AccorHotels Porter's Five Forces Analysis

Don't Miss the Bigger Picture

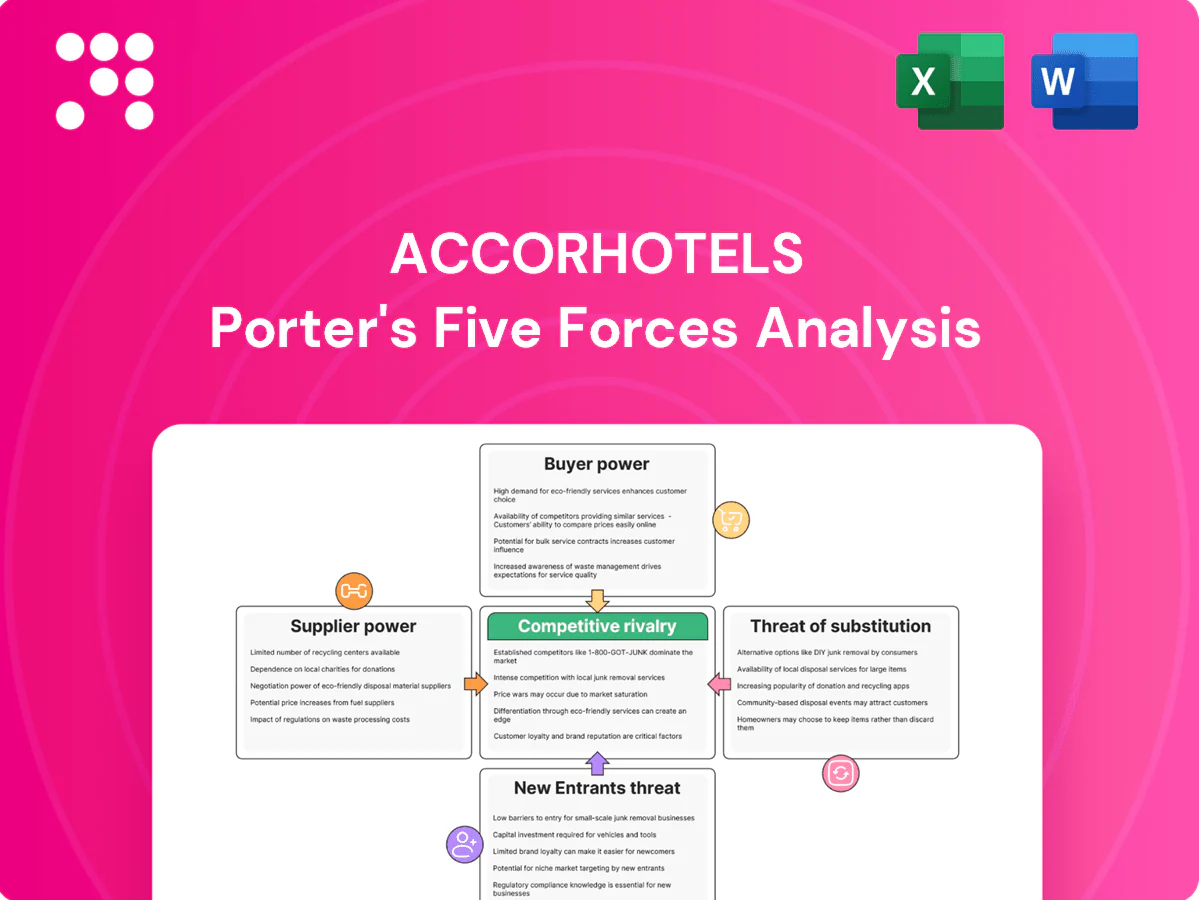

AccorHotels faces moderate bargaining power from corporate buyers, high rivalry across global brands, and growing threat from alternative-stay platforms and lifestyle entrants. Supplier influence and regulatory pressures vary by region, shaping margins and expansion. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AccorHotels’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented F&B and amenities

Food, beverage, linens and amenities suppliers are numerous, limiting individual supplier leverage. Accor's scale—around 5,600 hotels in 110 countries in 2024—allows multisourcing and volume-driven discounts across brands and regions. Premium and sustainable inputs have tightened supply and can raise costs by roughly 15–25% in industry benchmarks. Long-term contracts mitigate volatility but lock in prices and reduce sourcing flexibility.

Property owners and developers

In Accor’s managed and franchised models, property owners supply the room inventory and prime-location landlords can command higher fees and returns; Accor operates over 5,000 hotels across about 110 countries, improving its matchmaking with owners. The group’s brand depth helps secure deals, but trophy assets remain scarce and competing global flags push up acquisition and management bids. This drives tighter owner leverage in key markets.

Technology stack dependence

PMS, CRS, channel managers and cybersecurity vendors create strong switching costs for Accor given integration complexity and data migration risks across its ~5,300 hotels (2024), raising supplier bargaining power. Accor’s in-house digital teams and proprietary integrations help mitigate dependence, while vendor diversification and adoption of open APIs reduce lock-in and lower long-term supplier leverage.

Labor and service contractors

Housekeeping, security and maintenance are often outsourced, and rising wage floors and tighter labor markets plus stronger union activity in 2024 have increased supplier bargaining power; standardization and training programs broaden the vendor base while automation and productivity tools partially offset cost pressure.

- Outsourcing: increases flexibility

- Labor tightness: boosts supplier leverage

- Standardization: enlarges vendor pool

- Automation: reduces labor cost exposure

Renovation and capex partners

Designers, contractors and FF&E suppliers are pivotal to Accor brand standards and repositionings; FF&E lead times rose up to 30% in 2021–24, pushing capex and timelines higher.

Framework agreements and preferred-vendor programs materially lower procurement uncertainty and cost volatility, while unique luxury designs limit substitutability and boost niche supplier leverage.

- Designers: brand compliance risk

- Contractors: schedule/cost pressure

- FF&E: lead-times +30% (2021–24)

- Frameworks: lower uncertainty

- Luxury design: higher supplier power

Scale limits supplier power; FF&E lead times +30% and landlords retain leverage

Supplier power is moderate: Accor’s scale (≈5,600 hotels, 110 countries) enables multisourcing and volume discounts, reducing single-supplier leverage. Niche suppliers (luxury FF&E, designers) and tech vendors raise switching costs; FF&E lead times +30% (2021–24) and premium input inflation +15–25% increase costs. Outsourcing and frameworks limit volatility but landlords and trophy assets retain bargaining strength.

| Supplier | Power | Metric |

|---|---|---|

| Food/amenities | Low | Multisourcing, scale |

| FF&E/design | High | Lead times +30% |

| Tech vendors | Moderate | ~5,300 integrated hotels |

| Landlords | High | Trophy asset scarcity |

What is included in the product

Comprehensive Porter's Five Forces analysis of AccorHotels identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus disruptive trends and entry barriers that shape its pricing, margins and strategic positioning.

A clear one-sheet summary of AccorHotels' five competitive forces—fast insight into threats and opportunities for pricing, expansion and partnership decisions. Swap in current data or scenarios to model impacts of new entrants, regulation or demand shifts without macros or complex tools.

Customers Bargaining Power

Price transparency and OTAs

Metasearch and OTA platforms give guests high price visibility; OTAs account for roughly one-third of hotel bookings and commonly charge 15–25% commission, increasing buyer leverage.

Low switching costs raise customer power as travelers compare rates instantly.

Accor’s direct-book incentives and ALL loyalty, exceeding 70 million members in 2024, aim to cut OTA dependence, while rate parity and targeted offers are critical levers.

Corporate and group contracts

Large corporates, TMCs and MICE buyers extract volume discounts from Accor, leveraging consolidated demand to secure preferred rates and added amenities; Accor’s multi-brand portfolio of about 40 brands across 110 countries boosts RFP win rates by offering global coverage and tailored options. Dynamic pricing and revenue-management systems preserve yield on peak dates, limiting customer bargaining power.

Loyalty program influence

Accor Live Limitless (ALL) — over 70 million members by 2024 — deepens engagement and raises repeat stays, strengthening buyer leverage but lowering churn. Points, tiered status and partner benefits reduce switching and price sensitivity. Elite expectations elevate service and operational costs for loyalty guests. Targeted personalization and ancillary upsells boost margin per stay, improving unit economics.

Experience and review sensitivity

Guests lean heavily on ratings and social proof—82% consult reviews before booking (Statista 2024) and a one-star drop can cut bookings by up to 9%—so small quality gaps rapidly shift demand to rivals or substitutes; consistent brand standards and fast recovery protocols are therefore vital, while localized offerings and tailored F&B concepts boost perceived value and loyalty.

- Ratings-driven demand: 82% consult reviews (Statista 2024)

- One-star impact: bookings down up to 9%

- Mitigation: strict standards + recovery protocols

- Value uplift: localized F&B and experiences

Segment and region variability

Budget travelers show materially higher price sensitivity than luxury guests; 2024 industry data indicate the economy segment represented about 60% of global room nights, driving stronger discounting pressure on Accor’s midscale/budget brands. Resort, urban and extended‑stay patterns differ in elasticity, with urban business stays less price‑elastic. In emerging markets buyer power is weaker due to fewer alternatives, while seasonality raises bargaining power during shoulder periods.

- Budget segment ≈60% of room nights (2024)

- Urban stays: lower elasticity

- Resort/shoulder: higher bargaining power

- Emerging markets: weaker buyer power

OTA bookings ≈33%, commissions 15–25%, reviews hit demand

High OTA visibility (≈33% bookings; 15–25% commissions) and low switching costs boost customer leverage, offset by Accor’s ALL loyalty (>70m members in 2024) and direct-book incentives. Reviews drive demand (82% consult reviews; −up to 9% bookings per one-star drop). Budget segment (~60% room nights in 2024) increases price sensitivity; corporates/MICE extract volume discounts.

| Metric | 2024 value |

|---|---|

| OTA share | ≈33% |

| ALL members | >70 million |

| Review consult | 82% |

| Budget room nights | ≈60% |

Same Document Delivered

AccorHotels Porter's Five Forces Analysis

This preview shows the exact AccorHotels Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders. The report offers a concise evaluation of industry rivalry, bargaining power of suppliers and buyers, and the threats of new entrants and substitutes, with actionable strategic implications. It's fully formatted and ready for download the moment you buy.

Don't Miss the Bigger Picture

AccorHotels faces moderate bargaining power from corporate buyers, high rivalry across global brands, and growing threat from alternative-stay platforms and lifestyle entrants. Supplier influence and regulatory pressures vary by region, shaping margins and expansion. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AccorHotels’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented F&B and amenities

Food, beverage, linens and amenities suppliers are numerous, limiting individual supplier leverage. Accor's scale—around 5,600 hotels in 110 countries in 2024—allows multisourcing and volume-driven discounts across brands and regions. Premium and sustainable inputs have tightened supply and can raise costs by roughly 15–25% in industry benchmarks. Long-term contracts mitigate volatility but lock in prices and reduce sourcing flexibility.

Property owners and developers

In Accor’s managed and franchised models, property owners supply the room inventory and prime-location landlords can command higher fees and returns; Accor operates over 5,000 hotels across about 110 countries, improving its matchmaking with owners. The group’s brand depth helps secure deals, but trophy assets remain scarce and competing global flags push up acquisition and management bids. This drives tighter owner leverage in key markets.

Technology stack dependence

PMS, CRS, channel managers and cybersecurity vendors create strong switching costs for Accor given integration complexity and data migration risks across its ~5,300 hotels (2024), raising supplier bargaining power. Accor’s in-house digital teams and proprietary integrations help mitigate dependence, while vendor diversification and adoption of open APIs reduce lock-in and lower long-term supplier leverage.

Labor and service contractors

Housekeeping, security and maintenance are often outsourced, and rising wage floors and tighter labor markets plus stronger union activity in 2024 have increased supplier bargaining power; standardization and training programs broaden the vendor base while automation and productivity tools partially offset cost pressure.

- Outsourcing: increases flexibility

- Labor tightness: boosts supplier leverage

- Standardization: enlarges vendor pool

- Automation: reduces labor cost exposure

Renovation and capex partners

Designers, contractors and FF&E suppliers are pivotal to Accor brand standards and repositionings; FF&E lead times rose up to 30% in 2021–24, pushing capex and timelines higher.

Framework agreements and preferred-vendor programs materially lower procurement uncertainty and cost volatility, while unique luxury designs limit substitutability and boost niche supplier leverage.

- Designers: brand compliance risk

- Contractors: schedule/cost pressure

- FF&E: lead-times +30% (2021–24)

- Frameworks: lower uncertainty

- Luxury design: higher supplier power

Scale limits supplier power; FF&E lead times +30% and landlords retain leverage

Supplier power is moderate: Accor’s scale (≈5,600 hotels, 110 countries) enables multisourcing and volume discounts, reducing single-supplier leverage. Niche suppliers (luxury FF&E, designers) and tech vendors raise switching costs; FF&E lead times +30% (2021–24) and premium input inflation +15–25% increase costs. Outsourcing and frameworks limit volatility but landlords and trophy assets retain bargaining strength.

| Supplier | Power | Metric |

|---|---|---|

| Food/amenities | Low | Multisourcing, scale |

| FF&E/design | High | Lead times +30% |

| Tech vendors | Moderate | ~5,300 integrated hotels |

| Landlords | High | Trophy asset scarcity |

What is included in the product

Comprehensive Porter's Five Forces analysis of AccorHotels identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus disruptive trends and entry barriers that shape its pricing, margins and strategic positioning.

A clear one-sheet summary of AccorHotels' five competitive forces—fast insight into threats and opportunities for pricing, expansion and partnership decisions. Swap in current data or scenarios to model impacts of new entrants, regulation or demand shifts without macros or complex tools.

Customers Bargaining Power

Price transparency and OTAs

Metasearch and OTA platforms give guests high price visibility; OTAs account for roughly one-third of hotel bookings and commonly charge 15–25% commission, increasing buyer leverage.

Low switching costs raise customer power as travelers compare rates instantly.

Accor’s direct-book incentives and ALL loyalty, exceeding 70 million members in 2024, aim to cut OTA dependence, while rate parity and targeted offers are critical levers.

Corporate and group contracts

Large corporates, TMCs and MICE buyers extract volume discounts from Accor, leveraging consolidated demand to secure preferred rates and added amenities; Accor’s multi-brand portfolio of about 40 brands across 110 countries boosts RFP win rates by offering global coverage and tailored options. Dynamic pricing and revenue-management systems preserve yield on peak dates, limiting customer bargaining power.

Loyalty program influence

Accor Live Limitless (ALL) — over 70 million members by 2024 — deepens engagement and raises repeat stays, strengthening buyer leverage but lowering churn. Points, tiered status and partner benefits reduce switching and price sensitivity. Elite expectations elevate service and operational costs for loyalty guests. Targeted personalization and ancillary upsells boost margin per stay, improving unit economics.

Experience and review sensitivity

Guests lean heavily on ratings and social proof—82% consult reviews before booking (Statista 2024) and a one-star drop can cut bookings by up to 9%—so small quality gaps rapidly shift demand to rivals or substitutes; consistent brand standards and fast recovery protocols are therefore vital, while localized offerings and tailored F&B concepts boost perceived value and loyalty.

- Ratings-driven demand: 82% consult reviews (Statista 2024)

- One-star impact: bookings down up to 9%

- Mitigation: strict standards + recovery protocols

- Value uplift: localized F&B and experiences

Segment and region variability

Budget travelers show materially higher price sensitivity than luxury guests; 2024 industry data indicate the economy segment represented about 60% of global room nights, driving stronger discounting pressure on Accor’s midscale/budget brands. Resort, urban and extended‑stay patterns differ in elasticity, with urban business stays less price‑elastic. In emerging markets buyer power is weaker due to fewer alternatives, while seasonality raises bargaining power during shoulder periods.

- Budget segment ≈60% of room nights (2024)

- Urban stays: lower elasticity

- Resort/shoulder: higher bargaining power

- Emerging markets: weaker buyer power

OTA bookings ≈33%, commissions 15–25%, reviews hit demand

High OTA visibility (≈33% bookings; 15–25% commissions) and low switching costs boost customer leverage, offset by Accor’s ALL loyalty (>70m members in 2024) and direct-book incentives. Reviews drive demand (82% consult reviews; −up to 9% bookings per one-star drop). Budget segment (~60% room nights in 2024) increases price sensitivity; corporates/MICE extract volume discounts.

| Metric | 2024 value |

|---|---|

| OTA share | ≈33% |

| ALL members | >70 million |

| Review consult | 82% |

| Budget room nights | ≈60% |

Same Document Delivered

AccorHotels Porter's Five Forces Analysis

This preview shows the exact AccorHotels Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders. The report offers a concise evaluation of industry rivalry, bargaining power of suppliers and buyers, and the threats of new entrants and substitutes, with actionable strategic implications. It's fully formatted and ready for download the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

AccorHotels faces moderate bargaining power from corporate buyers, high rivalry across global brands, and growing threat from alternative-stay platforms and lifestyle entrants. Supplier influence and regulatory pressures vary by region, shaping margins and expansion. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AccorHotels’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented F&B and amenities

Food, beverage, linens and amenities suppliers are numerous, limiting individual supplier leverage. Accor's scale—around 5,600 hotels in 110 countries in 2024—allows multisourcing and volume-driven discounts across brands and regions. Premium and sustainable inputs have tightened supply and can raise costs by roughly 15–25% in industry benchmarks. Long-term contracts mitigate volatility but lock in prices and reduce sourcing flexibility.

Property owners and developers

In Accor’s managed and franchised models, property owners supply the room inventory and prime-location landlords can command higher fees and returns; Accor operates over 5,000 hotels across about 110 countries, improving its matchmaking with owners. The group’s brand depth helps secure deals, but trophy assets remain scarce and competing global flags push up acquisition and management bids. This drives tighter owner leverage in key markets.

Technology stack dependence

PMS, CRS, channel managers and cybersecurity vendors create strong switching costs for Accor given integration complexity and data migration risks across its ~5,300 hotels (2024), raising supplier bargaining power. Accor’s in-house digital teams and proprietary integrations help mitigate dependence, while vendor diversification and adoption of open APIs reduce lock-in and lower long-term supplier leverage.

Labor and service contractors

Housekeeping, security and maintenance are often outsourced, and rising wage floors and tighter labor markets plus stronger union activity in 2024 have increased supplier bargaining power; standardization and training programs broaden the vendor base while automation and productivity tools partially offset cost pressure.

- Outsourcing: increases flexibility

- Labor tightness: boosts supplier leverage

- Standardization: enlarges vendor pool

- Automation: reduces labor cost exposure

Renovation and capex partners

Designers, contractors and FF&E suppliers are pivotal to Accor brand standards and repositionings; FF&E lead times rose up to 30% in 2021–24, pushing capex and timelines higher.

Framework agreements and preferred-vendor programs materially lower procurement uncertainty and cost volatility, while unique luxury designs limit substitutability and boost niche supplier leverage.

- Designers: brand compliance risk

- Contractors: schedule/cost pressure

- FF&E: lead-times +30% (2021–24)

- Frameworks: lower uncertainty

- Luxury design: higher supplier power

Scale limits supplier power; FF&E lead times +30% and landlords retain leverage

Supplier power is moderate: Accor’s scale (≈5,600 hotels, 110 countries) enables multisourcing and volume discounts, reducing single-supplier leverage. Niche suppliers (luxury FF&E, designers) and tech vendors raise switching costs; FF&E lead times +30% (2021–24) and premium input inflation +15–25% increase costs. Outsourcing and frameworks limit volatility but landlords and trophy assets retain bargaining strength.

| Supplier | Power | Metric |

|---|---|---|

| Food/amenities | Low | Multisourcing, scale |

| FF&E/design | High | Lead times +30% |

| Tech vendors | Moderate | ~5,300 integrated hotels |

| Landlords | High | Trophy asset scarcity |

What is included in the product

Comprehensive Porter's Five Forces analysis of AccorHotels identifying competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus disruptive trends and entry barriers that shape its pricing, margins and strategic positioning.

A clear one-sheet summary of AccorHotels' five competitive forces—fast insight into threats and opportunities for pricing, expansion and partnership decisions. Swap in current data or scenarios to model impacts of new entrants, regulation or demand shifts without macros or complex tools.

Customers Bargaining Power

Price transparency and OTAs

Metasearch and OTA platforms give guests high price visibility; OTAs account for roughly one-third of hotel bookings and commonly charge 15–25% commission, increasing buyer leverage.

Low switching costs raise customer power as travelers compare rates instantly.

Accor’s direct-book incentives and ALL loyalty, exceeding 70 million members in 2024, aim to cut OTA dependence, while rate parity and targeted offers are critical levers.

Corporate and group contracts

Large corporates, TMCs and MICE buyers extract volume discounts from Accor, leveraging consolidated demand to secure preferred rates and added amenities; Accor’s multi-brand portfolio of about 40 brands across 110 countries boosts RFP win rates by offering global coverage and tailored options. Dynamic pricing and revenue-management systems preserve yield on peak dates, limiting customer bargaining power.

Loyalty program influence

Accor Live Limitless (ALL) — over 70 million members by 2024 — deepens engagement and raises repeat stays, strengthening buyer leverage but lowering churn. Points, tiered status and partner benefits reduce switching and price sensitivity. Elite expectations elevate service and operational costs for loyalty guests. Targeted personalization and ancillary upsells boost margin per stay, improving unit economics.

Experience and review sensitivity

Guests lean heavily on ratings and social proof—82% consult reviews before booking (Statista 2024) and a one-star drop can cut bookings by up to 9%—so small quality gaps rapidly shift demand to rivals or substitutes; consistent brand standards and fast recovery protocols are therefore vital, while localized offerings and tailored F&B concepts boost perceived value and loyalty.

- Ratings-driven demand: 82% consult reviews (Statista 2024)

- One-star impact: bookings down up to 9%

- Mitigation: strict standards + recovery protocols

- Value uplift: localized F&B and experiences

Segment and region variability

Budget travelers show materially higher price sensitivity than luxury guests; 2024 industry data indicate the economy segment represented about 60% of global room nights, driving stronger discounting pressure on Accor’s midscale/budget brands. Resort, urban and extended‑stay patterns differ in elasticity, with urban business stays less price‑elastic. In emerging markets buyer power is weaker due to fewer alternatives, while seasonality raises bargaining power during shoulder periods.

- Budget segment ≈60% of room nights (2024)

- Urban stays: lower elasticity

- Resort/shoulder: higher bargaining power

- Emerging markets: weaker buyer power

OTA bookings ≈33%, commissions 15–25%, reviews hit demand

High OTA visibility (≈33% bookings; 15–25% commissions) and low switching costs boost customer leverage, offset by Accor’s ALL loyalty (>70m members in 2024) and direct-book incentives. Reviews drive demand (82% consult reviews; −up to 9% bookings per one-star drop). Budget segment (~60% room nights in 2024) increases price sensitivity; corporates/MICE extract volume discounts.

| Metric | 2024 value |

|---|---|

| OTA share | ≈33% |

| ALL members | >70 million |

| Review consult | 82% |

| Budget room nights | ≈60% |

Same Document Delivered

AccorHotels Porter's Five Forces Analysis

This preview shows the exact AccorHotels Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders. The report offers a concise evaluation of industry rivalry, bargaining power of suppliers and buyers, and the threats of new entrants and substitutes, with actionable strategic implications. It's fully formatted and ready for download the moment you buy.