ACTIA Group Boston Consulting Group Matrix

Download Your Competitive Advantage

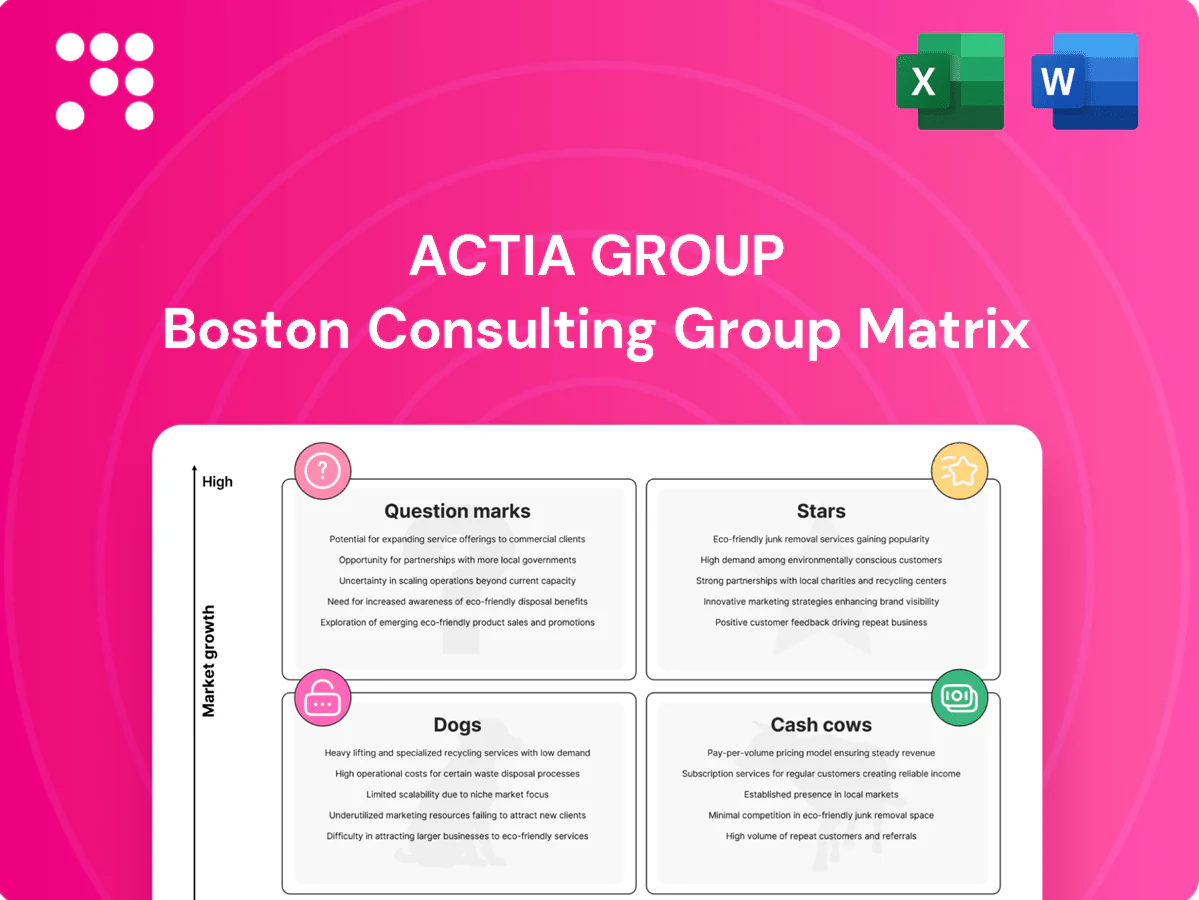

The ACTIA Group BCG Matrix snapshot shows which product lines are driving growth and which are quietly draining resources, giving you a quick read on Stars, Cash Cows, Dogs and Question Marks. This preview scratches the surface—buy the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for where to invest or divest. Get the full report in Word plus a high-level Excel summary so you can present and act fast. Purchase now for a ready-to-use strategic tool that saves you hours of analysis.

Stars

Vehicle diagnostics platforms

Vehicle diagnostics platforms are a core ACTIA strength with deep OEM and aftermarket reach; leadership and integrations raise switching costs while serving a growing market driven by connected and electric fleets (global EV stock exceeded 26.6 million by 2022). The unit soaks up cash for software, protocols and global support but scales profitably with each new program; continued investment is needed to cement standard status and convert late adopters.

Fleet telematics & connectivity modules

Commercial fleets are digitizing rapidly as uptime, regulatory compliance, and TCO reduction drive telematics adoption; the global fleet telematics market grew strongly into 2024, sustaining double-digit demand for embedded connectivity. ACTIA’s embedded modules and data services hold strong share in key niches such as coach and industrial fleets, leveraging long OEM relationships. Growth requires continuous certification, carrier partnerships and platform investment; doubling down to capture platform lock‑in is critical before market consolidation accelerates.

Embedded electronics for commercial vehicles

Embedded electronics for commercial vehicles covers onboard ECUs, HMIs and control units for buses, trucks and specialty vehicles where ACTIA already wins specs; OEM program cycles typically run 3–7 years, making ramps real and sticky. In 2024, rising smart/connected vehicle features drive higher content per unit, so funding roadmap depth and synchronized program launches are critical to defend design‑ins.

Rail onboard connectivity & diagnostics

Rail operators accelerated onboard comms and condition monitoring in 2024, creating strong demand for ruggedized electronics; ACTIA’s lifecycle support and proven rail certifications give it strategic footholds. Projects are capital‑intensive and multi‑year, but ACTIA’s staying power converts early investment into long, profitable service tails. ACTIA reported ~€910M revenue in 2024, underlining scale.

Data-driven service platforms

Data-driven service platforms are Stars: remote diagnostics, analytics, and OTA shifted from nice-to-have to mandatory by 2024, and ACTIA’s domain data gives it an edge in actionable insights; high dev burn today but recurring software/service revenue compounds and lifts lifetime margins—keep shipping features and cross-sell into existing hardware bases.

- 2024: OTA/diagnostics mandatory trend

- ACTIA domain data = differentiation

- High current development burn

- Recurring SaaS revenue compounds

- Prioritize feature cadence + cross-sell

Diagnostics & telematics: €910M revenue, SaaS + OTA tailwinds

Vehicle diagnostics, telematics and data services are ACTIA Stars: 2024 revenue ~€910M, strong OEM footholds and rising telematics/OTA mandates drive high growth; they need continued software, certification and carrier investment but deliver recurring SaaS, higher content per vehicle and durable service tails.

| Segment | 2024 signal | Investment need | Payoff |

|---|---|---|---|

| Diagnostics | OEM leadership | SW/protocols | Sticky revenue |

| Telematics | Double‑digit demand | Certs/carrier ties | Platform lock‑in |

| Data services | OTA mandatory 2024 | Dev burn | Recurring SaaS |

What is included in the product

BCG analysis of ACTIA Group’s portfolio, identifying Stars, Cash Cows, Question Marks and Dogs with investment recommendations.

One-page BCG matrix placing each ACTIA business unit in a quadrant, clarifying priorities and easing exec decisions.

Cash Cows

Legacy automotive electronics programs

Legacy automotive electronics programs deliver steady volumes and low churn, with instrumentation/ECU lines typically representing about 30% of ACTIA Group sales and showing low single-digit market growth (~2–3% annually in 2024). Tooling is fully amortized for these platforms, enabling gross margins to improve by 3–5% through scale and process learning. Minimal promotional spend is required; operating leverage drove EBITDA margin uplift to the high single digits in recent periods. Milk these cash cows while enforcing strict quality and cost discipline.

Electronic manufacturing services (mobility-focused)

Established EMS for transportation and industrial clients delivers predictable, recurring orders, supporting stable cash flow while the global EMS market reached an estimated $600 billion in 2024. Process efficiency, certifications and yields underpin strong margins; top-tier EMS yields often exceed 97% in mobility programs. Growth is modest (~3%–5% annual for mature EMS niches); invest selectively in automation to raise cash per build.

Diagnostic hardware tool ranges

Handhelds and test benches show long replacement cycles (typically 5–7 years) and sticky user bases, anchoring a valuable installed base. Accessories, software updates and calibration services generate repeatable, low-cost revenue, often accounting for roughly 15–25% of lifetime product revenues. The diagnostic market is mature with strong price discipline; maintain portfolio and channels and prioritize margin over aggressive share grabs.

Long-lifecycle rail/industrial maintenance contracts

Service, spares, and obsolescence management generate recurring, dependable cash; long-lifecycle rail/industrial maintenance contracts are locked in and deliver incremental growth. Capex light and schedule heavy, margins stem from effective planning and fast response. Optimizing parts planning and SLAs widens contribution and reduces downtime risk.

- Recurring service & spares revenue

- Multi-year locked contracts

- Capex-light, schedule-driven margins

- Optimize parts planning & response SLAs

Telecom infrastructure support modules

Telecom infrastructure support modules are cash cows for ACTIA, driven by steady, replacement-led demand for niche network and communication components with predictable order cadence and high margins.

Market share is stable with low marketing spend; incremental engineering updates keep products compliant with telecom standards and extend lifecycle without major R&D outlays.

Strategy: harvest cash flows, defer large strategic bets unless they are tied to anchored customers or long-term contracts that justify investment.

- steady demand

- low marketing needs

- incremental engineering

- harvest cash

- no big bets unless anchored

Legacy 30%, EMS in $600B market, services harvest cash

Legacy instrumentation/ECU ~30% of sales, low-single-digit growth (2–3% in 2024), margins +3–5% from amortized tooling.

EMS & modules: recurring orders; global EMS market ≈ $600B (2024); yields >97%, mature growth 3–5%.

Services/spares and telecom support are capex-light, multi-year contracts; harvest cash, invest selectively.

| Category | 2024 % | Growth 2024 | EBITDA % |

|---|---|---|---|

| Instrumentation/ECU | ≈30 | 2–3% | high single digits |

| EMS | — | 3–5% | mid–high single digits |

| Services/Telecom | — | stable | mid single digits |

What You’re Viewing Is Included

ACTIA Group BCG Matrix

The file you’re previewing here is the exact ACTIA Group BCG Matrix you’ll receive after purchase—no watermarks, no placeholders, just the finished, professionally formatted report. It’s built for immediate use: editable, printable, and ready to drop into presentations or strategy sessions. Crafted by market-savvy analysts, the content is final and accurate so there are no surprises or follow-up edits needed. Buy once and download instantly—straight to your inbox and your workflow.

Download Your Competitive Advantage

The ACTIA Group BCG Matrix snapshot shows which product lines are driving growth and which are quietly draining resources, giving you a quick read on Stars, Cash Cows, Dogs and Question Marks. This preview scratches the surface—buy the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for where to invest or divest. Get the full report in Word plus a high-level Excel summary so you can present and act fast. Purchase now for a ready-to-use strategic tool that saves you hours of analysis.

Stars

Vehicle diagnostics platforms

Vehicle diagnostics platforms are a core ACTIA strength with deep OEM and aftermarket reach; leadership and integrations raise switching costs while serving a growing market driven by connected and electric fleets (global EV stock exceeded 26.6 million by 2022). The unit soaks up cash for software, protocols and global support but scales profitably with each new program; continued investment is needed to cement standard status and convert late adopters.

Fleet telematics & connectivity modules

Commercial fleets are digitizing rapidly as uptime, regulatory compliance, and TCO reduction drive telematics adoption; the global fleet telematics market grew strongly into 2024, sustaining double-digit demand for embedded connectivity. ACTIA’s embedded modules and data services hold strong share in key niches such as coach and industrial fleets, leveraging long OEM relationships. Growth requires continuous certification, carrier partnerships and platform investment; doubling down to capture platform lock‑in is critical before market consolidation accelerates.

Embedded electronics for commercial vehicles

Embedded electronics for commercial vehicles covers onboard ECUs, HMIs and control units for buses, trucks and specialty vehicles where ACTIA already wins specs; OEM program cycles typically run 3–7 years, making ramps real and sticky. In 2024, rising smart/connected vehicle features drive higher content per unit, so funding roadmap depth and synchronized program launches are critical to defend design‑ins.

Rail onboard connectivity & diagnostics

Rail operators accelerated onboard comms and condition monitoring in 2024, creating strong demand for ruggedized electronics; ACTIA’s lifecycle support and proven rail certifications give it strategic footholds. Projects are capital‑intensive and multi‑year, but ACTIA’s staying power converts early investment into long, profitable service tails. ACTIA reported ~€910M revenue in 2024, underlining scale.

Data-driven service platforms

Data-driven service platforms are Stars: remote diagnostics, analytics, and OTA shifted from nice-to-have to mandatory by 2024, and ACTIA’s domain data gives it an edge in actionable insights; high dev burn today but recurring software/service revenue compounds and lifts lifetime margins—keep shipping features and cross-sell into existing hardware bases.

- 2024: OTA/diagnostics mandatory trend

- ACTIA domain data = differentiation

- High current development burn

- Recurring SaaS revenue compounds

- Prioritize feature cadence + cross-sell

Diagnostics & telematics: €910M revenue, SaaS + OTA tailwinds

Vehicle diagnostics, telematics and data services are ACTIA Stars: 2024 revenue ~€910M, strong OEM footholds and rising telematics/OTA mandates drive high growth; they need continued software, certification and carrier investment but deliver recurring SaaS, higher content per vehicle and durable service tails.

| Segment | 2024 signal | Investment need | Payoff |

|---|---|---|---|

| Diagnostics | OEM leadership | SW/protocols | Sticky revenue |

| Telematics | Double‑digit demand | Certs/carrier ties | Platform lock‑in |

| Data services | OTA mandatory 2024 | Dev burn | Recurring SaaS |

What is included in the product

BCG analysis of ACTIA Group’s portfolio, identifying Stars, Cash Cows, Question Marks and Dogs with investment recommendations.

One-page BCG matrix placing each ACTIA business unit in a quadrant, clarifying priorities and easing exec decisions.

Cash Cows

Legacy automotive electronics programs

Legacy automotive electronics programs deliver steady volumes and low churn, with instrumentation/ECU lines typically representing about 30% of ACTIA Group sales and showing low single-digit market growth (~2–3% annually in 2024). Tooling is fully amortized for these platforms, enabling gross margins to improve by 3–5% through scale and process learning. Minimal promotional spend is required; operating leverage drove EBITDA margin uplift to the high single digits in recent periods. Milk these cash cows while enforcing strict quality and cost discipline.

Electronic manufacturing services (mobility-focused)

Established EMS for transportation and industrial clients delivers predictable, recurring orders, supporting stable cash flow while the global EMS market reached an estimated $600 billion in 2024. Process efficiency, certifications and yields underpin strong margins; top-tier EMS yields often exceed 97% in mobility programs. Growth is modest (~3%–5% annual for mature EMS niches); invest selectively in automation to raise cash per build.

Diagnostic hardware tool ranges

Handhelds and test benches show long replacement cycles (typically 5–7 years) and sticky user bases, anchoring a valuable installed base. Accessories, software updates and calibration services generate repeatable, low-cost revenue, often accounting for roughly 15–25% of lifetime product revenues. The diagnostic market is mature with strong price discipline; maintain portfolio and channels and prioritize margin over aggressive share grabs.

Long-lifecycle rail/industrial maintenance contracts

Service, spares, and obsolescence management generate recurring, dependable cash; long-lifecycle rail/industrial maintenance contracts are locked in and deliver incremental growth. Capex light and schedule heavy, margins stem from effective planning and fast response. Optimizing parts planning and SLAs widens contribution and reduces downtime risk.

- Recurring service & spares revenue

- Multi-year locked contracts

- Capex-light, schedule-driven margins

- Optimize parts planning & response SLAs

Telecom infrastructure support modules

Telecom infrastructure support modules are cash cows for ACTIA, driven by steady, replacement-led demand for niche network and communication components with predictable order cadence and high margins.

Market share is stable with low marketing spend; incremental engineering updates keep products compliant with telecom standards and extend lifecycle without major R&D outlays.

Strategy: harvest cash flows, defer large strategic bets unless they are tied to anchored customers or long-term contracts that justify investment.

- steady demand

- low marketing needs

- incremental engineering

- harvest cash

- no big bets unless anchored

Legacy 30%, EMS in $600B market, services harvest cash

Legacy instrumentation/ECU ~30% of sales, low-single-digit growth (2–3% in 2024), margins +3–5% from amortized tooling.

EMS & modules: recurring orders; global EMS market ≈ $600B (2024); yields >97%, mature growth 3–5%.

Services/spares and telecom support are capex-light, multi-year contracts; harvest cash, invest selectively.

| Category | 2024 % | Growth 2024 | EBITDA % |

|---|---|---|---|

| Instrumentation/ECU | ≈30 | 2–3% | high single digits |

| EMS | — | 3–5% | mid–high single digits |

| Services/Telecom | — | stable | mid single digits |

What You’re Viewing Is Included

ACTIA Group BCG Matrix

The file you’re previewing here is the exact ACTIA Group BCG Matrix you’ll receive after purchase—no watermarks, no placeholders, just the finished, professionally formatted report. It’s built for immediate use: editable, printable, and ready to drop into presentations or strategy sessions. Crafted by market-savvy analysts, the content is final and accurate so there are no surprises or follow-up edits needed. Buy once and download instantly—straight to your inbox and your workflow.

Description

Download Your Competitive Advantage

The ACTIA Group BCG Matrix snapshot shows which product lines are driving growth and which are quietly draining resources, giving you a quick read on Stars, Cash Cows, Dogs and Question Marks. This preview scratches the surface—buy the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and a clear roadmap for where to invest or divest. Get the full report in Word plus a high-level Excel summary so you can present and act fast. Purchase now for a ready-to-use strategic tool that saves you hours of analysis.

Stars

Vehicle diagnostics platforms

Vehicle diagnostics platforms are a core ACTIA strength with deep OEM and aftermarket reach; leadership and integrations raise switching costs while serving a growing market driven by connected and electric fleets (global EV stock exceeded 26.6 million by 2022). The unit soaks up cash for software, protocols and global support but scales profitably with each new program; continued investment is needed to cement standard status and convert late adopters.

Fleet telematics & connectivity modules

Commercial fleets are digitizing rapidly as uptime, regulatory compliance, and TCO reduction drive telematics adoption; the global fleet telematics market grew strongly into 2024, sustaining double-digit demand for embedded connectivity. ACTIA’s embedded modules and data services hold strong share in key niches such as coach and industrial fleets, leveraging long OEM relationships. Growth requires continuous certification, carrier partnerships and platform investment; doubling down to capture platform lock‑in is critical before market consolidation accelerates.

Embedded electronics for commercial vehicles

Embedded electronics for commercial vehicles covers onboard ECUs, HMIs and control units for buses, trucks and specialty vehicles where ACTIA already wins specs; OEM program cycles typically run 3–7 years, making ramps real and sticky. In 2024, rising smart/connected vehicle features drive higher content per unit, so funding roadmap depth and synchronized program launches are critical to defend design‑ins.

Rail onboard connectivity & diagnostics

Rail operators accelerated onboard comms and condition monitoring in 2024, creating strong demand for ruggedized electronics; ACTIA’s lifecycle support and proven rail certifications give it strategic footholds. Projects are capital‑intensive and multi‑year, but ACTIA’s staying power converts early investment into long, profitable service tails. ACTIA reported ~€910M revenue in 2024, underlining scale.

Data-driven service platforms

Data-driven service platforms are Stars: remote diagnostics, analytics, and OTA shifted from nice-to-have to mandatory by 2024, and ACTIA’s domain data gives it an edge in actionable insights; high dev burn today but recurring software/service revenue compounds and lifts lifetime margins—keep shipping features and cross-sell into existing hardware bases.

- 2024: OTA/diagnostics mandatory trend

- ACTIA domain data = differentiation

- High current development burn

- Recurring SaaS revenue compounds

- Prioritize feature cadence + cross-sell

Diagnostics & telematics: €910M revenue, SaaS + OTA tailwinds

Vehicle diagnostics, telematics and data services are ACTIA Stars: 2024 revenue ~€910M, strong OEM footholds and rising telematics/OTA mandates drive high growth; they need continued software, certification and carrier investment but deliver recurring SaaS, higher content per vehicle and durable service tails.

| Segment | 2024 signal | Investment need | Payoff |

|---|---|---|---|

| Diagnostics | OEM leadership | SW/protocols | Sticky revenue |

| Telematics | Double‑digit demand | Certs/carrier ties | Platform lock‑in |

| Data services | OTA mandatory 2024 | Dev burn | Recurring SaaS |

What is included in the product

BCG analysis of ACTIA Group’s portfolio, identifying Stars, Cash Cows, Question Marks and Dogs with investment recommendations.

One-page BCG matrix placing each ACTIA business unit in a quadrant, clarifying priorities and easing exec decisions.

Cash Cows

Legacy automotive electronics programs

Legacy automotive electronics programs deliver steady volumes and low churn, with instrumentation/ECU lines typically representing about 30% of ACTIA Group sales and showing low single-digit market growth (~2–3% annually in 2024). Tooling is fully amortized for these platforms, enabling gross margins to improve by 3–5% through scale and process learning. Minimal promotional spend is required; operating leverage drove EBITDA margin uplift to the high single digits in recent periods. Milk these cash cows while enforcing strict quality and cost discipline.

Electronic manufacturing services (mobility-focused)

Established EMS for transportation and industrial clients delivers predictable, recurring orders, supporting stable cash flow while the global EMS market reached an estimated $600 billion in 2024. Process efficiency, certifications and yields underpin strong margins; top-tier EMS yields often exceed 97% in mobility programs. Growth is modest (~3%–5% annual for mature EMS niches); invest selectively in automation to raise cash per build.

Diagnostic hardware tool ranges

Handhelds and test benches show long replacement cycles (typically 5–7 years) and sticky user bases, anchoring a valuable installed base. Accessories, software updates and calibration services generate repeatable, low-cost revenue, often accounting for roughly 15–25% of lifetime product revenues. The diagnostic market is mature with strong price discipline; maintain portfolio and channels and prioritize margin over aggressive share grabs.

Long-lifecycle rail/industrial maintenance contracts

Service, spares, and obsolescence management generate recurring, dependable cash; long-lifecycle rail/industrial maintenance contracts are locked in and deliver incremental growth. Capex light and schedule heavy, margins stem from effective planning and fast response. Optimizing parts planning and SLAs widens contribution and reduces downtime risk.

- Recurring service & spares revenue

- Multi-year locked contracts

- Capex-light, schedule-driven margins

- Optimize parts planning & response SLAs

Telecom infrastructure support modules

Telecom infrastructure support modules are cash cows for ACTIA, driven by steady, replacement-led demand for niche network and communication components with predictable order cadence and high margins.

Market share is stable with low marketing spend; incremental engineering updates keep products compliant with telecom standards and extend lifecycle without major R&D outlays.

Strategy: harvest cash flows, defer large strategic bets unless they are tied to anchored customers or long-term contracts that justify investment.

- steady demand

- low marketing needs

- incremental engineering

- harvest cash

- no big bets unless anchored

Legacy 30%, EMS in $600B market, services harvest cash

Legacy instrumentation/ECU ~30% of sales, low-single-digit growth (2–3% in 2024), margins +3–5% from amortized tooling.

EMS & modules: recurring orders; global EMS market ≈ $600B (2024); yields >97%, mature growth 3–5%.

Services/spares and telecom support are capex-light, multi-year contracts; harvest cash, invest selectively.

| Category | 2024 % | Growth 2024 | EBITDA % |

|---|---|---|---|

| Instrumentation/ECU | ≈30 | 2–3% | high single digits |

| EMS | — | 3–5% | mid–high single digits |

| Services/Telecom | — | stable | mid single digits |

What You’re Viewing Is Included

ACTIA Group BCG Matrix

The file you’re previewing here is the exact ACTIA Group BCG Matrix you’ll receive after purchase—no watermarks, no placeholders, just the finished, professionally formatted report. It’s built for immediate use: editable, printable, and ready to drop into presentations or strategy sessions. Crafted by market-savvy analysts, the content is final and accurate so there are no surprises or follow-up edits needed. Buy once and download instantly—straight to your inbox and your workflow.