Addnode Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

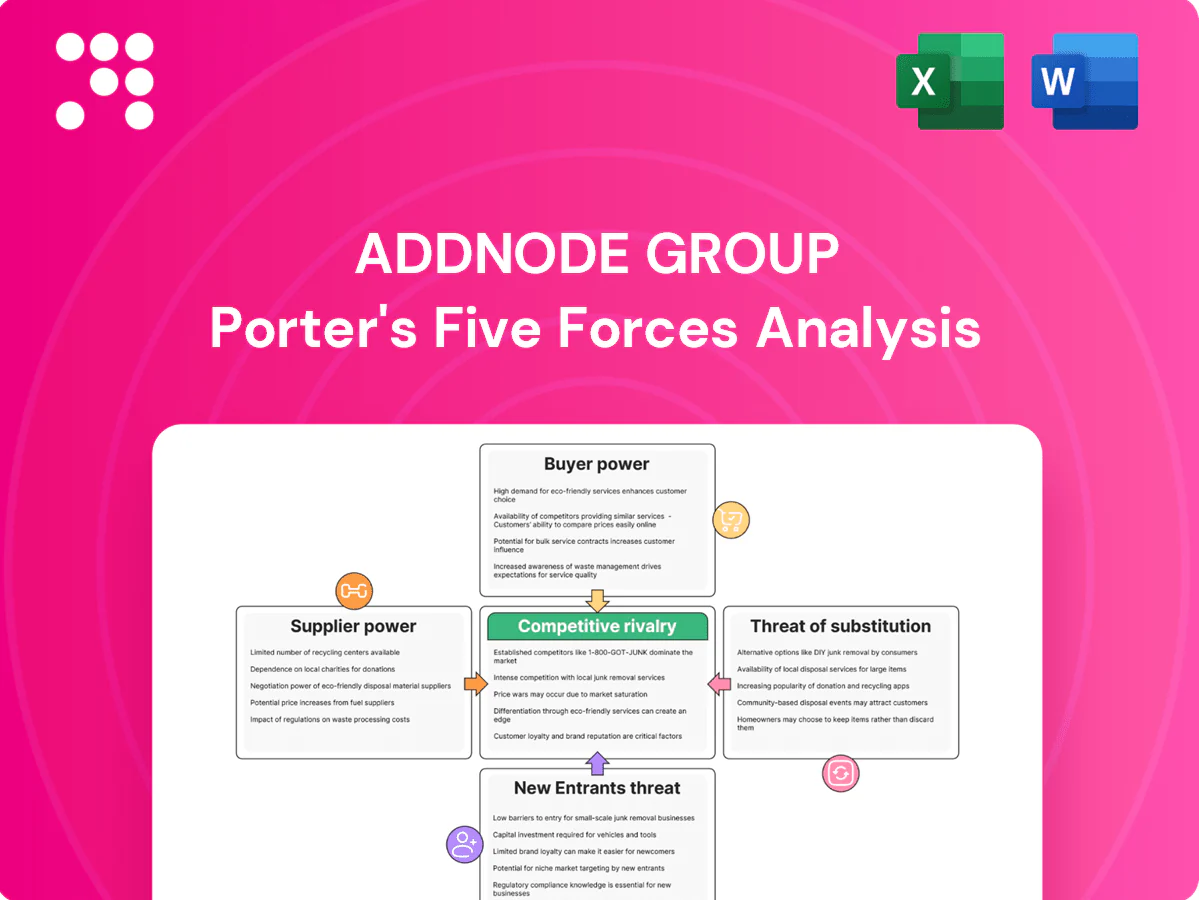

This snapshot outlines key competitive pressures facing Addnode Group, from buyer leverage to rivalry intensity. The full Porter's Five Forces Analysis reveals force-by-force ratings, supplier influence and threat of new entrants in actionable detail. Ready to deepen your strategic view? Unlock the complete report for consultant-grade insights and visuals to inform investment or strategy.

Suppliers Bargaining Power

Dependence on OEM Principals

Addnode relies on OEM principals such as Autodesk (FY2023 revenue $4.39bn), Dassault, Siemens and PTC for licenses, certifications and roadmap access, with Addnode Group reporting net sales SEK 3,966m in 2023; these vendors set pricing, discount structures and partner terms, concentrating power upstream. Any channel-policy change or direct-selling push from these principals can compress Addnode margins and limit solution flexibility.

Scarce Specialist Talent

Skilled PLM, CAD and BIM consultants are scarce, commanding wage premiums often exceeding 15% in 2024; labor-market supplier power spikes in peak project cycles, driving delivery-cost uplifts of 5–12% for firms like Addnode. Retention and targeted training now require ongoing investments—typically 8–12% of total HR spend—to stabilize capability and lower external dependence.

Cloud and Infrastructure Providers

Reliance on hyperscalers for hosting, AI and data gives concentrated supplier power; AWS, Azure and GCP held about 65% of the global IaaS/PaaS market in 2024 (AWS 31%, Azure 23%, GCP 11%). Price hikes or feature deprecations can raise operating costs and stress SLAs. Enterprise agreements mitigate but do not eliminate dependency.

Data and Content Providers

Geospatial and engineering content licensors control critical datasets and usage rights, creating concentrated supplier power that can constrain Addnode Group’s product feature set and delivery timelines. Sudden shifts to usage‑based or tiered licensing models can materially raise solution total cost of ownership and limit advanced analytics or ML use cases. Addnode mitigates exposure through multi‑source vendor strategies, open data adoption and investing in internal data pipelines and normalization.

- Supplier concentration: critical dataset control

- Licensing risk: raises TCO, limits analytics

- Mitigation: multi‑source + internal pipelines

M&A Target Valuations

The buy-and-build model depends on acquiring niche firms at fair multiples, but competitive auctions and strategic bidders elevate prices and shift value to sellers.

Empirical auction premia are often cited at ~20–30% and Nordic software median EV/EBITDA in 2024 sat near 10–14x; discipline in synergy capture and 6–12 month integration speed is essential to preserve returns.

- Buy-and-build sensitivity: high

- Auction premia: ~20–30%

- 2024 Nordic software EV/EBITDA: ~10–14x

- Integration horizon: 6–12 months

OEM concentration, >15% wage premium, ~65% hyperscaler share and licensing risk hurt margins

Addnode faces concentrated OEM power (Autodesk FY2023 revenue 4.39bn USD) versus Addnode sales SEK 3,966m (2023), exposing margin risk. Skilled PLM/CAD/BIM talent commanded >15% wage premium in 2024, raising delivery costs. Hyperscalers held ~65% IaaS/PaaS market share in 2024, creating hosting dependency. Data licensors’ licensing shifts can spike TCO and limit analytics.

| Supplier | Key stat | Impact | Mitigation |

|---|---|---|---|

| OEMs | Autodesk 4.39bn (FY2023) | Pricing power | Multi-vendor |

| Talent | >15% wage premium (2024) | Higher delivery costs | Training/retention |

| Hyperscalers | ~65% market (2024) | Cloud dependency | Enterprise deals |

| Data licensors | Tiered licensing risk | Higher TCO | Internal pipelines |

What is included in the product

Comprehensive Porter’s Five Forces analysis for Addnode Group, identifying competitive rivalry, supplier and buyer bargaining power, substitution risks, and entry barriers, with strategic insights on threats and defensive levers.

Clear one-sheet Porter's Five Forces for Addnode Group—instantly highlights competitive pressures and strategic levers to relieve decision-making pain points. Drag-and-drop inputs and a radar chart make it easy to model scenarios, update with new data, and export to decks or reports.

Customers Bargaining Power

Enterprise Consolidation and RFPs

Enterprise consolidation and formal RFP processes among large manufacturers, AEC firms and public bodies—public procurement representing about 14% of EU GDP—force vendor rationalization, driving demands for volume discounts, outcome-based SLAs and multi-year pricing protection. This concentrated buying power raises leverage across Addnode Group’s regional and product portfolios, pressuring margins and contract terms.

High Switching Costs, Yet Negotiation Leverage

Deeply embedded workflows, extensive integrations and user training create strong lock-in for Addnode Group clients, raising switching costs and reducing churn. Buyers still extract leverage by threatening to move modules or providers during procurement and renewal negotiations. Renewal cycles represent peak buyer power, when discounts and contract concessions are most often demanded. This dynamic keeps pricing discipline while protecting long-term recurring revenue.

Budget Cyclicality and Project Funding

Capex cycles in manufacturing and construction drive timing and scope of Addnode Group sales; with Addnode reporting about SEK 4.6 billion in net sales in 2023, capital spending slowdowns compress recurring license and implementation work in downturns. Buyers commonly defer upgrades or scale back services to extract price concessions, pressuring margins and lengthening sales cycles. Flexible packaging and managed services help cushion demand swings by shifting clients to OPEX models and recurring revenue.

Interoperability and Open Standards Demands

Customers insist on open formats and cross-vendor integrations to avoid vendor lock-in, and Addnode must support this while complying with BIM mandates and data sovereignty rules such as GDPR, which carries fines up to 4% of global turnover or €20m; meeting these requirements increases delivery complexity and strengthens buyer leverage.

Public Sector Procurement Rules

Public procurement frameworks and certifications (eg ISO/IEC) plus strict tender rules shape Addnode deal structure and margins, with transparent pricing and audit trails required. Auditability limits upsell latitude while long public contracts (often 3–7 years) stabilize revenue but compress initial pricing; EU public procurement accounts for ~14% of GDP, strengthening buyer leverage.

- Frameworks: strict tenders

- Certs: ISO/IEC mandatory

- Pricing: transparent, auditable

- Contract length: 3–7 years

Concentrated buyers squeeze margins as 14% procurement and 4% GDPR fines raise leverage

Concentrated buyers and formal RFPs (EU public procurement ~14% of GDP in 2024) force rationalization, discounts and outcome-based SLAs, squeezing margins.

High integration and training create strong lock-in, lowering churn but giving buyers leverage at renewals to demand concessions.

Capex cycles and compliance (GDPR 4% of turnover or €20m) shift demand and raise delivery complexity, favoring OPEX models.

| Metric | Value |

|---|---|

| Addnode sales (2023) | SEK 4.6bn |

| EU public procurement (2024) | ~14% GDP |

| GDPR fine | 4% turnover or €20m |

| Public contract length | 3–7 yrs |

Full Version Awaits

Addnode Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Addnode Group you'll receive immediately after purchase—fully formatted and ready to use. The document assesses competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants, offering actionable strategic insights. No samples, no placeholders.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot outlines key competitive pressures facing Addnode Group, from buyer leverage to rivalry intensity. The full Porter's Five Forces Analysis reveals force-by-force ratings, supplier influence and threat of new entrants in actionable detail. Ready to deepen your strategic view? Unlock the complete report for consultant-grade insights and visuals to inform investment or strategy.

Suppliers Bargaining Power

Dependence on OEM Principals

Addnode relies on OEM principals such as Autodesk (FY2023 revenue $4.39bn), Dassault, Siemens and PTC for licenses, certifications and roadmap access, with Addnode Group reporting net sales SEK 3,966m in 2023; these vendors set pricing, discount structures and partner terms, concentrating power upstream. Any channel-policy change or direct-selling push from these principals can compress Addnode margins and limit solution flexibility.

Scarce Specialist Talent

Skilled PLM, CAD and BIM consultants are scarce, commanding wage premiums often exceeding 15% in 2024; labor-market supplier power spikes in peak project cycles, driving delivery-cost uplifts of 5–12% for firms like Addnode. Retention and targeted training now require ongoing investments—typically 8–12% of total HR spend—to stabilize capability and lower external dependence.

Cloud and Infrastructure Providers

Reliance on hyperscalers for hosting, AI and data gives concentrated supplier power; AWS, Azure and GCP held about 65% of the global IaaS/PaaS market in 2024 (AWS 31%, Azure 23%, GCP 11%). Price hikes or feature deprecations can raise operating costs and stress SLAs. Enterprise agreements mitigate but do not eliminate dependency.

Data and Content Providers

Geospatial and engineering content licensors control critical datasets and usage rights, creating concentrated supplier power that can constrain Addnode Group’s product feature set and delivery timelines. Sudden shifts to usage‑based or tiered licensing models can materially raise solution total cost of ownership and limit advanced analytics or ML use cases. Addnode mitigates exposure through multi‑source vendor strategies, open data adoption and investing in internal data pipelines and normalization.

- Supplier concentration: critical dataset control

- Licensing risk: raises TCO, limits analytics

- Mitigation: multi‑source + internal pipelines

M&A Target Valuations

The buy-and-build model depends on acquiring niche firms at fair multiples, but competitive auctions and strategic bidders elevate prices and shift value to sellers.

Empirical auction premia are often cited at ~20–30% and Nordic software median EV/EBITDA in 2024 sat near 10–14x; discipline in synergy capture and 6–12 month integration speed is essential to preserve returns.

- Buy-and-build sensitivity: high

- Auction premia: ~20–30%

- 2024 Nordic software EV/EBITDA: ~10–14x

- Integration horizon: 6–12 months

OEM concentration, >15% wage premium, ~65% hyperscaler share and licensing risk hurt margins

Addnode faces concentrated OEM power (Autodesk FY2023 revenue 4.39bn USD) versus Addnode sales SEK 3,966m (2023), exposing margin risk. Skilled PLM/CAD/BIM talent commanded >15% wage premium in 2024, raising delivery costs. Hyperscalers held ~65% IaaS/PaaS market share in 2024, creating hosting dependency. Data licensors’ licensing shifts can spike TCO and limit analytics.

| Supplier | Key stat | Impact | Mitigation |

|---|---|---|---|

| OEMs | Autodesk 4.39bn (FY2023) | Pricing power | Multi-vendor |

| Talent | >15% wage premium (2024) | Higher delivery costs | Training/retention |

| Hyperscalers | ~65% market (2024) | Cloud dependency | Enterprise deals |

| Data licensors | Tiered licensing risk | Higher TCO | Internal pipelines |

What is included in the product

Comprehensive Porter’s Five Forces analysis for Addnode Group, identifying competitive rivalry, supplier and buyer bargaining power, substitution risks, and entry barriers, with strategic insights on threats and defensive levers.

Clear one-sheet Porter's Five Forces for Addnode Group—instantly highlights competitive pressures and strategic levers to relieve decision-making pain points. Drag-and-drop inputs and a radar chart make it easy to model scenarios, update with new data, and export to decks or reports.

Customers Bargaining Power

Enterprise Consolidation and RFPs

Enterprise consolidation and formal RFP processes among large manufacturers, AEC firms and public bodies—public procurement representing about 14% of EU GDP—force vendor rationalization, driving demands for volume discounts, outcome-based SLAs and multi-year pricing protection. This concentrated buying power raises leverage across Addnode Group’s regional and product portfolios, pressuring margins and contract terms.

High Switching Costs, Yet Negotiation Leverage

Deeply embedded workflows, extensive integrations and user training create strong lock-in for Addnode Group clients, raising switching costs and reducing churn. Buyers still extract leverage by threatening to move modules or providers during procurement and renewal negotiations. Renewal cycles represent peak buyer power, when discounts and contract concessions are most often demanded. This dynamic keeps pricing discipline while protecting long-term recurring revenue.

Budget Cyclicality and Project Funding

Capex cycles in manufacturing and construction drive timing and scope of Addnode Group sales; with Addnode reporting about SEK 4.6 billion in net sales in 2023, capital spending slowdowns compress recurring license and implementation work in downturns. Buyers commonly defer upgrades or scale back services to extract price concessions, pressuring margins and lengthening sales cycles. Flexible packaging and managed services help cushion demand swings by shifting clients to OPEX models and recurring revenue.

Interoperability and Open Standards Demands

Customers insist on open formats and cross-vendor integrations to avoid vendor lock-in, and Addnode must support this while complying with BIM mandates and data sovereignty rules such as GDPR, which carries fines up to 4% of global turnover or €20m; meeting these requirements increases delivery complexity and strengthens buyer leverage.

Public Sector Procurement Rules

Public procurement frameworks and certifications (eg ISO/IEC) plus strict tender rules shape Addnode deal structure and margins, with transparent pricing and audit trails required. Auditability limits upsell latitude while long public contracts (often 3–7 years) stabilize revenue but compress initial pricing; EU public procurement accounts for ~14% of GDP, strengthening buyer leverage.

- Frameworks: strict tenders

- Certs: ISO/IEC mandatory

- Pricing: transparent, auditable

- Contract length: 3–7 years

Concentrated buyers squeeze margins as 14% procurement and 4% GDPR fines raise leverage

Concentrated buyers and formal RFPs (EU public procurement ~14% of GDP in 2024) force rationalization, discounts and outcome-based SLAs, squeezing margins.

High integration and training create strong lock-in, lowering churn but giving buyers leverage at renewals to demand concessions.

Capex cycles and compliance (GDPR 4% of turnover or €20m) shift demand and raise delivery complexity, favoring OPEX models.

| Metric | Value |

|---|---|

| Addnode sales (2023) | SEK 4.6bn |

| EU public procurement (2024) | ~14% GDP |

| GDPR fine | 4% turnover or €20m |

| Public contract length | 3–7 yrs |

Full Version Awaits

Addnode Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Addnode Group you'll receive immediately after purchase—fully formatted and ready to use. The document assesses competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants, offering actionable strategic insights. No samples, no placeholders.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

This snapshot outlines key competitive pressures facing Addnode Group, from buyer leverage to rivalry intensity. The full Porter's Five Forces Analysis reveals force-by-force ratings, supplier influence and threat of new entrants in actionable detail. Ready to deepen your strategic view? Unlock the complete report for consultant-grade insights and visuals to inform investment or strategy.

Suppliers Bargaining Power

Dependence on OEM Principals

Addnode relies on OEM principals such as Autodesk (FY2023 revenue $4.39bn), Dassault, Siemens and PTC for licenses, certifications and roadmap access, with Addnode Group reporting net sales SEK 3,966m in 2023; these vendors set pricing, discount structures and partner terms, concentrating power upstream. Any channel-policy change or direct-selling push from these principals can compress Addnode margins and limit solution flexibility.

Scarce Specialist Talent

Skilled PLM, CAD and BIM consultants are scarce, commanding wage premiums often exceeding 15% in 2024; labor-market supplier power spikes in peak project cycles, driving delivery-cost uplifts of 5–12% for firms like Addnode. Retention and targeted training now require ongoing investments—typically 8–12% of total HR spend—to stabilize capability and lower external dependence.

Cloud and Infrastructure Providers

Reliance on hyperscalers for hosting, AI and data gives concentrated supplier power; AWS, Azure and GCP held about 65% of the global IaaS/PaaS market in 2024 (AWS 31%, Azure 23%, GCP 11%). Price hikes or feature deprecations can raise operating costs and stress SLAs. Enterprise agreements mitigate but do not eliminate dependency.

Data and Content Providers

Geospatial and engineering content licensors control critical datasets and usage rights, creating concentrated supplier power that can constrain Addnode Group’s product feature set and delivery timelines. Sudden shifts to usage‑based or tiered licensing models can materially raise solution total cost of ownership and limit advanced analytics or ML use cases. Addnode mitigates exposure through multi‑source vendor strategies, open data adoption and investing in internal data pipelines and normalization.

- Supplier concentration: critical dataset control

- Licensing risk: raises TCO, limits analytics

- Mitigation: multi‑source + internal pipelines

M&A Target Valuations

The buy-and-build model depends on acquiring niche firms at fair multiples, but competitive auctions and strategic bidders elevate prices and shift value to sellers.

Empirical auction premia are often cited at ~20–30% and Nordic software median EV/EBITDA in 2024 sat near 10–14x; discipline in synergy capture and 6–12 month integration speed is essential to preserve returns.

- Buy-and-build sensitivity: high

- Auction premia: ~20–30%

- 2024 Nordic software EV/EBITDA: ~10–14x

- Integration horizon: 6–12 months

OEM concentration, >15% wage premium, ~65% hyperscaler share and licensing risk hurt margins

Addnode faces concentrated OEM power (Autodesk FY2023 revenue 4.39bn USD) versus Addnode sales SEK 3,966m (2023), exposing margin risk. Skilled PLM/CAD/BIM talent commanded >15% wage premium in 2024, raising delivery costs. Hyperscalers held ~65% IaaS/PaaS market share in 2024, creating hosting dependency. Data licensors’ licensing shifts can spike TCO and limit analytics.

| Supplier | Key stat | Impact | Mitigation |

|---|---|---|---|

| OEMs | Autodesk 4.39bn (FY2023) | Pricing power | Multi-vendor |

| Talent | >15% wage premium (2024) | Higher delivery costs | Training/retention |

| Hyperscalers | ~65% market (2024) | Cloud dependency | Enterprise deals |

| Data licensors | Tiered licensing risk | Higher TCO | Internal pipelines |

What is included in the product

Comprehensive Porter’s Five Forces analysis for Addnode Group, identifying competitive rivalry, supplier and buyer bargaining power, substitution risks, and entry barriers, with strategic insights on threats and defensive levers.

Clear one-sheet Porter's Five Forces for Addnode Group—instantly highlights competitive pressures and strategic levers to relieve decision-making pain points. Drag-and-drop inputs and a radar chart make it easy to model scenarios, update with new data, and export to decks or reports.

Customers Bargaining Power

Enterprise Consolidation and RFPs

Enterprise consolidation and formal RFP processes among large manufacturers, AEC firms and public bodies—public procurement representing about 14% of EU GDP—force vendor rationalization, driving demands for volume discounts, outcome-based SLAs and multi-year pricing protection. This concentrated buying power raises leverage across Addnode Group’s regional and product portfolios, pressuring margins and contract terms.

High Switching Costs, Yet Negotiation Leverage

Deeply embedded workflows, extensive integrations and user training create strong lock-in for Addnode Group clients, raising switching costs and reducing churn. Buyers still extract leverage by threatening to move modules or providers during procurement and renewal negotiations. Renewal cycles represent peak buyer power, when discounts and contract concessions are most often demanded. This dynamic keeps pricing discipline while protecting long-term recurring revenue.

Budget Cyclicality and Project Funding

Capex cycles in manufacturing and construction drive timing and scope of Addnode Group sales; with Addnode reporting about SEK 4.6 billion in net sales in 2023, capital spending slowdowns compress recurring license and implementation work in downturns. Buyers commonly defer upgrades or scale back services to extract price concessions, pressuring margins and lengthening sales cycles. Flexible packaging and managed services help cushion demand swings by shifting clients to OPEX models and recurring revenue.

Interoperability and Open Standards Demands

Customers insist on open formats and cross-vendor integrations to avoid vendor lock-in, and Addnode must support this while complying with BIM mandates and data sovereignty rules such as GDPR, which carries fines up to 4% of global turnover or €20m; meeting these requirements increases delivery complexity and strengthens buyer leverage.

Public Sector Procurement Rules

Public procurement frameworks and certifications (eg ISO/IEC) plus strict tender rules shape Addnode deal structure and margins, with transparent pricing and audit trails required. Auditability limits upsell latitude while long public contracts (often 3–7 years) stabilize revenue but compress initial pricing; EU public procurement accounts for ~14% of GDP, strengthening buyer leverage.

- Frameworks: strict tenders

- Certs: ISO/IEC mandatory

- Pricing: transparent, auditable

- Contract length: 3–7 years

Concentrated buyers squeeze margins as 14% procurement and 4% GDPR fines raise leverage

Concentrated buyers and formal RFPs (EU public procurement ~14% of GDP in 2024) force rationalization, discounts and outcome-based SLAs, squeezing margins.

High integration and training create strong lock-in, lowering churn but giving buyers leverage at renewals to demand concessions.

Capex cycles and compliance (GDPR 4% of turnover or €20m) shift demand and raise delivery complexity, favoring OPEX models.

| Metric | Value |

|---|---|

| Addnode sales (2023) | SEK 4.6bn |

| EU public procurement (2024) | ~14% GDP |

| GDPR fine | 4% turnover or €20m |

| Public contract length | 3–7 yrs |

Full Version Awaits

Addnode Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Addnode Group you'll receive immediately after purchase—fully formatted and ready to use. The document assesses competitive rivalry, supplier and buyer power, and the threats of substitutes and new entrants, offering actionable strategic insights. No samples, no placeholders.