Adient Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

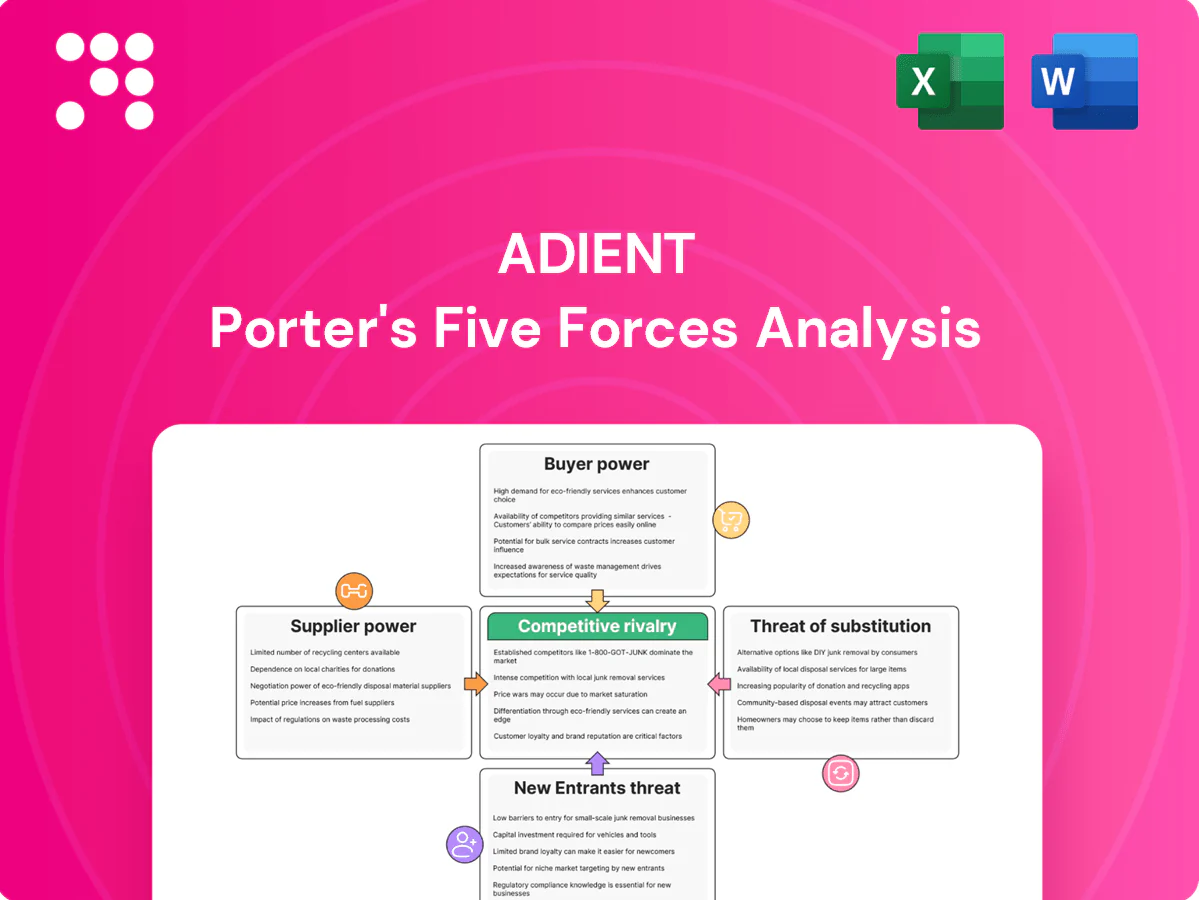

Adient faces strong buyer power and supplier concentration that pressure margins, while moderate threats from substitutes and new entrants keep competitive intensity high. Scale and OEM relationships are strategic advantages, yet cyclicality and material volatility are real risks. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Supplier Power 1

Adient depends on specialized global suppliers for steel, polyurethane chemicals, textiles and seating mechanisms, with roughly 60% of direct-material spend tied to these commodity categories. Steel and chemical price swings in 2024 amplified supplier leverage during tight markets, and while long-term contracts and hedging reduce volatility, pass-through cost pressures persisted. Regional JIT sourcing and local-content rules constrain substitution and increase supplier power.

Supplier Power 2

Advanced components like sensors, seat heaters and e-actuators come from a concentrated pool of qualified vendors, and stringent technical specs plus safety certifications create strong supplier stickiness that raises switching costs and can shift value capture to specialized Tier-2s; dual sourcing is feasible but typically adds complexity and extends validation time by around 6–12 months.

Supplier Power 3

Quality, safety and traceability mandates such as IATF 16949 drive higher supplier compliance costs; by 2024 over 60,000 certified sites globally increased bargaining credibility for compliant vendors. Vendors passing OEM-specific audits face lower risk of contract penalties, while non-conformance can trigger production stops and significant fines, boosting leverage for proven suppliers. Adient mitigates this through supplier development programs and performance scorecards that tracked a double-digit defect reduction in recent years.

Supplier Power 4

Regionalization and geopolitics sharply constrain Adient’s global supplier options, with import tariffs, logistics disruptions and local content rules favoring incumbent local suppliers and raising switching costs. Nearshoring reduces cross-border risk but narrows the qualified pool, increasing dependence on regional vendors. Requalification timelines remain long, typically 12–24 months, limiting rapid multi-sourcing.

- Regional supply entrenchment

- Tariffs and local content raise barriers

- Nearshoring lowers risk but reduces choices

- Requalification 12–24 months

Supplier Power 5

Supplier Power 5: Adient’s reliance on tooling and dedicated equipment ties platforms to specific suppliers for a program life, making mid-program supplier changes costly and risky for delays, warranty exposure, and added capex; tooling changeouts often cost millions and can delay launches. Suppliers time leverage around model launches to extract price concessions, while collaborative cost-down programs in 2024 reduced supplier cost exposure but did not eliminate asymmetry.

- Tooling lock-in: millions in sunk capex

- Switch risk: launch delays + warranty exposure

- Supplier timing: higher bargaining near launches

- 2024: cost-down programs partially offset pricing power

High supplier power: ~60%, 60k+ certified sites

Adient faces high supplier power: ~60% of direct-material spend tied to steel, chemicals and textiles, with 2024 price swings increasing leverage. Specialized electronic/actuator vendors and 60,000 IATF-certified sites raise switching costs; requalification takes 12–24 months. Tooling lock-in costs millions per program, concentrating bargaining around launches.

| Metric | 2024 |

|---|---|

| Direct-material spend concentration | ~60% |

| Certified supplier sites | 60,000+ |

| Requalification time | 12–24 months |

| Tooling cost (typ.) | Millions USD |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threats from new entrants and substitutes, and rivalry intensity specific to Adient—highlighting disruptive trends, pricing pressures, and barriers that protect incumbents; fully editable for integration into reports, investor materials, or strategy decks.

A clear, one-sheet Porter’s Five Forces for Adient—condensing supplier, buyer, rivalry, substitutes and entry threats into a single decision-ready view. Customize pressure levels and swap in your own data to reflect evolving automotive supply-chain and EV-market dynamics.

Customers Bargaining Power

Buyer Power 1

Global OEMs are highly concentrated and purchase in large volumes; top 5 OEMs represented about 45% of global light-vehicle production in 2024, giving them strong negotiating leverage. They run competitive RFQs and benchmark aggressively across Tier-1s, with annual price-downs commonly around 2–3% that pressure margins. Adient must deliver continuous productivity gains to retain awards and protect profitability.

Buyer Power 2

Switching costs for Adient are meaningful because design-in, tooling and validation are capital-intensive, yet OEMs typically plan multi-sourcing with ≥2 suppliers. Platform cycles of 4–6 years enable rebids that reset pricing and supplier mix. Performance on quality and delivery strongly influences re-awards, and poor KPIs can trigger rapid share loss within a program year despite switching frictions.

Buyer Power 3

OEMs enforce strict JIT/JIS schedules with line-stoppage penalties that materially raise suppliers’ service-risk; in 2024, global light-vehicle production was about 79 million units, intensifying delivery pressure. Sequencing near plants forces Adient to commit capital and working capital for kitting and sequencing lines, tying up cash and margins. Missing schedules can convert modest program margins into losses, amplifying buyer leverage on service and contract terms.

Buyer Power 4

Buyer Power 5

Electrification and interior innovation are shifting cockpit value as global EV sales reached about 14 million units in 2024, letting OEMs rebalance spend toward software and interiors. Buyers increasingly bundle interiors into larger Tier-1 packages to extract better terms, and consolidated regional sourcing drives scale concessions. Adient counters with lightweighting, modular platforms and sustainable materials to protect margins.

- Buyer leverage: bundling to Tier-1s

- Scale effect: cross-region sourcing

- Adient defense: lightweighting, modularity, recyclables

- 2024 signal: ~14M EVs accelerating cockpit repricing

Top-5 OEMs ≈45% share; 14M EVs shift cockpit pricing

Global OEMs (top-5 ≈45% of light-vehicle production in 2024) wield strong pricing and spec leverage, driving ~2–3% annual price-downs and aggressive RFQs. Design-in/tooling raise switching costs but OEMs multi-source (≥2) and rebid every 4–6 years, enabling rapid share shifts if KPIs fail. JIT penalties, kitting capital and 14M EVs in 2024 concentrate buyer bargaining power.

| Metric | 2024 value | Impact |

|---|---|---|

| Top-5 OEM share | ≈45% | High price leverage |

| Global LV production | ≈81M units | Delivery pressure |

| EV sales | ≈14M | Cockpit repricing |

| Annual price-downs | 2–3% | Margin compression |

Preview Before You Purchase

Adient Porter's Five Forces Analysis

This preview shows the exact Adient Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the same complete deliverable you'll get access to instantly upon payment.

A Must-Have Tool for Decision-Makers

Adient faces strong buyer power and supplier concentration that pressure margins, while moderate threats from substitutes and new entrants keep competitive intensity high. Scale and OEM relationships are strategic advantages, yet cyclicality and material volatility are real risks. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Supplier Power 1

Adient depends on specialized global suppliers for steel, polyurethane chemicals, textiles and seating mechanisms, with roughly 60% of direct-material spend tied to these commodity categories. Steel and chemical price swings in 2024 amplified supplier leverage during tight markets, and while long-term contracts and hedging reduce volatility, pass-through cost pressures persisted. Regional JIT sourcing and local-content rules constrain substitution and increase supplier power.

Supplier Power 2

Advanced components like sensors, seat heaters and e-actuators come from a concentrated pool of qualified vendors, and stringent technical specs plus safety certifications create strong supplier stickiness that raises switching costs and can shift value capture to specialized Tier-2s; dual sourcing is feasible but typically adds complexity and extends validation time by around 6–12 months.

Supplier Power 3

Quality, safety and traceability mandates such as IATF 16949 drive higher supplier compliance costs; by 2024 over 60,000 certified sites globally increased bargaining credibility for compliant vendors. Vendors passing OEM-specific audits face lower risk of contract penalties, while non-conformance can trigger production stops and significant fines, boosting leverage for proven suppliers. Adient mitigates this through supplier development programs and performance scorecards that tracked a double-digit defect reduction in recent years.

Supplier Power 4

Regionalization and geopolitics sharply constrain Adient’s global supplier options, with import tariffs, logistics disruptions and local content rules favoring incumbent local suppliers and raising switching costs. Nearshoring reduces cross-border risk but narrows the qualified pool, increasing dependence on regional vendors. Requalification timelines remain long, typically 12–24 months, limiting rapid multi-sourcing.

- Regional supply entrenchment

- Tariffs and local content raise barriers

- Nearshoring lowers risk but reduces choices

- Requalification 12–24 months

Supplier Power 5

Supplier Power 5: Adient’s reliance on tooling and dedicated equipment ties platforms to specific suppliers for a program life, making mid-program supplier changes costly and risky for delays, warranty exposure, and added capex; tooling changeouts often cost millions and can delay launches. Suppliers time leverage around model launches to extract price concessions, while collaborative cost-down programs in 2024 reduced supplier cost exposure but did not eliminate asymmetry.

- Tooling lock-in: millions in sunk capex

- Switch risk: launch delays + warranty exposure

- Supplier timing: higher bargaining near launches

- 2024: cost-down programs partially offset pricing power

High supplier power: ~60%, 60k+ certified sites

Adient faces high supplier power: ~60% of direct-material spend tied to steel, chemicals and textiles, with 2024 price swings increasing leverage. Specialized electronic/actuator vendors and 60,000 IATF-certified sites raise switching costs; requalification takes 12–24 months. Tooling lock-in costs millions per program, concentrating bargaining around launches.

| Metric | 2024 |

|---|---|

| Direct-material spend concentration | ~60% |

| Certified supplier sites | 60,000+ |

| Requalification time | 12–24 months |

| Tooling cost (typ.) | Millions USD |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threats from new entrants and substitutes, and rivalry intensity specific to Adient—highlighting disruptive trends, pricing pressures, and barriers that protect incumbents; fully editable for integration into reports, investor materials, or strategy decks.

A clear, one-sheet Porter’s Five Forces for Adient—condensing supplier, buyer, rivalry, substitutes and entry threats into a single decision-ready view. Customize pressure levels and swap in your own data to reflect evolving automotive supply-chain and EV-market dynamics.

Customers Bargaining Power

Buyer Power 1

Global OEMs are highly concentrated and purchase in large volumes; top 5 OEMs represented about 45% of global light-vehicle production in 2024, giving them strong negotiating leverage. They run competitive RFQs and benchmark aggressively across Tier-1s, with annual price-downs commonly around 2–3% that pressure margins. Adient must deliver continuous productivity gains to retain awards and protect profitability.

Buyer Power 2

Switching costs for Adient are meaningful because design-in, tooling and validation are capital-intensive, yet OEMs typically plan multi-sourcing with ≥2 suppliers. Platform cycles of 4–6 years enable rebids that reset pricing and supplier mix. Performance on quality and delivery strongly influences re-awards, and poor KPIs can trigger rapid share loss within a program year despite switching frictions.

Buyer Power 3

OEMs enforce strict JIT/JIS schedules with line-stoppage penalties that materially raise suppliers’ service-risk; in 2024, global light-vehicle production was about 79 million units, intensifying delivery pressure. Sequencing near plants forces Adient to commit capital and working capital for kitting and sequencing lines, tying up cash and margins. Missing schedules can convert modest program margins into losses, amplifying buyer leverage on service and contract terms.

Buyer Power 4

Buyer Power 5

Electrification and interior innovation are shifting cockpit value as global EV sales reached about 14 million units in 2024, letting OEMs rebalance spend toward software and interiors. Buyers increasingly bundle interiors into larger Tier-1 packages to extract better terms, and consolidated regional sourcing drives scale concessions. Adient counters with lightweighting, modular platforms and sustainable materials to protect margins.

- Buyer leverage: bundling to Tier-1s

- Scale effect: cross-region sourcing

- Adient defense: lightweighting, modularity, recyclables

- 2024 signal: ~14M EVs accelerating cockpit repricing

Top-5 OEMs ≈45% share; 14M EVs shift cockpit pricing

Global OEMs (top-5 ≈45% of light-vehicle production in 2024) wield strong pricing and spec leverage, driving ~2–3% annual price-downs and aggressive RFQs. Design-in/tooling raise switching costs but OEMs multi-source (≥2) and rebid every 4–6 years, enabling rapid share shifts if KPIs fail. JIT penalties, kitting capital and 14M EVs in 2024 concentrate buyer bargaining power.

| Metric | 2024 value | Impact |

|---|---|---|

| Top-5 OEM share | ≈45% | High price leverage |

| Global LV production | ≈81M units | Delivery pressure |

| EV sales | ≈14M | Cockpit repricing |

| Annual price-downs | 2–3% | Margin compression |

Preview Before You Purchase

Adient Porter's Five Forces Analysis

This preview shows the exact Adient Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the same complete deliverable you'll get access to instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Adient faces strong buyer power and supplier concentration that pressure margins, while moderate threats from substitutes and new entrants keep competitive intensity high. Scale and OEM relationships are strategic advantages, yet cyclicality and material volatility are real risks. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Supplier Power 1

Adient depends on specialized global suppliers for steel, polyurethane chemicals, textiles and seating mechanisms, with roughly 60% of direct-material spend tied to these commodity categories. Steel and chemical price swings in 2024 amplified supplier leverage during tight markets, and while long-term contracts and hedging reduce volatility, pass-through cost pressures persisted. Regional JIT sourcing and local-content rules constrain substitution and increase supplier power.

Supplier Power 2

Advanced components like sensors, seat heaters and e-actuators come from a concentrated pool of qualified vendors, and stringent technical specs plus safety certifications create strong supplier stickiness that raises switching costs and can shift value capture to specialized Tier-2s; dual sourcing is feasible but typically adds complexity and extends validation time by around 6–12 months.

Supplier Power 3

Quality, safety and traceability mandates such as IATF 16949 drive higher supplier compliance costs; by 2024 over 60,000 certified sites globally increased bargaining credibility for compliant vendors. Vendors passing OEM-specific audits face lower risk of contract penalties, while non-conformance can trigger production stops and significant fines, boosting leverage for proven suppliers. Adient mitigates this through supplier development programs and performance scorecards that tracked a double-digit defect reduction in recent years.

Supplier Power 4

Regionalization and geopolitics sharply constrain Adient’s global supplier options, with import tariffs, logistics disruptions and local content rules favoring incumbent local suppliers and raising switching costs. Nearshoring reduces cross-border risk but narrows the qualified pool, increasing dependence on regional vendors. Requalification timelines remain long, typically 12–24 months, limiting rapid multi-sourcing.

- Regional supply entrenchment

- Tariffs and local content raise barriers

- Nearshoring lowers risk but reduces choices

- Requalification 12–24 months

Supplier Power 5

Supplier Power 5: Adient’s reliance on tooling and dedicated equipment ties platforms to specific suppliers for a program life, making mid-program supplier changes costly and risky for delays, warranty exposure, and added capex; tooling changeouts often cost millions and can delay launches. Suppliers time leverage around model launches to extract price concessions, while collaborative cost-down programs in 2024 reduced supplier cost exposure but did not eliminate asymmetry.

- Tooling lock-in: millions in sunk capex

- Switch risk: launch delays + warranty exposure

- Supplier timing: higher bargaining near launches

- 2024: cost-down programs partially offset pricing power

High supplier power: ~60%, 60k+ certified sites

Adient faces high supplier power: ~60% of direct-material spend tied to steel, chemicals and textiles, with 2024 price swings increasing leverage. Specialized electronic/actuator vendors and 60,000 IATF-certified sites raise switching costs; requalification takes 12–24 months. Tooling lock-in costs millions per program, concentrating bargaining around launches.

| Metric | 2024 |

|---|---|

| Direct-material spend concentration | ~60% |

| Certified supplier sites | 60,000+ |

| Requalification time | 12–24 months |

| Tooling cost (typ.) | Millions USD |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threats from new entrants and substitutes, and rivalry intensity specific to Adient—highlighting disruptive trends, pricing pressures, and barriers that protect incumbents; fully editable for integration into reports, investor materials, or strategy decks.

A clear, one-sheet Porter’s Five Forces for Adient—condensing supplier, buyer, rivalry, substitutes and entry threats into a single decision-ready view. Customize pressure levels and swap in your own data to reflect evolving automotive supply-chain and EV-market dynamics.

Customers Bargaining Power

Buyer Power 1

Global OEMs are highly concentrated and purchase in large volumes; top 5 OEMs represented about 45% of global light-vehicle production in 2024, giving them strong negotiating leverage. They run competitive RFQs and benchmark aggressively across Tier-1s, with annual price-downs commonly around 2–3% that pressure margins. Adient must deliver continuous productivity gains to retain awards and protect profitability.

Buyer Power 2

Switching costs for Adient are meaningful because design-in, tooling and validation are capital-intensive, yet OEMs typically plan multi-sourcing with ≥2 suppliers. Platform cycles of 4–6 years enable rebids that reset pricing and supplier mix. Performance on quality and delivery strongly influences re-awards, and poor KPIs can trigger rapid share loss within a program year despite switching frictions.

Buyer Power 3

OEMs enforce strict JIT/JIS schedules with line-stoppage penalties that materially raise suppliers’ service-risk; in 2024, global light-vehicle production was about 79 million units, intensifying delivery pressure. Sequencing near plants forces Adient to commit capital and working capital for kitting and sequencing lines, tying up cash and margins. Missing schedules can convert modest program margins into losses, amplifying buyer leverage on service and contract terms.

Buyer Power 4

Buyer Power 5

Electrification and interior innovation are shifting cockpit value as global EV sales reached about 14 million units in 2024, letting OEMs rebalance spend toward software and interiors. Buyers increasingly bundle interiors into larger Tier-1 packages to extract better terms, and consolidated regional sourcing drives scale concessions. Adient counters with lightweighting, modular platforms and sustainable materials to protect margins.

- Buyer leverage: bundling to Tier-1s

- Scale effect: cross-region sourcing

- Adient defense: lightweighting, modularity, recyclables

- 2024 signal: ~14M EVs accelerating cockpit repricing

Top-5 OEMs ≈45% share; 14M EVs shift cockpit pricing

Global OEMs (top-5 ≈45% of light-vehicle production in 2024) wield strong pricing and spec leverage, driving ~2–3% annual price-downs and aggressive RFQs. Design-in/tooling raise switching costs but OEMs multi-source (≥2) and rebid every 4–6 years, enabling rapid share shifts if KPIs fail. JIT penalties, kitting capital and 14M EVs in 2024 concentrate buyer bargaining power.

| Metric | 2024 value | Impact |

|---|---|---|

| Top-5 OEM share | ≈45% | High price leverage |

| Global LV production | ≈81M units | Delivery pressure |

| EV sales | ≈14M | Cockpit repricing |

| Annual price-downs | 2–3% | Margin compression |

Preview Before You Purchase

Adient Porter's Five Forces Analysis

This preview shows the exact Adient Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the same complete deliverable you'll get access to instantly upon payment.