Acerinox Porter's Five Forces Analysis

From Overview to Strategy Blueprint

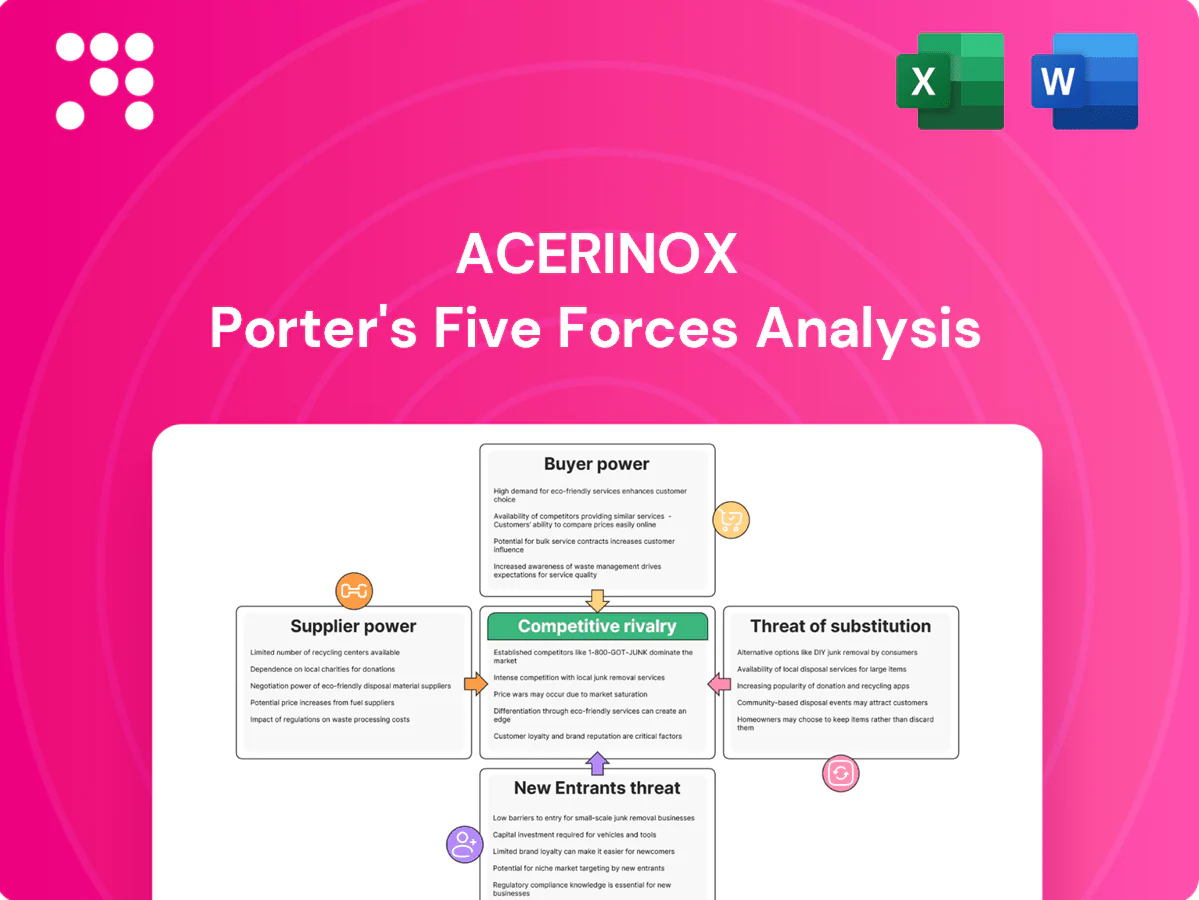

Acerinox faces intense rivalry in stainless steel with cyclical demand and price pressure, while supplier influence is moderate and buyer power significant; substitutes and new entrants pose limited but real risks given capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acerinox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Nickel and ferrochrome reliance

Acerinox relies on a concentrated set of suppliers for nickel, chromium and ferrochrome that are essential for stainless grades, with China supplying roughly 70% of global ferrochrome production. Nickel markets were highly volatile in 2024, with intrayear swings exceeding 20%, creating margin pressure. Long-term contracts and hedging programs partially mitigate price exposure, but limited vertical integration keeps supplier leverage elevated.

Energy cost intensity

Melting (~600 kWh/ton) and hot rolling are power-intensive processes, making Acerinox vulnerable to electricity and gas markets; European industrial electricity averaged ~€0.18/kWh in 2024 and EU ETS carbon prices were near €89/t, directly lifting conversion costs. Regional price volatility erodes pricing power and margins; long-term PPAs and efficiency upgrades cut exposure but cannot eliminate spikes. Suppliers of power and carbon allowances seize leverage during tight markets or rapid carbon-price jumps.

Scrap market volatility

In 2024 stainless and carbon steel scrap remained the primary cyclical inputs for Acerinox, with tight markets elevating input costs and causing mills to prioritize supply to larger buyers. Acerinox’s scale improves access to volumes but cannot fully control market-driven scrap pricing. Limited substitution with virgin inputs is constrained by strict grade specifications, keeping supplier leverage elevated.

Logistics and bulk freight

Bulk ores and alloys require reliable sea freight and port capacity; global seaborne iron ore trade was about 1.6 billion tonnes in 2024, making freight a key cost and timing factor for Acerinox. Freight-rate spikes and port bottlenecks lift delivered input costs and extend lead times, while diversified sourcing and multi-port strategies cut single-point risk. Suppliers frequently pass logistics surcharges through, preserving bargaining leverage.

- Freight share of delivered ore cost: ~10–15% (industry range)

- Seaborne iron ore ~1.6bn t in 2024

- Multi-port/sourcing reduces disruption risk

Environmental compliance costs

Upstream suppliers face tighter ESG and traceability demands in the EU and US, raising verification costs and lead times; EU ETS carbon prices averaged around €90/tCO2 in 2024, adding to input costs. Compliance premiums for certified or low-carbon alloys push stainless feedstock prices higher, while limited low-carbon nickel and chrome supply strengthens supplier pricing power. Acerinox must balance decarbonization targets with cost competitiveness.

- ESG/traceability: higher verification costs

- EU ETS ~€90/tCO2 (2024)

- Premiums for green alloys raise input costs

- Scarce low-carbon Ni/Cr increases supplier power

Concentrated alloy supply, rising energy and carbon costs, and logistics squeeze steelmakers

Suppliers hold elevated leverage: concentrated Ni/Cr/ferrochrome sourcing (China ~70% ferrochrome) and limited vertical integration constrain Acerinox bargaining power.

Energy and carbon cost exposure (EU industrial power ~€0.18/kWh; EU ETS ~€89–90/t in 2024) increases supplier influence via utilities and permits.

Logistics and scrap tightness (seaborne ore ~1.6bn t; freight share ~10–15%) and ESG premiums for low-carbon alloys further strengthen supplier power.

| Metric | 2024 |

|---|---|

| Ferrochrome supply (China) | ~70% |

| Nickel intrayear volatility | >20% |

| EU industrial power | ~€0.18/kWh |

| EU ETS price | €89–90/t |

| Seaborne iron ore | ~1.6bn t |

| Freight share | 10–15% |

What is included in the product

Concise Porter's Five Forces overview for Acerinox, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and market entry barriers that shape its pricing power and profitability.

Concise Acerinox Porter's Five Forces snapshot—instantly reveal competitive pressures with a customizable radar view and clean, copy-ready layout to simplify boardroom decisions and strategic planning.

Customers Bargaining Power

Large OEM concentration

Large OEM concentration in automotive, appliance and machinery drives aggressive negotiation; global vehicle output was about 63 million units in 2023, creating major volume buyers for stainless. OEMs routinely dual‑source across regions, amplifying price pressure on mills. Contracts often tie surcharges to alloy indices, capping Acerinox margins, while qualification stickiness limits but does not eliminate buyer leverage.

Service centers’ influence

Service centers aggregate customer demand and shape end-user pricing, using scale to pressure mills on standard grades and switch suppliers, increasing price competition. Their inventory cycles create timing leverage in negotiations, allowing them to buy when prices dip. Acerinox’s value-added processing secures share with service centers but cannot fully transfer value into higher mill pricing or prevent margin squeeze.

Specification and quality lock-in

Engineered applications demand certified grades and tight tolerances, and industry qualification cycles commonly run 6–18 months, raising switching costs for buyers. High-nickel and specialty grades command pricing resilience, with premiums typically in the 10–30% range versus commodity flats. Qualification costs and lead times thus create stickiness in critical uses, while commodity flats remain exposed to buyer price shopping.

Global price transparency

Global price transparency—via benchmarks like LME/SHFE nickel (LME nickel averaged ~25,000 USD/t in 2024) and chrome spreads—gives buyers clearer cost reference and reduces information asymmetry. Import parity and regional arbitrage cap local price premiums, while buyers time purchases by visible cost curves and inventory data. Digital RFQs and e-auctions further compress mill margins and shorten negotiation cycles.

- Benchmarks: LME/SHFE nickel ~25,000 USD/t (2024)

- Import parity limits local premiums

- Timed buys from inventory/cost curves

- Digital RFQs compress mill margins

Demand cyclicality

OEM concentration strengthens buyer price leverage; specialty grades hold 10-30% premiums

Large OEM/service-center concentration gives buyers strong price leverage; 2023 global auto output ~63m units and LME nickel ~25,000 USD/t (2024) anchor surcharges and cap Acerinox margins. Qualification stickiness supports specialty grades with 10–30% premiums, but commodity flats face intense sourcing and digital RFQs that compress spreads.

| Metric | Value |

|---|---|

| Auto output 2023 | ~63m units |

| LME nickel 2024 | ~25,000 USD/t |

| Specialty premium | 10–30% |

What You See Is What You Get

Acerinox Porter's Five Forces Analysis

This preview shows the exact Acerinox Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or sample pages. The file is professionally formatted, comprehensive, and ready for download and use the moment you buy. No edits or setup required.

From Overview to Strategy Blueprint

Acerinox faces intense rivalry in stainless steel with cyclical demand and price pressure, while supplier influence is moderate and buyer power significant; substitutes and new entrants pose limited but real risks given capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acerinox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Nickel and ferrochrome reliance

Acerinox relies on a concentrated set of suppliers for nickel, chromium and ferrochrome that are essential for stainless grades, with China supplying roughly 70% of global ferrochrome production. Nickel markets were highly volatile in 2024, with intrayear swings exceeding 20%, creating margin pressure. Long-term contracts and hedging programs partially mitigate price exposure, but limited vertical integration keeps supplier leverage elevated.

Energy cost intensity

Melting (~600 kWh/ton) and hot rolling are power-intensive processes, making Acerinox vulnerable to electricity and gas markets; European industrial electricity averaged ~€0.18/kWh in 2024 and EU ETS carbon prices were near €89/t, directly lifting conversion costs. Regional price volatility erodes pricing power and margins; long-term PPAs and efficiency upgrades cut exposure but cannot eliminate spikes. Suppliers of power and carbon allowances seize leverage during tight markets or rapid carbon-price jumps.

Scrap market volatility

In 2024 stainless and carbon steel scrap remained the primary cyclical inputs for Acerinox, with tight markets elevating input costs and causing mills to prioritize supply to larger buyers. Acerinox’s scale improves access to volumes but cannot fully control market-driven scrap pricing. Limited substitution with virgin inputs is constrained by strict grade specifications, keeping supplier leverage elevated.

Logistics and bulk freight

Bulk ores and alloys require reliable sea freight and port capacity; global seaborne iron ore trade was about 1.6 billion tonnes in 2024, making freight a key cost and timing factor for Acerinox. Freight-rate spikes and port bottlenecks lift delivered input costs and extend lead times, while diversified sourcing and multi-port strategies cut single-point risk. Suppliers frequently pass logistics surcharges through, preserving bargaining leverage.

- Freight share of delivered ore cost: ~10–15% (industry range)

- Seaborne iron ore ~1.6bn t in 2024

- Multi-port/sourcing reduces disruption risk

Environmental compliance costs

Upstream suppliers face tighter ESG and traceability demands in the EU and US, raising verification costs and lead times; EU ETS carbon prices averaged around €90/tCO2 in 2024, adding to input costs. Compliance premiums for certified or low-carbon alloys push stainless feedstock prices higher, while limited low-carbon nickel and chrome supply strengthens supplier pricing power. Acerinox must balance decarbonization targets with cost competitiveness.

- ESG/traceability: higher verification costs

- EU ETS ~€90/tCO2 (2024)

- Premiums for green alloys raise input costs

- Scarce low-carbon Ni/Cr increases supplier power

Concentrated alloy supply, rising energy and carbon costs, and logistics squeeze steelmakers

Suppliers hold elevated leverage: concentrated Ni/Cr/ferrochrome sourcing (China ~70% ferrochrome) and limited vertical integration constrain Acerinox bargaining power.

Energy and carbon cost exposure (EU industrial power ~€0.18/kWh; EU ETS ~€89–90/t in 2024) increases supplier influence via utilities and permits.

Logistics and scrap tightness (seaborne ore ~1.6bn t; freight share ~10–15%) and ESG premiums for low-carbon alloys further strengthen supplier power.

| Metric | 2024 |

|---|---|

| Ferrochrome supply (China) | ~70% |

| Nickel intrayear volatility | >20% |

| EU industrial power | ~€0.18/kWh |

| EU ETS price | €89–90/t |

| Seaborne iron ore | ~1.6bn t |

| Freight share | 10–15% |

What is included in the product

Concise Porter's Five Forces overview for Acerinox, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and market entry barriers that shape its pricing power and profitability.

Concise Acerinox Porter's Five Forces snapshot—instantly reveal competitive pressures with a customizable radar view and clean, copy-ready layout to simplify boardroom decisions and strategic planning.

Customers Bargaining Power

Large OEM concentration

Large OEM concentration in automotive, appliance and machinery drives aggressive negotiation; global vehicle output was about 63 million units in 2023, creating major volume buyers for stainless. OEMs routinely dual‑source across regions, amplifying price pressure on mills. Contracts often tie surcharges to alloy indices, capping Acerinox margins, while qualification stickiness limits but does not eliminate buyer leverage.

Service centers’ influence

Service centers aggregate customer demand and shape end-user pricing, using scale to pressure mills on standard grades and switch suppliers, increasing price competition. Their inventory cycles create timing leverage in negotiations, allowing them to buy when prices dip. Acerinox’s value-added processing secures share with service centers but cannot fully transfer value into higher mill pricing or prevent margin squeeze.

Specification and quality lock-in

Engineered applications demand certified grades and tight tolerances, and industry qualification cycles commonly run 6–18 months, raising switching costs for buyers. High-nickel and specialty grades command pricing resilience, with premiums typically in the 10–30% range versus commodity flats. Qualification costs and lead times thus create stickiness in critical uses, while commodity flats remain exposed to buyer price shopping.

Global price transparency

Global price transparency—via benchmarks like LME/SHFE nickel (LME nickel averaged ~25,000 USD/t in 2024) and chrome spreads—gives buyers clearer cost reference and reduces information asymmetry. Import parity and regional arbitrage cap local price premiums, while buyers time purchases by visible cost curves and inventory data. Digital RFQs and e-auctions further compress mill margins and shorten negotiation cycles.

- Benchmarks: LME/SHFE nickel ~25,000 USD/t (2024)

- Import parity limits local premiums

- Timed buys from inventory/cost curves

- Digital RFQs compress mill margins

Demand cyclicality

OEM concentration strengthens buyer price leverage; specialty grades hold 10-30% premiums

Large OEM/service-center concentration gives buyers strong price leverage; 2023 global auto output ~63m units and LME nickel ~25,000 USD/t (2024) anchor surcharges and cap Acerinox margins. Qualification stickiness supports specialty grades with 10–30% premiums, but commodity flats face intense sourcing and digital RFQs that compress spreads.

| Metric | Value |

|---|---|

| Auto output 2023 | ~63m units |

| LME nickel 2024 | ~25,000 USD/t |

| Specialty premium | 10–30% |

What You See Is What You Get

Acerinox Porter's Five Forces Analysis

This preview shows the exact Acerinox Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or sample pages. The file is professionally formatted, comprehensive, and ready for download and use the moment you buy. No edits or setup required.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Acerinox faces intense rivalry in stainless steel with cyclical demand and price pressure, while supplier influence is moderate and buyer power significant; substitutes and new entrants pose limited but real risks given capital intensity. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Acerinox’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Nickel and ferrochrome reliance

Acerinox relies on a concentrated set of suppliers for nickel, chromium and ferrochrome that are essential for stainless grades, with China supplying roughly 70% of global ferrochrome production. Nickel markets were highly volatile in 2024, with intrayear swings exceeding 20%, creating margin pressure. Long-term contracts and hedging programs partially mitigate price exposure, but limited vertical integration keeps supplier leverage elevated.

Energy cost intensity

Melting (~600 kWh/ton) and hot rolling are power-intensive processes, making Acerinox vulnerable to electricity and gas markets; European industrial electricity averaged ~€0.18/kWh in 2024 and EU ETS carbon prices were near €89/t, directly lifting conversion costs. Regional price volatility erodes pricing power and margins; long-term PPAs and efficiency upgrades cut exposure but cannot eliminate spikes. Suppliers of power and carbon allowances seize leverage during tight markets or rapid carbon-price jumps.

Scrap market volatility

In 2024 stainless and carbon steel scrap remained the primary cyclical inputs for Acerinox, with tight markets elevating input costs and causing mills to prioritize supply to larger buyers. Acerinox’s scale improves access to volumes but cannot fully control market-driven scrap pricing. Limited substitution with virgin inputs is constrained by strict grade specifications, keeping supplier leverage elevated.

Logistics and bulk freight

Bulk ores and alloys require reliable sea freight and port capacity; global seaborne iron ore trade was about 1.6 billion tonnes in 2024, making freight a key cost and timing factor for Acerinox. Freight-rate spikes and port bottlenecks lift delivered input costs and extend lead times, while diversified sourcing and multi-port strategies cut single-point risk. Suppliers frequently pass logistics surcharges through, preserving bargaining leverage.

- Freight share of delivered ore cost: ~10–15% (industry range)

- Seaborne iron ore ~1.6bn t in 2024

- Multi-port/sourcing reduces disruption risk

Environmental compliance costs

Upstream suppliers face tighter ESG and traceability demands in the EU and US, raising verification costs and lead times; EU ETS carbon prices averaged around €90/tCO2 in 2024, adding to input costs. Compliance premiums for certified or low-carbon alloys push stainless feedstock prices higher, while limited low-carbon nickel and chrome supply strengthens supplier pricing power. Acerinox must balance decarbonization targets with cost competitiveness.

- ESG/traceability: higher verification costs

- EU ETS ~€90/tCO2 (2024)

- Premiums for green alloys raise input costs

- Scarce low-carbon Ni/Cr increases supplier power

Concentrated alloy supply, rising energy and carbon costs, and logistics squeeze steelmakers

Suppliers hold elevated leverage: concentrated Ni/Cr/ferrochrome sourcing (China ~70% ferrochrome) and limited vertical integration constrain Acerinox bargaining power.

Energy and carbon cost exposure (EU industrial power ~€0.18/kWh; EU ETS ~€89–90/t in 2024) increases supplier influence via utilities and permits.

Logistics and scrap tightness (seaborne ore ~1.6bn t; freight share ~10–15%) and ESG premiums for low-carbon alloys further strengthen supplier power.

| Metric | 2024 |

|---|---|

| Ferrochrome supply (China) | ~70% |

| Nickel intrayear volatility | >20% |

| EU industrial power | ~€0.18/kWh |

| EU ETS price | €89–90/t |

| Seaborne iron ore | ~1.6bn t |

| Freight share | 10–15% |

What is included in the product

Concise Porter's Five Forces overview for Acerinox, assessing competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and market entry barriers that shape its pricing power and profitability.

Concise Acerinox Porter's Five Forces snapshot—instantly reveal competitive pressures with a customizable radar view and clean, copy-ready layout to simplify boardroom decisions and strategic planning.

Customers Bargaining Power

Large OEM concentration

Large OEM concentration in automotive, appliance and machinery drives aggressive negotiation; global vehicle output was about 63 million units in 2023, creating major volume buyers for stainless. OEMs routinely dual‑source across regions, amplifying price pressure on mills. Contracts often tie surcharges to alloy indices, capping Acerinox margins, while qualification stickiness limits but does not eliminate buyer leverage.

Service centers’ influence

Service centers aggregate customer demand and shape end-user pricing, using scale to pressure mills on standard grades and switch suppliers, increasing price competition. Their inventory cycles create timing leverage in negotiations, allowing them to buy when prices dip. Acerinox’s value-added processing secures share with service centers but cannot fully transfer value into higher mill pricing or prevent margin squeeze.

Specification and quality lock-in

Engineered applications demand certified grades and tight tolerances, and industry qualification cycles commonly run 6–18 months, raising switching costs for buyers. High-nickel and specialty grades command pricing resilience, with premiums typically in the 10–30% range versus commodity flats. Qualification costs and lead times thus create stickiness in critical uses, while commodity flats remain exposed to buyer price shopping.

Global price transparency

Global price transparency—via benchmarks like LME/SHFE nickel (LME nickel averaged ~25,000 USD/t in 2024) and chrome spreads—gives buyers clearer cost reference and reduces information asymmetry. Import parity and regional arbitrage cap local price premiums, while buyers time purchases by visible cost curves and inventory data. Digital RFQs and e-auctions further compress mill margins and shorten negotiation cycles.

- Benchmarks: LME/SHFE nickel ~25,000 USD/t (2024)

- Import parity limits local premiums

- Timed buys from inventory/cost curves

- Digital RFQs compress mill margins

Demand cyclicality

OEM concentration strengthens buyer price leverage; specialty grades hold 10-30% premiums

Large OEM/service-center concentration gives buyers strong price leverage; 2023 global auto output ~63m units and LME nickel ~25,000 USD/t (2024) anchor surcharges and cap Acerinox margins. Qualification stickiness supports specialty grades with 10–30% premiums, but commodity flats face intense sourcing and digital RFQs that compress spreads.

| Metric | Value |

|---|---|

| Auto output 2023 | ~63m units |

| LME nickel 2024 | ~25,000 USD/t |

| Specialty premium | 10–30% |

What You See Is What You Get

Acerinox Porter's Five Forces Analysis

This preview shows the exact Acerinox Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or sample pages. The file is professionally formatted, comprehensive, and ready for download and use the moment you buy. No edits or setup required.