Abu Dhabi Islamic Bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

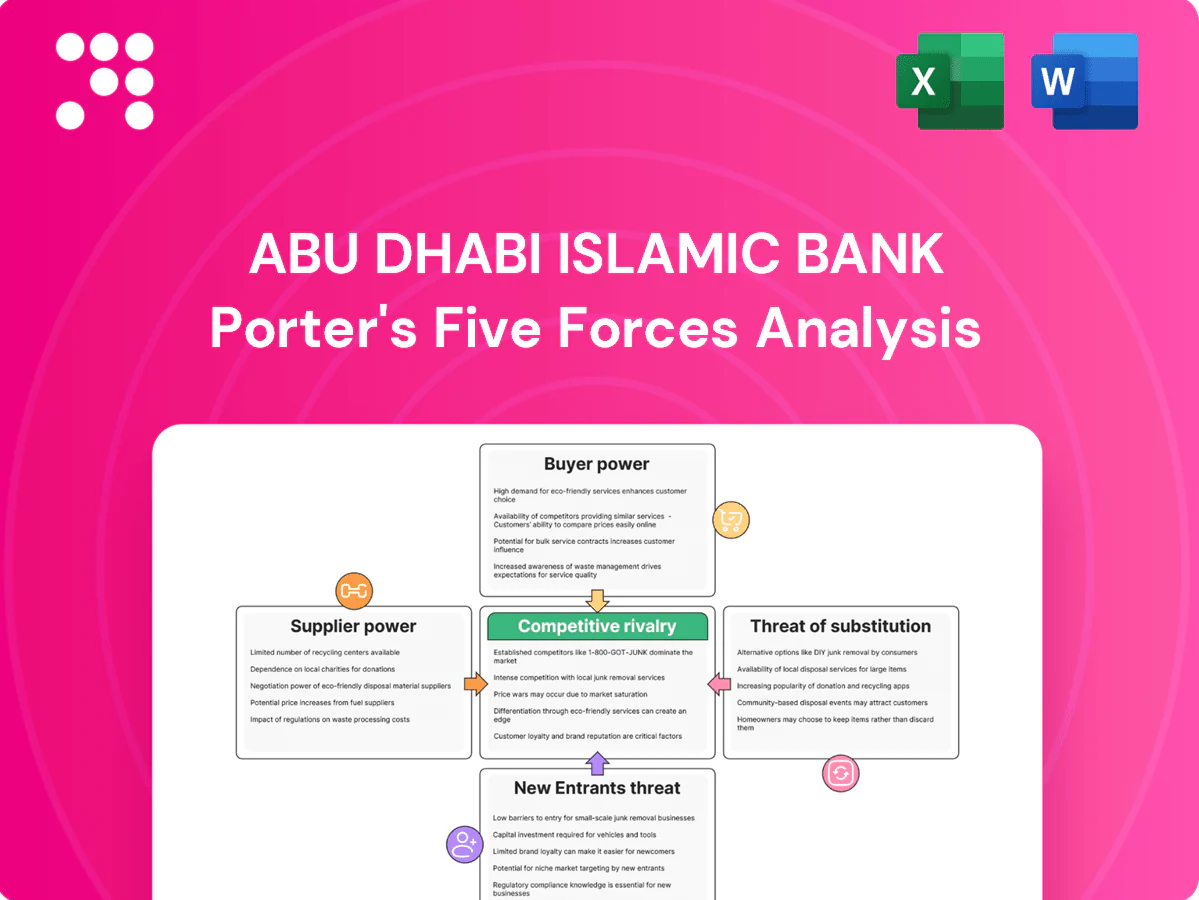

Abu Dhabi Islamic Bank faces moderate buyer power, regulatory-driven barriers limiting new entrants, strong rivalry among UAE banks, low substitute threat for Shari'ah-compliant services, and concentrated supplier influence on funding costs. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to reveal force-by-force ratings, visuals, and strategic implications for informed decisions.

Suppliers Bargaining Power

Concentration of funding sources

In 2024 ADIB continues to fund primarily through retail deposits, corporate deposits and wholesale sukuk; large corporate and government-related depositors can reprice or reallocate balances quickly, pushing up funding costs. A diversified mix of deposits and sukuk tempers concentration risk, but abrupt withdrawals from a few large accounts can tighten liquidity. Islamic constraints restrict some conventional hedging and funding tools, slightly increasing sensitivity to shifts.

Sharia scholars and governance

Accredited Sharia scholars are a scarce, reputation-critical resource in Islamic finance, with global Islamic finance assets near $3.7 trillion in 2024 increasing scrutiny on approvals. Their rulings shape product design and time-to-market, giving them leverage over fees and availability. Strong internal Sharia governance at ADIB reduces dependency risk but cannot fully substitute external scholarly credibility. Turnover in scholars can delay launches and create compliance bottlenecks.

Core banking and fintech vendors

Core systems, cloud, cyber, and payments providers are few and sticky, creating high switching costs for ADIB as vendor lock-in and integration complexity grant suppliers pricing and contractual leverage. Multi-vendor strategies and adoption of open APIs can reduce single-supplier concentration and interoperability risk. Regulatory requirements on data residency and localization further constrain ADIB’s supplier optionality and contract flexibility.

Wholesale capital market investors

Wholesale capital market investors—sukuk buyers and interbank counterparties—set pricing and tenor access for ADIB; market risk cycles and the Fed funds rate (about 5.25–5.50% in 2024) transmit quickly into ADIB’s funding costs. Strong credit ratings and investor relations soften but cannot fully offset broad risk-off episodes. Sharia structuring complexity can narrow investor pools in stressed markets.

- Sukuk and interbank influence on pricing/tenor

- Fed funds ~5.25–5.50% in 2024 raises funding pass-through

- Credit/IR mitigate but not eliminate risk-off

- Sharia structuring narrows investor base in stress

Skilled Islamic finance talent

Experienced Islamic product, risk and compliance professionals are scarce across the GCC, constraining ADIB’s internal capabilities and increasing reliance on external consultants; global Islamic finance assets exceeded 3 trillion USD in 2023, raising demand for specialized talent into 2024.

- Limited regional supply increases hiring and retention costs

- GCC competition drives premium compensation

- Remote/digital pipelines ease but don’t remove scarcity

- Talent gaps slow product innovation

Supplier power moderate-high: sukuk, depositors repricing; Fed 5.25–5.50%

Supplier power for ADIB is moderate-high: large depositors and sukuk investors can reprice liquidity, Fed funds ~5.25–5.50% (2024) lifts funding costs; scarce Sharia scholars and Islamic specialists constrain product rollout; core IT/vendors create high switching costs.

| Supplier | Concentration | 2024 metric |

|---|---|---|

| Sukuk/interbank | Medium | Fed funds 5.25–5.50% |

| Sharia scholars | High | Global Islamic assets ~$3.7T |

| IT vendors | High | Vendor lock-in |

What is included in the product

Concise Porter's Five Forces assessment of Abu Dhabi Islamic Bank, identifying competitive rivalry, buyer and supplier power, entry barriers, and substitute threats with strategic implications for market positioning.

Concise one-sheet Porter's Five Forces for Abu Dhabi Islamic Bank—instantly spot competitive pressures and regulatory risks for faster decisions. Customize force levels, swap your data, and export a radar chart-ready layout for pitch decks or boardroom slides.

Customers Bargaining Power

Large corporates and GREs

Large corporates and GREs wield strong bargaining power at Abu Dhabi Islamic Bank because their volume and multi-product relationships create concentrated revenue pools. In 2024 they routinely negotiate tighter pricing, stricter covenants and bespoke capital and treasury structures. Their ability to move relationships across UAE banks forces ADIB to offer competitive concessions. Losing such clients materially reduces fee income and cross-sell potential.

Retail customers’ switching ease

Digital onboarding and one-click account switching have lowered friction for retail clients, with UAE mobile banking adoption reaching about 80% in 2024, raising churn risk. Transparent profit rates and fees heighten price sensitivity across comparable Shariah products. Loyalty programs and personalized journeys reduce churn but are easily replicated. Service lapses rapidly trigger migration to rival apps, reflected in higher app-switch rates in 2024.

Sharia compliance expectations

Clients demand strong Sharia assurance, narrowing acceptable alternatives and increasing scrutiny on product design which concentrates buyer power around institutions with credible Sharia governance. Any perceived deviation can trigger reputational risk, client renegotiations and loss of trust, amplifying the stakes for ADIB. Clear disclosure and reputable Sharia boards help rebalance expectations and reduce bilateral friction.

SME financing needs

SMEs are highly rate-sensitive and routinely compare Islamic versus conventional pricing and collateral; globally SMEs represent about 90% of firms and ~50% of employment (World Bank/IFC), increasing their negotiating importance. Government-backed guarantee schemes partially standardize pricing, aiding buyer leverage, while faster credit decisions and digital documentation shift choices beyond price; weak SME data still limits bargaining power for some segments.

- SME price sensitivity

- Islamic vs conventional comparison

- Govt guarantees standardize pricing

- Speed and digital docs drive choice

- Poor SME data reduces leverage

Wealth and private clients

- multi‑banking: ~70% use custody/advisory mandates

- exclusive access: sukuk/private placements drive negotiation

- fee resilience: tied to relationship depth and bespoke services

Scale-driven pricing pressure; retail churn with 80% mobile adoption

Large corporates/GREs exert strong leverage through volume and multi‑product ties, forcing pricing and covenant concessions. Retail churn rose with UAE mobile banking adoption ~80% in 2024, increasing price sensitivity. SMEs remain highly price‑sensitive; SMEs are ~90% of firms and ~50% of employment (World Bank/IFC). Affluent clients multi‑bank (~70%) to secure exclusives and fee relief.

| Segment | Driver | 2024 metric |

|---|---|---|

| Corporates/GREs | Volume, bespoke terms | High revenue concentration |

| Retail | Digital churn | 80% mobile adoption |

| SMEs | Price sensitivity | 90% firms; 50% employment |

| Affluent | Multi‑banking, exclusives | ~70% advisory/custody |

Same Document Delivered

Abu Dhabi Islamic Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Abu Dhabi Islamic Bank you'll receive immediately after purchase—fully formatted, sourced and ready for use. It assesses competitive rivalry, supplier and buyer power, and threats of entry and substitutes, with clear strategic implications for ADIB. No placeholders or samples; the document available after payment is precisely this file.

A Must-Have Tool for Decision-Makers

Abu Dhabi Islamic Bank faces moderate buyer power, regulatory-driven barriers limiting new entrants, strong rivalry among UAE banks, low substitute threat for Shari'ah-compliant services, and concentrated supplier influence on funding costs. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to reveal force-by-force ratings, visuals, and strategic implications for informed decisions.

Suppliers Bargaining Power

Concentration of funding sources

In 2024 ADIB continues to fund primarily through retail deposits, corporate deposits and wholesale sukuk; large corporate and government-related depositors can reprice or reallocate balances quickly, pushing up funding costs. A diversified mix of deposits and sukuk tempers concentration risk, but abrupt withdrawals from a few large accounts can tighten liquidity. Islamic constraints restrict some conventional hedging and funding tools, slightly increasing sensitivity to shifts.

Sharia scholars and governance

Accredited Sharia scholars are a scarce, reputation-critical resource in Islamic finance, with global Islamic finance assets near $3.7 trillion in 2024 increasing scrutiny on approvals. Their rulings shape product design and time-to-market, giving them leverage over fees and availability. Strong internal Sharia governance at ADIB reduces dependency risk but cannot fully substitute external scholarly credibility. Turnover in scholars can delay launches and create compliance bottlenecks.

Core banking and fintech vendors

Core systems, cloud, cyber, and payments providers are few and sticky, creating high switching costs for ADIB as vendor lock-in and integration complexity grant suppliers pricing and contractual leverage. Multi-vendor strategies and adoption of open APIs can reduce single-supplier concentration and interoperability risk. Regulatory requirements on data residency and localization further constrain ADIB’s supplier optionality and contract flexibility.

Wholesale capital market investors

Wholesale capital market investors—sukuk buyers and interbank counterparties—set pricing and tenor access for ADIB; market risk cycles and the Fed funds rate (about 5.25–5.50% in 2024) transmit quickly into ADIB’s funding costs. Strong credit ratings and investor relations soften but cannot fully offset broad risk-off episodes. Sharia structuring complexity can narrow investor pools in stressed markets.

- Sukuk and interbank influence on pricing/tenor

- Fed funds ~5.25–5.50% in 2024 raises funding pass-through

- Credit/IR mitigate but not eliminate risk-off

- Sharia structuring narrows investor base in stress

Skilled Islamic finance talent

Experienced Islamic product, risk and compliance professionals are scarce across the GCC, constraining ADIB’s internal capabilities and increasing reliance on external consultants; global Islamic finance assets exceeded 3 trillion USD in 2023, raising demand for specialized talent into 2024.

- Limited regional supply increases hiring and retention costs

- GCC competition drives premium compensation

- Remote/digital pipelines ease but don’t remove scarcity

- Talent gaps slow product innovation

Supplier power moderate-high: sukuk, depositors repricing; Fed 5.25–5.50%

Supplier power for ADIB is moderate-high: large depositors and sukuk investors can reprice liquidity, Fed funds ~5.25–5.50% (2024) lifts funding costs; scarce Sharia scholars and Islamic specialists constrain product rollout; core IT/vendors create high switching costs.

| Supplier | Concentration | 2024 metric |

|---|---|---|

| Sukuk/interbank | Medium | Fed funds 5.25–5.50% |

| Sharia scholars | High | Global Islamic assets ~$3.7T |

| IT vendors | High | Vendor lock-in |

What is included in the product

Concise Porter's Five Forces assessment of Abu Dhabi Islamic Bank, identifying competitive rivalry, buyer and supplier power, entry barriers, and substitute threats with strategic implications for market positioning.

Concise one-sheet Porter's Five Forces for Abu Dhabi Islamic Bank—instantly spot competitive pressures and regulatory risks for faster decisions. Customize force levels, swap your data, and export a radar chart-ready layout for pitch decks or boardroom slides.

Customers Bargaining Power

Large corporates and GREs

Large corporates and GREs wield strong bargaining power at Abu Dhabi Islamic Bank because their volume and multi-product relationships create concentrated revenue pools. In 2024 they routinely negotiate tighter pricing, stricter covenants and bespoke capital and treasury structures. Their ability to move relationships across UAE banks forces ADIB to offer competitive concessions. Losing such clients materially reduces fee income and cross-sell potential.

Retail customers’ switching ease

Digital onboarding and one-click account switching have lowered friction for retail clients, with UAE mobile banking adoption reaching about 80% in 2024, raising churn risk. Transparent profit rates and fees heighten price sensitivity across comparable Shariah products. Loyalty programs and personalized journeys reduce churn but are easily replicated. Service lapses rapidly trigger migration to rival apps, reflected in higher app-switch rates in 2024.

Sharia compliance expectations

Clients demand strong Sharia assurance, narrowing acceptable alternatives and increasing scrutiny on product design which concentrates buyer power around institutions with credible Sharia governance. Any perceived deviation can trigger reputational risk, client renegotiations and loss of trust, amplifying the stakes for ADIB. Clear disclosure and reputable Sharia boards help rebalance expectations and reduce bilateral friction.

SME financing needs

SMEs are highly rate-sensitive and routinely compare Islamic versus conventional pricing and collateral; globally SMEs represent about 90% of firms and ~50% of employment (World Bank/IFC), increasing their negotiating importance. Government-backed guarantee schemes partially standardize pricing, aiding buyer leverage, while faster credit decisions and digital documentation shift choices beyond price; weak SME data still limits bargaining power for some segments.

- SME price sensitivity

- Islamic vs conventional comparison

- Govt guarantees standardize pricing

- Speed and digital docs drive choice

- Poor SME data reduces leverage

Wealth and private clients

- multi‑banking: ~70% use custody/advisory mandates

- exclusive access: sukuk/private placements drive negotiation

- fee resilience: tied to relationship depth and bespoke services

Scale-driven pricing pressure; retail churn with 80% mobile adoption

Large corporates/GREs exert strong leverage through volume and multi‑product ties, forcing pricing and covenant concessions. Retail churn rose with UAE mobile banking adoption ~80% in 2024, increasing price sensitivity. SMEs remain highly price‑sensitive; SMEs are ~90% of firms and ~50% of employment (World Bank/IFC). Affluent clients multi‑bank (~70%) to secure exclusives and fee relief.

| Segment | Driver | 2024 metric |

|---|---|---|

| Corporates/GREs | Volume, bespoke terms | High revenue concentration |

| Retail | Digital churn | 80% mobile adoption |

| SMEs | Price sensitivity | 90% firms; 50% employment |

| Affluent | Multi‑banking, exclusives | ~70% advisory/custody |

Same Document Delivered

Abu Dhabi Islamic Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Abu Dhabi Islamic Bank you'll receive immediately after purchase—fully formatted, sourced and ready for use. It assesses competitive rivalry, supplier and buyer power, and threats of entry and substitutes, with clear strategic implications for ADIB. No placeholders or samples; the document available after payment is precisely this file.

Description

A Must-Have Tool for Decision-Makers

Abu Dhabi Islamic Bank faces moderate buyer power, regulatory-driven barriers limiting new entrants, strong rivalry among UAE banks, low substitute threat for Shari'ah-compliant services, and concentrated supplier influence on funding costs. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to reveal force-by-force ratings, visuals, and strategic implications for informed decisions.

Suppliers Bargaining Power

Concentration of funding sources

In 2024 ADIB continues to fund primarily through retail deposits, corporate deposits and wholesale sukuk; large corporate and government-related depositors can reprice or reallocate balances quickly, pushing up funding costs. A diversified mix of deposits and sukuk tempers concentration risk, but abrupt withdrawals from a few large accounts can tighten liquidity. Islamic constraints restrict some conventional hedging and funding tools, slightly increasing sensitivity to shifts.

Sharia scholars and governance

Accredited Sharia scholars are a scarce, reputation-critical resource in Islamic finance, with global Islamic finance assets near $3.7 trillion in 2024 increasing scrutiny on approvals. Their rulings shape product design and time-to-market, giving them leverage over fees and availability. Strong internal Sharia governance at ADIB reduces dependency risk but cannot fully substitute external scholarly credibility. Turnover in scholars can delay launches and create compliance bottlenecks.

Core banking and fintech vendors

Core systems, cloud, cyber, and payments providers are few and sticky, creating high switching costs for ADIB as vendor lock-in and integration complexity grant suppliers pricing and contractual leverage. Multi-vendor strategies and adoption of open APIs can reduce single-supplier concentration and interoperability risk. Regulatory requirements on data residency and localization further constrain ADIB’s supplier optionality and contract flexibility.

Wholesale capital market investors

Wholesale capital market investors—sukuk buyers and interbank counterparties—set pricing and tenor access for ADIB; market risk cycles and the Fed funds rate (about 5.25–5.50% in 2024) transmit quickly into ADIB’s funding costs. Strong credit ratings and investor relations soften but cannot fully offset broad risk-off episodes. Sharia structuring complexity can narrow investor pools in stressed markets.

- Sukuk and interbank influence on pricing/tenor

- Fed funds ~5.25–5.50% in 2024 raises funding pass-through

- Credit/IR mitigate but not eliminate risk-off

- Sharia structuring narrows investor base in stress

Skilled Islamic finance talent

Experienced Islamic product, risk and compliance professionals are scarce across the GCC, constraining ADIB’s internal capabilities and increasing reliance on external consultants; global Islamic finance assets exceeded 3 trillion USD in 2023, raising demand for specialized talent into 2024.

- Limited regional supply increases hiring and retention costs

- GCC competition drives premium compensation

- Remote/digital pipelines ease but don’t remove scarcity

- Talent gaps slow product innovation

Supplier power moderate-high: sukuk, depositors repricing; Fed 5.25–5.50%

Supplier power for ADIB is moderate-high: large depositors and sukuk investors can reprice liquidity, Fed funds ~5.25–5.50% (2024) lifts funding costs; scarce Sharia scholars and Islamic specialists constrain product rollout; core IT/vendors create high switching costs.

| Supplier | Concentration | 2024 metric |

|---|---|---|

| Sukuk/interbank | Medium | Fed funds 5.25–5.50% |

| Sharia scholars | High | Global Islamic assets ~$3.7T |

| IT vendors | High | Vendor lock-in |

What is included in the product

Concise Porter's Five Forces assessment of Abu Dhabi Islamic Bank, identifying competitive rivalry, buyer and supplier power, entry barriers, and substitute threats with strategic implications for market positioning.

Concise one-sheet Porter's Five Forces for Abu Dhabi Islamic Bank—instantly spot competitive pressures and regulatory risks for faster decisions. Customize force levels, swap your data, and export a radar chart-ready layout for pitch decks or boardroom slides.

Customers Bargaining Power

Large corporates and GREs

Large corporates and GREs wield strong bargaining power at Abu Dhabi Islamic Bank because their volume and multi-product relationships create concentrated revenue pools. In 2024 they routinely negotiate tighter pricing, stricter covenants and bespoke capital and treasury structures. Their ability to move relationships across UAE banks forces ADIB to offer competitive concessions. Losing such clients materially reduces fee income and cross-sell potential.

Retail customers’ switching ease

Digital onboarding and one-click account switching have lowered friction for retail clients, with UAE mobile banking adoption reaching about 80% in 2024, raising churn risk. Transparent profit rates and fees heighten price sensitivity across comparable Shariah products. Loyalty programs and personalized journeys reduce churn but are easily replicated. Service lapses rapidly trigger migration to rival apps, reflected in higher app-switch rates in 2024.

Sharia compliance expectations

Clients demand strong Sharia assurance, narrowing acceptable alternatives and increasing scrutiny on product design which concentrates buyer power around institutions with credible Sharia governance. Any perceived deviation can trigger reputational risk, client renegotiations and loss of trust, amplifying the stakes for ADIB. Clear disclosure and reputable Sharia boards help rebalance expectations and reduce bilateral friction.

SME financing needs

SMEs are highly rate-sensitive and routinely compare Islamic versus conventional pricing and collateral; globally SMEs represent about 90% of firms and ~50% of employment (World Bank/IFC), increasing their negotiating importance. Government-backed guarantee schemes partially standardize pricing, aiding buyer leverage, while faster credit decisions and digital documentation shift choices beyond price; weak SME data still limits bargaining power for some segments.

- SME price sensitivity

- Islamic vs conventional comparison

- Govt guarantees standardize pricing

- Speed and digital docs drive choice

- Poor SME data reduces leverage

Wealth and private clients

- multi‑banking: ~70% use custody/advisory mandates

- exclusive access: sukuk/private placements drive negotiation

- fee resilience: tied to relationship depth and bespoke services

Scale-driven pricing pressure; retail churn with 80% mobile adoption

Large corporates/GREs exert strong leverage through volume and multi‑product ties, forcing pricing and covenant concessions. Retail churn rose with UAE mobile banking adoption ~80% in 2024, increasing price sensitivity. SMEs remain highly price‑sensitive; SMEs are ~90% of firms and ~50% of employment (World Bank/IFC). Affluent clients multi‑bank (~70%) to secure exclusives and fee relief.

| Segment | Driver | 2024 metric |

|---|---|---|

| Corporates/GREs | Volume, bespoke terms | High revenue concentration |

| Retail | Digital churn | 80% mobile adoption |

| SMEs | Price sensitivity | 90% firms; 50% employment |

| Affluent | Multi‑banking, exclusives | ~70% advisory/custody |

Same Document Delivered

Abu Dhabi Islamic Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Abu Dhabi Islamic Bank you'll receive immediately after purchase—fully formatted, sourced and ready for use. It assesses competitive rivalry, supplier and buyer power, and threats of entry and substitutes, with clear strategic implications for ADIB. No placeholders or samples; the document available after payment is precisely this file.