ADM Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

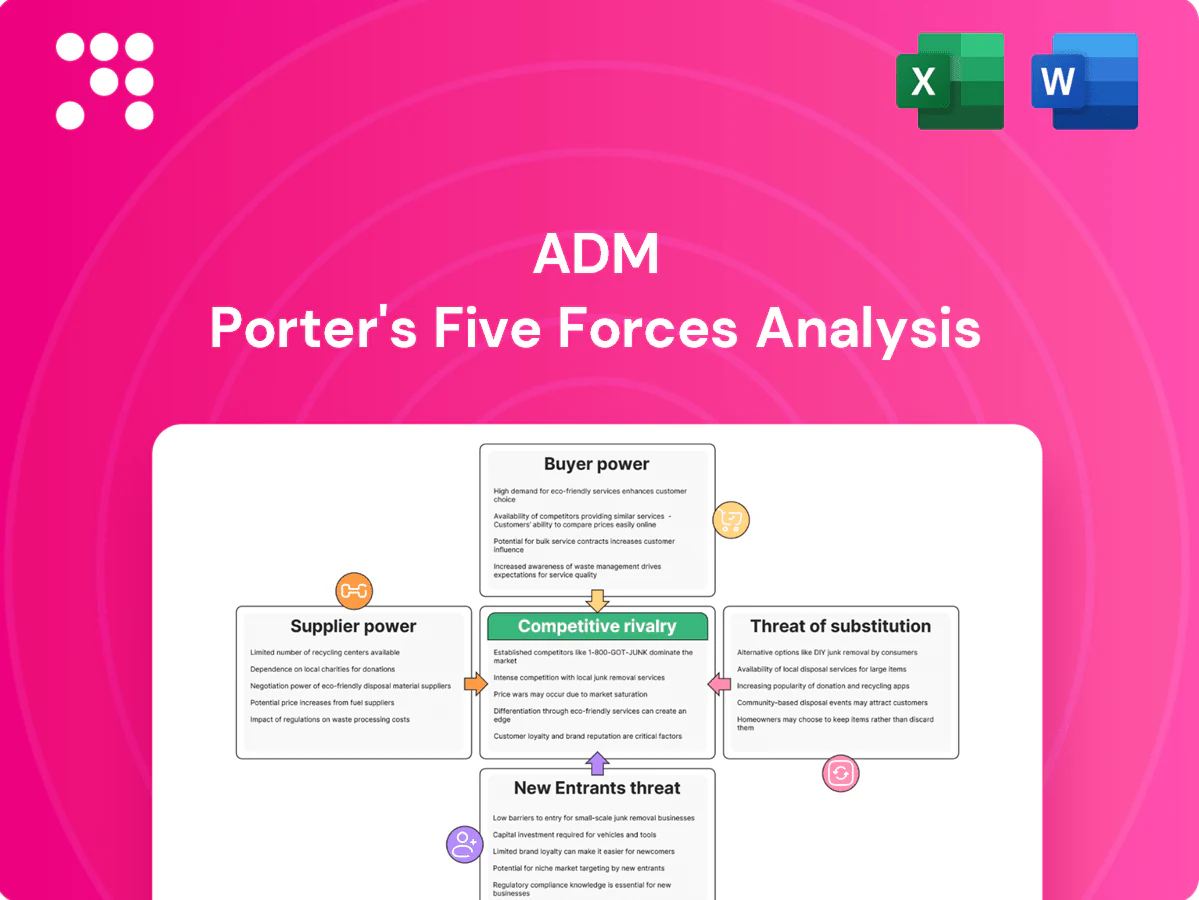

Archer-Daniels-Midland’s Porter’s Five Forces snapshot highlights supplier clout, buyer pressures, competitive rivalry, substitute risks and entry barriers shaping its agribusiness edge. This brief outlines where ADM gains leverage and where external threats persist. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals and actionable strategy insights.

Suppliers Bargaining Power

Fragmented farm base limits leverage

ADM sources crops from millions of farmers across regions, diluting any single supplier’s bargaining power and keeping supplier concentration low in 2024. Transparent spot and forward markets, including exchange-traded benchmarks, further cap supplier influence on pricing. Localized cooperatives can gain leverage during tight harvests or logistical bottlenecks. ADM’s broad origination footprint lets it pivot across sources, reducing dependency on any single supplier.

Weather and geopolitics swing supply

Yield shocks from droughts, floods or export bans temporarily raise supplier power as scarcity pricing forces ADM to pay up or reroute volumes, compressing margins. Hedging reduces traded-price exposure but leaves physical basis risk during local shortfalls. Diversified sourcing and on‑farm and commercial storage smooth supply swings and limit episodic supplier leverage. Operational flexibility and logistics scale remain essential to contain cost shocks.

Transport providers hold chokepoints

Railroads, barge operators and ocean shippers exert chokepoint power where capacity tightens—U.S. rail moves roughly 40% of freight by ton‑miles and ocean carriers remain highly concentrated (top 10 carriers control over 80% of container capacity). Fuel surcharges and congestion lift freight costs—U.S. average on‑highway diesel ran around $4/gal in 2024 (EIA). ADM’s owned and leased logistics assets offset some leverage but cannot cover every lane, while long‑term contracts and modal flexibility materially reduce exposure.

Specialty inputs tighten switching

Processing relies on enzymes, specialty chemicals and packaging where qualified suppliers are concentrated—top 3 enzyme makers supply roughly 60–70% of the market—so qualification and audit requirements create switching frictions that allow niche suppliers pricing latitude; ADM reported about $91.8 billion revenue in 2024 and mitigates this via dual-sourcing and scale purchasing to lower cost exposure.

- Supplier concentration: top 3 ~60–70%

- Switching frictions: strict audits/qualifications

- ADM 2024 revenue: ~$91.8B

- Mitigants: dual-sourcing, scale purchasing

Sustainability and identity-preserved crops

Certified non-GMO, organic and regenerative crops come from narrow supplier pools, raising supplier leverage as premiums and monitoring costs (often 10–30% in 2024 markets) increase. ADM’s contract-farming and traceability programs lock volumes and harvest data, reducing short-term supply risk. Long-term supplier development and capacity building can rebalance power.

- Narrow pools: limited certified growers

- Premiums: 10–30% typical (2024)

- ADM mitigants: contracts + traceability

- Outlook: supplier development reduces power over time

Scale limits supplier power; transport chokepoints and enzyme concentration drive price spikes

ADM’s supplier power is limited by millions of farmers, diversified origination and $91.8B 2024 scale, but certified/organic pools (premiums 10–30% in 2024) and niche inputs raise leverage. Transport chokepoints (U.S. rail ~40% ton‑miles; top10 carriers >80% capacity) and top‑3 enzyme share ~60–70% create episodic pricing pressure. Dual‑sourcing, contracts and storage mitigate risk.

| Metric | 2024 Value |

|---|---|

| ADM revenue | $91.8B |

| Certified premiums | 10–30% |

| U.S. rail share | ~40% ton‑miles |

| Top‑3 enzyme share | 60–70% |

What is included in the product

Tailored Porter's Five Forces analysis for ADM that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats affecting its pricing and profitability; includes strategic commentary and editable findings for investor reports and strategy decks.

Condensed ADM Porter's Five Forces snapshot—clarifies supplier/customer power, commodity price risk, substitute and entrant threats for faster strategic decisions and investor briefings.

Customers Bargaining Power

Large CPGs and feed integrators negotiate hard

Global food and beverage giants and large animal-protein integrators concentrate buying power, forcing price concessions, higher service levels, and supplier consolidation; ADM reported full-year 2024 net sales of about $103 billion, underscoring the scale it faces.

Commodity price transparency

In 2024 futures benchmarks and published basis quotes provided clear reference points that empowered buyers to compare offers transparently. Easy switching among merchandisers for standard grades kept origination and trading spreads compressed. ADM countered this pressure by differentiating through reliability, working-capital financing and superior logistics performance.

Value-added ingredients reduce power

ADM’s customized systems, flavors and nutrition solutions increase customer stickiness, with specialty nutrition representing roughly 20% of ADM’s portfolio by 2024 and growing faster than commodity segments. Formulation support and co-innovation raise switching costs as customers integrate ADM recipes and specs into products, enabling ADM to capture higher-margin contracts. Buyers often accept 5–15% pricing premiums when verified performance or health claims are delivered, reinforcing reduced bargaining power.

Backward integration and direct sourcing

Some buyers increasingly procure directly from farmers or via digital platforms, bypassing intermediaries for basic commodities; yet ADM’s scale and FY2023 net sales of 98.3 billion dollars, global risk-management systems and certified quality controls keep customers tied to the firm. Service bundling (logistics, processing, traceability) blunts disintermediation by adding switching costs and reliability advantages.

- Direct sourcing growth: selective bypass

- ADM scale: $98.3B FY2023

- Bundled services reduce churn

Demand volatility and SKU churn

Rapid shifts in consumer preferences force buyers to demand flexibility, shortening lead times and transferring inventory risk to suppliers, increasing customer bargaining power; ADM’s global logistics and storage mitigate variability but at the cost of scale—ADM reported approximately $95 billion in net sales in 2024, reflecting volume resilience amid volatility.

- Shorter lead times raise buyer leverage

- Inventory risk shifted to suppliers

- ADM storage/network absorb variability

- 2024 net sales ~ $95 billion

- Contracts use indexation/fees to rebalance

Concentrated buyers squeeze margins; supplier posts $103B

Large global buyers concentrate purchasing power, forcing price concessions and service demands; ADM reported full-year 2024 net sales of about $103 billion, reflecting the scale of counterparties. Transparent 2024 futures and basis quotes compressed spreads and eased switching for standard grades, while ADM’s specialty nutrition (~20% of portfolio in 2024) and co‑innovation raise switching costs, enabling 5–15% pricing premiums for verified claims.

| Metric | 2024 |

|---|---|

| ADM net sales | $103B |

| Specialty nutrition share | ~20% |

| Buyer premium for verified claims | 5–15% |

Full Version Awaits

ADM Porter's Five Forces Analysis

This preview shows the exact ADM Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted and ready to use. It contains the complete assessment of supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. No placeholders or samples; what you see is the deliverable available for instant download after payment.

A Must-Have Tool for Decision-Makers

Archer-Daniels-Midland’s Porter’s Five Forces snapshot highlights supplier clout, buyer pressures, competitive rivalry, substitute risks and entry barriers shaping its agribusiness edge. This brief outlines where ADM gains leverage and where external threats persist. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals and actionable strategy insights.

Suppliers Bargaining Power

Fragmented farm base limits leverage

ADM sources crops from millions of farmers across regions, diluting any single supplier’s bargaining power and keeping supplier concentration low in 2024. Transparent spot and forward markets, including exchange-traded benchmarks, further cap supplier influence on pricing. Localized cooperatives can gain leverage during tight harvests or logistical bottlenecks. ADM’s broad origination footprint lets it pivot across sources, reducing dependency on any single supplier.

Weather and geopolitics swing supply

Yield shocks from droughts, floods or export bans temporarily raise supplier power as scarcity pricing forces ADM to pay up or reroute volumes, compressing margins. Hedging reduces traded-price exposure but leaves physical basis risk during local shortfalls. Diversified sourcing and on‑farm and commercial storage smooth supply swings and limit episodic supplier leverage. Operational flexibility and logistics scale remain essential to contain cost shocks.

Transport providers hold chokepoints

Railroads, barge operators and ocean shippers exert chokepoint power where capacity tightens—U.S. rail moves roughly 40% of freight by ton‑miles and ocean carriers remain highly concentrated (top 10 carriers control over 80% of container capacity). Fuel surcharges and congestion lift freight costs—U.S. average on‑highway diesel ran around $4/gal in 2024 (EIA). ADM’s owned and leased logistics assets offset some leverage but cannot cover every lane, while long‑term contracts and modal flexibility materially reduce exposure.

Specialty inputs tighten switching

Processing relies on enzymes, specialty chemicals and packaging where qualified suppliers are concentrated—top 3 enzyme makers supply roughly 60–70% of the market—so qualification and audit requirements create switching frictions that allow niche suppliers pricing latitude; ADM reported about $91.8 billion revenue in 2024 and mitigates this via dual-sourcing and scale purchasing to lower cost exposure.

- Supplier concentration: top 3 ~60–70%

- Switching frictions: strict audits/qualifications

- ADM 2024 revenue: ~$91.8B

- Mitigants: dual-sourcing, scale purchasing

Sustainability and identity-preserved crops

Certified non-GMO, organic and regenerative crops come from narrow supplier pools, raising supplier leverage as premiums and monitoring costs (often 10–30% in 2024 markets) increase. ADM’s contract-farming and traceability programs lock volumes and harvest data, reducing short-term supply risk. Long-term supplier development and capacity building can rebalance power.

- Narrow pools: limited certified growers

- Premiums: 10–30% typical (2024)

- ADM mitigants: contracts + traceability

- Outlook: supplier development reduces power over time

Scale limits supplier power; transport chokepoints and enzyme concentration drive price spikes

ADM’s supplier power is limited by millions of farmers, diversified origination and $91.8B 2024 scale, but certified/organic pools (premiums 10–30% in 2024) and niche inputs raise leverage. Transport chokepoints (U.S. rail ~40% ton‑miles; top10 carriers >80% capacity) and top‑3 enzyme share ~60–70% create episodic pricing pressure. Dual‑sourcing, contracts and storage mitigate risk.

| Metric | 2024 Value |

|---|---|

| ADM revenue | $91.8B |

| Certified premiums | 10–30% |

| U.S. rail share | ~40% ton‑miles |

| Top‑3 enzyme share | 60–70% |

What is included in the product

Tailored Porter's Five Forces analysis for ADM that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats affecting its pricing and profitability; includes strategic commentary and editable findings for investor reports and strategy decks.

Condensed ADM Porter's Five Forces snapshot—clarifies supplier/customer power, commodity price risk, substitute and entrant threats for faster strategic decisions and investor briefings.

Customers Bargaining Power

Large CPGs and feed integrators negotiate hard

Global food and beverage giants and large animal-protein integrators concentrate buying power, forcing price concessions, higher service levels, and supplier consolidation; ADM reported full-year 2024 net sales of about $103 billion, underscoring the scale it faces.

Commodity price transparency

In 2024 futures benchmarks and published basis quotes provided clear reference points that empowered buyers to compare offers transparently. Easy switching among merchandisers for standard grades kept origination and trading spreads compressed. ADM countered this pressure by differentiating through reliability, working-capital financing and superior logistics performance.

Value-added ingredients reduce power

ADM’s customized systems, flavors and nutrition solutions increase customer stickiness, with specialty nutrition representing roughly 20% of ADM’s portfolio by 2024 and growing faster than commodity segments. Formulation support and co-innovation raise switching costs as customers integrate ADM recipes and specs into products, enabling ADM to capture higher-margin contracts. Buyers often accept 5–15% pricing premiums when verified performance or health claims are delivered, reinforcing reduced bargaining power.

Backward integration and direct sourcing

Some buyers increasingly procure directly from farmers or via digital platforms, bypassing intermediaries for basic commodities; yet ADM’s scale and FY2023 net sales of 98.3 billion dollars, global risk-management systems and certified quality controls keep customers tied to the firm. Service bundling (logistics, processing, traceability) blunts disintermediation by adding switching costs and reliability advantages.

- Direct sourcing growth: selective bypass

- ADM scale: $98.3B FY2023

- Bundled services reduce churn

Demand volatility and SKU churn

Rapid shifts in consumer preferences force buyers to demand flexibility, shortening lead times and transferring inventory risk to suppliers, increasing customer bargaining power; ADM’s global logistics and storage mitigate variability but at the cost of scale—ADM reported approximately $95 billion in net sales in 2024, reflecting volume resilience amid volatility.

- Shorter lead times raise buyer leverage

- Inventory risk shifted to suppliers

- ADM storage/network absorb variability

- 2024 net sales ~ $95 billion

- Contracts use indexation/fees to rebalance

Concentrated buyers squeeze margins; supplier posts $103B

Large global buyers concentrate purchasing power, forcing price concessions and service demands; ADM reported full-year 2024 net sales of about $103 billion, reflecting the scale of counterparties. Transparent 2024 futures and basis quotes compressed spreads and eased switching for standard grades, while ADM’s specialty nutrition (~20% of portfolio in 2024) and co‑innovation raise switching costs, enabling 5–15% pricing premiums for verified claims.

| Metric | 2024 |

|---|---|

| ADM net sales | $103B |

| Specialty nutrition share | ~20% |

| Buyer premium for verified claims | 5–15% |

Full Version Awaits

ADM Porter's Five Forces Analysis

This preview shows the exact ADM Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted and ready to use. It contains the complete assessment of supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. No placeholders or samples; what you see is the deliverable available for instant download after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Archer-Daniels-Midland’s Porter’s Five Forces snapshot highlights supplier clout, buyer pressures, competitive rivalry, substitute risks and entry barriers shaping its agribusiness edge. This brief outlines where ADM gains leverage and where external threats persist. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals and actionable strategy insights.

Suppliers Bargaining Power

Fragmented farm base limits leverage

ADM sources crops from millions of farmers across regions, diluting any single supplier’s bargaining power and keeping supplier concentration low in 2024. Transparent spot and forward markets, including exchange-traded benchmarks, further cap supplier influence on pricing. Localized cooperatives can gain leverage during tight harvests or logistical bottlenecks. ADM’s broad origination footprint lets it pivot across sources, reducing dependency on any single supplier.

Weather and geopolitics swing supply

Yield shocks from droughts, floods or export bans temporarily raise supplier power as scarcity pricing forces ADM to pay up or reroute volumes, compressing margins. Hedging reduces traded-price exposure but leaves physical basis risk during local shortfalls. Diversified sourcing and on‑farm and commercial storage smooth supply swings and limit episodic supplier leverage. Operational flexibility and logistics scale remain essential to contain cost shocks.

Transport providers hold chokepoints

Railroads, barge operators and ocean shippers exert chokepoint power where capacity tightens—U.S. rail moves roughly 40% of freight by ton‑miles and ocean carriers remain highly concentrated (top 10 carriers control over 80% of container capacity). Fuel surcharges and congestion lift freight costs—U.S. average on‑highway diesel ran around $4/gal in 2024 (EIA). ADM’s owned and leased logistics assets offset some leverage but cannot cover every lane, while long‑term contracts and modal flexibility materially reduce exposure.

Specialty inputs tighten switching

Processing relies on enzymes, specialty chemicals and packaging where qualified suppliers are concentrated—top 3 enzyme makers supply roughly 60–70% of the market—so qualification and audit requirements create switching frictions that allow niche suppliers pricing latitude; ADM reported about $91.8 billion revenue in 2024 and mitigates this via dual-sourcing and scale purchasing to lower cost exposure.

- Supplier concentration: top 3 ~60–70%

- Switching frictions: strict audits/qualifications

- ADM 2024 revenue: ~$91.8B

- Mitigants: dual-sourcing, scale purchasing

Sustainability and identity-preserved crops

Certified non-GMO, organic and regenerative crops come from narrow supplier pools, raising supplier leverage as premiums and monitoring costs (often 10–30% in 2024 markets) increase. ADM’s contract-farming and traceability programs lock volumes and harvest data, reducing short-term supply risk. Long-term supplier development and capacity building can rebalance power.

- Narrow pools: limited certified growers

- Premiums: 10–30% typical (2024)

- ADM mitigants: contracts + traceability

- Outlook: supplier development reduces power over time

Scale limits supplier power; transport chokepoints and enzyme concentration drive price spikes

ADM’s supplier power is limited by millions of farmers, diversified origination and $91.8B 2024 scale, but certified/organic pools (premiums 10–30% in 2024) and niche inputs raise leverage. Transport chokepoints (U.S. rail ~40% ton‑miles; top10 carriers >80% capacity) and top‑3 enzyme share ~60–70% create episodic pricing pressure. Dual‑sourcing, contracts and storage mitigate risk.

| Metric | 2024 Value |

|---|---|

| ADM revenue | $91.8B |

| Certified premiums | 10–30% |

| U.S. rail share | ~40% ton‑miles |

| Top‑3 enzyme share | 60–70% |

What is included in the product

Tailored Porter's Five Forces analysis for ADM that uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats affecting its pricing and profitability; includes strategic commentary and editable findings for investor reports and strategy decks.

Condensed ADM Porter's Five Forces snapshot—clarifies supplier/customer power, commodity price risk, substitute and entrant threats for faster strategic decisions and investor briefings.

Customers Bargaining Power

Large CPGs and feed integrators negotiate hard

Global food and beverage giants and large animal-protein integrators concentrate buying power, forcing price concessions, higher service levels, and supplier consolidation; ADM reported full-year 2024 net sales of about $103 billion, underscoring the scale it faces.

Commodity price transparency

In 2024 futures benchmarks and published basis quotes provided clear reference points that empowered buyers to compare offers transparently. Easy switching among merchandisers for standard grades kept origination and trading spreads compressed. ADM countered this pressure by differentiating through reliability, working-capital financing and superior logistics performance.

Value-added ingredients reduce power

ADM’s customized systems, flavors and nutrition solutions increase customer stickiness, with specialty nutrition representing roughly 20% of ADM’s portfolio by 2024 and growing faster than commodity segments. Formulation support and co-innovation raise switching costs as customers integrate ADM recipes and specs into products, enabling ADM to capture higher-margin contracts. Buyers often accept 5–15% pricing premiums when verified performance or health claims are delivered, reinforcing reduced bargaining power.

Backward integration and direct sourcing

Some buyers increasingly procure directly from farmers or via digital platforms, bypassing intermediaries for basic commodities; yet ADM’s scale and FY2023 net sales of 98.3 billion dollars, global risk-management systems and certified quality controls keep customers tied to the firm. Service bundling (logistics, processing, traceability) blunts disintermediation by adding switching costs and reliability advantages.

- Direct sourcing growth: selective bypass

- ADM scale: $98.3B FY2023

- Bundled services reduce churn

Demand volatility and SKU churn

Rapid shifts in consumer preferences force buyers to demand flexibility, shortening lead times and transferring inventory risk to suppliers, increasing customer bargaining power; ADM’s global logistics and storage mitigate variability but at the cost of scale—ADM reported approximately $95 billion in net sales in 2024, reflecting volume resilience amid volatility.

- Shorter lead times raise buyer leverage

- Inventory risk shifted to suppliers

- ADM storage/network absorb variability

- 2024 net sales ~ $95 billion

- Contracts use indexation/fees to rebalance

Concentrated buyers squeeze margins; supplier posts $103B

Large global buyers concentrate purchasing power, forcing price concessions and service demands; ADM reported full-year 2024 net sales of about $103 billion, reflecting the scale of counterparties. Transparent 2024 futures and basis quotes compressed spreads and eased switching for standard grades, while ADM’s specialty nutrition (~20% of portfolio in 2024) and co‑innovation raise switching costs, enabling 5–15% pricing premiums for verified claims.

| Metric | 2024 |

|---|---|

| ADM net sales | $103B |

| Specialty nutrition share | ~20% |

| Buyer premium for verified claims | 5–15% |

Full Version Awaits

ADM Porter's Five Forces Analysis

This preview shows the exact ADM Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted and ready to use. It contains the complete assessment of supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. No placeholders or samples; what you see is the deliverable available for instant download after payment.