Adeia Porter's Five Forces Analysis

From Overview to Strategy Blueprint

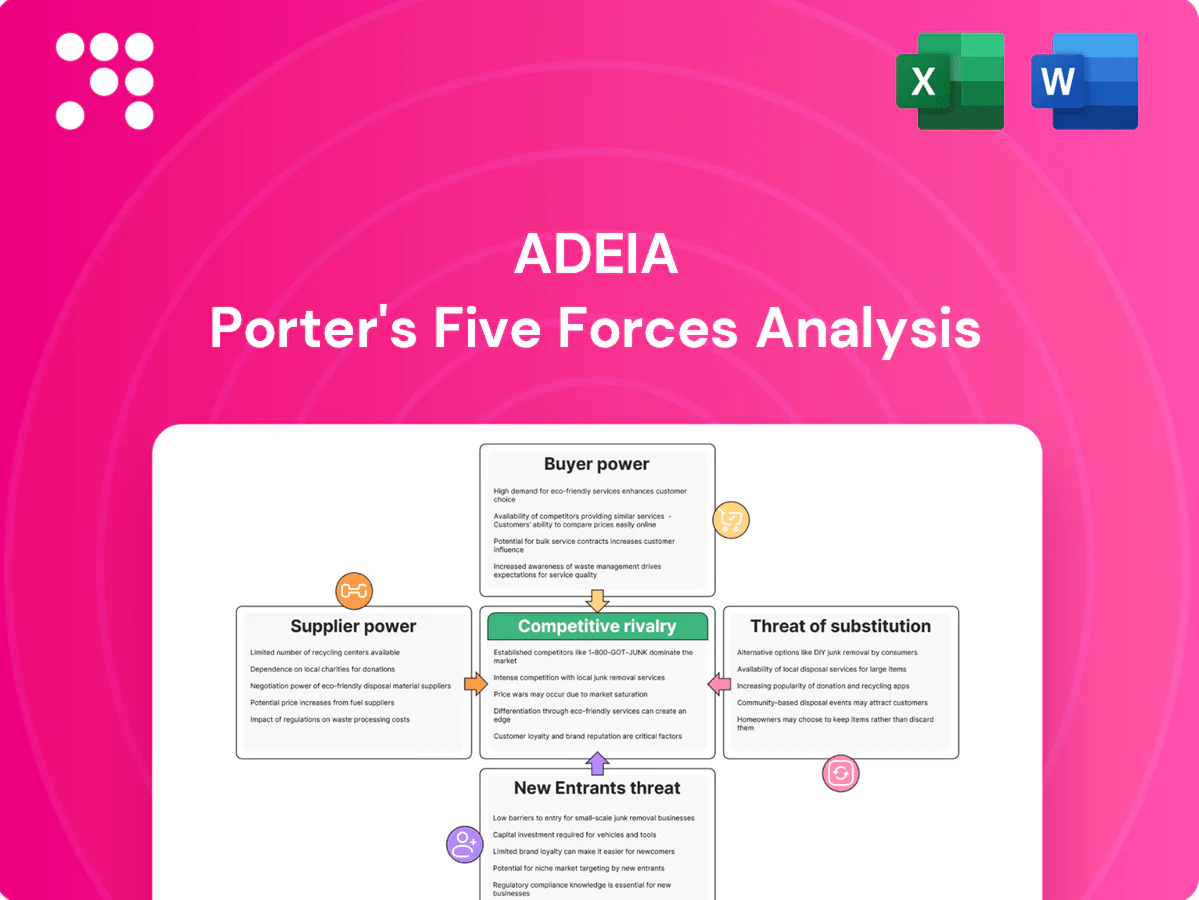

Adeia’s Porter's Five Forces assessment maps competitive intensity across supplier and buyer power, threat of new entrants, substitutes, and industry rivalry. It highlights pressures from dominant customers, potential low-cost rivals, and technology-driven substitutes shaping margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Adeia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce deep-tech R&D talent

Adeia depends on a tiny global pool of specialists in codecs, signal processing and UX algorithms, driving a 32% YoY growth in ML-related job postings in 2024 and pushing senior researcher total comp often above $300k, increasing wage costs and switching frictions. Adeia’s scale, mission focus and patenting record improve hiring leverage, while long-term incentive plans and research autonomy materially reduce supplier power.

Standards body dependencies

Participation in next-gen codec and delivery specs hinges on access, contribution influence and timing, and gatekeeping by consortia and technical committees can shift bargaining power upstream. Adeia reduces supplier power through sustained technical contributions and asserted essentiality of its claims, though acceptance and licensing risk persist. Influence differs markedly by working group and region, affecting negotiation leverage.

Legal and patent prosecution services

High-end IP law firms and specialized prosecution counsel are concentrated and costly, with premium partner rates commonly in the $800–1,200/hour range in 2024; switching counsel risks loss of continuity across complex families and jurisdictions. Adeia’s steady docket size gives volume leverage, but niche expertise still commands premium fees, while international filings add translation and local agent costs often increasing budgets by 10–20%.

Data and platform access

R&D gains from device telemetry, SDKs and partner testbeds accelerate feature development, but platform operators controlling APIs and beta programs can constrain access or impose commercial terms; in 2024 Android held ~70% and iOS ~30% of mobile OS share, concentrating gatekeeping power. Adeia mitigates risk through broad licensee relationships to secure datasets, though GDPR/CCPA privacy rules and security policies still limit data granularity.

- Telemetry + SDKs = faster R&D

- Platform gatekeepers (Android 70% / iOS 30%)

- Licensee networks secure data

- Privacy/security limit granularity

Upstream OEM/semiconductor collaboration

Prototype validation frequently requires chipset and device-vendor cooperation, and upstream partners can deprioritize third-party integrations in favor of their own roadmaps, creating potential delays. Design cycles typically span 12–24 months, giving OEMs and semiconductor vendors gating power and negotiation leverage during integration. Adeia’s cross-ecosystem footprint helps secure collaboration slots and shortens feedback loops, mitigating but not eliminating supplier leverage.

- Design cycles: 12–24 months

- Supplier leverage: gating on integration feedback

- Adeia strength: cross-ecosystem footprint secures collaboration

Supplier power spikes as ML talent tightens +32% YoY, senior pay >$300k

Adeia faces elevated supplier power from a scarce pool of codec/ML specialists (32% YoY rise in ML job postings in 2024; senior comp >$300k) and platform gatekeepers (Android ~70%/iOS ~30% in 2024). IP counsel and chipset partners add premium fees ($800–1,200/hr) and 12–24m integration gating. Adeia’s scale, patents and partner spread partially mitigate but do not eliminate supplier leverage.

| Factor | 2024 Metric |

|---|---|

| ML hiring growth | +32% YoY |

| Senior comp | >$300k |

| Mobile OS share | Android 70% / iOS 30% |

| IP counsel rates | $800–1,200/hr |

| Design cycle | 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for Adeia uncovering competitive drivers, buyer/supplier power, substitutes, entry barriers and disruptive threats, with strategic commentary and an editable Word deliverable for investor and internal use.

Adeia’s Porter's Five Forces delivers a clean one-sheet with customizable pressure levels and an instant spider chart—no macros required—so teams can quickly assess competitive threats, swap in current data, and drop the summary straight into pitch decks or dashboards.

Customers Bargaining Power

Concentrated mega-licensees

Buyers for Adeia include major CE OEMs, operators, streamers and chip vendors whose scale concentrates purchasing power—top CE OEMs accounted for roughly 60% of global TV shipments in 2023 (Omdia), boosting leverage on licensing rates and terms. Adeia mitigates this through diversified end-markets and multi-device coverage across TVs, set‑tops and SoCs. Nonetheless, a small number of renewals or pricing concessions can materially affect revenue timing and visibility.

Essential patents lower switching

Adeia (NASDAQ: ADEA), spun off in 2023, holds a portfolio of thousands of patents including standard-essential claims, which diminishes buyer switching where implementations are widespread. This lowers outright avoidance but does not eliminate pricing pressure; Adeia enforces value through litigation and licensing. Buyers, however, can delay deals or contest essentiality to extract concessions.

Litigation and cross-licensing

Large corporate buyers often leverage counter-litigation and defenses to push down royalty rates, using threat of invalidity or noninfringement suits as bargaining chips. Cross-licensing deals can offset upfront fees when buyers own overlapping patents, turning potential payables into reciprocal IP value. Adeia’s litigation credibility and prior case outcomes materially affect settlement leverage, where agreements commonly mix past-use lump sums with future-running royalties.

Volume and price sensitivity

Per-unit royalties on high-volume devices make total cost salient to buyers; with ~1.18 billion global smartphone shipments in 2024 buyers press for caps, tiers and regional differentials to limit cumulative royalty exposure. Adeia leverages portfolio breadth to argue value-based pricing while audits and reporting requirements add negotiation friction and enforcement costs.

- Royalty visibility

- Caps/tiers demanded

- Portfolio justification

- Audit friction

Regulatory and FRAND scrutiny

Competition authorities actively monitor SEP licensing and injunctions, with FRAND scrutiny shaping rate-setting and limiting exclusionary remedies; buyers increasingly invoke FRAND norms to constrain terms. Adeia must document fairness and non-discrimination in licensing and record negotiation processes to reduce disputes. Jurisdictional differences across the US, EU and Asia materially shape customer leverage and enforcement risk.

- Regulatory oversight: cross-jurisdictional variance

- Buyer leverage: FRAND defenses

- Adeia action: document fairness + non-discrimination

OEM concentration, billions of phones and FRAND limits squeeze patent royalty leverage

Buyers (CE OEMs, operators, chip vendors) concentrate purchasing power—top CE OEMs ≈60% of global TV shipments in 2023 (Omdia)—pressing for caps/tiers and concessions. Adeia (spun off 2023) holds thousands of patents including SEPs, reducing switching but not eliminating price pressure; 1.18B smartphone shipments in 2024 make per-unit royalties salient. FRAND scrutiny (US/EU/Asia) limits exclusionary leverage.

| Metric | Value | Note |

|---|---|---|

| Top CE OEM share | ~60% | TV shipments 2023 (Omdia) |

| Smartphone market | 1.18B | Shipments 2024 |

| Adeia status | Spun off 2023 | Portfolio: thousands of patents |

Preview Before You Purchase

Adeia Porter's Five Forces Analysis

This preview shows the exact Adeia Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The document is the full, professionally formatted file, ready to download and use immediately upon payment. What you see is what you get.

From Overview to Strategy Blueprint

Adeia’s Porter's Five Forces assessment maps competitive intensity across supplier and buyer power, threat of new entrants, substitutes, and industry rivalry. It highlights pressures from dominant customers, potential low-cost rivals, and technology-driven substitutes shaping margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Adeia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce deep-tech R&D talent

Adeia depends on a tiny global pool of specialists in codecs, signal processing and UX algorithms, driving a 32% YoY growth in ML-related job postings in 2024 and pushing senior researcher total comp often above $300k, increasing wage costs and switching frictions. Adeia’s scale, mission focus and patenting record improve hiring leverage, while long-term incentive plans and research autonomy materially reduce supplier power.

Standards body dependencies

Participation in next-gen codec and delivery specs hinges on access, contribution influence and timing, and gatekeeping by consortia and technical committees can shift bargaining power upstream. Adeia reduces supplier power through sustained technical contributions and asserted essentiality of its claims, though acceptance and licensing risk persist. Influence differs markedly by working group and region, affecting negotiation leverage.

Legal and patent prosecution services

High-end IP law firms and specialized prosecution counsel are concentrated and costly, with premium partner rates commonly in the $800–1,200/hour range in 2024; switching counsel risks loss of continuity across complex families and jurisdictions. Adeia’s steady docket size gives volume leverage, but niche expertise still commands premium fees, while international filings add translation and local agent costs often increasing budgets by 10–20%.

Data and platform access

R&D gains from device telemetry, SDKs and partner testbeds accelerate feature development, but platform operators controlling APIs and beta programs can constrain access or impose commercial terms; in 2024 Android held ~70% and iOS ~30% of mobile OS share, concentrating gatekeeping power. Adeia mitigates risk through broad licensee relationships to secure datasets, though GDPR/CCPA privacy rules and security policies still limit data granularity.

- Telemetry + SDKs = faster R&D

- Platform gatekeepers (Android 70% / iOS 30%)

- Licensee networks secure data

- Privacy/security limit granularity

Upstream OEM/semiconductor collaboration

Prototype validation frequently requires chipset and device-vendor cooperation, and upstream partners can deprioritize third-party integrations in favor of their own roadmaps, creating potential delays. Design cycles typically span 12–24 months, giving OEMs and semiconductor vendors gating power and negotiation leverage during integration. Adeia’s cross-ecosystem footprint helps secure collaboration slots and shortens feedback loops, mitigating but not eliminating supplier leverage.

- Design cycles: 12–24 months

- Supplier leverage: gating on integration feedback

- Adeia strength: cross-ecosystem footprint secures collaboration

Supplier power spikes as ML talent tightens +32% YoY, senior pay >$300k

Adeia faces elevated supplier power from a scarce pool of codec/ML specialists (32% YoY rise in ML job postings in 2024; senior comp >$300k) and platform gatekeepers (Android ~70%/iOS ~30% in 2024). IP counsel and chipset partners add premium fees ($800–1,200/hr) and 12–24m integration gating. Adeia’s scale, patents and partner spread partially mitigate but do not eliminate supplier leverage.

| Factor | 2024 Metric |

|---|---|

| ML hiring growth | +32% YoY |

| Senior comp | >$300k |

| Mobile OS share | Android 70% / iOS 30% |

| IP counsel rates | $800–1,200/hr |

| Design cycle | 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for Adeia uncovering competitive drivers, buyer/supplier power, substitutes, entry barriers and disruptive threats, with strategic commentary and an editable Word deliverable for investor and internal use.

Adeia’s Porter's Five Forces delivers a clean one-sheet with customizable pressure levels and an instant spider chart—no macros required—so teams can quickly assess competitive threats, swap in current data, and drop the summary straight into pitch decks or dashboards.

Customers Bargaining Power

Concentrated mega-licensees

Buyers for Adeia include major CE OEMs, operators, streamers and chip vendors whose scale concentrates purchasing power—top CE OEMs accounted for roughly 60% of global TV shipments in 2023 (Omdia), boosting leverage on licensing rates and terms. Adeia mitigates this through diversified end-markets and multi-device coverage across TVs, set‑tops and SoCs. Nonetheless, a small number of renewals or pricing concessions can materially affect revenue timing and visibility.

Essential patents lower switching

Adeia (NASDAQ: ADEA), spun off in 2023, holds a portfolio of thousands of patents including standard-essential claims, which diminishes buyer switching where implementations are widespread. This lowers outright avoidance but does not eliminate pricing pressure; Adeia enforces value through litigation and licensing. Buyers, however, can delay deals or contest essentiality to extract concessions.

Litigation and cross-licensing

Large corporate buyers often leverage counter-litigation and defenses to push down royalty rates, using threat of invalidity or noninfringement suits as bargaining chips. Cross-licensing deals can offset upfront fees when buyers own overlapping patents, turning potential payables into reciprocal IP value. Adeia’s litigation credibility and prior case outcomes materially affect settlement leverage, where agreements commonly mix past-use lump sums with future-running royalties.

Volume and price sensitivity

Per-unit royalties on high-volume devices make total cost salient to buyers; with ~1.18 billion global smartphone shipments in 2024 buyers press for caps, tiers and regional differentials to limit cumulative royalty exposure. Adeia leverages portfolio breadth to argue value-based pricing while audits and reporting requirements add negotiation friction and enforcement costs.

- Royalty visibility

- Caps/tiers demanded

- Portfolio justification

- Audit friction

Regulatory and FRAND scrutiny

Competition authorities actively monitor SEP licensing and injunctions, with FRAND scrutiny shaping rate-setting and limiting exclusionary remedies; buyers increasingly invoke FRAND norms to constrain terms. Adeia must document fairness and non-discrimination in licensing and record negotiation processes to reduce disputes. Jurisdictional differences across the US, EU and Asia materially shape customer leverage and enforcement risk.

- Regulatory oversight: cross-jurisdictional variance

- Buyer leverage: FRAND defenses

- Adeia action: document fairness + non-discrimination

OEM concentration, billions of phones and FRAND limits squeeze patent royalty leverage

Buyers (CE OEMs, operators, chip vendors) concentrate purchasing power—top CE OEMs ≈60% of global TV shipments in 2023 (Omdia)—pressing for caps/tiers and concessions. Adeia (spun off 2023) holds thousands of patents including SEPs, reducing switching but not eliminating price pressure; 1.18B smartphone shipments in 2024 make per-unit royalties salient. FRAND scrutiny (US/EU/Asia) limits exclusionary leverage.

| Metric | Value | Note |

|---|---|---|

| Top CE OEM share | ~60% | TV shipments 2023 (Omdia) |

| Smartphone market | 1.18B | Shipments 2024 |

| Adeia status | Spun off 2023 | Portfolio: thousands of patents |

Preview Before You Purchase

Adeia Porter's Five Forces Analysis

This preview shows the exact Adeia Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The document is the full, professionally formatted file, ready to download and use immediately upon payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Adeia’s Porter's Five Forces assessment maps competitive intensity across supplier and buyer power, threat of new entrants, substitutes, and industry rivalry. It highlights pressures from dominant customers, potential low-cost rivals, and technology-driven substitutes shaping margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Adeia’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce deep-tech R&D talent

Adeia depends on a tiny global pool of specialists in codecs, signal processing and UX algorithms, driving a 32% YoY growth in ML-related job postings in 2024 and pushing senior researcher total comp often above $300k, increasing wage costs and switching frictions. Adeia’s scale, mission focus and patenting record improve hiring leverage, while long-term incentive plans and research autonomy materially reduce supplier power.

Standards body dependencies

Participation in next-gen codec and delivery specs hinges on access, contribution influence and timing, and gatekeeping by consortia and technical committees can shift bargaining power upstream. Adeia reduces supplier power through sustained technical contributions and asserted essentiality of its claims, though acceptance and licensing risk persist. Influence differs markedly by working group and region, affecting negotiation leverage.

Legal and patent prosecution services

High-end IP law firms and specialized prosecution counsel are concentrated and costly, with premium partner rates commonly in the $800–1,200/hour range in 2024; switching counsel risks loss of continuity across complex families and jurisdictions. Adeia’s steady docket size gives volume leverage, but niche expertise still commands premium fees, while international filings add translation and local agent costs often increasing budgets by 10–20%.

Data and platform access

R&D gains from device telemetry, SDKs and partner testbeds accelerate feature development, but platform operators controlling APIs and beta programs can constrain access or impose commercial terms; in 2024 Android held ~70% and iOS ~30% of mobile OS share, concentrating gatekeeping power. Adeia mitigates risk through broad licensee relationships to secure datasets, though GDPR/CCPA privacy rules and security policies still limit data granularity.

- Telemetry + SDKs = faster R&D

- Platform gatekeepers (Android 70% / iOS 30%)

- Licensee networks secure data

- Privacy/security limit granularity

Upstream OEM/semiconductor collaboration

Prototype validation frequently requires chipset and device-vendor cooperation, and upstream partners can deprioritize third-party integrations in favor of their own roadmaps, creating potential delays. Design cycles typically span 12–24 months, giving OEMs and semiconductor vendors gating power and negotiation leverage during integration. Adeia’s cross-ecosystem footprint helps secure collaboration slots and shortens feedback loops, mitigating but not eliminating supplier leverage.

- Design cycles: 12–24 months

- Supplier leverage: gating on integration feedback

- Adeia strength: cross-ecosystem footprint secures collaboration

Supplier power spikes as ML talent tightens +32% YoY, senior pay >$300k

Adeia faces elevated supplier power from a scarce pool of codec/ML specialists (32% YoY rise in ML job postings in 2024; senior comp >$300k) and platform gatekeepers (Android ~70%/iOS ~30% in 2024). IP counsel and chipset partners add premium fees ($800–1,200/hr) and 12–24m integration gating. Adeia’s scale, patents and partner spread partially mitigate but do not eliminate supplier leverage.

| Factor | 2024 Metric |

|---|---|

| ML hiring growth | +32% YoY |

| Senior comp | >$300k |

| Mobile OS share | Android 70% / iOS 30% |

| IP counsel rates | $800–1,200/hr |

| Design cycle | 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis for Adeia uncovering competitive drivers, buyer/supplier power, substitutes, entry barriers and disruptive threats, with strategic commentary and an editable Word deliverable for investor and internal use.

Adeia’s Porter's Five Forces delivers a clean one-sheet with customizable pressure levels and an instant spider chart—no macros required—so teams can quickly assess competitive threats, swap in current data, and drop the summary straight into pitch decks or dashboards.

Customers Bargaining Power

Concentrated mega-licensees

Buyers for Adeia include major CE OEMs, operators, streamers and chip vendors whose scale concentrates purchasing power—top CE OEMs accounted for roughly 60% of global TV shipments in 2023 (Omdia), boosting leverage on licensing rates and terms. Adeia mitigates this through diversified end-markets and multi-device coverage across TVs, set‑tops and SoCs. Nonetheless, a small number of renewals or pricing concessions can materially affect revenue timing and visibility.

Essential patents lower switching

Adeia (NASDAQ: ADEA), spun off in 2023, holds a portfolio of thousands of patents including standard-essential claims, which diminishes buyer switching where implementations are widespread. This lowers outright avoidance but does not eliminate pricing pressure; Adeia enforces value through litigation and licensing. Buyers, however, can delay deals or contest essentiality to extract concessions.

Litigation and cross-licensing

Large corporate buyers often leverage counter-litigation and defenses to push down royalty rates, using threat of invalidity or noninfringement suits as bargaining chips. Cross-licensing deals can offset upfront fees when buyers own overlapping patents, turning potential payables into reciprocal IP value. Adeia’s litigation credibility and prior case outcomes materially affect settlement leverage, where agreements commonly mix past-use lump sums with future-running royalties.

Volume and price sensitivity

Per-unit royalties on high-volume devices make total cost salient to buyers; with ~1.18 billion global smartphone shipments in 2024 buyers press for caps, tiers and regional differentials to limit cumulative royalty exposure. Adeia leverages portfolio breadth to argue value-based pricing while audits and reporting requirements add negotiation friction and enforcement costs.

- Royalty visibility

- Caps/tiers demanded

- Portfolio justification

- Audit friction

Regulatory and FRAND scrutiny

Competition authorities actively monitor SEP licensing and injunctions, with FRAND scrutiny shaping rate-setting and limiting exclusionary remedies; buyers increasingly invoke FRAND norms to constrain terms. Adeia must document fairness and non-discrimination in licensing and record negotiation processes to reduce disputes. Jurisdictional differences across the US, EU and Asia materially shape customer leverage and enforcement risk.

- Regulatory oversight: cross-jurisdictional variance

- Buyer leverage: FRAND defenses

- Adeia action: document fairness + non-discrimination

OEM concentration, billions of phones and FRAND limits squeeze patent royalty leverage

Buyers (CE OEMs, operators, chip vendors) concentrate purchasing power—top CE OEMs ≈60% of global TV shipments in 2023 (Omdia)—pressing for caps/tiers and concessions. Adeia (spun off 2023) holds thousands of patents including SEPs, reducing switching but not eliminating price pressure; 1.18B smartphone shipments in 2024 make per-unit royalties salient. FRAND scrutiny (US/EU/Asia) limits exclusionary leverage.

| Metric | Value | Note |

|---|---|---|

| Top CE OEM share | ~60% | TV shipments 2023 (Omdia) |

| Smartphone market | 1.18B | Shipments 2024 |

| Adeia status | Spun off 2023 | Portfolio: thousands of patents |

Preview Before You Purchase

Adeia Porter's Five Forces Analysis

This preview shows the exact Adeia Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The document is the full, professionally formatted file, ready to download and use immediately upon payment. What you see is what you get.