Accent Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

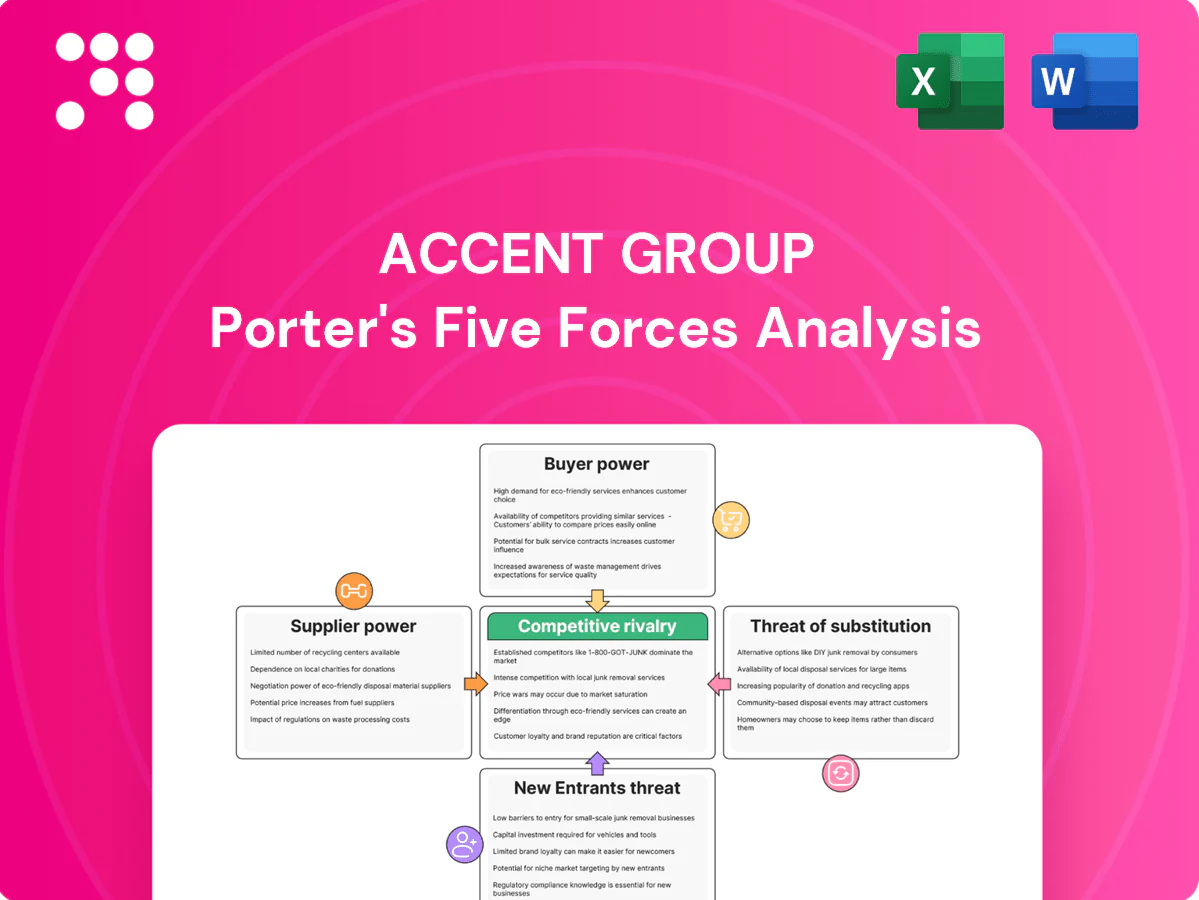

Accent Group faces intense retail competition, rising supplier consolidation, and evolving consumer preferences that pressure margins and growth prospects. This snapshot highlights key pressure points but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to quantify threats, identify strategic levers, and inform investment or strategy. Purchase the complete report for a consultant-grade, actionable breakdown.

Suppliers Bargaining Power

Global brand concentration

Accent Group (ASX: AX1) relies on global brands such as Nike, Vans, New Balance and Skechers that carry strong equity and pricing power. Exclusive distribution deals can blunt supplier leverage, but major brands’ 2024 direct-to-consumer push preserved bargaining power. Supplier choices on assortments, MAP policies and allocations directly affect margins and store traffic. Expanding brand mix and growing own-brand lines is a key hedge.

Exclusive licenses & contracts

Regional exclusivities and long-term distribution rights give Accent Group (ASX:AX1) stable access and predictable terms, supporting its FY24 group sales of A$1.64bn; however contract renewals create renegotiation and performance-clause risk. Strong sell-through, wide retail reach and data-sharing improve Accent’s leverage, yet reliance on a few marquee licenses maintains elevated single-supplier risk.

Multi-channel scale leverage

ASX-listed Accent Group (ASX:AX1) leverages an omnichannel footprint of around 1,000 stores plus growing e-commerce reach, giving suppliers strong visibility and speed-to-market; vendors consistently support co-op marketing and preferred allocations. Scale drives improved payment terms and faster inventory turns, but supplier bargaining is weakened when brands prioritize direct-to-consumer channels.

Switching and assortment flexibility

As of 2024 Accent leverages footwear category adjacency to substitute across brands and styles, enabling rapid SKU rotation and markdown control while flexing shelf space toward higher-margin or faster-selling labels. Private-label and exclusive partnerships lower vendor dependence and improve gross margin mix, yet premium franchises like Nike and Vans remain less substitutable because brand-led demand sustains price and footfall power.

- Category adjacency supports substitution

- Flexed shelf space boosts margin capture

- Private label/exclusives reduce single-vendor risk

- Premium franchises maintain supplier leverage

Supply chain and compliance pressures

Supply chain pressures—lead times often 8–12+ weeks in 2024, volatile freight and FX exposure—shift bargaining toward scarce-capacity suppliers, who can pass through higher costs. ESG, modern slavery and traceability compliance add cost and documentation that suppliers may offset. In-season factory or logistics disruptions can quickly tighten supplier power; collaborative planning and VMI help share risk.

- Lead times: 8–12+ weeks (2024)

- Freight/FX: elevated volatility

- Compliance: ESG/modern slavery traceability costs

- Mitigation: collaborative planning, vendor-managed inventory

Retailer hit by supplier squeeze; FY24 sales A$1.64bn

Accent Group faces elevated supplier power in 2024: marquee brands' DTC push and MAP policies constrain margin control, while exclusives and long-term rights provide stability; FY24 group sales A$1.64bn and ~1,000 stores boost leverage. Lead times 8–12+ weeks and freight/FX volatility increase supplier leverage; private-label expansion mitigates single-supplier risk.

| Metric | Value (2024) |

|---|---|

| FY24 group sales | A$1.64bn |

| Stores | ~1,000 |

| Lead times | 8–12+ weeks |

| Supplier risk | High for marquee brands |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Accent Group, revealing competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic barriers that shape its pricing, profitability and market positioning.

Clear one-sheet Porter's Five Forces for Accent Group—instantly highlights supplier/buyer power, rivalry, substitutes and entry threats to speed strategic decisions. Editable pressure levels and an exportable radar chart let you model scenarios and drop visuals into decks without extra setup.

Customers Bargaining Power

Low switching costs

Low switching costs mean consumers can easily compare prices and availability across retailers and brand DTC sites, with ~75% of shoppers checking multiple sites before buying in 2024, intensifying price sensitivity for commoditized styles. Exclusive colorways and limited drops partially reduce substitution by creating scarcity premiums. Seamless returns and fast fulfillment remain critical to retain loyalty and repeat purchases.

Price transparency online

Price transparency via marketplace listings and price-matching norms compress Accent Group gross margins, contributing to reported FY24 revenue of AUD 1.32bn and tighter margin pressure. Promotional calendars train customers to wait for deals, lowering full-price sell-through. Dynamic pricing and loyalty personalization can protect AURs on core SKUs, while differentiated service and fit expertise justify higher full-price conversion.

Omnichannel service expectations

Shoppers now treat BOPIS, fast delivery and easy returns as table stakes, with 84% of consumers in a 2024 Salesforce survey saying experience is as important as product; missed SLAs drive higher churn and refund rates. Investment in last-mile logistics and real-time inventory visibility measurably cuts friction and returns. Superior CX lets Accent Group sustain modest price gaps vs competitors while preserving market share.

Wholesale customer influence

As a distributor, Accent’s retail partners can exert volume and timing pressure, with FY24 group revenue of AUD 1.68bn concentrating negotiating power in larger chains that secure sharper margins and increased marketing support. Sell-through data sharing in 2024 improved joint planning but also exposed underperforming lines to buyers. Diversifying accounts reduced reliance on any single wholesaler and softened pricing leverage.

- Wholesale concentration: major chains drive terms

- FY24 revenue: AUD 1.68bn

- Data sharing: improves planning, increases transparency

- Diversification: lowers single-buyer risk

Loyalty and exclusivity dampeners

Loyalty programs, exclusive drops and limited editions raise perceived switching costs—members often spend ~20% more and limited releases can command 1.5–3x secondary-market premiums, strengthening Accent Group’s customer hold. Curated brand communities deepen engagement beyond price, but hype cycles are volatile and can reverse within months. Consistent newness and allocation access are key to sustaining stickiness.

- membership: ~20% higher spend

- exclusive drops: 1.5–3x resale

- community: engagement > price

- risk: hype can reverse fast

Customers compare: ~75% — experience 84% — members +20% spend

Customers have high bargaining power due to low switching costs and price transparency—~75% check multiple sites in 2024—pressuring AURs and margins despite FY24 retail revenue AUD 1.32bn. Experience expectations (84% in 2024) make delivery/returns critical to retention. Wholesale buyers concentrate leverage (group revenue AUD 1.68bn), while loyalty lifts spend ~20% and exclusive drops yield 1.5–3x resale premiums.

| Metric | 2024 Value |

|---|---|

| Shoppers comparing sites | ~75% |

| Experience importance (Salesforce) | 84% |

| Retail FY24 revenue | AUD 1.32bn |

| Group FY24 revenue | AUD 1.68bn |

| Member premium | ~20% higher spend |

| Exclusive resale | 1.5–3x |

Preview Before You Purchase

Accent Group Porter's Five Forces Analysis

This preview of the Accent Group Porter's Five Forces Analysis is the exact, fully formatted document you’ll receive upon purchase—no placeholders or samples. It contains the complete analysis ready for download and immediate use. Purchase grants instant access to this same file, prepared for professional use.

Don't Miss the Bigger Picture

Accent Group faces intense retail competition, rising supplier consolidation, and evolving consumer preferences that pressure margins and growth prospects. This snapshot highlights key pressure points but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to quantify threats, identify strategic levers, and inform investment or strategy. Purchase the complete report for a consultant-grade, actionable breakdown.

Suppliers Bargaining Power

Global brand concentration

Accent Group (ASX: AX1) relies on global brands such as Nike, Vans, New Balance and Skechers that carry strong equity and pricing power. Exclusive distribution deals can blunt supplier leverage, but major brands’ 2024 direct-to-consumer push preserved bargaining power. Supplier choices on assortments, MAP policies and allocations directly affect margins and store traffic. Expanding brand mix and growing own-brand lines is a key hedge.

Exclusive licenses & contracts

Regional exclusivities and long-term distribution rights give Accent Group (ASX:AX1) stable access and predictable terms, supporting its FY24 group sales of A$1.64bn; however contract renewals create renegotiation and performance-clause risk. Strong sell-through, wide retail reach and data-sharing improve Accent’s leverage, yet reliance on a few marquee licenses maintains elevated single-supplier risk.

Multi-channel scale leverage

ASX-listed Accent Group (ASX:AX1) leverages an omnichannel footprint of around 1,000 stores plus growing e-commerce reach, giving suppliers strong visibility and speed-to-market; vendors consistently support co-op marketing and preferred allocations. Scale drives improved payment terms and faster inventory turns, but supplier bargaining is weakened when brands prioritize direct-to-consumer channels.

Switching and assortment flexibility

As of 2024 Accent leverages footwear category adjacency to substitute across brands and styles, enabling rapid SKU rotation and markdown control while flexing shelf space toward higher-margin or faster-selling labels. Private-label and exclusive partnerships lower vendor dependence and improve gross margin mix, yet premium franchises like Nike and Vans remain less substitutable because brand-led demand sustains price and footfall power.

- Category adjacency supports substitution

- Flexed shelf space boosts margin capture

- Private label/exclusives reduce single-vendor risk

- Premium franchises maintain supplier leverage

Supply chain and compliance pressures

Supply chain pressures—lead times often 8–12+ weeks in 2024, volatile freight and FX exposure—shift bargaining toward scarce-capacity suppliers, who can pass through higher costs. ESG, modern slavery and traceability compliance add cost and documentation that suppliers may offset. In-season factory or logistics disruptions can quickly tighten supplier power; collaborative planning and VMI help share risk.

- Lead times: 8–12+ weeks (2024)

- Freight/FX: elevated volatility

- Compliance: ESG/modern slavery traceability costs

- Mitigation: collaborative planning, vendor-managed inventory

Retailer hit by supplier squeeze; FY24 sales A$1.64bn

Accent Group faces elevated supplier power in 2024: marquee brands' DTC push and MAP policies constrain margin control, while exclusives and long-term rights provide stability; FY24 group sales A$1.64bn and ~1,000 stores boost leverage. Lead times 8–12+ weeks and freight/FX volatility increase supplier leverage; private-label expansion mitigates single-supplier risk.

| Metric | Value (2024) |

|---|---|

| FY24 group sales | A$1.64bn |

| Stores | ~1,000 |

| Lead times | 8–12+ weeks |

| Supplier risk | High for marquee brands |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Accent Group, revealing competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic barriers that shape its pricing, profitability and market positioning.

Clear one-sheet Porter's Five Forces for Accent Group—instantly highlights supplier/buyer power, rivalry, substitutes and entry threats to speed strategic decisions. Editable pressure levels and an exportable radar chart let you model scenarios and drop visuals into decks without extra setup.

Customers Bargaining Power

Low switching costs

Low switching costs mean consumers can easily compare prices and availability across retailers and brand DTC sites, with ~75% of shoppers checking multiple sites before buying in 2024, intensifying price sensitivity for commoditized styles. Exclusive colorways and limited drops partially reduce substitution by creating scarcity premiums. Seamless returns and fast fulfillment remain critical to retain loyalty and repeat purchases.

Price transparency online

Price transparency via marketplace listings and price-matching norms compress Accent Group gross margins, contributing to reported FY24 revenue of AUD 1.32bn and tighter margin pressure. Promotional calendars train customers to wait for deals, lowering full-price sell-through. Dynamic pricing and loyalty personalization can protect AURs on core SKUs, while differentiated service and fit expertise justify higher full-price conversion.

Omnichannel service expectations

Shoppers now treat BOPIS, fast delivery and easy returns as table stakes, with 84% of consumers in a 2024 Salesforce survey saying experience is as important as product; missed SLAs drive higher churn and refund rates. Investment in last-mile logistics and real-time inventory visibility measurably cuts friction and returns. Superior CX lets Accent Group sustain modest price gaps vs competitors while preserving market share.

Wholesale customer influence

As a distributor, Accent’s retail partners can exert volume and timing pressure, with FY24 group revenue of AUD 1.68bn concentrating negotiating power in larger chains that secure sharper margins and increased marketing support. Sell-through data sharing in 2024 improved joint planning but also exposed underperforming lines to buyers. Diversifying accounts reduced reliance on any single wholesaler and softened pricing leverage.

- Wholesale concentration: major chains drive terms

- FY24 revenue: AUD 1.68bn

- Data sharing: improves planning, increases transparency

- Diversification: lowers single-buyer risk

Loyalty and exclusivity dampeners

Loyalty programs, exclusive drops and limited editions raise perceived switching costs—members often spend ~20% more and limited releases can command 1.5–3x secondary-market premiums, strengthening Accent Group’s customer hold. Curated brand communities deepen engagement beyond price, but hype cycles are volatile and can reverse within months. Consistent newness and allocation access are key to sustaining stickiness.

- membership: ~20% higher spend

- exclusive drops: 1.5–3x resale

- community: engagement > price

- risk: hype can reverse fast

Customers compare: ~75% — experience 84% — members +20% spend

Customers have high bargaining power due to low switching costs and price transparency—~75% check multiple sites in 2024—pressuring AURs and margins despite FY24 retail revenue AUD 1.32bn. Experience expectations (84% in 2024) make delivery/returns critical to retention. Wholesale buyers concentrate leverage (group revenue AUD 1.68bn), while loyalty lifts spend ~20% and exclusive drops yield 1.5–3x resale premiums.

| Metric | 2024 Value |

|---|---|

| Shoppers comparing sites | ~75% |

| Experience importance (Salesforce) | 84% |

| Retail FY24 revenue | AUD 1.32bn |

| Group FY24 revenue | AUD 1.68bn |

| Member premium | ~20% higher spend |

| Exclusive resale | 1.5–3x |

Preview Before You Purchase

Accent Group Porter's Five Forces Analysis

This preview of the Accent Group Porter's Five Forces Analysis is the exact, fully formatted document you’ll receive upon purchase—no placeholders or samples. It contains the complete analysis ready for download and immediate use. Purchase grants instant access to this same file, prepared for professional use.

Description

Don't Miss the Bigger Picture

Accent Group faces intense retail competition, rising supplier consolidation, and evolving consumer preferences that pressure margins and growth prospects. This snapshot highlights key pressure points but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis to quantify threats, identify strategic levers, and inform investment or strategy. Purchase the complete report for a consultant-grade, actionable breakdown.

Suppliers Bargaining Power

Global brand concentration

Accent Group (ASX: AX1) relies on global brands such as Nike, Vans, New Balance and Skechers that carry strong equity and pricing power. Exclusive distribution deals can blunt supplier leverage, but major brands’ 2024 direct-to-consumer push preserved bargaining power. Supplier choices on assortments, MAP policies and allocations directly affect margins and store traffic. Expanding brand mix and growing own-brand lines is a key hedge.

Exclusive licenses & contracts

Regional exclusivities and long-term distribution rights give Accent Group (ASX:AX1) stable access and predictable terms, supporting its FY24 group sales of A$1.64bn; however contract renewals create renegotiation and performance-clause risk. Strong sell-through, wide retail reach and data-sharing improve Accent’s leverage, yet reliance on a few marquee licenses maintains elevated single-supplier risk.

Multi-channel scale leverage

ASX-listed Accent Group (ASX:AX1) leverages an omnichannel footprint of around 1,000 stores plus growing e-commerce reach, giving suppliers strong visibility and speed-to-market; vendors consistently support co-op marketing and preferred allocations. Scale drives improved payment terms and faster inventory turns, but supplier bargaining is weakened when brands prioritize direct-to-consumer channels.

Switching and assortment flexibility

As of 2024 Accent leverages footwear category adjacency to substitute across brands and styles, enabling rapid SKU rotation and markdown control while flexing shelf space toward higher-margin or faster-selling labels. Private-label and exclusive partnerships lower vendor dependence and improve gross margin mix, yet premium franchises like Nike and Vans remain less substitutable because brand-led demand sustains price and footfall power.

- Category adjacency supports substitution

- Flexed shelf space boosts margin capture

- Private label/exclusives reduce single-vendor risk

- Premium franchises maintain supplier leverage

Supply chain and compliance pressures

Supply chain pressures—lead times often 8–12+ weeks in 2024, volatile freight and FX exposure—shift bargaining toward scarce-capacity suppliers, who can pass through higher costs. ESG, modern slavery and traceability compliance add cost and documentation that suppliers may offset. In-season factory or logistics disruptions can quickly tighten supplier power; collaborative planning and VMI help share risk.

- Lead times: 8–12+ weeks (2024)

- Freight/FX: elevated volatility

- Compliance: ESG/modern slavery traceability costs

- Mitigation: collaborative planning, vendor-managed inventory

Retailer hit by supplier squeeze; FY24 sales A$1.64bn

Accent Group faces elevated supplier power in 2024: marquee brands' DTC push and MAP policies constrain margin control, while exclusives and long-term rights provide stability; FY24 group sales A$1.64bn and ~1,000 stores boost leverage. Lead times 8–12+ weeks and freight/FX volatility increase supplier leverage; private-label expansion mitigates single-supplier risk.

| Metric | Value (2024) |

|---|---|

| FY24 group sales | A$1.64bn |

| Stores | ~1,000 |

| Lead times | 8–12+ weeks |

| Supplier risk | High for marquee brands |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Accent Group, revealing competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic barriers that shape its pricing, profitability and market positioning.

Clear one-sheet Porter's Five Forces for Accent Group—instantly highlights supplier/buyer power, rivalry, substitutes and entry threats to speed strategic decisions. Editable pressure levels and an exportable radar chart let you model scenarios and drop visuals into decks without extra setup.

Customers Bargaining Power

Low switching costs

Low switching costs mean consumers can easily compare prices and availability across retailers and brand DTC sites, with ~75% of shoppers checking multiple sites before buying in 2024, intensifying price sensitivity for commoditized styles. Exclusive colorways and limited drops partially reduce substitution by creating scarcity premiums. Seamless returns and fast fulfillment remain critical to retain loyalty and repeat purchases.

Price transparency online

Price transparency via marketplace listings and price-matching norms compress Accent Group gross margins, contributing to reported FY24 revenue of AUD 1.32bn and tighter margin pressure. Promotional calendars train customers to wait for deals, lowering full-price sell-through. Dynamic pricing and loyalty personalization can protect AURs on core SKUs, while differentiated service and fit expertise justify higher full-price conversion.

Omnichannel service expectations

Shoppers now treat BOPIS, fast delivery and easy returns as table stakes, with 84% of consumers in a 2024 Salesforce survey saying experience is as important as product; missed SLAs drive higher churn and refund rates. Investment in last-mile logistics and real-time inventory visibility measurably cuts friction and returns. Superior CX lets Accent Group sustain modest price gaps vs competitors while preserving market share.

Wholesale customer influence

As a distributor, Accent’s retail partners can exert volume and timing pressure, with FY24 group revenue of AUD 1.68bn concentrating negotiating power in larger chains that secure sharper margins and increased marketing support. Sell-through data sharing in 2024 improved joint planning but also exposed underperforming lines to buyers. Diversifying accounts reduced reliance on any single wholesaler and softened pricing leverage.

- Wholesale concentration: major chains drive terms

- FY24 revenue: AUD 1.68bn

- Data sharing: improves planning, increases transparency

- Diversification: lowers single-buyer risk

Loyalty and exclusivity dampeners

Loyalty programs, exclusive drops and limited editions raise perceived switching costs—members often spend ~20% more and limited releases can command 1.5–3x secondary-market premiums, strengthening Accent Group’s customer hold. Curated brand communities deepen engagement beyond price, but hype cycles are volatile and can reverse within months. Consistent newness and allocation access are key to sustaining stickiness.

- membership: ~20% higher spend

- exclusive drops: 1.5–3x resale

- community: engagement > price

- risk: hype can reverse fast

Customers compare: ~75% — experience 84% — members +20% spend

Customers have high bargaining power due to low switching costs and price transparency—~75% check multiple sites in 2024—pressuring AURs and margins despite FY24 retail revenue AUD 1.32bn. Experience expectations (84% in 2024) make delivery/returns critical to retention. Wholesale buyers concentrate leverage (group revenue AUD 1.68bn), while loyalty lifts spend ~20% and exclusive drops yield 1.5–3x resale premiums.

| Metric | 2024 Value |

|---|---|

| Shoppers comparing sites | ~75% |

| Experience importance (Salesforce) | 84% |

| Retail FY24 revenue | AUD 1.32bn |

| Group FY24 revenue | AUD 1.68bn |

| Member premium | ~20% higher spend |

| Exclusive resale | 1.5–3x |

Preview Before You Purchase

Accent Group Porter's Five Forces Analysis

This preview of the Accent Group Porter's Five Forces Analysis is the exact, fully formatted document you’ll receive upon purchase—no placeholders or samples. It contains the complete analysis ready for download and immediate use. Purchase grants instant access to this same file, prepared for professional use.