Asia Commercial Bank Business Model Canvas

Unlock a bank Business Model Canvas — editable Word/Excel for investors & strategists

Unlock the full strategic blueprint behind Asia Commercial Bank with our Business Model Canvas—detailed, company-specific insights into customer segments, revenue streams, partnerships, and growth levers. Ideal for investors, consultants, and founders; download the editable Word/Excel file to benchmark, plan, and act today.

Partnerships

State Bank & Regulators

Partnership with the State Bank of Vietnam ensures compliance, liquidity access and policy alignment, leveraging SBV oversight of a banking system with total assets exceeding $1 trillion in 2024 and foreign-exchange reserves above $80 billion. It enables Asia Commercial Bank to participate in interbank markets and national payment systems. Close coordination cuts regulatory risk and speeds new-product approvals, strengthening trust with institutional clients.

Payment & Card Networks

Alliances with Visa, Mastercard and local NAPAS enable ACB to issue cards and acquire merchants across networks that together serve over 5 billion cards worldwide and NAPAS processing exceeding 1 billion transactions annually, expanding acceptance and driving card fee income. Joint risk controls with network-level fraud scoring and tokenization have cut chargeback rates where deployed, strengthening loss prevention. Co-branded programs with merchants and wallets accelerate digital payments adoption, lifting contactless and e-commerce volumes significantly year-over-year.

Fintech & Technology Vendors

API partners and core banking providers enhance mobile, online and analytics capabilities, accelerating feature rollout by 30–50% and lowering development risk; cloud and cybersecurity vendors, with APAC cloud adoption ~60% in 2024, boost resilience and compliance; KYC providers can cut onboarding costs by up to 40%; sandbox pilots shorten time-to-market roughly 25–40%.

Corporate & Institutional Partners

Treasury partners, insurers and asset managers widen ACB’s product breadth, enabling bundled cash management, bancassurance and investment solutions that deepen client share of wallet; correspondent banks support cross-border trade and remittances (global remittances to low‑ and middle‑income countries were $626 billion in 2023), while co‑origination deals expand lending reach into SME segments.

- Treasury partners: liquidity & FX products

- Insurers: bancassurance for fee income

- Asset managers: managed solutions & AUM growth

- Correspondent banks: cross‑border corridors, remittances

- Co‑origination: extended SME loan distribution

Agents & Distribution Allies

Agents and distribution allies — ATM networks, payment agents and retail chains — extend Asia Commercial Bank last-mile service, lowering capex per outlet and improving accessibility across urban and rural areas.

Alliances with employers and universities secure payroll flows and student acquisition channels, while partnerships with real estate developers and auto dealers feed secured lending pipelines and boost loan originations.

- ATM networks expand reach

- Payment agents reduce capex

- Employer/university payrolls grow deposits

- Developers/dealers increase secured loans

Vietnam banks tap SBV, NAPAS and global card rails to speed payments and remittances

ACB leverages SBV oversight (Vietnam banking assets >$1T in 2024; FX reserves >$80B) for liquidity and regulatory alignment. Card/NAPAS ties (NAPAS >1B tx/yr; global cards >5B) expand payments and fee income. Tech, treasury, insurer and correspondent partners cut onboarding by ~40%, speed rollouts 30–50% and support remittances ($626B global, 2023).

| Partner | Metric | 2024/2023 |

|---|---|---|

| SBV | Banking assets | >$1T (2024) |

| NAPAS | Transactions | >1B/yr |

| Card networks | Cards | >5B global |

| Remittances | Global flow | $626B (2023) |

What is included in the product

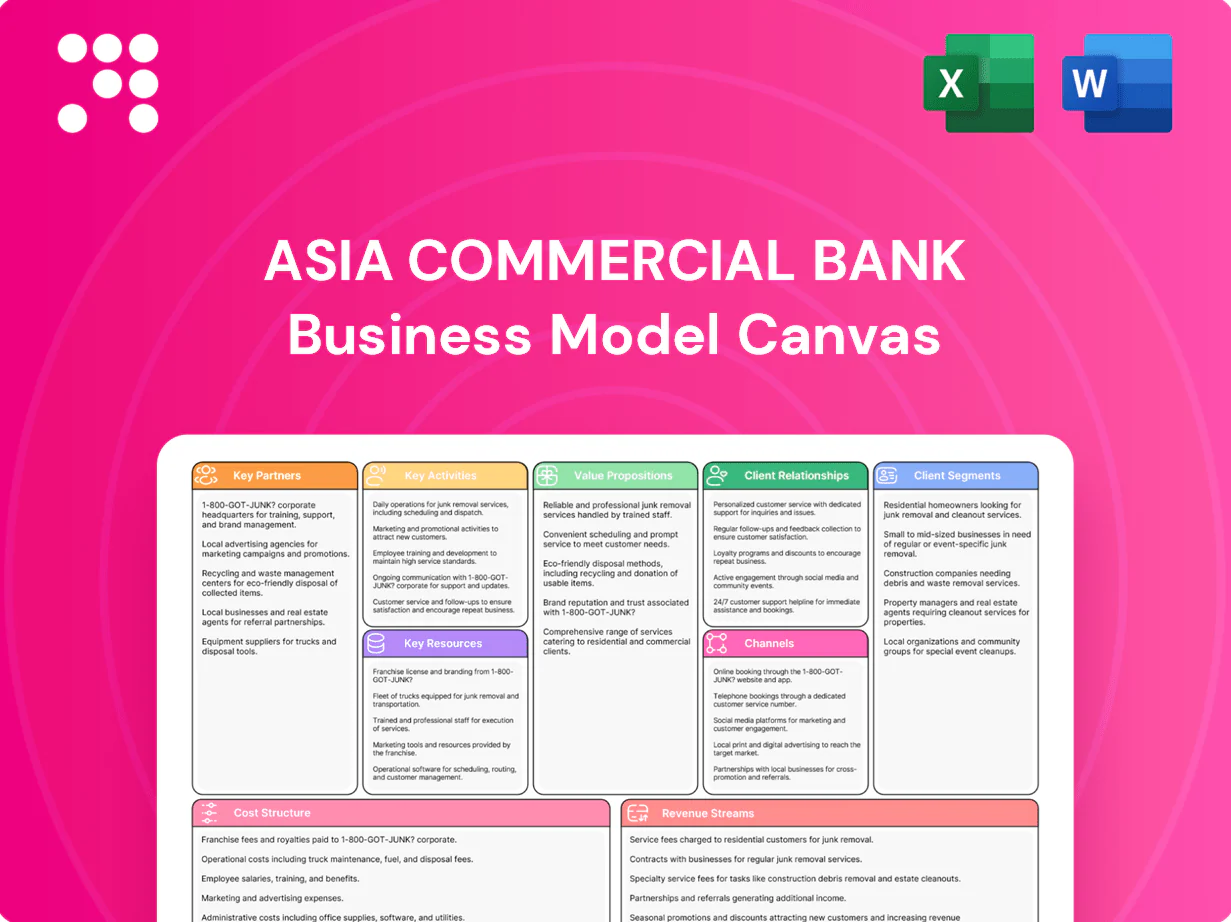

A comprehensive, pre-written Business Model Canvas for Asia Commercial Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships with strategic insights, competitive advantages and linked SWOT analysis—designed for presentations, funding discussions and informed decision‑making by entrepreneurs, analysts and investors.

High-level view of Asia Commercial Bank’s business model with editable cells to quickly identify core banking components, relieve strategic planning pain points, and accelerate team alignment.

Activities

Deposit & Liquidity Management

Designing competitive deposit products secures stable funding while active ALM balances cost of funds and interest rate risk; daily liquidity monitoring ensures compliance with regulators, including Vietnam’s 2024 LCR minimum of 100%. Marketing campaigns target CASA growth to lower funding costs and improve margins, supported by real-time treasury dashboards and intraday liquidity limits.

Lending & Risk Underwriting

Origination across retail, SME, and corporate lending—accounting for robust loan book growth of about 12% Y/Y in 2024—drives asset expansion. Credit scoring models, collateral management, and risk-based pricing target optimized risk-return and maintain net interest margins. Active portfolio monitoring and collections keep NPLs under 2% and protect asset quality. Regular stress testing (capital buffer planning) informs capital allocation and contingency limits.

Digital Banking Operations

Running mobile and internet platforms enables self-service, with over 50% of retail transactions migrating to digital channels in recent years, reducing branch costs and improving processing speed. Continuous UX enhancements lift engagement and retention, yielding double-digit increases in session time and monthly active users. API integrations support ecosystems and embedded finance, enabling partner flows and scalable third-party onboarding. Incident response and uptime management target 99.9% availability to safeguard customer trust.

Payments & Transaction Services

Payments & Transaction Services at Asia Commercial Bank processes cards, transfers and merchant acquiring to generate fee income while cash management and payroll embed ACB in client workflows; Vietnam non-cash transactions grew ~20% in 2024 per State Bank of Vietnam. FX and trade finance support cross-border commerce; fraud monitoring and dispute handling cut chargebacks and improve reliability.

- 120m+ transactions processed (2024 est.)

- 12k corporate cash management clients

- USD 4.5bn trade finance flow

- 35% reduction in chargebacks (2024)

Compliance & Cybersecurity

Compliance & Cybersecurity: KYC/AML, reporting and conduct controls meet regulatory standards; cyber defense protects customer data and systems—average cost of a data breach in 2024 was $4.45M (IBM); training and audits reinforce a risk-aware culture; vendor and third-party risk oversight reduces exposure.

- KYC/AML & reporting

- Cyber defense & data protection

- Training, audits, culture

- Vendor/third-party oversight

Stable funding: LCR ≥100%, 12% loan growth, 120m payments, NPLs <2%

Designing deposit products and active ALM ensure funding stability and 2024 LCR ≥100%; targeted CASA campaigns and real-time treasury lower funding costs. Lending origination grew ~12% Y/Y in 2024 with NPLs <2% via risk-based pricing and stress tests. Digital channels (50%+ transactions) and payments (120m txns, USD4.5bn trade) drive fee income; cybersecurity and KYC/AML uphold compliance.

| Metric | 2024 |

|---|---|

| Transactions | 120m+ |

| Loan growth | ~12% Y/Y |

| NPLs | <2% |

| Trade finance flow | USD 4.5bn |

| LCR | ≥100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Asia Commercial Bank Business Model Canvas, not a mockup or sample. It shows real content and layout exactly as delivered. After purchase you’ll receive this same file in full, ready to edit and present. No surprises—what you see is what you get.

Unlock a bank Business Model Canvas — editable Word/Excel for investors & strategists

Unlock the full strategic blueprint behind Asia Commercial Bank with our Business Model Canvas—detailed, company-specific insights into customer segments, revenue streams, partnerships, and growth levers. Ideal for investors, consultants, and founders; download the editable Word/Excel file to benchmark, plan, and act today.

Partnerships

State Bank & Regulators

Partnership with the State Bank of Vietnam ensures compliance, liquidity access and policy alignment, leveraging SBV oversight of a banking system with total assets exceeding $1 trillion in 2024 and foreign-exchange reserves above $80 billion. It enables Asia Commercial Bank to participate in interbank markets and national payment systems. Close coordination cuts regulatory risk and speeds new-product approvals, strengthening trust with institutional clients.

Payment & Card Networks

Alliances with Visa, Mastercard and local NAPAS enable ACB to issue cards and acquire merchants across networks that together serve over 5 billion cards worldwide and NAPAS processing exceeding 1 billion transactions annually, expanding acceptance and driving card fee income. Joint risk controls with network-level fraud scoring and tokenization have cut chargeback rates where deployed, strengthening loss prevention. Co-branded programs with merchants and wallets accelerate digital payments adoption, lifting contactless and e-commerce volumes significantly year-over-year.

Fintech & Technology Vendors

API partners and core banking providers enhance mobile, online and analytics capabilities, accelerating feature rollout by 30–50% and lowering development risk; cloud and cybersecurity vendors, with APAC cloud adoption ~60% in 2024, boost resilience and compliance; KYC providers can cut onboarding costs by up to 40%; sandbox pilots shorten time-to-market roughly 25–40%.

Corporate & Institutional Partners

Treasury partners, insurers and asset managers widen ACB’s product breadth, enabling bundled cash management, bancassurance and investment solutions that deepen client share of wallet; correspondent banks support cross-border trade and remittances (global remittances to low‑ and middle‑income countries were $626 billion in 2023), while co‑origination deals expand lending reach into SME segments.

- Treasury partners: liquidity & FX products

- Insurers: bancassurance for fee income

- Asset managers: managed solutions & AUM growth

- Correspondent banks: cross‑border corridors, remittances

- Co‑origination: extended SME loan distribution

Agents & Distribution Allies

Agents and distribution allies — ATM networks, payment agents and retail chains — extend Asia Commercial Bank last-mile service, lowering capex per outlet and improving accessibility across urban and rural areas.

Alliances with employers and universities secure payroll flows and student acquisition channels, while partnerships with real estate developers and auto dealers feed secured lending pipelines and boost loan originations.

- ATM networks expand reach

- Payment agents reduce capex

- Employer/university payrolls grow deposits

- Developers/dealers increase secured loans

Vietnam banks tap SBV, NAPAS and global card rails to speed payments and remittances

ACB leverages SBV oversight (Vietnam banking assets >$1T in 2024; FX reserves >$80B) for liquidity and regulatory alignment. Card/NAPAS ties (NAPAS >1B tx/yr; global cards >5B) expand payments and fee income. Tech, treasury, insurer and correspondent partners cut onboarding by ~40%, speed rollouts 30–50% and support remittances ($626B global, 2023).

| Partner | Metric | 2024/2023 |

|---|---|---|

| SBV | Banking assets | >$1T (2024) |

| NAPAS | Transactions | >1B/yr |

| Card networks | Cards | >5B global |

| Remittances | Global flow | $626B (2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Asia Commercial Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships with strategic insights, competitive advantages and linked SWOT analysis—designed for presentations, funding discussions and informed decision‑making by entrepreneurs, analysts and investors.

High-level view of Asia Commercial Bank’s business model with editable cells to quickly identify core banking components, relieve strategic planning pain points, and accelerate team alignment.

Activities

Deposit & Liquidity Management

Designing competitive deposit products secures stable funding while active ALM balances cost of funds and interest rate risk; daily liquidity monitoring ensures compliance with regulators, including Vietnam’s 2024 LCR minimum of 100%. Marketing campaigns target CASA growth to lower funding costs and improve margins, supported by real-time treasury dashboards and intraday liquidity limits.

Lending & Risk Underwriting

Origination across retail, SME, and corporate lending—accounting for robust loan book growth of about 12% Y/Y in 2024—drives asset expansion. Credit scoring models, collateral management, and risk-based pricing target optimized risk-return and maintain net interest margins. Active portfolio monitoring and collections keep NPLs under 2% and protect asset quality. Regular stress testing (capital buffer planning) informs capital allocation and contingency limits.

Digital Banking Operations

Running mobile and internet platforms enables self-service, with over 50% of retail transactions migrating to digital channels in recent years, reducing branch costs and improving processing speed. Continuous UX enhancements lift engagement and retention, yielding double-digit increases in session time and monthly active users. API integrations support ecosystems and embedded finance, enabling partner flows and scalable third-party onboarding. Incident response and uptime management target 99.9% availability to safeguard customer trust.

Payments & Transaction Services

Payments & Transaction Services at Asia Commercial Bank processes cards, transfers and merchant acquiring to generate fee income while cash management and payroll embed ACB in client workflows; Vietnam non-cash transactions grew ~20% in 2024 per State Bank of Vietnam. FX and trade finance support cross-border commerce; fraud monitoring and dispute handling cut chargebacks and improve reliability.

- 120m+ transactions processed (2024 est.)

- 12k corporate cash management clients

- USD 4.5bn trade finance flow

- 35% reduction in chargebacks (2024)

Compliance & Cybersecurity

Compliance & Cybersecurity: KYC/AML, reporting and conduct controls meet regulatory standards; cyber defense protects customer data and systems—average cost of a data breach in 2024 was $4.45M (IBM); training and audits reinforce a risk-aware culture; vendor and third-party risk oversight reduces exposure.

- KYC/AML & reporting

- Cyber defense & data protection

- Training, audits, culture

- Vendor/third-party oversight

Stable funding: LCR ≥100%, 12% loan growth, 120m payments, NPLs <2%

Designing deposit products and active ALM ensure funding stability and 2024 LCR ≥100%; targeted CASA campaigns and real-time treasury lower funding costs. Lending origination grew ~12% Y/Y in 2024 with NPLs <2% via risk-based pricing and stress tests. Digital channels (50%+ transactions) and payments (120m txns, USD4.5bn trade) drive fee income; cybersecurity and KYC/AML uphold compliance.

| Metric | 2024 |

|---|---|

| Transactions | 120m+ |

| Loan growth | ~12% Y/Y |

| NPLs | <2% |

| Trade finance flow | USD 4.5bn |

| LCR | ≥100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Asia Commercial Bank Business Model Canvas, not a mockup or sample. It shows real content and layout exactly as delivered. After purchase you’ll receive this same file in full, ready to edit and present. No surprises—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a bank Business Model Canvas — editable Word/Excel for investors & strategists

Unlock the full strategic blueprint behind Asia Commercial Bank with our Business Model Canvas—detailed, company-specific insights into customer segments, revenue streams, partnerships, and growth levers. Ideal for investors, consultants, and founders; download the editable Word/Excel file to benchmark, plan, and act today.

Partnerships

State Bank & Regulators

Partnership with the State Bank of Vietnam ensures compliance, liquidity access and policy alignment, leveraging SBV oversight of a banking system with total assets exceeding $1 trillion in 2024 and foreign-exchange reserves above $80 billion. It enables Asia Commercial Bank to participate in interbank markets and national payment systems. Close coordination cuts regulatory risk and speeds new-product approvals, strengthening trust with institutional clients.

Payment & Card Networks

Alliances with Visa, Mastercard and local NAPAS enable ACB to issue cards and acquire merchants across networks that together serve over 5 billion cards worldwide and NAPAS processing exceeding 1 billion transactions annually, expanding acceptance and driving card fee income. Joint risk controls with network-level fraud scoring and tokenization have cut chargeback rates where deployed, strengthening loss prevention. Co-branded programs with merchants and wallets accelerate digital payments adoption, lifting contactless and e-commerce volumes significantly year-over-year.

Fintech & Technology Vendors

API partners and core banking providers enhance mobile, online and analytics capabilities, accelerating feature rollout by 30–50% and lowering development risk; cloud and cybersecurity vendors, with APAC cloud adoption ~60% in 2024, boost resilience and compliance; KYC providers can cut onboarding costs by up to 40%; sandbox pilots shorten time-to-market roughly 25–40%.

Corporate & Institutional Partners

Treasury partners, insurers and asset managers widen ACB’s product breadth, enabling bundled cash management, bancassurance and investment solutions that deepen client share of wallet; correspondent banks support cross-border trade and remittances (global remittances to low‑ and middle‑income countries were $626 billion in 2023), while co‑origination deals expand lending reach into SME segments.

- Treasury partners: liquidity & FX products

- Insurers: bancassurance for fee income

- Asset managers: managed solutions & AUM growth

- Correspondent banks: cross‑border corridors, remittances

- Co‑origination: extended SME loan distribution

Agents & Distribution Allies

Agents and distribution allies — ATM networks, payment agents and retail chains — extend Asia Commercial Bank last-mile service, lowering capex per outlet and improving accessibility across urban and rural areas.

Alliances with employers and universities secure payroll flows and student acquisition channels, while partnerships with real estate developers and auto dealers feed secured lending pipelines and boost loan originations.

- ATM networks expand reach

- Payment agents reduce capex

- Employer/university payrolls grow deposits

- Developers/dealers increase secured loans

Vietnam banks tap SBV, NAPAS and global card rails to speed payments and remittances

ACB leverages SBV oversight (Vietnam banking assets >$1T in 2024; FX reserves >$80B) for liquidity and regulatory alignment. Card/NAPAS ties (NAPAS >1B tx/yr; global cards >5B) expand payments and fee income. Tech, treasury, insurer and correspondent partners cut onboarding by ~40%, speed rollouts 30–50% and support remittances ($626B global, 2023).

| Partner | Metric | 2024/2023 |

|---|---|---|

| SBV | Banking assets | >$1T (2024) |

| NAPAS | Transactions | >1B/yr |

| Card networks | Cards | >5B global |

| Remittances | Global flow | $626B (2023) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Asia Commercial Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships with strategic insights, competitive advantages and linked SWOT analysis—designed for presentations, funding discussions and informed decision‑making by entrepreneurs, analysts and investors.

High-level view of Asia Commercial Bank’s business model with editable cells to quickly identify core banking components, relieve strategic planning pain points, and accelerate team alignment.

Activities

Deposit & Liquidity Management

Designing competitive deposit products secures stable funding while active ALM balances cost of funds and interest rate risk; daily liquidity monitoring ensures compliance with regulators, including Vietnam’s 2024 LCR minimum of 100%. Marketing campaigns target CASA growth to lower funding costs and improve margins, supported by real-time treasury dashboards and intraday liquidity limits.

Lending & Risk Underwriting

Origination across retail, SME, and corporate lending—accounting for robust loan book growth of about 12% Y/Y in 2024—drives asset expansion. Credit scoring models, collateral management, and risk-based pricing target optimized risk-return and maintain net interest margins. Active portfolio monitoring and collections keep NPLs under 2% and protect asset quality. Regular stress testing (capital buffer planning) informs capital allocation and contingency limits.

Digital Banking Operations

Running mobile and internet platforms enables self-service, with over 50% of retail transactions migrating to digital channels in recent years, reducing branch costs and improving processing speed. Continuous UX enhancements lift engagement and retention, yielding double-digit increases in session time and monthly active users. API integrations support ecosystems and embedded finance, enabling partner flows and scalable third-party onboarding. Incident response and uptime management target 99.9% availability to safeguard customer trust.

Payments & Transaction Services

Payments & Transaction Services at Asia Commercial Bank processes cards, transfers and merchant acquiring to generate fee income while cash management and payroll embed ACB in client workflows; Vietnam non-cash transactions grew ~20% in 2024 per State Bank of Vietnam. FX and trade finance support cross-border commerce; fraud monitoring and dispute handling cut chargebacks and improve reliability.

- 120m+ transactions processed (2024 est.)

- 12k corporate cash management clients

- USD 4.5bn trade finance flow

- 35% reduction in chargebacks (2024)

Compliance & Cybersecurity

Compliance & Cybersecurity: KYC/AML, reporting and conduct controls meet regulatory standards; cyber defense protects customer data and systems—average cost of a data breach in 2024 was $4.45M (IBM); training and audits reinforce a risk-aware culture; vendor and third-party risk oversight reduces exposure.

- KYC/AML & reporting

- Cyber defense & data protection

- Training, audits, culture

- Vendor/third-party oversight

Stable funding: LCR ≥100%, 12% loan growth, 120m payments, NPLs <2%

Designing deposit products and active ALM ensure funding stability and 2024 LCR ≥100%; targeted CASA campaigns and real-time treasury lower funding costs. Lending origination grew ~12% Y/Y in 2024 with NPLs <2% via risk-based pricing and stress tests. Digital channels (50%+ transactions) and payments (120m txns, USD4.5bn trade) drive fee income; cybersecurity and KYC/AML uphold compliance.

| Metric | 2024 |

|---|---|

| Transactions | 120m+ |

| Loan growth | ~12% Y/Y |

| NPLs | <2% |

| Trade finance flow | USD 4.5bn |

| LCR | ≥100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Asia Commercial Bank Business Model Canvas, not a mockup or sample. It shows real content and layout exactly as delivered. After purchase you’ll receive this same file in full, ready to edit and present. No surprises—what you see is what you get.