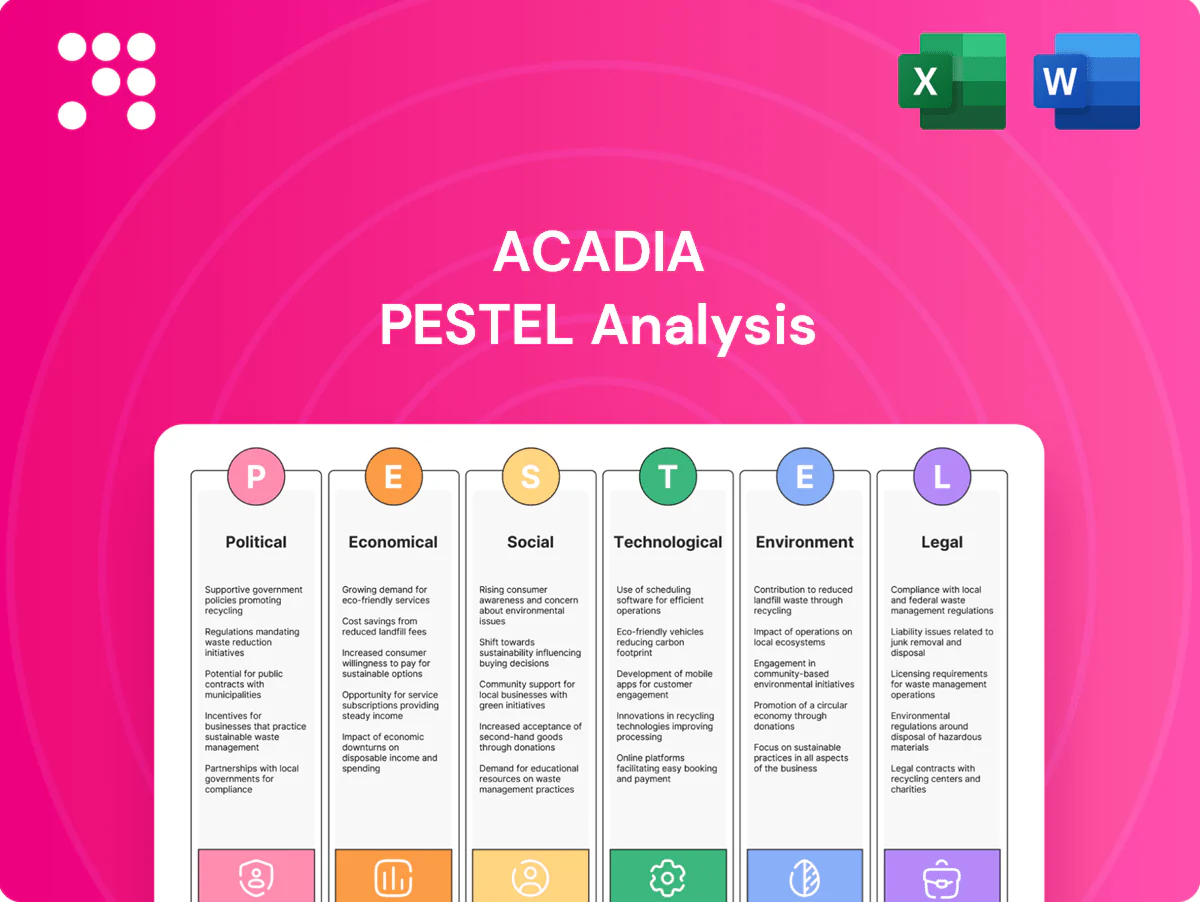

What You See Is What You Get

Acadia PESTLE Analysis

The Acadia PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It examines political, economic, social, technological, legal, and environmental factors with clear, actionable insights and cited data. No placeholders, no surprises.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Acadia—three to five expert-level insights into the political, economic, social, technological, legal and environmental forces shaping its outlook. Ready-to-use and fully sourced, this report helps investors and strategists act with confidence; buy the full version for the complete deep dive and editable files.

Political factors

Medicaid/Medicare reimbursement priorities

Federal and state funding priorities drive behavioral health reimbursement—Medicaid covers about 85 million Americans and Medicare about 66 million (CMS 2024), so shifts in these programs materially affect volumes and margins. Changes in Medicaid expansion, IMD waivers and evolving Medicare behavioral health coverage have recently expanded provider eligibility and revenue opportunities. Election cycles and budget pressures can quickly expand or constrain services and rate-setting. Acadia must actively engage policymakers and model reimbursement variability in financial forecasts.

Mental health parity enforcement

Stronger federal and state enforcement of mental health parity can boost commercial reimbursement and utilization, important given roughly 1 in 5 US adults experience mental illness annually. Uneven enforcement drives geographic revenue variance and payer-specific authorization hurdles that affect length-of-stay approvals. Consistent enforcement favors Acadia, though the company must adapt to varied payer behavior and claims practices.

State regulatory regimes and CON rules

Thirty-five states plus Washington, DC maintain certificate-of-need programs as of 2024, and CON/licensing rules directly shape market entry and capacity. States differ on bed-expansion approvals and service-line restrictions, with CON reviews commonly taking 6–18 months and altering timing of capital deployments. Political leadership shifts frequently tighten or loosen these constraints, so strategic growth requires tailored, state-level regulatory navigation.

Public health and opioid response funding

- Grants/appropriations influence service demand and partnerships

- ~110,000 provisional US overdose deaths in 2023 keep funding prioritized

- Shift toward outpatient/community care reallocates funding opportunities

- Acadia should optimize grant-ready outpatient and crisis-stabilization offerings

Puerto Rico territorial policy dynamics

Puerto Rico territorial funding formulas and distinct healthcare policy, given a resident population of about 3.2 million, materially affect Acadia operations and reimbursement rates; federal Medicaid for territories is capped, creating revenue uncertainty. Federal disaster recovery support — including roughly $42.5 billion in HUD CDBG-DR allocations after Hurricane Maria — and FEMA responses influence infrastructure resilience and cost. Political shifts on-island and in Washington can change funding flows and regulatory support, so tailored advocacy and contingency planning are essential.

- Population ~3.2M impacts service demand

- $42.5B HUD CDBG-DR shows disaster funding scale

- Medicaid caps = reimbursement uncertainty

- Advocacy + contingency planning required

Medicaid/Medicare shifts, CON limits and rising overdoses reshape SUD care and funding

Federal/state program changes (Medicaid ~85M, Medicare ~66M in 2024) and parity enforcement drive volumes and reimbursement; election cycles affect budgets. 35 states+DC have CONs, slowing capacity expansion. ~110,000 provisional overdose deaths in 2023 focus SUD funding toward community care. Puerto Rico (pop ~3.2M) faces capped Medicaid and disaster funding exposure.

| Factor | Key Data |

|---|---|

| Medicaid/Medicare | Medicaid ~85M; Medicare ~66M (CMS 2024) |

| CONs | 35 states + DC |

| Overdose deaths | ~110,000 (2023 provisional) |

| Puerto Rico | Pop ~3.2M; capped Medicaid; $42.5B HUD CDBG-DR |

What is included in the product

Explores how macro-environmental factors uniquely affect Acadia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples; designed to help executives and investors identify risks, opportunities, and actionable strategies for planning and funding.

A concise, visually segmented PESTLE summary for Acadia that’s easily dropped into presentations, editable for local context or business lines, and shareable to align teams quickly during strategy and risk discussions.

Economic factors

Labor availability and wage inflation

Shortages of psychiatrists, nurses, and therapists—with RN turnover near 27% (NSI 2023) and behavioral‑health provider shortfalls estimated in the low tens of thousands—drive higher wages and staffing costs for Acadia. Overtime, contract labor (often 20–40% premium) and retention incentives compress margins. Economic cycles affect turnover and recruitment pipelines, while efficient staffing models and in‑house training programs reduce volatility and curb agency reliance.

Payer mix and consumer affordability

Revenue hinges on the payer mix between Medicaid, Medicare, commercial and self-pay; Medicaid/CHIP covers roughly one-quarter of Americans (~80–90 million, KFF 2024) while Medicare enrolls about 65 million beneficiaries (CMS 2024), shaping reimbursement levels. Macroeconomic stress tends to boost Medicaid enrollment and increases bad debt and charity care as patient affordability falls. Benefit design shifts alter patient share and access, changing case mix and margins. Optimizing network participation and proactive financial counseling stabilizes cash flow and reduces receivable days.

Interest rates and capital intensity

Inpatient facilities require significant capital for builds, expansions, and upgrades; US hospital construction averages roughly $1.2–1.8 million per bed, raising project costs for Acadia. Higher interest rates (Fed funds ~5.25–5.50% in 2024–2025) increase borrowing costs and hurdle rates, compressing valuations and delaying M&A. Rate environment influences deal timing and multiples; disciplined capex and financing structures are critical.

Utilization trends and occupancy

Economic uncertainty has pushed behavioral health demand higher—about 1 in 5 US adults (≈20%) experience mental illness—while strained payer budgets compress reimbursements and margins. Seasonal and regional census swings alter case mix, length-of-stay management directly influences throughput and revenue, and data-driven scheduling plus referral management stabilize occupancy and reduce idle capacity.

- Demand: 20% prevalence

- Payer pressure: lower reimbursement risk

- Seasonality: regional census swings

- Ops: LOS drives throughput

- Tools: analytics for scheduling/referrals

M&A landscape and competition

Private equity and health systems remain highly active in behavioral health roll-ups, increasing competitive bidding for assets and accelerating consolidation.

Valuation cycle swings influence timing of acquisitions and divestitures, creating windows for strategic buys when multiples compress and for exits when they expand.

Scale advantages in contracting and overhead management can lift margins, and Acadia’s robust pipeline and proven integration capabilities are key drivers of its organic and M&A growth.

- PE and health systems: heightened roll-up activity

- Valuation cycles: dictate buy/sell timing

- Scale: contracting and overhead leverage

- Acadia: pipeline + integration = growth

Medicaid/Medicare shifts, CON limits and rising overdoses reshape SUD care and funding

Staff shortages (RN turnover ~27% NSI 2023; behavioral‑health shortfall low tens of thousands) drive wage inflation and agency spend, while payer mix (Medicaid ~80–90M KFF 2024; Medicare ~65M CMS 2024) and Fed funds (~5.25–5.50% 2024–25) compress margins and slow deals; scale and analytics mitigate volatility.

| Metric | Value |

|---|---|

| RN turnover | ~27% |

| BH provider gap | 20–30k |

| Medicaid | 80–90M |

| Medicare | ~65M |

| Fed funds | 5.25–5.50% |

| Constr. cost/bed | $1.2–1.8M |

What You See Is What You Get

Acadia PESTLE Analysis

The Acadia PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It examines political, economic, social, technological, legal, and environmental factors with clear, actionable insights and cited data. No placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Acadia—three to five expert-level insights into the political, economic, social, technological, legal and environmental forces shaping its outlook. Ready-to-use and fully sourced, this report helps investors and strategists act with confidence; buy the full version for the complete deep dive and editable files.

Political factors

Medicaid/Medicare reimbursement priorities

Federal and state funding priorities drive behavioral health reimbursement—Medicaid covers about 85 million Americans and Medicare about 66 million (CMS 2024), so shifts in these programs materially affect volumes and margins. Changes in Medicaid expansion, IMD waivers and evolving Medicare behavioral health coverage have recently expanded provider eligibility and revenue opportunities. Election cycles and budget pressures can quickly expand or constrain services and rate-setting. Acadia must actively engage policymakers and model reimbursement variability in financial forecasts.

Mental health parity enforcement

Stronger federal and state enforcement of mental health parity can boost commercial reimbursement and utilization, important given roughly 1 in 5 US adults experience mental illness annually. Uneven enforcement drives geographic revenue variance and payer-specific authorization hurdles that affect length-of-stay approvals. Consistent enforcement favors Acadia, though the company must adapt to varied payer behavior and claims practices.

State regulatory regimes and CON rules

Thirty-five states plus Washington, DC maintain certificate-of-need programs as of 2024, and CON/licensing rules directly shape market entry and capacity. States differ on bed-expansion approvals and service-line restrictions, with CON reviews commonly taking 6–18 months and altering timing of capital deployments. Political leadership shifts frequently tighten or loosen these constraints, so strategic growth requires tailored, state-level regulatory navigation.

Public health and opioid response funding

- Grants/appropriations influence service demand and partnerships

- ~110,000 provisional US overdose deaths in 2023 keep funding prioritized

- Shift toward outpatient/community care reallocates funding opportunities

- Acadia should optimize grant-ready outpatient and crisis-stabilization offerings

Puerto Rico territorial policy dynamics

Puerto Rico territorial funding formulas and distinct healthcare policy, given a resident population of about 3.2 million, materially affect Acadia operations and reimbursement rates; federal Medicaid for territories is capped, creating revenue uncertainty. Federal disaster recovery support — including roughly $42.5 billion in HUD CDBG-DR allocations after Hurricane Maria — and FEMA responses influence infrastructure resilience and cost. Political shifts on-island and in Washington can change funding flows and regulatory support, so tailored advocacy and contingency planning are essential.

- Population ~3.2M impacts service demand

- $42.5B HUD CDBG-DR shows disaster funding scale

- Medicaid caps = reimbursement uncertainty

- Advocacy + contingency planning required

Medicaid/Medicare shifts, CON limits and rising overdoses reshape SUD care and funding

Federal/state program changes (Medicaid ~85M, Medicare ~66M in 2024) and parity enforcement drive volumes and reimbursement; election cycles affect budgets. 35 states+DC have CONs, slowing capacity expansion. ~110,000 provisional overdose deaths in 2023 focus SUD funding toward community care. Puerto Rico (pop ~3.2M) faces capped Medicaid and disaster funding exposure.

| Factor | Key Data |

|---|---|

| Medicaid/Medicare | Medicaid ~85M; Medicare ~66M (CMS 2024) |

| CONs | 35 states + DC |

| Overdose deaths | ~110,000 (2023 provisional) |

| Puerto Rico | Pop ~3.2M; capped Medicaid; $42.5B HUD CDBG-DR |

What is included in the product

Explores how macro-environmental factors uniquely affect Acadia across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples; designed to help executives and investors identify risks, opportunities, and actionable strategies for planning and funding.

A concise, visually segmented PESTLE summary for Acadia that’s easily dropped into presentations, editable for local context or business lines, and shareable to align teams quickly during strategy and risk discussions.

Economic factors

Labor availability and wage inflation

Shortages of psychiatrists, nurses, and therapists—with RN turnover near 27% (NSI 2023) and behavioral‑health provider shortfalls estimated in the low tens of thousands—drive higher wages and staffing costs for Acadia. Overtime, contract labor (often 20–40% premium) and retention incentives compress margins. Economic cycles affect turnover and recruitment pipelines, while efficient staffing models and in‑house training programs reduce volatility and curb agency reliance.

Payer mix and consumer affordability

Revenue hinges on the payer mix between Medicaid, Medicare, commercial and self-pay; Medicaid/CHIP covers roughly one-quarter of Americans (~80–90 million, KFF 2024) while Medicare enrolls about 65 million beneficiaries (CMS 2024), shaping reimbursement levels. Macroeconomic stress tends to boost Medicaid enrollment and increases bad debt and charity care as patient affordability falls. Benefit design shifts alter patient share and access, changing case mix and margins. Optimizing network participation and proactive financial counseling stabilizes cash flow and reduces receivable days.

Interest rates and capital intensity

Inpatient facilities require significant capital for builds, expansions, and upgrades; US hospital construction averages roughly $1.2–1.8 million per bed, raising project costs for Acadia. Higher interest rates (Fed funds ~5.25–5.50% in 2024–2025) increase borrowing costs and hurdle rates, compressing valuations and delaying M&A. Rate environment influences deal timing and multiples; disciplined capex and financing structures are critical.

Utilization trends and occupancy

Economic uncertainty has pushed behavioral health demand higher—about 1 in 5 US adults (≈20%) experience mental illness—while strained payer budgets compress reimbursements and margins. Seasonal and regional census swings alter case mix, length-of-stay management directly influences throughput and revenue, and data-driven scheduling plus referral management stabilize occupancy and reduce idle capacity.

- Demand: 20% prevalence

- Payer pressure: lower reimbursement risk

- Seasonality: regional census swings

- Ops: LOS drives throughput

- Tools: analytics for scheduling/referrals

M&A landscape and competition

Private equity and health systems remain highly active in behavioral health roll-ups, increasing competitive bidding for assets and accelerating consolidation.

Valuation cycle swings influence timing of acquisitions and divestitures, creating windows for strategic buys when multiples compress and for exits when they expand.

Scale advantages in contracting and overhead management can lift margins, and Acadia’s robust pipeline and proven integration capabilities are key drivers of its organic and M&A growth.

- PE and health systems: heightened roll-up activity

- Valuation cycles: dictate buy/sell timing

- Scale: contracting and overhead leverage

- Acadia: pipeline + integration = growth

Medicaid/Medicare shifts, CON limits and rising overdoses reshape SUD care and funding

Staff shortages (RN turnover ~27% NSI 2023; behavioral‑health shortfall low tens of thousands) drive wage inflation and agency spend, while payer mix (Medicaid ~80–90M KFF 2024; Medicare ~65M CMS 2024) and Fed funds (~5.25–5.50% 2024–25) compress margins and slow deals; scale and analytics mitigate volatility.

| Metric | Value |

|---|---|

| RN turnover | ~27% |

| BH provider gap | 20–30k |

| Medicaid | 80–90M |

| Medicare | ~65M |

| Fed funds | 5.25–5.50% |

| Constr. cost/bed | $1.2–1.8M |

What You See Is What You Get

Acadia PESTLE Analysis

The Acadia PESTLE analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It examines political, economic, social, technological, legal, and environmental factors with clear, actionable insights and cited data. No placeholders, no surprises.