ACP Holding GmbH Porter's Five Forces Analysis

From Overview to Strategy Blueprint

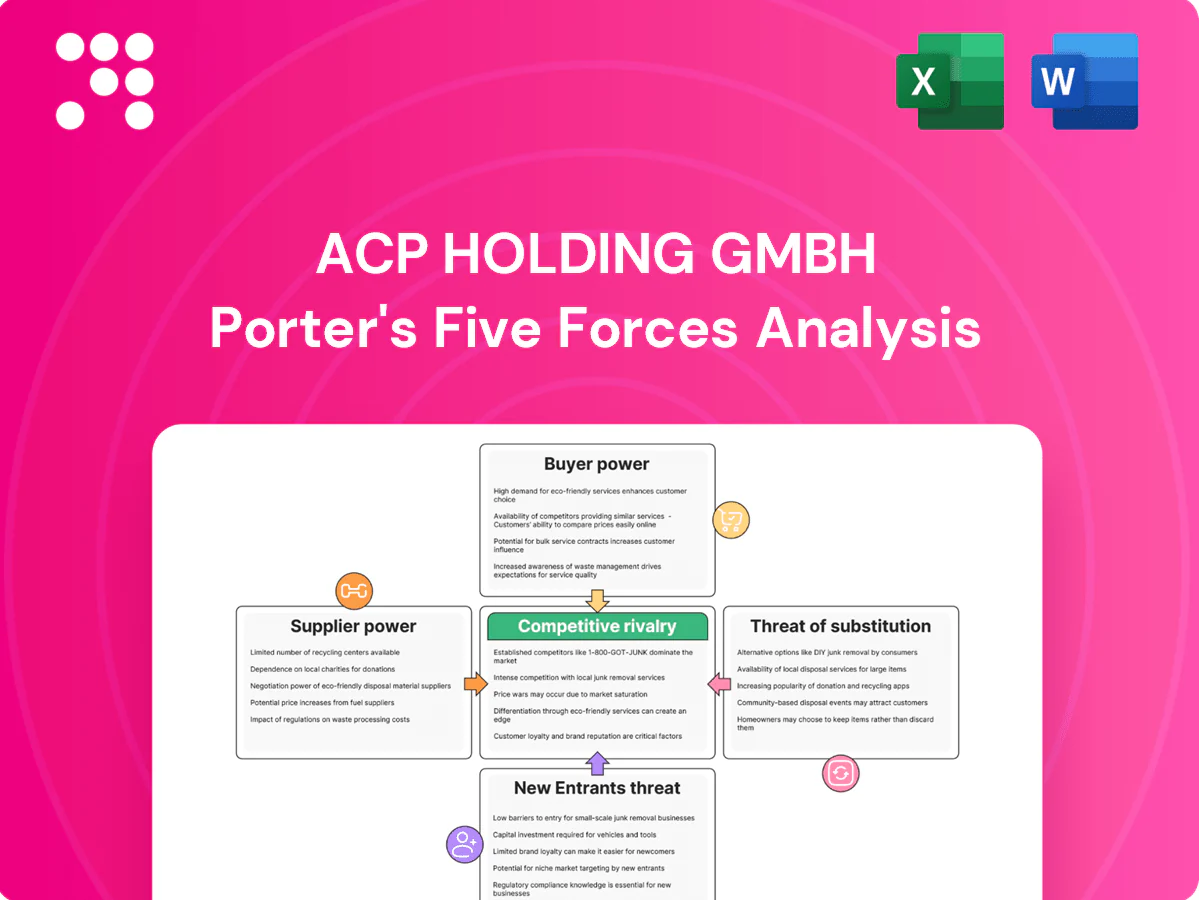

This concise Porter's Five Forces snapshot highlights ACP Holding GmbH’s competitive pressures—supplier leverage, buyer power, substitute threats, entry barriers, and industry rivalry—framing immediate strategic risks. The full report reveals force-by-force ratings, market data, and actionable implications to refine positioning and investment decisions. Unlock the complete analysis with visuals and ready-to-use Word/Excel deliverables to drive smarter strategy.

Suppliers Bargaining Power

Concentrated OEM ecosystems

ACP depends on concentrated OEM ecosystems—Gartner 2024 shows the top five server, networking and storage vendors capture roughly 80% of market revenue—making portfolio substitution costly and redesign-intensive. Vendor concentration increases upstream leverage on pricing, rebates and contract terms, while preferred partner status mitigates some risk but tier thresholds (often linked to quarterly revenue targets) steer sales toward qualifying SKUs. Any supply disruption or EOL policy shift by a dominant OEM can compress project margins and delay deliveries, amplifying financial volatility across contracts.

Hyperscaler dependency

Cloud partnerships are strategic yet asymmetrical: hyperscalers (AWS ~32%, Azure ~23%, Google Cloud ~11% in 2024) set partner incentives and retain ability to compete via direct services. Changes in discount structures and marketplace rules (AWS Marketplace fees up to 20%) pressure ACP’s packaged offerings and margins. Joint go‑to‑market lifts volume but increases margin compression and dependency risk.

Cybersecurity vendor lock-ins

Point-solution stacks create integration path-dependency, with enterprises running a median of ~50 security tools (2024 surveys), while certifications, MSSP rights and license tiers lock ACP into vendor roadmaps and update cycles. Subscription price inflation (~10% in 2024) can be passed through but undermines TCO claims, and switching tools incurs retraining and service-redesign costs that often exceed six-figure program budgets.

Scarce skilled labor as a “supplier”

Senior architects and security experts are central to ACP Holding’s delivery capacity and quality; 2024 Bitkom data shows over 130,000 unfilled IT roles in Germany, pushing senior contractor rates up ~10–15% year-on-year and squeezing gross margins. Certification upkeep (ISO/IEC, CISSP) adds recurring costs and scheduling risk, while attrition risks knowledge loss and SLA exposure.

- High dependence on senior hires

- Wage/subcontractor inflation ~10–15% (2024)

- Certification and attrition = recurring cost/SLA risk

Logistics and component lead times

Hardware supply chains in 2024 still saw lead times from roughly 12–26 weeks, creating risks to project timing, revenue recognition and cash cycles for ACP Holding GmbH; ACP must buffer with 3–6 months of stocking and multi-vendor sourcing, as long-dated quotes can produce cost variance on delivery.

- Lead times: 12–26 weeks

- Stock buffer: 3–6 months

- Mitigation: multi-vendor sourcing

Supplier power: top-5 ~80%, 32%/23%/11%, 12–26w

ACP faces strong supplier bargaining: top five OEMs capture ~80% of server/storage revenue (Gartner 2024), hyperscalers AWS 32% Azure 23% Google 11% (2024) shape partner economics and margin pressure. Lead times 12–26 weeks and wage inflation 10–15% increase costs, inventory needs and revenue timing risk.

| Metric | 2024 |

|---|---|

| Top-5 OEM share | ~80% |

| AWS/Azure/Google | 32%/23%/11% |

| Lead times | 12–26 weeks |

| Wage inflation | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for ACP Holding GmbH that uncovers key drivers of competition, customer and supplier power, entry barriers and substitute threats, identifying disruptive forces and strategic vulnerabilities affecting pricing and market share. Fully editable for inclusion in investor materials, strategy decks, or academic projects.

A clear, one-sheet summary of all five forces—enabling ACP Holding GmbH to quickly spot competitive pressures and make faster, data-driven strategic decisions.

Customers Bargaining Power

Professional procurement and tenders

Mid-market and enterprise clients increasingly run standardized RFPs that boost price comparability, forcing ACP Holding to defend margins; in 2024 median RFP win rates hovered near 20% and framework agreements routinely lock in discounts and SLAs that erode gross margins by an estimated 5–10%. Winning hinges on demonstrable total-value propositions and verifiable outcome metrics.

Moderate switching costs

Managed services and integrations embed ACP processes and tooling, yet buyers can phase transitions by tower or region to reduce risk; the global managed services market was about $308B in 2024, enabling scale-driven competition. Clear documentation and standardized ITIL practices lower vendor-change friction, and widespread multi-sourcing—used by roughly 60% of enterprises in 2024—keeps ongoing price pressure on ACP.

Demand for outcome SLAs

Customers increasingly demand outcome SLAs—uptime, security, and response metrics with financial penalties—shifting operational risk to ACP and compressing margins; industry surveys in 2024 report roughly 60% of large enterprises favor outcome-based pricing. To protect EBITDA, ACP must invest in robust tooling and automation, as underperforming contracts can erode profitability within quarters.

Price transparency in cloud

Price transparency in cloud means public list prices and online calculators anchor buyer expectations; ACP must quantify value through optimization, FinOps, and governance to show measurable savings — global public cloud spend was roughly $623 billion in 2023 (Gartner), increasing buyer price sensitivity; without visible savings customers seek direct or alternate partners, while reserved instances and multi-year commitments complicate renegotiations.

- Anchor: list prices set expectations

- Value: optimization + FinOps required

- Switch: customers seek alternatives if no savings

- Lock-in: reservations hinder renegotiation

Cross-sell leverage by large clients

Multi-domain deals at ACP Holding amplify scale but increase client bargaining power; in 2024 procurement surveys showed 68% of enterprises use consolidated sourcing to secure bundled discounts. Consolidated spend lets top clients push for price & SLA concessions; renewal cycles are decisive negotiation moments. Strong referenceability and long-term outcomes can limit price erosion.

- Client share concentration: high

- Bundled discount pressure: 68% (2024)

- Renewals: key leverage point

- Referenceability offsets price risk

RFPs trim ACP margins 5-10%; FinOps, automation and references protect EBITDA

Enterprise buyers' standardized RFPs and framework discounts (median RFP win ~20% in 2024) compress ACP margins ~5–10%; outcome SLAs and financial penalties shift risk to ACP. Multi-sourcing (~60% of enterprises in 2024) and consolidated sourcing (68% use bundled discounts) increase price pressure; robust FinOps, automation and referenceability are pivotal to defend EBITDA.

| Metric | 2023/24 |

|---|---|

| RFP win rate | ~20% (2024) |

| Margin erosion | 5–10% |

| Managed services market | $308B (2024) |

| Cloud spend | $623B (2023) |

| Multi-sourcing | ~60% (2024) |

| Consolidated sourcing | 68% (2024) |

What You See Is What You Get

ACP Holding GmbH Porter's Five Forces Analysis

This preview displays the exact ACP Holding GmbH Porter's Five Forces analysis you will receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download after purchase. Use it as-is for strategy, valuation, or presentation needs.

From Overview to Strategy Blueprint

This concise Porter's Five Forces snapshot highlights ACP Holding GmbH’s competitive pressures—supplier leverage, buyer power, substitute threats, entry barriers, and industry rivalry—framing immediate strategic risks. The full report reveals force-by-force ratings, market data, and actionable implications to refine positioning and investment decisions. Unlock the complete analysis with visuals and ready-to-use Word/Excel deliverables to drive smarter strategy.

Suppliers Bargaining Power

Concentrated OEM ecosystems

ACP depends on concentrated OEM ecosystems—Gartner 2024 shows the top five server, networking and storage vendors capture roughly 80% of market revenue—making portfolio substitution costly and redesign-intensive. Vendor concentration increases upstream leverage on pricing, rebates and contract terms, while preferred partner status mitigates some risk but tier thresholds (often linked to quarterly revenue targets) steer sales toward qualifying SKUs. Any supply disruption or EOL policy shift by a dominant OEM can compress project margins and delay deliveries, amplifying financial volatility across contracts.

Hyperscaler dependency

Cloud partnerships are strategic yet asymmetrical: hyperscalers (AWS ~32%, Azure ~23%, Google Cloud ~11% in 2024) set partner incentives and retain ability to compete via direct services. Changes in discount structures and marketplace rules (AWS Marketplace fees up to 20%) pressure ACP’s packaged offerings and margins. Joint go‑to‑market lifts volume but increases margin compression and dependency risk.

Cybersecurity vendor lock-ins

Point-solution stacks create integration path-dependency, with enterprises running a median of ~50 security tools (2024 surveys), while certifications, MSSP rights and license tiers lock ACP into vendor roadmaps and update cycles. Subscription price inflation (~10% in 2024) can be passed through but undermines TCO claims, and switching tools incurs retraining and service-redesign costs that often exceed six-figure program budgets.

Scarce skilled labor as a “supplier”

Senior architects and security experts are central to ACP Holding’s delivery capacity and quality; 2024 Bitkom data shows over 130,000 unfilled IT roles in Germany, pushing senior contractor rates up ~10–15% year-on-year and squeezing gross margins. Certification upkeep (ISO/IEC, CISSP) adds recurring costs and scheduling risk, while attrition risks knowledge loss and SLA exposure.

- High dependence on senior hires

- Wage/subcontractor inflation ~10–15% (2024)

- Certification and attrition = recurring cost/SLA risk

Logistics and component lead times

Hardware supply chains in 2024 still saw lead times from roughly 12–26 weeks, creating risks to project timing, revenue recognition and cash cycles for ACP Holding GmbH; ACP must buffer with 3–6 months of stocking and multi-vendor sourcing, as long-dated quotes can produce cost variance on delivery.

- Lead times: 12–26 weeks

- Stock buffer: 3–6 months

- Mitigation: multi-vendor sourcing

Supplier power: top-5 ~80%, 32%/23%/11%, 12–26w

ACP faces strong supplier bargaining: top five OEMs capture ~80% of server/storage revenue (Gartner 2024), hyperscalers AWS 32% Azure 23% Google 11% (2024) shape partner economics and margin pressure. Lead times 12–26 weeks and wage inflation 10–15% increase costs, inventory needs and revenue timing risk.

| Metric | 2024 |

|---|---|

| Top-5 OEM share | ~80% |

| AWS/Azure/Google | 32%/23%/11% |

| Lead times | 12–26 weeks |

| Wage inflation | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for ACP Holding GmbH that uncovers key drivers of competition, customer and supplier power, entry barriers and substitute threats, identifying disruptive forces and strategic vulnerabilities affecting pricing and market share. Fully editable for inclusion in investor materials, strategy decks, or academic projects.

A clear, one-sheet summary of all five forces—enabling ACP Holding GmbH to quickly spot competitive pressures and make faster, data-driven strategic decisions.

Customers Bargaining Power

Professional procurement and tenders

Mid-market and enterprise clients increasingly run standardized RFPs that boost price comparability, forcing ACP Holding to defend margins; in 2024 median RFP win rates hovered near 20% and framework agreements routinely lock in discounts and SLAs that erode gross margins by an estimated 5–10%. Winning hinges on demonstrable total-value propositions and verifiable outcome metrics.

Moderate switching costs

Managed services and integrations embed ACP processes and tooling, yet buyers can phase transitions by tower or region to reduce risk; the global managed services market was about $308B in 2024, enabling scale-driven competition. Clear documentation and standardized ITIL practices lower vendor-change friction, and widespread multi-sourcing—used by roughly 60% of enterprises in 2024—keeps ongoing price pressure on ACP.

Demand for outcome SLAs

Customers increasingly demand outcome SLAs—uptime, security, and response metrics with financial penalties—shifting operational risk to ACP and compressing margins; industry surveys in 2024 report roughly 60% of large enterprises favor outcome-based pricing. To protect EBITDA, ACP must invest in robust tooling and automation, as underperforming contracts can erode profitability within quarters.

Price transparency in cloud

Price transparency in cloud means public list prices and online calculators anchor buyer expectations; ACP must quantify value through optimization, FinOps, and governance to show measurable savings — global public cloud spend was roughly $623 billion in 2023 (Gartner), increasing buyer price sensitivity; without visible savings customers seek direct or alternate partners, while reserved instances and multi-year commitments complicate renegotiations.

- Anchor: list prices set expectations

- Value: optimization + FinOps required

- Switch: customers seek alternatives if no savings

- Lock-in: reservations hinder renegotiation

Cross-sell leverage by large clients

Multi-domain deals at ACP Holding amplify scale but increase client bargaining power; in 2024 procurement surveys showed 68% of enterprises use consolidated sourcing to secure bundled discounts. Consolidated spend lets top clients push for price & SLA concessions; renewal cycles are decisive negotiation moments. Strong referenceability and long-term outcomes can limit price erosion.

- Client share concentration: high

- Bundled discount pressure: 68% (2024)

- Renewals: key leverage point

- Referenceability offsets price risk

RFPs trim ACP margins 5-10%; FinOps, automation and references protect EBITDA

Enterprise buyers' standardized RFPs and framework discounts (median RFP win ~20% in 2024) compress ACP margins ~5–10%; outcome SLAs and financial penalties shift risk to ACP. Multi-sourcing (~60% of enterprises in 2024) and consolidated sourcing (68% use bundled discounts) increase price pressure; robust FinOps, automation and referenceability are pivotal to defend EBITDA.

| Metric | 2023/24 |

|---|---|

| RFP win rate | ~20% (2024) |

| Margin erosion | 5–10% |

| Managed services market | $308B (2024) |

| Cloud spend | $623B (2023) |

| Multi-sourcing | ~60% (2024) |

| Consolidated sourcing | 68% (2024) |

What You See Is What You Get

ACP Holding GmbH Porter's Five Forces Analysis

This preview displays the exact ACP Holding GmbH Porter's Five Forces analysis you will receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download after purchase. Use it as-is for strategy, valuation, or presentation needs.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

This concise Porter's Five Forces snapshot highlights ACP Holding GmbH’s competitive pressures—supplier leverage, buyer power, substitute threats, entry barriers, and industry rivalry—framing immediate strategic risks. The full report reveals force-by-force ratings, market data, and actionable implications to refine positioning and investment decisions. Unlock the complete analysis with visuals and ready-to-use Word/Excel deliverables to drive smarter strategy.

Suppliers Bargaining Power

Concentrated OEM ecosystems

ACP depends on concentrated OEM ecosystems—Gartner 2024 shows the top five server, networking and storage vendors capture roughly 80% of market revenue—making portfolio substitution costly and redesign-intensive. Vendor concentration increases upstream leverage on pricing, rebates and contract terms, while preferred partner status mitigates some risk but tier thresholds (often linked to quarterly revenue targets) steer sales toward qualifying SKUs. Any supply disruption or EOL policy shift by a dominant OEM can compress project margins and delay deliveries, amplifying financial volatility across contracts.

Hyperscaler dependency

Cloud partnerships are strategic yet asymmetrical: hyperscalers (AWS ~32%, Azure ~23%, Google Cloud ~11% in 2024) set partner incentives and retain ability to compete via direct services. Changes in discount structures and marketplace rules (AWS Marketplace fees up to 20%) pressure ACP’s packaged offerings and margins. Joint go‑to‑market lifts volume but increases margin compression and dependency risk.

Cybersecurity vendor lock-ins

Point-solution stacks create integration path-dependency, with enterprises running a median of ~50 security tools (2024 surveys), while certifications, MSSP rights and license tiers lock ACP into vendor roadmaps and update cycles. Subscription price inflation (~10% in 2024) can be passed through but undermines TCO claims, and switching tools incurs retraining and service-redesign costs that often exceed six-figure program budgets.

Scarce skilled labor as a “supplier”

Senior architects and security experts are central to ACP Holding’s delivery capacity and quality; 2024 Bitkom data shows over 130,000 unfilled IT roles in Germany, pushing senior contractor rates up ~10–15% year-on-year and squeezing gross margins. Certification upkeep (ISO/IEC, CISSP) adds recurring costs and scheduling risk, while attrition risks knowledge loss and SLA exposure.

- High dependence on senior hires

- Wage/subcontractor inflation ~10–15% (2024)

- Certification and attrition = recurring cost/SLA risk

Logistics and component lead times

Hardware supply chains in 2024 still saw lead times from roughly 12–26 weeks, creating risks to project timing, revenue recognition and cash cycles for ACP Holding GmbH; ACP must buffer with 3–6 months of stocking and multi-vendor sourcing, as long-dated quotes can produce cost variance on delivery.

- Lead times: 12–26 weeks

- Stock buffer: 3–6 months

- Mitigation: multi-vendor sourcing

Supplier power: top-5 ~80%, 32%/23%/11%, 12–26w

ACP faces strong supplier bargaining: top five OEMs capture ~80% of server/storage revenue (Gartner 2024), hyperscalers AWS 32% Azure 23% Google 11% (2024) shape partner economics and margin pressure. Lead times 12–26 weeks and wage inflation 10–15% increase costs, inventory needs and revenue timing risk.

| Metric | 2024 |

|---|---|

| Top-5 OEM share | ~80% |

| AWS/Azure/Google | 32%/23%/11% |

| Lead times | 12–26 weeks |

| Wage inflation | 10–15% |

What is included in the product

Tailored Porter's Five Forces analysis for ACP Holding GmbH that uncovers key drivers of competition, customer and supplier power, entry barriers and substitute threats, identifying disruptive forces and strategic vulnerabilities affecting pricing and market share. Fully editable for inclusion in investor materials, strategy decks, or academic projects.

A clear, one-sheet summary of all five forces—enabling ACP Holding GmbH to quickly spot competitive pressures and make faster, data-driven strategic decisions.

Customers Bargaining Power

Professional procurement and tenders

Mid-market and enterprise clients increasingly run standardized RFPs that boost price comparability, forcing ACP Holding to defend margins; in 2024 median RFP win rates hovered near 20% and framework agreements routinely lock in discounts and SLAs that erode gross margins by an estimated 5–10%. Winning hinges on demonstrable total-value propositions and verifiable outcome metrics.

Moderate switching costs

Managed services and integrations embed ACP processes and tooling, yet buyers can phase transitions by tower or region to reduce risk; the global managed services market was about $308B in 2024, enabling scale-driven competition. Clear documentation and standardized ITIL practices lower vendor-change friction, and widespread multi-sourcing—used by roughly 60% of enterprises in 2024—keeps ongoing price pressure on ACP.

Demand for outcome SLAs

Customers increasingly demand outcome SLAs—uptime, security, and response metrics with financial penalties—shifting operational risk to ACP and compressing margins; industry surveys in 2024 report roughly 60% of large enterprises favor outcome-based pricing. To protect EBITDA, ACP must invest in robust tooling and automation, as underperforming contracts can erode profitability within quarters.

Price transparency in cloud

Price transparency in cloud means public list prices and online calculators anchor buyer expectations; ACP must quantify value through optimization, FinOps, and governance to show measurable savings — global public cloud spend was roughly $623 billion in 2023 (Gartner), increasing buyer price sensitivity; without visible savings customers seek direct or alternate partners, while reserved instances and multi-year commitments complicate renegotiations.

- Anchor: list prices set expectations

- Value: optimization + FinOps required

- Switch: customers seek alternatives if no savings

- Lock-in: reservations hinder renegotiation

Cross-sell leverage by large clients

Multi-domain deals at ACP Holding amplify scale but increase client bargaining power; in 2024 procurement surveys showed 68% of enterprises use consolidated sourcing to secure bundled discounts. Consolidated spend lets top clients push for price & SLA concessions; renewal cycles are decisive negotiation moments. Strong referenceability and long-term outcomes can limit price erosion.

- Client share concentration: high

- Bundled discount pressure: 68% (2024)

- Renewals: key leverage point

- Referenceability offsets price risk

RFPs trim ACP margins 5-10%; FinOps, automation and references protect EBITDA

Enterprise buyers' standardized RFPs and framework discounts (median RFP win ~20% in 2024) compress ACP margins ~5–10%; outcome SLAs and financial penalties shift risk to ACP. Multi-sourcing (~60% of enterprises in 2024) and consolidated sourcing (68% use bundled discounts) increase price pressure; robust FinOps, automation and referenceability are pivotal to defend EBITDA.

| Metric | 2023/24 |

|---|---|

| RFP win rate | ~20% (2024) |

| Margin erosion | 5–10% |

| Managed services market | $308B (2024) |

| Cloud spend | $623B (2023) |

| Multi-sourcing | ~60% (2024) |

| Consolidated sourcing | 68% (2024) |

What You See Is What You Get

ACP Holding GmbH Porter's Five Forces Analysis

This preview displays the exact ACP Holding GmbH Porter's Five Forces analysis you will receive—no placeholders or samples. The full, professionally formatted document is ready for immediate download after purchase. Use it as-is for strategy, valuation, or presentation needs.