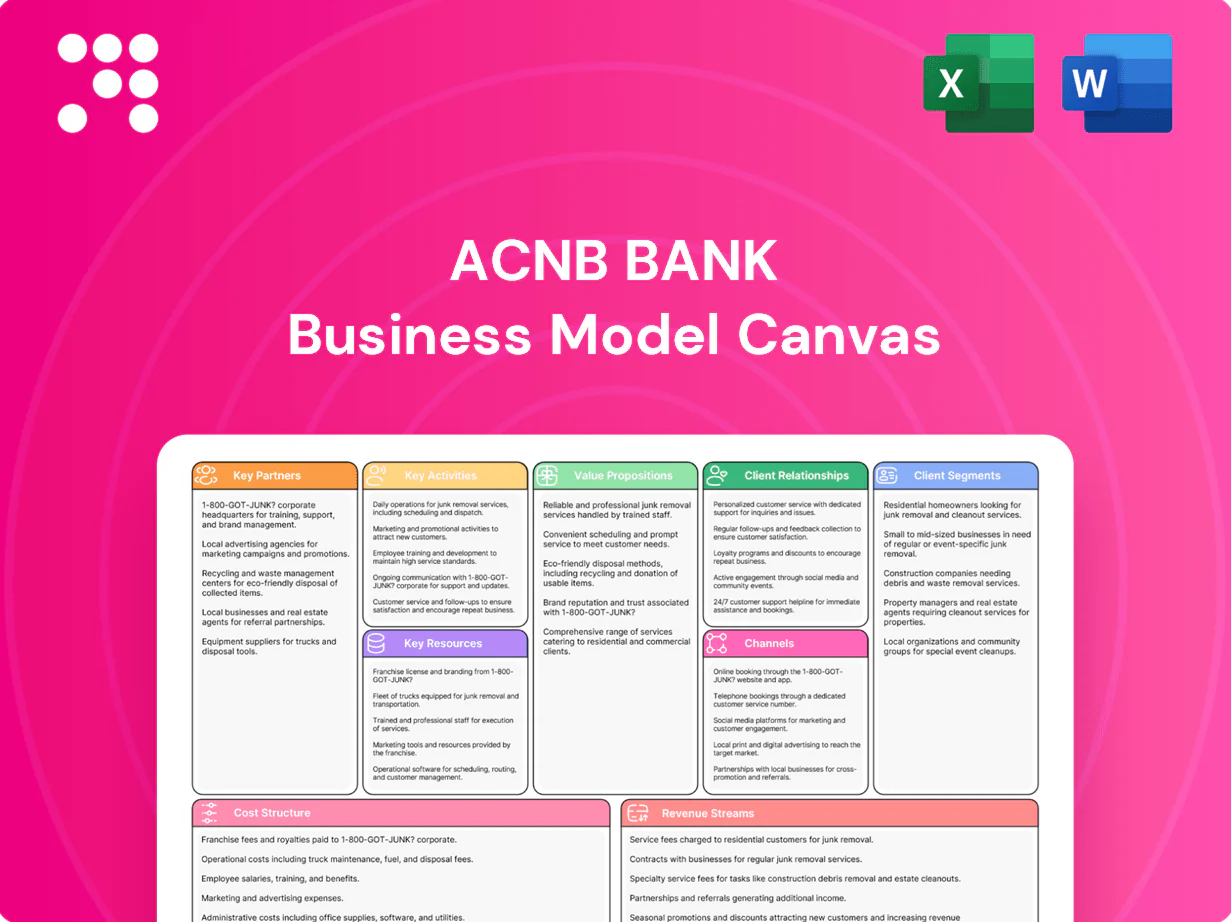

ACNB Bank Business Model Canvas

Unlock a regional bank's strategic blueprint with our Business Model Canvas

Unlock ACNB Bank’s strategic blueprint with our Business Model Canvas — a concise, actionable map of its value propositions, customer segments, revenue streams, and cost structure. Perfect for investors, consultants, and founders, this downloadable Canvas reveals where ACNB creates advantage and growth. Purchase the full Word/Excel file to access section-by-section analysis and practical insights you can apply today.

Partnerships

Core banking and fintech vendors

Core banking and fintech vendors supply core processing, digital banking, payments and cybersecurity solutions, enabling ACNB to offer feature-rich mobile and online services without building everything in-house. Vendor SLAs commonly guarantee 99.9%+ uptime and drive compliance updates (PCI DSS, FFIEC) and product roadmaps. Co-development and API integrations accelerate time-to-market and shorten integration cycles.

Payment networks and processors

Card networks, ACH rails and merchant processors enable deposits, transfers and card acceptance for ACNB, with interchange fees in 2024 typically ranging 1–3% and ACH handling tens of billions of U.S. transactions annually. These partners drive interchange revenue and secure settlement via daily net-settlement cycles. They let small businesses accept payments seamlessly through integrated treasury services and POS. Fraud tools and tokenization (widely adopted in 2024) enhance customer trust.

Secondary market and correspondent banks

ACNB leverages secondary market and correspondent banks to sell mortgages, originate loan participations and manage liquidity, freeing regulatory capital and reducing concentration and interest-rate risk; in 2024 the 30-year fixed averaged about 7.0% and the federal funds rate held at 5.25–5.50%, driving hedging demand. Correspondents provide specialized services ACNB lacks in-house, improving pricing and competitiveness for borrowers.

Wealth, trust, and custodial platforms

Community organizations and referral networks

Local chambers, realtors, CPAs, and attorneys drive relationship-based growth for ACNB, supporting loan, deposit, and wealth-service pipelines; ACNB reported about $3.6 billion in assets in 2023 and leverages local networks to boost originations and deposits. These referral channels generate warm leads and sponsorships/education events increase brand reach and reinforce the bank’s community mission and credibility.

- Local chambers: referral amplification

- Realtors/CPAs/attorneys: warm loan/deposit leads

- Sponsorships/events: brand lift

- Community ties: mission credibility

99.9%+ uptime; interchange 1-3%

Core banking, fintech and cybersecurity vendors deliver 99.9%+ uptime and API integrations for digital services; card networks/ACH drive interchange revenue (1–3% typical in 2024) and secure settlements. Correspondent banks and secondary markets manage liquidity and mortgage sales amid a 30-year fixed ~7.0% and fed funds 5.25–5.50% in 2024. Wealth/custody partners tap >$35T US retirement assets, expanding fee income; ACNB held ~$3.6B assets (2023).

| Partner | Role | 2024/2023 Metric |

|---|---|---|

| Core vendors | Core processing, APIs | 99.9%+ uptime |

| Card/ACH | Transactions, settlement | Interchange 1–3% |

| Correspondents | Liquidity, mortgage sales | 30y fixed ~7.0% |

| Wealth/custody | Advisory, custody | US retirement >$35T |

| Local partners | Referrals, community | ACNB assets ~$3.6B (2023) |

What is included in the product

Comprehensive Business Model Canvas for ACNB Bank detailing customer segments, channels, value propositions, revenue and cost structures across the 9 BMC blocks, reflecting real-world operations and strategic plans. Designed for presentations and funding discussions, it includes competitive advantage analysis and SWOT-linked insights to support investors, analysts, and decision-makers.

Condenses ACNB Bank’s strategy into a digestible, one-page Business Model Canvas to quickly identify core components and relieve planning pain points for boards, teams, and advisors.

Activities

Deposit gathering and relationship banking

Acquire and retain checking, savings and time deposits from consumers and businesses to support ACNBs ~$3.5B balance sheet and roughly $2.9B deposit base (2024); focus on onboarding seasonal cash flows and commercial accounts. Cross-sell lending, wealth and treasury services tied to life events and cash-flow needs to raise share of wallet and fee income. Maintain competitive pricing and service quality to reduce churn while monitoring deposit mix and cost of funds to protect net interest margin.

Prudent lending and credit risk management

Originate consumer, commercial, and CRE loans tied to local demand, prioritizing sectors core to ACNB’s central Pennsylvania footprint. Underwrite with disciplined policies and data-driven models including credit scoring, stress testing, and documented covenants. Monitor portfolios, covenants, and collateral continuously and adjust pricing and loan structures as interest rates and risk profiles evolve to minimize losses.

Regulatory compliance and enterprise risk

Meet BSA/AML, fair lending, privacy, and safety-and-soundness standards by filing Currency Transaction Reports for cash transactions over $10,000 and adhering to BSA obligations established in 1970; operate robust monitoring, testing, and training programs with quarterly AML reviews and annual fair-lending assessments. Maintain governance, internal audit, and vendor risk oversight in line with OCC third-party guidance, and keep policies updated as regulations evolve.

Digital operations and customer experience

ACNB Bank enhances mobile, online, and payments journeys for convenience and security, supporting customers across devices and reducing branch dependency; ACNB reported total assets of about $4.0 billion in 2024. Analytics refine onboarding, alerts, and self-service to lift digital activation and reduce drop-offs, while omnichannel support resolves issues quickly. Continuous UX improvements proceed alongside layered fraud controls to limit losses.

- digital activation: analytics-driven

- omnichannel support: fast resolution

- fraud controls: layered, continuous

Wealth management and trust administration

We provide planning, advisory, and fiduciary services for individuals and businesses, managing portfolios and retirement plans tailored to clients' risk profiles and goals while coordinating estate, tax, and charitable strategies with legal and tax partners.

These services generate recurring fee-based revenue, deepen client relationships, and support cross-sell of banking products to enhance lifetime value for ACNB Bank.

- services: planning, advisory, fiduciary

- focus: portfolio & retirement alignment

- coordination: estate, tax, charitable partners

- outcome: recurring fee revenue & deeper relationships

Drive deposit growth to $2.9B and fund a $4.0B balance sheet

Acquire/retain ~$2.9B deposits to fund a ~$4.0B balance sheet (2024), cross-sell lending, wealth and treasury services to raise fee income and wallet share.

Originate/underwrite consumer, commercial and CRE loans for central PA with disciplined credit models, covenants and continuous portfolio monitoring.

Maintain BSA/AML, fair-lending and safety-and-soundness controls (CTR filings >$10k, quarterly AML reviews, annual fair-lending tests).

Enhance digital/mobile UX and layered fraud controls to boost activation, reduce branch load and limit losses.

| Metric | 2024 |

|---|---|

| Total assets | $4.0B |

| Deposits | $2.9B |

Preview Before You Purchase

Business Model Canvas

The ACNB Bank Business Model Canvas you see here is the actual deliverable, not a mockup. It’s the same document you’ll receive after purchase, complete and editable. Upon ordering you’ll get the full file formatted exactly as previewed, ready for use in Word and Excel. No surprises—what you see is what you’ll own.

Unlock a regional bank's strategic blueprint with our Business Model Canvas

Unlock ACNB Bank’s strategic blueprint with our Business Model Canvas — a concise, actionable map of its value propositions, customer segments, revenue streams, and cost structure. Perfect for investors, consultants, and founders, this downloadable Canvas reveals where ACNB creates advantage and growth. Purchase the full Word/Excel file to access section-by-section analysis and practical insights you can apply today.

Partnerships

Core banking and fintech vendors

Core banking and fintech vendors supply core processing, digital banking, payments and cybersecurity solutions, enabling ACNB to offer feature-rich mobile and online services without building everything in-house. Vendor SLAs commonly guarantee 99.9%+ uptime and drive compliance updates (PCI DSS, FFIEC) and product roadmaps. Co-development and API integrations accelerate time-to-market and shorten integration cycles.

Payment networks and processors

Card networks, ACH rails and merchant processors enable deposits, transfers and card acceptance for ACNB, with interchange fees in 2024 typically ranging 1–3% and ACH handling tens of billions of U.S. transactions annually. These partners drive interchange revenue and secure settlement via daily net-settlement cycles. They let small businesses accept payments seamlessly through integrated treasury services and POS. Fraud tools and tokenization (widely adopted in 2024) enhance customer trust.

Secondary market and correspondent banks

ACNB leverages secondary market and correspondent banks to sell mortgages, originate loan participations and manage liquidity, freeing regulatory capital and reducing concentration and interest-rate risk; in 2024 the 30-year fixed averaged about 7.0% and the federal funds rate held at 5.25–5.50%, driving hedging demand. Correspondents provide specialized services ACNB lacks in-house, improving pricing and competitiveness for borrowers.

Wealth, trust, and custodial platforms

Community organizations and referral networks

Local chambers, realtors, CPAs, and attorneys drive relationship-based growth for ACNB, supporting loan, deposit, and wealth-service pipelines; ACNB reported about $3.6 billion in assets in 2023 and leverages local networks to boost originations and deposits. These referral channels generate warm leads and sponsorships/education events increase brand reach and reinforce the bank’s community mission and credibility.

- Local chambers: referral amplification

- Realtors/CPAs/attorneys: warm loan/deposit leads

- Sponsorships/events: brand lift

- Community ties: mission credibility

99.9%+ uptime; interchange 1-3%

Core banking, fintech and cybersecurity vendors deliver 99.9%+ uptime and API integrations for digital services; card networks/ACH drive interchange revenue (1–3% typical in 2024) and secure settlements. Correspondent banks and secondary markets manage liquidity and mortgage sales amid a 30-year fixed ~7.0% and fed funds 5.25–5.50% in 2024. Wealth/custody partners tap >$35T US retirement assets, expanding fee income; ACNB held ~$3.6B assets (2023).

| Partner | Role | 2024/2023 Metric |

|---|---|---|

| Core vendors | Core processing, APIs | 99.9%+ uptime |

| Card/ACH | Transactions, settlement | Interchange 1–3% |

| Correspondents | Liquidity, mortgage sales | 30y fixed ~7.0% |

| Wealth/custody | Advisory, custody | US retirement >$35T |

| Local partners | Referrals, community | ACNB assets ~$3.6B (2023) |

What is included in the product

Comprehensive Business Model Canvas for ACNB Bank detailing customer segments, channels, value propositions, revenue and cost structures across the 9 BMC blocks, reflecting real-world operations and strategic plans. Designed for presentations and funding discussions, it includes competitive advantage analysis and SWOT-linked insights to support investors, analysts, and decision-makers.

Condenses ACNB Bank’s strategy into a digestible, one-page Business Model Canvas to quickly identify core components and relieve planning pain points for boards, teams, and advisors.

Activities

Deposit gathering and relationship banking

Acquire and retain checking, savings and time deposits from consumers and businesses to support ACNBs ~$3.5B balance sheet and roughly $2.9B deposit base (2024); focus on onboarding seasonal cash flows and commercial accounts. Cross-sell lending, wealth and treasury services tied to life events and cash-flow needs to raise share of wallet and fee income. Maintain competitive pricing and service quality to reduce churn while monitoring deposit mix and cost of funds to protect net interest margin.

Prudent lending and credit risk management

Originate consumer, commercial, and CRE loans tied to local demand, prioritizing sectors core to ACNB’s central Pennsylvania footprint. Underwrite with disciplined policies and data-driven models including credit scoring, stress testing, and documented covenants. Monitor portfolios, covenants, and collateral continuously and adjust pricing and loan structures as interest rates and risk profiles evolve to minimize losses.

Regulatory compliance and enterprise risk

Meet BSA/AML, fair lending, privacy, and safety-and-soundness standards by filing Currency Transaction Reports for cash transactions over $10,000 and adhering to BSA obligations established in 1970; operate robust monitoring, testing, and training programs with quarterly AML reviews and annual fair-lending assessments. Maintain governance, internal audit, and vendor risk oversight in line with OCC third-party guidance, and keep policies updated as regulations evolve.

Digital operations and customer experience

ACNB Bank enhances mobile, online, and payments journeys for convenience and security, supporting customers across devices and reducing branch dependency; ACNB reported total assets of about $4.0 billion in 2024. Analytics refine onboarding, alerts, and self-service to lift digital activation and reduce drop-offs, while omnichannel support resolves issues quickly. Continuous UX improvements proceed alongside layered fraud controls to limit losses.

- digital activation: analytics-driven

- omnichannel support: fast resolution

- fraud controls: layered, continuous

Wealth management and trust administration

We provide planning, advisory, and fiduciary services for individuals and businesses, managing portfolios and retirement plans tailored to clients' risk profiles and goals while coordinating estate, tax, and charitable strategies with legal and tax partners.

These services generate recurring fee-based revenue, deepen client relationships, and support cross-sell of banking products to enhance lifetime value for ACNB Bank.

- services: planning, advisory, fiduciary

- focus: portfolio & retirement alignment

- coordination: estate, tax, charitable partners

- outcome: recurring fee revenue & deeper relationships

Drive deposit growth to $2.9B and fund a $4.0B balance sheet

Acquire/retain ~$2.9B deposits to fund a ~$4.0B balance sheet (2024), cross-sell lending, wealth and treasury services to raise fee income and wallet share.

Originate/underwrite consumer, commercial and CRE loans for central PA with disciplined credit models, covenants and continuous portfolio monitoring.

Maintain BSA/AML, fair-lending and safety-and-soundness controls (CTR filings >$10k, quarterly AML reviews, annual fair-lending tests).

Enhance digital/mobile UX and layered fraud controls to boost activation, reduce branch load and limit losses.

| Metric | 2024 |

|---|---|

| Total assets | $4.0B |

| Deposits | $2.9B |

Preview Before You Purchase

Business Model Canvas

The ACNB Bank Business Model Canvas you see here is the actual deliverable, not a mockup. It’s the same document you’ll receive after purchase, complete and editable. Upon ordering you’ll get the full file formatted exactly as previewed, ready for use in Word and Excel. No surprises—what you see is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a regional bank's strategic blueprint with our Business Model Canvas

Unlock ACNB Bank’s strategic blueprint with our Business Model Canvas — a concise, actionable map of its value propositions, customer segments, revenue streams, and cost structure. Perfect for investors, consultants, and founders, this downloadable Canvas reveals where ACNB creates advantage and growth. Purchase the full Word/Excel file to access section-by-section analysis and practical insights you can apply today.

Partnerships

Core banking and fintech vendors

Core banking and fintech vendors supply core processing, digital banking, payments and cybersecurity solutions, enabling ACNB to offer feature-rich mobile and online services without building everything in-house. Vendor SLAs commonly guarantee 99.9%+ uptime and drive compliance updates (PCI DSS, FFIEC) and product roadmaps. Co-development and API integrations accelerate time-to-market and shorten integration cycles.

Payment networks and processors

Card networks, ACH rails and merchant processors enable deposits, transfers and card acceptance for ACNB, with interchange fees in 2024 typically ranging 1–3% and ACH handling tens of billions of U.S. transactions annually. These partners drive interchange revenue and secure settlement via daily net-settlement cycles. They let small businesses accept payments seamlessly through integrated treasury services and POS. Fraud tools and tokenization (widely adopted in 2024) enhance customer trust.

Secondary market and correspondent banks

ACNB leverages secondary market and correspondent banks to sell mortgages, originate loan participations and manage liquidity, freeing regulatory capital and reducing concentration and interest-rate risk; in 2024 the 30-year fixed averaged about 7.0% and the federal funds rate held at 5.25–5.50%, driving hedging demand. Correspondents provide specialized services ACNB lacks in-house, improving pricing and competitiveness for borrowers.

Wealth, trust, and custodial platforms

Community organizations and referral networks

Local chambers, realtors, CPAs, and attorneys drive relationship-based growth for ACNB, supporting loan, deposit, and wealth-service pipelines; ACNB reported about $3.6 billion in assets in 2023 and leverages local networks to boost originations and deposits. These referral channels generate warm leads and sponsorships/education events increase brand reach and reinforce the bank’s community mission and credibility.

- Local chambers: referral amplification

- Realtors/CPAs/attorneys: warm loan/deposit leads

- Sponsorships/events: brand lift

- Community ties: mission credibility

99.9%+ uptime; interchange 1-3%

Core banking, fintech and cybersecurity vendors deliver 99.9%+ uptime and API integrations for digital services; card networks/ACH drive interchange revenue (1–3% typical in 2024) and secure settlements. Correspondent banks and secondary markets manage liquidity and mortgage sales amid a 30-year fixed ~7.0% and fed funds 5.25–5.50% in 2024. Wealth/custody partners tap >$35T US retirement assets, expanding fee income; ACNB held ~$3.6B assets (2023).

| Partner | Role | 2024/2023 Metric |

|---|---|---|

| Core vendors | Core processing, APIs | 99.9%+ uptime |

| Card/ACH | Transactions, settlement | Interchange 1–3% |

| Correspondents | Liquidity, mortgage sales | 30y fixed ~7.0% |

| Wealth/custody | Advisory, custody | US retirement >$35T |

| Local partners | Referrals, community | ACNB assets ~$3.6B (2023) |

What is included in the product

Comprehensive Business Model Canvas for ACNB Bank detailing customer segments, channels, value propositions, revenue and cost structures across the 9 BMC blocks, reflecting real-world operations and strategic plans. Designed for presentations and funding discussions, it includes competitive advantage analysis and SWOT-linked insights to support investors, analysts, and decision-makers.

Condenses ACNB Bank’s strategy into a digestible, one-page Business Model Canvas to quickly identify core components and relieve planning pain points for boards, teams, and advisors.

Activities

Deposit gathering and relationship banking

Acquire and retain checking, savings and time deposits from consumers and businesses to support ACNBs ~$3.5B balance sheet and roughly $2.9B deposit base (2024); focus on onboarding seasonal cash flows and commercial accounts. Cross-sell lending, wealth and treasury services tied to life events and cash-flow needs to raise share of wallet and fee income. Maintain competitive pricing and service quality to reduce churn while monitoring deposit mix and cost of funds to protect net interest margin.

Prudent lending and credit risk management

Originate consumer, commercial, and CRE loans tied to local demand, prioritizing sectors core to ACNB’s central Pennsylvania footprint. Underwrite with disciplined policies and data-driven models including credit scoring, stress testing, and documented covenants. Monitor portfolios, covenants, and collateral continuously and adjust pricing and loan structures as interest rates and risk profiles evolve to minimize losses.

Regulatory compliance and enterprise risk

Meet BSA/AML, fair lending, privacy, and safety-and-soundness standards by filing Currency Transaction Reports for cash transactions over $10,000 and adhering to BSA obligations established in 1970; operate robust monitoring, testing, and training programs with quarterly AML reviews and annual fair-lending assessments. Maintain governance, internal audit, and vendor risk oversight in line with OCC third-party guidance, and keep policies updated as regulations evolve.

Digital operations and customer experience

ACNB Bank enhances mobile, online, and payments journeys for convenience and security, supporting customers across devices and reducing branch dependency; ACNB reported total assets of about $4.0 billion in 2024. Analytics refine onboarding, alerts, and self-service to lift digital activation and reduce drop-offs, while omnichannel support resolves issues quickly. Continuous UX improvements proceed alongside layered fraud controls to limit losses.

- digital activation: analytics-driven

- omnichannel support: fast resolution

- fraud controls: layered, continuous

Wealth management and trust administration

We provide planning, advisory, and fiduciary services for individuals and businesses, managing portfolios and retirement plans tailored to clients' risk profiles and goals while coordinating estate, tax, and charitable strategies with legal and tax partners.

These services generate recurring fee-based revenue, deepen client relationships, and support cross-sell of banking products to enhance lifetime value for ACNB Bank.

- services: planning, advisory, fiduciary

- focus: portfolio & retirement alignment

- coordination: estate, tax, charitable partners

- outcome: recurring fee revenue & deeper relationships

Drive deposit growth to $2.9B and fund a $4.0B balance sheet

Acquire/retain ~$2.9B deposits to fund a ~$4.0B balance sheet (2024), cross-sell lending, wealth and treasury services to raise fee income and wallet share.

Originate/underwrite consumer, commercial and CRE loans for central PA with disciplined credit models, covenants and continuous portfolio monitoring.

Maintain BSA/AML, fair-lending and safety-and-soundness controls (CTR filings >$10k, quarterly AML reviews, annual fair-lending tests).

Enhance digital/mobile UX and layered fraud controls to boost activation, reduce branch load and limit losses.

| Metric | 2024 |

|---|---|

| Total assets | $4.0B |

| Deposits | $2.9B |

Preview Before You Purchase

Business Model Canvas

The ACNB Bank Business Model Canvas you see here is the actual deliverable, not a mockup. It’s the same document you’ll receive after purchase, complete and editable. Upon ordering you’ll get the full file formatted exactly as previewed, ready for use in Word and Excel. No surprises—what you see is what you’ll own.