Addnode Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

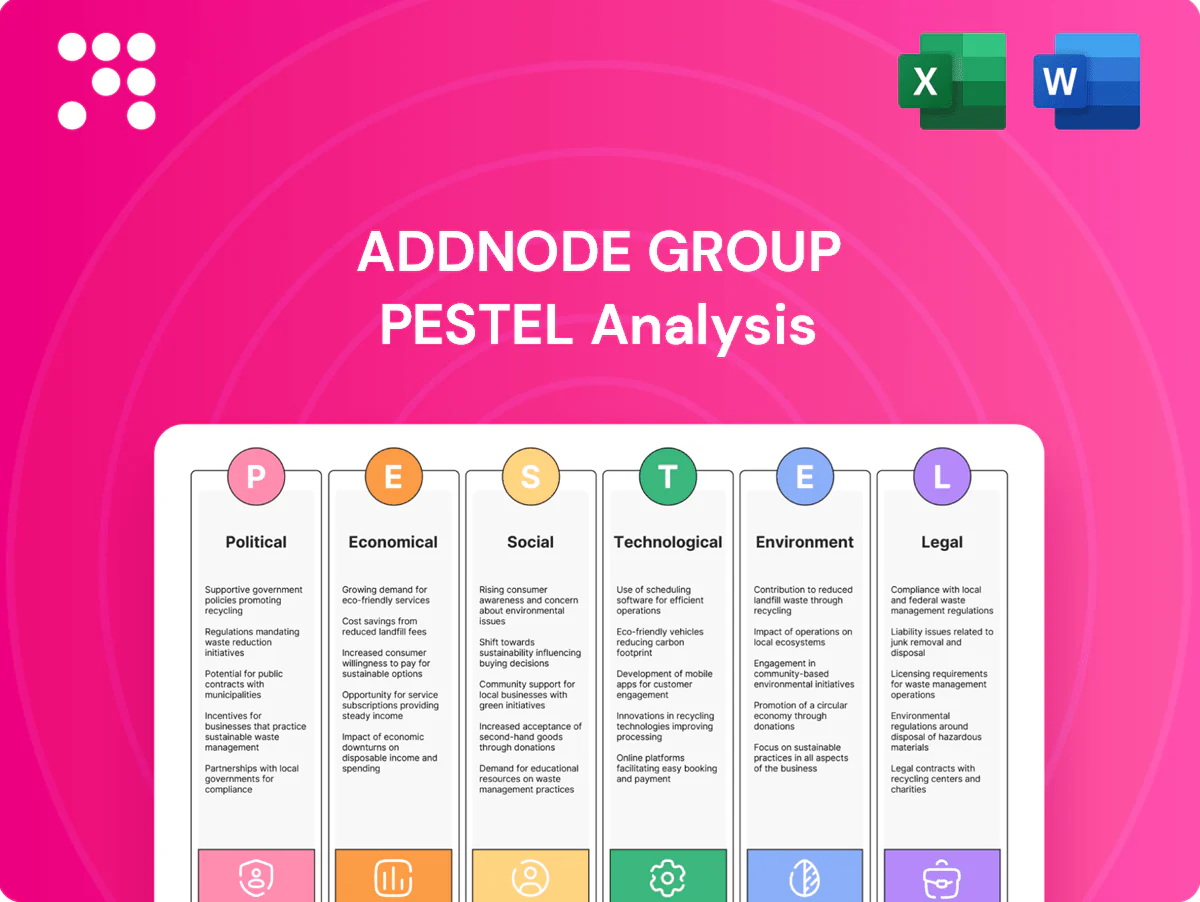

Gain strategic clarity with our PESTLE analysis of Addnode Group—an incisive look at political, economic, social, technological, legal and environmental forces shaping growth and risk. Ideal for investors and strategists, it translates macro trends into actionable implications. Buy the full, editable report now for instant, board‑ready insights.

Political factors

EU digital policies

EU digitalization drives demand for CAD/BIM/PLM via programmes like Digital Europe (€7.5bn for 2021–27) and NextGenerationEU recovery funds (€806.9bn), plus Data Act/Data Spaces initiatives shaping cross-border data use. Harmonized standards and targeted grants can accelerate public procurement cycles, while shifts in industrial subsidy focus may reweight verticals. Addnode’s European footprint benefits commercially but increases compliance complexity.

Public procurement reliance

Geographic IT and BIM solutions for government and municipalities face procurement-driven timing and scope shifts, with public procurement in Sweden roughly SEK 700 billion annually and EU NextGenerationEU recovery funds near €800 billion supporting large projects. Tender dynamics, budget cycles and political leadership changes create 6–24 month sales cycles and scope volatility. Transparent rules aid access, yet persistent price pressure and lengthy procurements constrain margins despite policy-driven infrastructure investments that can trigger step-change demand.

Infrastructure and housing agendas

National commitments such as the US Bipartisan Infrastructure Law (~$1.2 trillion) and the UK 300,000 homes-per-year target drive BIM/CAD adoption across transport, housing and resilience programs. Stimulus or austerity swings—visible in €723.8bn EU Recovery and Resilience Facility allocations—shift project pipelines for engineering clients. Urban planning emphasis boosts demand for geospatial solutions, while election outcomes can reprioritize capital projects and permitting timelines.

Defense and critical infrastructure

Heightened geopolitical risk is driving higher defense and secure-infrastructure spending, with global military expenditure surpassing 2.4 trillion USD in 2024, increasing demand for PLM tailored to aerospace and defense that meet strict compliance and cybersecurity standards. Export controls and security-clearance requirements raise barriers but create high-margin niches for certified vendors, while political scrutiny of supply chains tightens vendor selection and due-diligence requirements.

- Defense spend: >2.4T USD (2024)

- PLM needs: compliance + security

- Barriers: export controls, clearances

- Vendor risk: supply-chain political scrutiny

Nordic policy stability

Nordic regulatory stability underpins long-term software and service contracts for Addnode, with EU Digital Europe funding of €1.9bn (2021–2027) and OECD R&D intensity at ~3.4% GDP in Sweden (2022) catalyzing innovation and digital twin pilots; shifts in corporate taxation or labor rules can compress margins and raise hiring costs, while strong regional cooperation drives cross-border BIM/PLM standardization.

- Stable regs: supports multi-year contracts

- Funding: EU Digital Europe €1.9bn

- R&D: Sweden ~3.4% GDP (2022)

- Risks: tax/labor shifts affect margins

- Benefit: Nordic cooperation → BIM/PLM standards

EU and US mega-funding boost CAD/BIM/PLM as procurement and compliance squeeze margins

EU and national digitalization funds (Digital Europe €7.5bn 2021–27; NextGenerationEU €806.9bn) plus US Bipartisan Infrastructure ~$1.2T drive CAD/BIM/PLM demand while raising compliance burdens. Public procurement (Sweden ~SEK 700bn) and 6–24 month tender cycles create timing and margin pressure. Geopolitical tension (global military spend >$2.4T 2024) expands certified PLM niches amid export controls and supply-chain scrutiny.

| Policy/Region | Key figure | Impact |

|---|---|---|

| Digital Europe | €7.5bn (2021–27) | Push for digital twin/BIM |

| NextGenerationEU | €806.9bn | Large infrastructure pipelines |

| Sweden procurement | ~SEK 700bn/yr | Procurement-driven demand timing |

| Global defense spend | >$2.4T (2024) | High-margin secure PLM demand |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Addnode Group across Political, Economic, Social, Technological, Environmental and Legal dimensions. Each section is data-backed with forward-looking insights to support strategic planning, risk management and investor communications.

A concise, visually segmented PESTLE summary for Addnode Group that’s editable by region or business line, easily dropped into slides or reports, and shareable for quick alignment to support external risk and market-positioning discussions.

Economic factors

Capex cycles

Addnode Group (Nasdaq Stockholm ADN B) serves cyclical engineering, construction and manufacturing customers, so capex pullbacks tend to delay software upgrades and new-seat purchases. Services and maintenance revenue historically cushions downturns, supporting recurring margins. Recovery phases drive demand for PLM/BIM modernization and cloud migrations as clients resume digital investments. Geographic and vertical diversification reduces revenue volatility for the group.

Interest rates and M&A

Addnode's buy-and-build model is sensitive to financing conditions; with Sweden's Riksbank policy rate at 4.00% (Dec 2024) higher rates compressed deal pipelines and valuation spreads, slowing acquisition pacing. Lower rates reopen accretive deals and allow earnout flexibility, while strict balance-sheet discipline and strong cash generation remain critical.

Currency exposure

Revenues span SEK, EUR, GBP and USD markets, creating material currency exposure across Addnode Groups operations in FY 2024. FX swings have measurably affected reported growth rates and operating margins during recent quarters. Active hedging programs reduce but do not eliminate translation and transaction risks. Pricing localization and natural cost hedges in local operations further stabilize reported results.

Labor market tightness

Scarcity of CAD/PLM/BIM consultants and developers has pushed specialist wage costs up about 8% year-on-year (2024), making utilization and project mix management key margin levers; nearshoring and partner ecosystems have reduced delivery bottlenecks and can cut labor cost per hour by ~20%. Talent retention directly underpins recurring services revenue, which accounts for roughly 60% of many engineering-software peers' turnover in 2024.

- Wage inflation: 8% (2024)

- Margin levers: utilization & project mix

- Nearshoring benefit: ~20% cost reduction

- Recurring revenue reliance: ~60%

SaaS and recurring mix

Shift from perpetual licences to subscription models increases revenue visibility for Addnode Group and shifts valuation emphasis to recurring ARR, with net retention and ACV growth becoming primary KPIs; short-term cash flow can dip during migration as upfront licence receipts fall while subscription billing ramps. Uplift derives from seat expansion, modular add‑ons and managed services, which drive higher lifetime value and margin expansion.

- Net retention: core valuation driver

- ACV growth: signals sales momentum

- Transition risk: near-term cash flow pressure

- Upsell levers: seats, modules, managed services

EU and US mega-funding boost CAD/BIM/PLM as procurement and compliance squeeze margins

Addnode faces cyclical capex sensitivity, but recurring services (~60% revenue) cushions downturns; wage inflation rose 8% in 2024 and nearshoring can cut delivery costs ~20%. Riksbank policy rate 4.00% (Dec 2024) tightened M&A; FX across SEK/EUR/GBP/USD materially affects reported growth.

| Metric | Value |

|---|---|

| Recurring rev | ~60% |

| Wage inflation (2024) | 8% |

| Nearshoring saving | ~20% |

| Riksbank rate (Dec 2024) | 4.00% |

Full Version Awaits

Addnode Group PESTLE Analysis

The Addnode Group PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors affecting the company. It highlights regulatory risks, market opportunities and tech trends shaping growth. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it to inform strategy, risk management and investment decisions.

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE analysis of Addnode Group—an incisive look at political, economic, social, technological, legal and environmental forces shaping growth and risk. Ideal for investors and strategists, it translates macro trends into actionable implications. Buy the full, editable report now for instant, board‑ready insights.

Political factors

EU digital policies

EU digitalization drives demand for CAD/BIM/PLM via programmes like Digital Europe (€7.5bn for 2021–27) and NextGenerationEU recovery funds (€806.9bn), plus Data Act/Data Spaces initiatives shaping cross-border data use. Harmonized standards and targeted grants can accelerate public procurement cycles, while shifts in industrial subsidy focus may reweight verticals. Addnode’s European footprint benefits commercially but increases compliance complexity.

Public procurement reliance

Geographic IT and BIM solutions for government and municipalities face procurement-driven timing and scope shifts, with public procurement in Sweden roughly SEK 700 billion annually and EU NextGenerationEU recovery funds near €800 billion supporting large projects. Tender dynamics, budget cycles and political leadership changes create 6–24 month sales cycles and scope volatility. Transparent rules aid access, yet persistent price pressure and lengthy procurements constrain margins despite policy-driven infrastructure investments that can trigger step-change demand.

Infrastructure and housing agendas

National commitments such as the US Bipartisan Infrastructure Law (~$1.2 trillion) and the UK 300,000 homes-per-year target drive BIM/CAD adoption across transport, housing and resilience programs. Stimulus or austerity swings—visible in €723.8bn EU Recovery and Resilience Facility allocations—shift project pipelines for engineering clients. Urban planning emphasis boosts demand for geospatial solutions, while election outcomes can reprioritize capital projects and permitting timelines.

Defense and critical infrastructure

Heightened geopolitical risk is driving higher defense and secure-infrastructure spending, with global military expenditure surpassing 2.4 trillion USD in 2024, increasing demand for PLM tailored to aerospace and defense that meet strict compliance and cybersecurity standards. Export controls and security-clearance requirements raise barriers but create high-margin niches for certified vendors, while political scrutiny of supply chains tightens vendor selection and due-diligence requirements.

- Defense spend: >2.4T USD (2024)

- PLM needs: compliance + security

- Barriers: export controls, clearances

- Vendor risk: supply-chain political scrutiny

Nordic policy stability

Nordic regulatory stability underpins long-term software and service contracts for Addnode, with EU Digital Europe funding of €1.9bn (2021–2027) and OECD R&D intensity at ~3.4% GDP in Sweden (2022) catalyzing innovation and digital twin pilots; shifts in corporate taxation or labor rules can compress margins and raise hiring costs, while strong regional cooperation drives cross-border BIM/PLM standardization.

- Stable regs: supports multi-year contracts

- Funding: EU Digital Europe €1.9bn

- R&D: Sweden ~3.4% GDP (2022)

- Risks: tax/labor shifts affect margins

- Benefit: Nordic cooperation → BIM/PLM standards

EU and US mega-funding boost CAD/BIM/PLM as procurement and compliance squeeze margins

EU and national digitalization funds (Digital Europe €7.5bn 2021–27; NextGenerationEU €806.9bn) plus US Bipartisan Infrastructure ~$1.2T drive CAD/BIM/PLM demand while raising compliance burdens. Public procurement (Sweden ~SEK 700bn) and 6–24 month tender cycles create timing and margin pressure. Geopolitical tension (global military spend >$2.4T 2024) expands certified PLM niches amid export controls and supply-chain scrutiny.

| Policy/Region | Key figure | Impact |

|---|---|---|

| Digital Europe | €7.5bn (2021–27) | Push for digital twin/BIM |

| NextGenerationEU | €806.9bn | Large infrastructure pipelines |

| Sweden procurement | ~SEK 700bn/yr | Procurement-driven demand timing |

| Global defense spend | >$2.4T (2024) | High-margin secure PLM demand |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Addnode Group across Political, Economic, Social, Technological, Environmental and Legal dimensions. Each section is data-backed with forward-looking insights to support strategic planning, risk management and investor communications.

A concise, visually segmented PESTLE summary for Addnode Group that’s editable by region or business line, easily dropped into slides or reports, and shareable for quick alignment to support external risk and market-positioning discussions.

Economic factors

Capex cycles

Addnode Group (Nasdaq Stockholm ADN B) serves cyclical engineering, construction and manufacturing customers, so capex pullbacks tend to delay software upgrades and new-seat purchases. Services and maintenance revenue historically cushions downturns, supporting recurring margins. Recovery phases drive demand for PLM/BIM modernization and cloud migrations as clients resume digital investments. Geographic and vertical diversification reduces revenue volatility for the group.

Interest rates and M&A

Addnode's buy-and-build model is sensitive to financing conditions; with Sweden's Riksbank policy rate at 4.00% (Dec 2024) higher rates compressed deal pipelines and valuation spreads, slowing acquisition pacing. Lower rates reopen accretive deals and allow earnout flexibility, while strict balance-sheet discipline and strong cash generation remain critical.

Currency exposure

Revenues span SEK, EUR, GBP and USD markets, creating material currency exposure across Addnode Groups operations in FY 2024. FX swings have measurably affected reported growth rates and operating margins during recent quarters. Active hedging programs reduce but do not eliminate translation and transaction risks. Pricing localization and natural cost hedges in local operations further stabilize reported results.

Labor market tightness

Scarcity of CAD/PLM/BIM consultants and developers has pushed specialist wage costs up about 8% year-on-year (2024), making utilization and project mix management key margin levers; nearshoring and partner ecosystems have reduced delivery bottlenecks and can cut labor cost per hour by ~20%. Talent retention directly underpins recurring services revenue, which accounts for roughly 60% of many engineering-software peers' turnover in 2024.

- Wage inflation: 8% (2024)

- Margin levers: utilization & project mix

- Nearshoring benefit: ~20% cost reduction

- Recurring revenue reliance: ~60%

SaaS and recurring mix

Shift from perpetual licences to subscription models increases revenue visibility for Addnode Group and shifts valuation emphasis to recurring ARR, with net retention and ACV growth becoming primary KPIs; short-term cash flow can dip during migration as upfront licence receipts fall while subscription billing ramps. Uplift derives from seat expansion, modular add‑ons and managed services, which drive higher lifetime value and margin expansion.

- Net retention: core valuation driver

- ACV growth: signals sales momentum

- Transition risk: near-term cash flow pressure

- Upsell levers: seats, modules, managed services

EU and US mega-funding boost CAD/BIM/PLM as procurement and compliance squeeze margins

Addnode faces cyclical capex sensitivity, but recurring services (~60% revenue) cushions downturns; wage inflation rose 8% in 2024 and nearshoring can cut delivery costs ~20%. Riksbank policy rate 4.00% (Dec 2024) tightened M&A; FX across SEK/EUR/GBP/USD materially affects reported growth.

| Metric | Value |

|---|---|

| Recurring rev | ~60% |

| Wage inflation (2024) | 8% |

| Nearshoring saving | ~20% |

| Riksbank rate (Dec 2024) | 4.00% |

Full Version Awaits

Addnode Group PESTLE Analysis

The Addnode Group PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors affecting the company. It highlights regulatory risks, market opportunities and tech trends shaping growth. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it to inform strategy, risk management and investment decisions.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE analysis of Addnode Group—an incisive look at political, economic, social, technological, legal and environmental forces shaping growth and risk. Ideal for investors and strategists, it translates macro trends into actionable implications. Buy the full, editable report now for instant, board‑ready insights.

Political factors

EU digital policies

EU digitalization drives demand for CAD/BIM/PLM via programmes like Digital Europe (€7.5bn for 2021–27) and NextGenerationEU recovery funds (€806.9bn), plus Data Act/Data Spaces initiatives shaping cross-border data use. Harmonized standards and targeted grants can accelerate public procurement cycles, while shifts in industrial subsidy focus may reweight verticals. Addnode’s European footprint benefits commercially but increases compliance complexity.

Public procurement reliance

Geographic IT and BIM solutions for government and municipalities face procurement-driven timing and scope shifts, with public procurement in Sweden roughly SEK 700 billion annually and EU NextGenerationEU recovery funds near €800 billion supporting large projects. Tender dynamics, budget cycles and political leadership changes create 6–24 month sales cycles and scope volatility. Transparent rules aid access, yet persistent price pressure and lengthy procurements constrain margins despite policy-driven infrastructure investments that can trigger step-change demand.

Infrastructure and housing agendas

National commitments such as the US Bipartisan Infrastructure Law (~$1.2 trillion) and the UK 300,000 homes-per-year target drive BIM/CAD adoption across transport, housing and resilience programs. Stimulus or austerity swings—visible in €723.8bn EU Recovery and Resilience Facility allocations—shift project pipelines for engineering clients. Urban planning emphasis boosts demand for geospatial solutions, while election outcomes can reprioritize capital projects and permitting timelines.

Defense and critical infrastructure

Heightened geopolitical risk is driving higher defense and secure-infrastructure spending, with global military expenditure surpassing 2.4 trillion USD in 2024, increasing demand for PLM tailored to aerospace and defense that meet strict compliance and cybersecurity standards. Export controls and security-clearance requirements raise barriers but create high-margin niches for certified vendors, while political scrutiny of supply chains tightens vendor selection and due-diligence requirements.

- Defense spend: >2.4T USD (2024)

- PLM needs: compliance + security

- Barriers: export controls, clearances

- Vendor risk: supply-chain political scrutiny

Nordic policy stability

Nordic regulatory stability underpins long-term software and service contracts for Addnode, with EU Digital Europe funding of €1.9bn (2021–2027) and OECD R&D intensity at ~3.4% GDP in Sweden (2022) catalyzing innovation and digital twin pilots; shifts in corporate taxation or labor rules can compress margins and raise hiring costs, while strong regional cooperation drives cross-border BIM/PLM standardization.

- Stable regs: supports multi-year contracts

- Funding: EU Digital Europe €1.9bn

- R&D: Sweden ~3.4% GDP (2022)

- Risks: tax/labor shifts affect margins

- Benefit: Nordic cooperation → BIM/PLM standards

EU and US mega-funding boost CAD/BIM/PLM as procurement and compliance squeeze margins

EU and national digitalization funds (Digital Europe €7.5bn 2021–27; NextGenerationEU €806.9bn) plus US Bipartisan Infrastructure ~$1.2T drive CAD/BIM/PLM demand while raising compliance burdens. Public procurement (Sweden ~SEK 700bn) and 6–24 month tender cycles create timing and margin pressure. Geopolitical tension (global military spend >$2.4T 2024) expands certified PLM niches amid export controls and supply-chain scrutiny.

| Policy/Region | Key figure | Impact |

|---|---|---|

| Digital Europe | €7.5bn (2021–27) | Push for digital twin/BIM |

| NextGenerationEU | €806.9bn | Large infrastructure pipelines |

| Sweden procurement | ~SEK 700bn/yr | Procurement-driven demand timing |

| Global defense spend | >$2.4T (2024) | High-margin secure PLM demand |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Addnode Group across Political, Economic, Social, Technological, Environmental and Legal dimensions. Each section is data-backed with forward-looking insights to support strategic planning, risk management and investor communications.

A concise, visually segmented PESTLE summary for Addnode Group that’s editable by region or business line, easily dropped into slides or reports, and shareable for quick alignment to support external risk and market-positioning discussions.

Economic factors

Capex cycles

Addnode Group (Nasdaq Stockholm ADN B) serves cyclical engineering, construction and manufacturing customers, so capex pullbacks tend to delay software upgrades and new-seat purchases. Services and maintenance revenue historically cushions downturns, supporting recurring margins. Recovery phases drive demand for PLM/BIM modernization and cloud migrations as clients resume digital investments. Geographic and vertical diversification reduces revenue volatility for the group.

Interest rates and M&A

Addnode's buy-and-build model is sensitive to financing conditions; with Sweden's Riksbank policy rate at 4.00% (Dec 2024) higher rates compressed deal pipelines and valuation spreads, slowing acquisition pacing. Lower rates reopen accretive deals and allow earnout flexibility, while strict balance-sheet discipline and strong cash generation remain critical.

Currency exposure

Revenues span SEK, EUR, GBP and USD markets, creating material currency exposure across Addnode Groups operations in FY 2024. FX swings have measurably affected reported growth rates and operating margins during recent quarters. Active hedging programs reduce but do not eliminate translation and transaction risks. Pricing localization and natural cost hedges in local operations further stabilize reported results.

Labor market tightness

Scarcity of CAD/PLM/BIM consultants and developers has pushed specialist wage costs up about 8% year-on-year (2024), making utilization and project mix management key margin levers; nearshoring and partner ecosystems have reduced delivery bottlenecks and can cut labor cost per hour by ~20%. Talent retention directly underpins recurring services revenue, which accounts for roughly 60% of many engineering-software peers' turnover in 2024.

- Wage inflation: 8% (2024)

- Margin levers: utilization & project mix

- Nearshoring benefit: ~20% cost reduction

- Recurring revenue reliance: ~60%

SaaS and recurring mix

Shift from perpetual licences to subscription models increases revenue visibility for Addnode Group and shifts valuation emphasis to recurring ARR, with net retention and ACV growth becoming primary KPIs; short-term cash flow can dip during migration as upfront licence receipts fall while subscription billing ramps. Uplift derives from seat expansion, modular add‑ons and managed services, which drive higher lifetime value and margin expansion.

- Net retention: core valuation driver

- ACV growth: signals sales momentum

- Transition risk: near-term cash flow pressure

- Upsell levers: seats, modules, managed services

EU and US mega-funding boost CAD/BIM/PLM as procurement and compliance squeeze margins

Addnode faces cyclical capex sensitivity, but recurring services (~60% revenue) cushions downturns; wage inflation rose 8% in 2024 and nearshoring can cut delivery costs ~20%. Riksbank policy rate 4.00% (Dec 2024) tightened M&A; FX across SEK/EUR/GBP/USD materially affects reported growth.

| Metric | Value |

|---|---|

| Recurring rev | ~60% |

| Wage inflation (2024) | 8% |

| Nearshoring saving | ~20% |

| Riksbank rate (Dec 2024) | 4.00% |

Full Version Awaits

Addnode Group PESTLE Analysis

The Addnode Group PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal and environmental factors affecting the company. It highlights regulatory risks, market opportunities and tech trends shaping growth. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it to inform strategy, risk management and investment decisions.