ACP Holding GmbH PESTLE Analysis

Skip the Research. Get the Strategy.

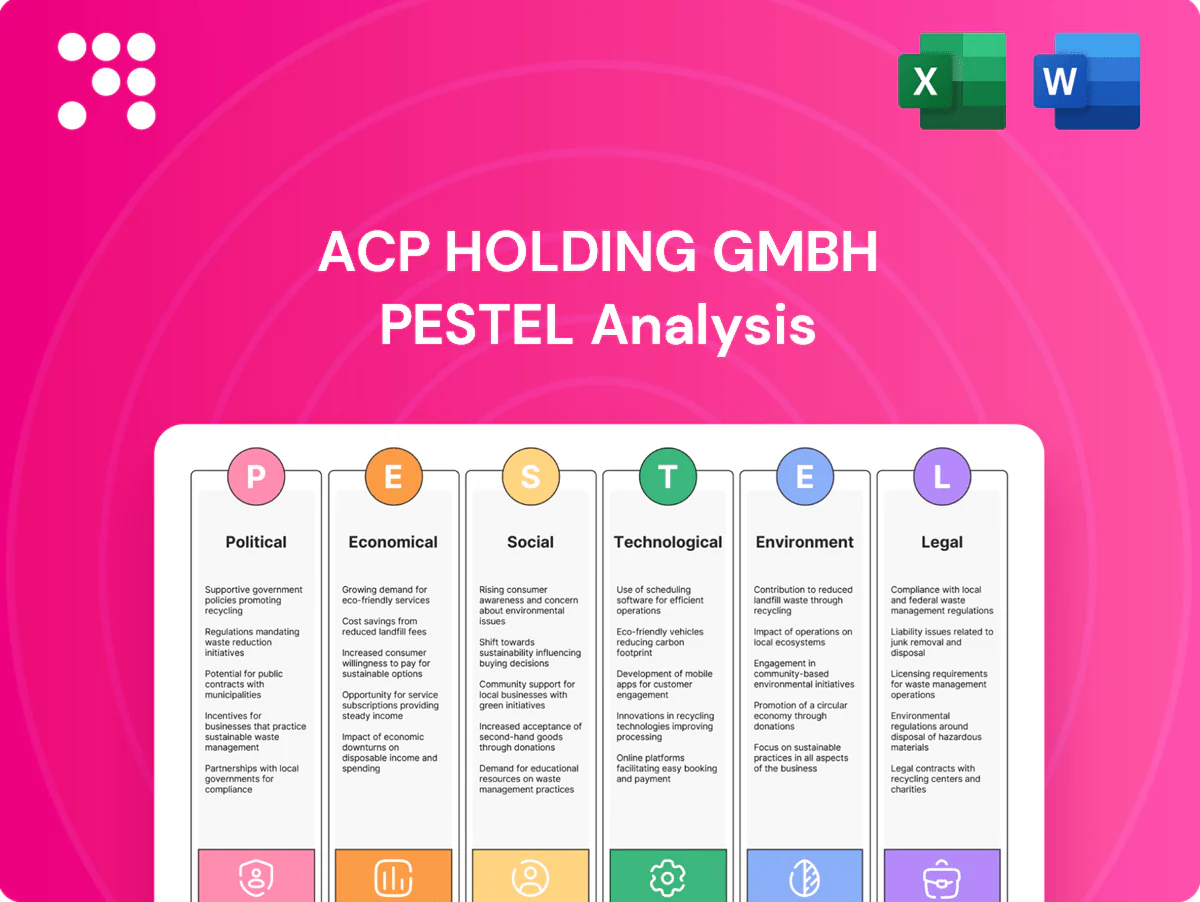

Discover how political, economic, social, technological, legal and environmental forces are reshaping ACP Holding GmbH's strategic outlook. This concise PESTLE snapshot highlights risks and growth levers you can act on today. Want the full, editable analysis with deep-dive insights and recommendations? Purchase the complete report for instant download.

Political factors

EU digital policy & funding

EU recovery and digitalization programs — notably NextGenerationEU (~€750bn) and the Digital Europe Programme (€7.5bn for 2021–27) — prioritize cloud, cybersecurity and connectivity, creating procurement pipelines ACP can target. Participation in national/EU grants reduces client capex and shortens deal cycles. Monitoring timelines and eligibility aligns ACP offerings to funded themes. Close ties with innovation agencies boost visibility on upcoming calls.

Public sector IT procurement

Government modernization agendas are driving multi-year tenders for data center, networking and workplace services; public procurement accounts for about 14% of EU GDP (Eurostat), representing a sizeable addressable market ACP can target. Procurement rules prioritize compliance, security certifications and local support—areas ACP can leverage. Political shifts can reprioritize budgets or delay awards, affecting backlog timing, so building framework agreements hedges election-cycle volatility.

Geopolitics & vendor access

Geopolitical tensions and 2023–24 US export controls on advanced semiconductors and tooling—when combined with TSMC’s ~54% foundry share—heighten risk of delivery delays for hardware and telecom equipment. Policymaker scrutiny of foreign cloud and hardware vendors is shifting enterprise architecture toward sovereign and hybrid models. ACP’s multi-vendor integration reduces single-supplier exposure, and scenario planning for sanctions and trade restrictions preserves project continuity.

Digital sovereignty priorities

European digital sovereignty drives platform selection as policymakers push for data residency and sovereign cloud standards; hyperscalers still hold ~70% of EU IaaS/PaaS market (2024) but national initiatives increase demand for local hosting. ACP can leverage regional data-center partnerships to offer compliant architectures, capturing workloads that governments and regulated firms shift away from extra-EU footprints.

Taxation & incentives

Investment incentives such as Germany’s Forschungzulage (25% R&D wage credit up to €4m) and EU/state energy-efficiency grants lower solution TCO and accelerate refresh cycles, while OECD data show an average statutory corporate tax of 23.8% (2023) and national social charges that materially affect ACP’s cross-border cost base; optimizing entity structures is needed for VAT and withholding rules, and stable fiscal regimes underpin long-term managed services contracts.

- R&D credit: Germany Forschungzulage 25% (up to €4m)

- OECD corp tax avg 23.8% (2023)

- Energy grants cut TCO, drive faster refresh

- VAT/withholding optimization vital for cross-border delivery

EU recovery funds and Digital Europe boost sovereign-cloud demand; hyperscalers ~70%

EU recovery funds (NextGenerationEU ~€750bn) and Digital Europe (€7.5bn) drive cloud/cyber procurement; public procurement ~14% of EU GDP (Eurostat) expands addressable market. Hyperscalers hold ~70% EU IaaS/PaaS (2024), boosting sovereign-cloud demand. Germany Forschungzulage 25% (up to €4m) lowers TCO; OECD average corp tax 23.8% (2023) shapes structures.

| Metric | Value |

|---|---|

| NextGenerationEU | ~€750bn |

| Digital Europe | €7.5bn (2021–27) |

| Public procurement | ~14% EU GDP |

| Hyperscaler share | ~70% (2024) |

| Forschungzulage | 25% R&D credit (up to €4m) |

| OECD corp tax | 23.8% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect ACP Holding GmbH, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors. Each section offers forward-looking insights to support scenario planning and strategic decisions.

A concise ACP Holding GmbH PESTLE summary that neatly segments political, economic, social, technological, legal and environmental factors for quick reference, editable for local context and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

IT spending cycles

Macro growth and elevated rates (US fed funds ~5.25% in 2024) push CFOs toward opex, shifting capex-to-opex choices as global IT spend nears $4.7T (2024); managed services and pay-as-you-go (managed services CAGR ~7–8%) sustain demand in slowdowns. Cybersecurity and automation budgets, ~10–12% of IT spend and growing ~10% YoY, stay resilient, while SMB-to-enterprise pipeline diversification lowers revenue cyclicality.

Labor market & wage inflation

High demand for cloud, security and network engineers is pushing IT salaries—Hays Germany reported ~6% salary growth for IT specialists in 2024—raising ACP margin pressure. Rigorous utilization management and standardized delivery frameworks reduce margin erosion by improving billable efficiency. Nearshoring and in-house talent academies expand capacity at more stable cost bases. Multi-year pricing should include inflation indexing given 2024 euro-area inflation ~2.4% (Eurostat).

Energy prices & data center costs

Volatile European wholesale power has materially affected hosting and private cloud unit economics, with data centers accounting for roughly 1% of global electricity use. Energy-efficient designs and renewable corporate PPAs can stabilize long-term costs. Transparent pass-through clauses help preserve margins for power-intensive services. Clients increasingly evaluate TCO with energy as a primary variable.

SMB digitalization momentum

- SMB cloud spend ↑: ~70% planning increases (IDC 2024)

- Productivity gains ~20% from modern workplace (Microsoft 2024)

- Managed security adoption rising YoY

- Regional footprint = stronger localized sales & support

M&A and consolidation

Industry consolidation opens tuck-in acquisition opportunities for niche capabilities, while larger scale secures better vendor terms and shared delivery centers; disciplined integration is essential to protect service quality and culture, and heightened private equity activity increases competitive bidding for assets and clients.

EU recovery funds and Digital Europe boost sovereign-cloud demand; hyperscalers ~70%

Macro growth and elevated rates (US fed funds ~5.25% in 2024) push buyers to opex models as global IT spend nears $4.7T (2024); managed services CAGR ~7–8% cushions demand. Cybersecurity ≈10–12% of IT budgets, growing ~10% YoY; IT salaries rose ~6% in Germany (Hays 2024), pressuring margins. Energy volatility (data centers ~1% global electricity) raises TCO focus; Euro area inflation ~2.4% (2024) supports inflation-indexed pricing.

| Metric | 2024/2025 Value |

|---|---|

| Global IT spend | $4.7T (2024) |

| Fed funds | ~5.25% (2024) |

| Managed services CAGR | 7–8% |

| Cybersecurity share | 10–12% IT spend, ~10% YoY growth |

| IT salary growth (DE) | ~6% (Hays 2024) |

| Euro inflation | ~2.4% (2024) |

| Data center electricity | ~1% global use |

What You See Is What You Get

ACP Holding GmbH PESTLE Analysis

The preview shown here is the exact ACP Holding GmbH PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This real snapshot reflects the final content, layout and structure with no placeholders. After payment you’ll instantly download this identical, professionally structured file.

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal and environmental forces are reshaping ACP Holding GmbH's strategic outlook. This concise PESTLE snapshot highlights risks and growth levers you can act on today. Want the full, editable analysis with deep-dive insights and recommendations? Purchase the complete report for instant download.

Political factors

EU digital policy & funding

EU recovery and digitalization programs — notably NextGenerationEU (~€750bn) and the Digital Europe Programme (€7.5bn for 2021–27) — prioritize cloud, cybersecurity and connectivity, creating procurement pipelines ACP can target. Participation in national/EU grants reduces client capex and shortens deal cycles. Monitoring timelines and eligibility aligns ACP offerings to funded themes. Close ties with innovation agencies boost visibility on upcoming calls.

Public sector IT procurement

Government modernization agendas are driving multi-year tenders for data center, networking and workplace services; public procurement accounts for about 14% of EU GDP (Eurostat), representing a sizeable addressable market ACP can target. Procurement rules prioritize compliance, security certifications and local support—areas ACP can leverage. Political shifts can reprioritize budgets or delay awards, affecting backlog timing, so building framework agreements hedges election-cycle volatility.

Geopolitics & vendor access

Geopolitical tensions and 2023–24 US export controls on advanced semiconductors and tooling—when combined with TSMC’s ~54% foundry share—heighten risk of delivery delays for hardware and telecom equipment. Policymaker scrutiny of foreign cloud and hardware vendors is shifting enterprise architecture toward sovereign and hybrid models. ACP’s multi-vendor integration reduces single-supplier exposure, and scenario planning for sanctions and trade restrictions preserves project continuity.

Digital sovereignty priorities

European digital sovereignty drives platform selection as policymakers push for data residency and sovereign cloud standards; hyperscalers still hold ~70% of EU IaaS/PaaS market (2024) but national initiatives increase demand for local hosting. ACP can leverage regional data-center partnerships to offer compliant architectures, capturing workloads that governments and regulated firms shift away from extra-EU footprints.

Taxation & incentives

Investment incentives such as Germany’s Forschungzulage (25% R&D wage credit up to €4m) and EU/state energy-efficiency grants lower solution TCO and accelerate refresh cycles, while OECD data show an average statutory corporate tax of 23.8% (2023) and national social charges that materially affect ACP’s cross-border cost base; optimizing entity structures is needed for VAT and withholding rules, and stable fiscal regimes underpin long-term managed services contracts.

- R&D credit: Germany Forschungzulage 25% (up to €4m)

- OECD corp tax avg 23.8% (2023)

- Energy grants cut TCO, drive faster refresh

- VAT/withholding optimization vital for cross-border delivery

EU recovery funds and Digital Europe boost sovereign-cloud demand; hyperscalers ~70%

EU recovery funds (NextGenerationEU ~€750bn) and Digital Europe (€7.5bn) drive cloud/cyber procurement; public procurement ~14% of EU GDP (Eurostat) expands addressable market. Hyperscalers hold ~70% EU IaaS/PaaS (2024), boosting sovereign-cloud demand. Germany Forschungzulage 25% (up to €4m) lowers TCO; OECD average corp tax 23.8% (2023) shapes structures.

| Metric | Value |

|---|---|

| NextGenerationEU | ~€750bn |

| Digital Europe | €7.5bn (2021–27) |

| Public procurement | ~14% EU GDP |

| Hyperscaler share | ~70% (2024) |

| Forschungzulage | 25% R&D credit (up to €4m) |

| OECD corp tax | 23.8% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect ACP Holding GmbH, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors. Each section offers forward-looking insights to support scenario planning and strategic decisions.

A concise ACP Holding GmbH PESTLE summary that neatly segments political, economic, social, technological, legal and environmental factors for quick reference, editable for local context and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

IT spending cycles

Macro growth and elevated rates (US fed funds ~5.25% in 2024) push CFOs toward opex, shifting capex-to-opex choices as global IT spend nears $4.7T (2024); managed services and pay-as-you-go (managed services CAGR ~7–8%) sustain demand in slowdowns. Cybersecurity and automation budgets, ~10–12% of IT spend and growing ~10% YoY, stay resilient, while SMB-to-enterprise pipeline diversification lowers revenue cyclicality.

Labor market & wage inflation

High demand for cloud, security and network engineers is pushing IT salaries—Hays Germany reported ~6% salary growth for IT specialists in 2024—raising ACP margin pressure. Rigorous utilization management and standardized delivery frameworks reduce margin erosion by improving billable efficiency. Nearshoring and in-house talent academies expand capacity at more stable cost bases. Multi-year pricing should include inflation indexing given 2024 euro-area inflation ~2.4% (Eurostat).

Energy prices & data center costs

Volatile European wholesale power has materially affected hosting and private cloud unit economics, with data centers accounting for roughly 1% of global electricity use. Energy-efficient designs and renewable corporate PPAs can stabilize long-term costs. Transparent pass-through clauses help preserve margins for power-intensive services. Clients increasingly evaluate TCO with energy as a primary variable.

SMB digitalization momentum

- SMB cloud spend ↑: ~70% planning increases (IDC 2024)

- Productivity gains ~20% from modern workplace (Microsoft 2024)

- Managed security adoption rising YoY

- Regional footprint = stronger localized sales & support

M&A and consolidation

Industry consolidation opens tuck-in acquisition opportunities for niche capabilities, while larger scale secures better vendor terms and shared delivery centers; disciplined integration is essential to protect service quality and culture, and heightened private equity activity increases competitive bidding for assets and clients.

EU recovery funds and Digital Europe boost sovereign-cloud demand; hyperscalers ~70%

Macro growth and elevated rates (US fed funds ~5.25% in 2024) push buyers to opex models as global IT spend nears $4.7T (2024); managed services CAGR ~7–8% cushions demand. Cybersecurity ≈10–12% of IT budgets, growing ~10% YoY; IT salaries rose ~6% in Germany (Hays 2024), pressuring margins. Energy volatility (data centers ~1% global electricity) raises TCO focus; Euro area inflation ~2.4% (2024) supports inflation-indexed pricing.

| Metric | 2024/2025 Value |

|---|---|

| Global IT spend | $4.7T (2024) |

| Fed funds | ~5.25% (2024) |

| Managed services CAGR | 7–8% |

| Cybersecurity share | 10–12% IT spend, ~10% YoY growth |

| IT salary growth (DE) | ~6% (Hays 2024) |

| Euro inflation | ~2.4% (2024) |

| Data center electricity | ~1% global use |

What You See Is What You Get

ACP Holding GmbH PESTLE Analysis

The preview shown here is the exact ACP Holding GmbH PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This real snapshot reflects the final content, layout and structure with no placeholders. After payment you’ll instantly download this identical, professionally structured file.

Description

Skip the Research. Get the Strategy.

Discover how political, economic, social, technological, legal and environmental forces are reshaping ACP Holding GmbH's strategic outlook. This concise PESTLE snapshot highlights risks and growth levers you can act on today. Want the full, editable analysis with deep-dive insights and recommendations? Purchase the complete report for instant download.

Political factors

EU digital policy & funding

EU recovery and digitalization programs — notably NextGenerationEU (~€750bn) and the Digital Europe Programme (€7.5bn for 2021–27) — prioritize cloud, cybersecurity and connectivity, creating procurement pipelines ACP can target. Participation in national/EU grants reduces client capex and shortens deal cycles. Monitoring timelines and eligibility aligns ACP offerings to funded themes. Close ties with innovation agencies boost visibility on upcoming calls.

Public sector IT procurement

Government modernization agendas are driving multi-year tenders for data center, networking and workplace services; public procurement accounts for about 14% of EU GDP (Eurostat), representing a sizeable addressable market ACP can target. Procurement rules prioritize compliance, security certifications and local support—areas ACP can leverage. Political shifts can reprioritize budgets or delay awards, affecting backlog timing, so building framework agreements hedges election-cycle volatility.

Geopolitics & vendor access

Geopolitical tensions and 2023–24 US export controls on advanced semiconductors and tooling—when combined with TSMC’s ~54% foundry share—heighten risk of delivery delays for hardware and telecom equipment. Policymaker scrutiny of foreign cloud and hardware vendors is shifting enterprise architecture toward sovereign and hybrid models. ACP’s multi-vendor integration reduces single-supplier exposure, and scenario planning for sanctions and trade restrictions preserves project continuity.

Digital sovereignty priorities

European digital sovereignty drives platform selection as policymakers push for data residency and sovereign cloud standards; hyperscalers still hold ~70% of EU IaaS/PaaS market (2024) but national initiatives increase demand for local hosting. ACP can leverage regional data-center partnerships to offer compliant architectures, capturing workloads that governments and regulated firms shift away from extra-EU footprints.

Taxation & incentives

Investment incentives such as Germany’s Forschungzulage (25% R&D wage credit up to €4m) and EU/state energy-efficiency grants lower solution TCO and accelerate refresh cycles, while OECD data show an average statutory corporate tax of 23.8% (2023) and national social charges that materially affect ACP’s cross-border cost base; optimizing entity structures is needed for VAT and withholding rules, and stable fiscal regimes underpin long-term managed services contracts.

- R&D credit: Germany Forschungzulage 25% (up to €4m)

- OECD corp tax avg 23.8% (2023)

- Energy grants cut TCO, drive faster refresh

- VAT/withholding optimization vital for cross-border delivery

EU recovery funds and Digital Europe boost sovereign-cloud demand; hyperscalers ~70%

EU recovery funds (NextGenerationEU ~€750bn) and Digital Europe (€7.5bn) drive cloud/cyber procurement; public procurement ~14% of EU GDP (Eurostat) expands addressable market. Hyperscalers hold ~70% EU IaaS/PaaS (2024), boosting sovereign-cloud demand. Germany Forschungzulage 25% (up to €4m) lowers TCO; OECD average corp tax 23.8% (2023) shapes structures.

| Metric | Value |

|---|---|

| NextGenerationEU | ~€750bn |

| Digital Europe | €7.5bn (2021–27) |

| Public procurement | ~14% EU GDP |

| Hyperscaler share | ~70% (2024) |

| Forschungzulage | 25% R&D credit (up to €4m) |

| OECD corp tax | 23.8% (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect ACP Holding GmbH, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors. Each section offers forward-looking insights to support scenario planning and strategic decisions.

A concise ACP Holding GmbH PESTLE summary that neatly segments political, economic, social, technological, legal and environmental factors for quick reference, editable for local context and easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

IT spending cycles

Macro growth and elevated rates (US fed funds ~5.25% in 2024) push CFOs toward opex, shifting capex-to-opex choices as global IT spend nears $4.7T (2024); managed services and pay-as-you-go (managed services CAGR ~7–8%) sustain demand in slowdowns. Cybersecurity and automation budgets, ~10–12% of IT spend and growing ~10% YoY, stay resilient, while SMB-to-enterprise pipeline diversification lowers revenue cyclicality.

Labor market & wage inflation

High demand for cloud, security and network engineers is pushing IT salaries—Hays Germany reported ~6% salary growth for IT specialists in 2024—raising ACP margin pressure. Rigorous utilization management and standardized delivery frameworks reduce margin erosion by improving billable efficiency. Nearshoring and in-house talent academies expand capacity at more stable cost bases. Multi-year pricing should include inflation indexing given 2024 euro-area inflation ~2.4% (Eurostat).

Energy prices & data center costs

Volatile European wholesale power has materially affected hosting and private cloud unit economics, with data centers accounting for roughly 1% of global electricity use. Energy-efficient designs and renewable corporate PPAs can stabilize long-term costs. Transparent pass-through clauses help preserve margins for power-intensive services. Clients increasingly evaluate TCO with energy as a primary variable.

SMB digitalization momentum

- SMB cloud spend ↑: ~70% planning increases (IDC 2024)

- Productivity gains ~20% from modern workplace (Microsoft 2024)

- Managed security adoption rising YoY

- Regional footprint = stronger localized sales & support

M&A and consolidation

Industry consolidation opens tuck-in acquisition opportunities for niche capabilities, while larger scale secures better vendor terms and shared delivery centers; disciplined integration is essential to protect service quality and culture, and heightened private equity activity increases competitive bidding for assets and clients.

EU recovery funds and Digital Europe boost sovereign-cloud demand; hyperscalers ~70%

Macro growth and elevated rates (US fed funds ~5.25% in 2024) push buyers to opex models as global IT spend nears $4.7T (2024); managed services CAGR ~7–8% cushions demand. Cybersecurity ≈10–12% of IT budgets, growing ~10% YoY; IT salaries rose ~6% in Germany (Hays 2024), pressuring margins. Energy volatility (data centers ~1% global electricity) raises TCO focus; Euro area inflation ~2.4% (2024) supports inflation-indexed pricing.

| Metric | 2024/2025 Value |

|---|---|

| Global IT spend | $4.7T (2024) |

| Fed funds | ~5.25% (2024) |

| Managed services CAGR | 7–8% |

| Cybersecurity share | 10–12% IT spend, ~10% YoY growth |

| IT salary growth (DE) | ~6% (Hays 2024) |

| Euro inflation | ~2.4% (2024) |

| Data center electricity | ~1% global use |

What You See Is What You Get

ACP Holding GmbH PESTLE Analysis

The preview shown here is the exact ACP Holding GmbH PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This real snapshot reflects the final content, layout and structure with no placeholders. After payment you’ll instantly download this identical, professionally structured file.