Advanced Medical Solutions Group SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

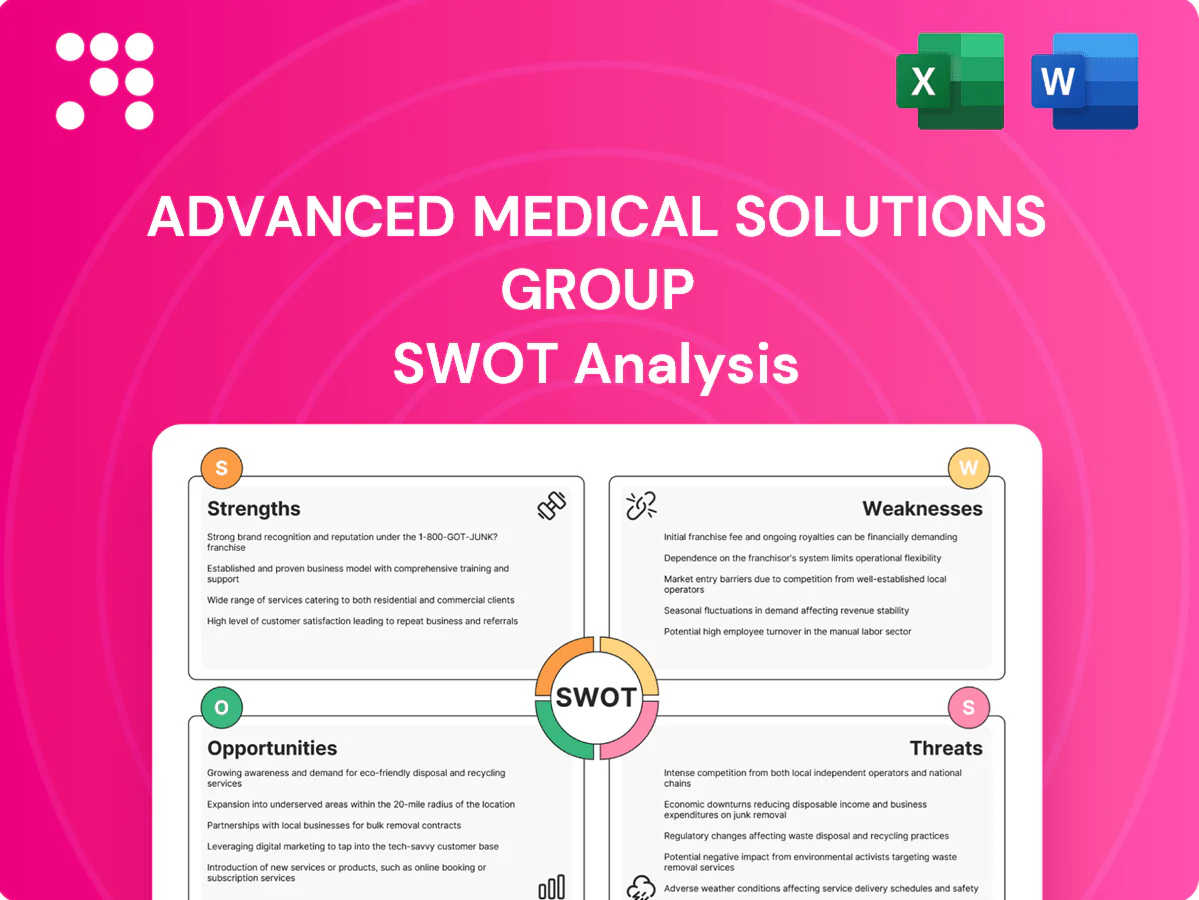

Advanced Medical Solutions Group shows strengths in a diversified med‑tech portfolio, strong R&D and global contracts, but faces regulatory exposure and supply‑chain sensitivity; growth opportunities include aging populations and emerging markets. Want the full strategic picture and editable Word+Excel deliverables? Purchase the complete SWOT analysis for actionable insights and investor-ready planning.

Strengths

Diversified wound & surgical portfolio

AMS’s portfolio spans wound dressings, tissue adhesives, sutures and internal fixation devices, spreading commercial risk and supporting cross-selling and bundled hospital solutions; the group supplies c.60 countries and reported c.£170m revenue in FY2023, enabling access to surgical, wound-care and infection-prevention budgets and cushioning demand cyclicality in any single product line.

Proprietary materials & infection control

AMS proprietary silver alginates (Silvercel), advanced foams and adhesives deliver antimicrobial and hemostatic benefits that drive clinician preference and support premium pricing. With 1 in 31 hospital patients affected by healthcare-associated infections (CDC) and ~7% HAI prevalence in high-income settings (WHO), infection-prevention positioning aligns with quality metrics and cost-reduction goals, strengthening formulary acceptance and guideline inclusion.

In-house R&D and manufacturing

Vertical integration supports quality, supply reliability and cost control, helping Advanced Medical Solutions translate internal manufacturing into stronger unit economics noted in FY 2024. In-house R&D and production accelerate iterative innovation and customization for OEM and private-label partners, shortening time-to-market. Specialized manufacturing know-how in biomaterials and adhesives creates a tangible barrier to entry and supports higher margins versus outsourced peers.

Global market access

Advanced Medical Solutions markets products in over 80 countries, diversifying revenue streams and reducing single-market exposure; group revenue in FY2024 reached £114.5m, underscoring international contribution to growth.

Its global reach lets AMS capture varying reimbursement regimes and higher procedure growth in emerging markets, supporting scalable partnerships with distributors and device OEMs to expand market share.

Broader geographic access accelerates multicentre data generation and clinician advocacy across regions, strengthening adoption and long-term commercial traction.

- Global footprint: presence in 80+ countries

- FY2024 revenue: £114.5m

- International revenue: ~65% of group sales

- Supports distributor and OEM partnerships for scale

Regulatory and quality track record

Advanced Medical Solutions Group plc, an AIM-listed UK medtech, operates in surgical and wound care where stringent compliance is mandatory; its ISO 13485 certification and CE-marked portfolio underpin trust with surgeons and procurers. A sustained record of regulatory approvals and audits reduces switching costs for new launches and smooths entry into adjacent indications and markets.

- Regulatory credentials: ISO 13485, CE-marked portfolio

- Market trust: AIM-listed UK medtech

- Commercial impact: lowers switching costs for adopters

Vertical integration and CE-marked portfolio boost pricing; FY2024 revenue £114.5m

Vertical integration, ISO 13485 certification and CE-marked portfolio underpin reliable supply, quality and higher margins; FY2024 revenue £114.5m with ~65% international sales and presence in 80+ countries. Proprietary Silvercel silver alginates and adhesives drive clinician preference, infection-prevention positioning and premium pricing. Diversified product mix (wound dressings, adhesives, sutures, fixation) supports cross-selling and OEM partnerships.

| Metric | Value |

|---|---|

| FY2024 revenue | £114.5m |

| International sales | ~65% |

| Geographic reach | 80+ countries |

What is included in the product

Provides a concise SWOT overview of Advanced Medical Solutions Group, highlighting internal capabilities and operational gaps, identifying market opportunities and competitive threats that shape the company’s growth and strategic positioning.

Delivers a compact SWOT matrix tailored to Advanced Medical Solutions Group for rapid identification and mitigation of operational, regulatory, and market pain points.

Weaknesses

Limited brand versus medtech giants

Against large medtech incumbents, AMS has lower brand recognition and narrower direct sales coverage, slowing uptake in competitive hospital tenders and extending sales cycles.

This increases reliance on distribution partners for international reach, raising margin leakage and control risks in key markets.

Brand gaps also constrain pricing power as several product lines face commoditization and tender-driven price pressure.

Exposure to tender pricing pressure

Wound dressings and sutures face commoditization and large hospital tenders, with the global wound care market at about $20.2bn in 2023 and competitive pricing squeezing margins. Price competition in tenders can cut supplier margins materially, while hospitals increasingly focus on total cost of care. AMS must continuously prove clinical outcomes and economic value to defend pricing and avoid margin erosion.

Product concentration in wound care

Despite diversification, wound and surgical care still account for c.50% of AMS Group sales, concentrating revenue and making results vulnerable to market slowdowns or guideline changes; a 1% volume decline in this segment could cut group revenue materially. New entrants and private-label competition have pressured pricing in 2024, while reliance on public reimbursement increases sensitivity to tariff or policy shifts.

Regulatory and clinical evidence intensity

Adhesives and implantables demand robust clinical trials and ongoing post-market surveillance, often adding 12–24 months to development timelines and requiring multi-million-dollar evidence programs. Evidence generation is costly and time-consuming, and regulatory delays can stall pipeline launches and revenue recognition. Heavy resource allocation to compliance reduces commercial agility and limits capex for marketing and R&D expansion.

- 12–24 months added to development timelines

- Multi-million-dollar trial and surveillance costs

- Regulatory delays can postpone launches and revenues

- Compliance spending limits commercial flexibility

Scale constraints for direct sales

Building hospital-direct coverage is capital-intensive and AMS's limited feet-on-the-street restricts penetration in key metropolitan and tertiary markets, often ceding influence to distributor priorities and purchasing groups. Reliance on distributors can deprioritize AMS products versus larger principals, while slow rollout of clinician education hampers adoption of complex products requiring hands-on training and clinical support.

- High cost of direct hospital coverage

- Limited salesforce limits market penetration

- Distributor influence can deprioritize AMS

- Clinical-education needs slow adoption

Low brand recognition and distributor reliance slow tenders; wound sales ~50% in $20.2bn market

Lower brand recognition and limited hospital-direct coverage slow tender wins and extend sales cycles against larger medtech incumbents.

Heavy reliance on distributors raises margin leakage and control risk, constraining pricing power amid product commoditization.

Wound/surgical remains c.50% of Group sales, facing tender price pressure in a $20.2bn global wound market (2023); evidence programs add 12–24 months and multi-million-dollar costs.

| Weakness | Impact | Key metric |

|---|---|---|

| Revenue concentration | High sensitivity to market shifts | c.50% sales |

| Market pressure | Margin erosion | $20.2bn wound market (2023) |

| Evidence/regulatory | Delayed launches | 12–24 months; multi-million-$ trials |

Preview Before You Purchase

Advanced Medical Solutions Group SWOT Analysis

This is a real excerpt from the complete Advanced Medical Solutions Group SWOT analysis you'll receive upon purchase. The preview below is taken directly from the full report—no placeholders or samples. Buy now to unlock the full, editable, professional-quality document ready for use.

Go Beyond the Preview—Access the Full Strategic Report

Advanced Medical Solutions Group shows strengths in a diversified med‑tech portfolio, strong R&D and global contracts, but faces regulatory exposure and supply‑chain sensitivity; growth opportunities include aging populations and emerging markets. Want the full strategic picture and editable Word+Excel deliverables? Purchase the complete SWOT analysis for actionable insights and investor-ready planning.

Strengths

Diversified wound & surgical portfolio

AMS’s portfolio spans wound dressings, tissue adhesives, sutures and internal fixation devices, spreading commercial risk and supporting cross-selling and bundled hospital solutions; the group supplies c.60 countries and reported c.£170m revenue in FY2023, enabling access to surgical, wound-care and infection-prevention budgets and cushioning demand cyclicality in any single product line.

Proprietary materials & infection control

AMS proprietary silver alginates (Silvercel), advanced foams and adhesives deliver antimicrobial and hemostatic benefits that drive clinician preference and support premium pricing. With 1 in 31 hospital patients affected by healthcare-associated infections (CDC) and ~7% HAI prevalence in high-income settings (WHO), infection-prevention positioning aligns with quality metrics and cost-reduction goals, strengthening formulary acceptance and guideline inclusion.

In-house R&D and manufacturing

Vertical integration supports quality, supply reliability and cost control, helping Advanced Medical Solutions translate internal manufacturing into stronger unit economics noted in FY 2024. In-house R&D and production accelerate iterative innovation and customization for OEM and private-label partners, shortening time-to-market. Specialized manufacturing know-how in biomaterials and adhesives creates a tangible barrier to entry and supports higher margins versus outsourced peers.

Global market access

Advanced Medical Solutions markets products in over 80 countries, diversifying revenue streams and reducing single-market exposure; group revenue in FY2024 reached £114.5m, underscoring international contribution to growth.

Its global reach lets AMS capture varying reimbursement regimes and higher procedure growth in emerging markets, supporting scalable partnerships with distributors and device OEMs to expand market share.

Broader geographic access accelerates multicentre data generation and clinician advocacy across regions, strengthening adoption and long-term commercial traction.

- Global footprint: presence in 80+ countries

- FY2024 revenue: £114.5m

- International revenue: ~65% of group sales

- Supports distributor and OEM partnerships for scale

Regulatory and quality track record

Advanced Medical Solutions Group plc, an AIM-listed UK medtech, operates in surgical and wound care where stringent compliance is mandatory; its ISO 13485 certification and CE-marked portfolio underpin trust with surgeons and procurers. A sustained record of regulatory approvals and audits reduces switching costs for new launches and smooths entry into adjacent indications and markets.

- Regulatory credentials: ISO 13485, CE-marked portfolio

- Market trust: AIM-listed UK medtech

- Commercial impact: lowers switching costs for adopters

Vertical integration and CE-marked portfolio boost pricing; FY2024 revenue £114.5m

Vertical integration, ISO 13485 certification and CE-marked portfolio underpin reliable supply, quality and higher margins; FY2024 revenue £114.5m with ~65% international sales and presence in 80+ countries. Proprietary Silvercel silver alginates and adhesives drive clinician preference, infection-prevention positioning and premium pricing. Diversified product mix (wound dressings, adhesives, sutures, fixation) supports cross-selling and OEM partnerships.

| Metric | Value |

|---|---|

| FY2024 revenue | £114.5m |

| International sales | ~65% |

| Geographic reach | 80+ countries |

What is included in the product

Provides a concise SWOT overview of Advanced Medical Solutions Group, highlighting internal capabilities and operational gaps, identifying market opportunities and competitive threats that shape the company’s growth and strategic positioning.

Delivers a compact SWOT matrix tailored to Advanced Medical Solutions Group for rapid identification and mitigation of operational, regulatory, and market pain points.

Weaknesses

Limited brand versus medtech giants

Against large medtech incumbents, AMS has lower brand recognition and narrower direct sales coverage, slowing uptake in competitive hospital tenders and extending sales cycles.

This increases reliance on distribution partners for international reach, raising margin leakage and control risks in key markets.

Brand gaps also constrain pricing power as several product lines face commoditization and tender-driven price pressure.

Exposure to tender pricing pressure

Wound dressings and sutures face commoditization and large hospital tenders, with the global wound care market at about $20.2bn in 2023 and competitive pricing squeezing margins. Price competition in tenders can cut supplier margins materially, while hospitals increasingly focus on total cost of care. AMS must continuously prove clinical outcomes and economic value to defend pricing and avoid margin erosion.

Product concentration in wound care

Despite diversification, wound and surgical care still account for c.50% of AMS Group sales, concentrating revenue and making results vulnerable to market slowdowns or guideline changes; a 1% volume decline in this segment could cut group revenue materially. New entrants and private-label competition have pressured pricing in 2024, while reliance on public reimbursement increases sensitivity to tariff or policy shifts.

Regulatory and clinical evidence intensity

Adhesives and implantables demand robust clinical trials and ongoing post-market surveillance, often adding 12–24 months to development timelines and requiring multi-million-dollar evidence programs. Evidence generation is costly and time-consuming, and regulatory delays can stall pipeline launches and revenue recognition. Heavy resource allocation to compliance reduces commercial agility and limits capex for marketing and R&D expansion.

- 12–24 months added to development timelines

- Multi-million-dollar trial and surveillance costs

- Regulatory delays can postpone launches and revenues

- Compliance spending limits commercial flexibility

Scale constraints for direct sales

Building hospital-direct coverage is capital-intensive and AMS's limited feet-on-the-street restricts penetration in key metropolitan and tertiary markets, often ceding influence to distributor priorities and purchasing groups. Reliance on distributors can deprioritize AMS products versus larger principals, while slow rollout of clinician education hampers adoption of complex products requiring hands-on training and clinical support.

- High cost of direct hospital coverage

- Limited salesforce limits market penetration

- Distributor influence can deprioritize AMS

- Clinical-education needs slow adoption

Low brand recognition and distributor reliance slow tenders; wound sales ~50% in $20.2bn market

Lower brand recognition and limited hospital-direct coverage slow tender wins and extend sales cycles against larger medtech incumbents.

Heavy reliance on distributors raises margin leakage and control risk, constraining pricing power amid product commoditization.

Wound/surgical remains c.50% of Group sales, facing tender price pressure in a $20.2bn global wound market (2023); evidence programs add 12–24 months and multi-million-dollar costs.

| Weakness | Impact | Key metric |

|---|---|---|

| Revenue concentration | High sensitivity to market shifts | c.50% sales |

| Market pressure | Margin erosion | $20.2bn wound market (2023) |

| Evidence/regulatory | Delayed launches | 12–24 months; multi-million-$ trials |

Preview Before You Purchase

Advanced Medical Solutions Group SWOT Analysis

This is a real excerpt from the complete Advanced Medical Solutions Group SWOT analysis you'll receive upon purchase. The preview below is taken directly from the full report—no placeholders or samples. Buy now to unlock the full, editable, professional-quality document ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Advanced Medical Solutions Group shows strengths in a diversified med‑tech portfolio, strong R&D and global contracts, but faces regulatory exposure and supply‑chain sensitivity; growth opportunities include aging populations and emerging markets. Want the full strategic picture and editable Word+Excel deliverables? Purchase the complete SWOT analysis for actionable insights and investor-ready planning.

Strengths

Diversified wound & surgical portfolio

AMS’s portfolio spans wound dressings, tissue adhesives, sutures and internal fixation devices, spreading commercial risk and supporting cross-selling and bundled hospital solutions; the group supplies c.60 countries and reported c.£170m revenue in FY2023, enabling access to surgical, wound-care and infection-prevention budgets and cushioning demand cyclicality in any single product line.

Proprietary materials & infection control

AMS proprietary silver alginates (Silvercel), advanced foams and adhesives deliver antimicrobial and hemostatic benefits that drive clinician preference and support premium pricing. With 1 in 31 hospital patients affected by healthcare-associated infections (CDC) and ~7% HAI prevalence in high-income settings (WHO), infection-prevention positioning aligns with quality metrics and cost-reduction goals, strengthening formulary acceptance and guideline inclusion.

In-house R&D and manufacturing

Vertical integration supports quality, supply reliability and cost control, helping Advanced Medical Solutions translate internal manufacturing into stronger unit economics noted in FY 2024. In-house R&D and production accelerate iterative innovation and customization for OEM and private-label partners, shortening time-to-market. Specialized manufacturing know-how in biomaterials and adhesives creates a tangible barrier to entry and supports higher margins versus outsourced peers.

Global market access

Advanced Medical Solutions markets products in over 80 countries, diversifying revenue streams and reducing single-market exposure; group revenue in FY2024 reached £114.5m, underscoring international contribution to growth.

Its global reach lets AMS capture varying reimbursement regimes and higher procedure growth in emerging markets, supporting scalable partnerships with distributors and device OEMs to expand market share.

Broader geographic access accelerates multicentre data generation and clinician advocacy across regions, strengthening adoption and long-term commercial traction.

- Global footprint: presence in 80+ countries

- FY2024 revenue: £114.5m

- International revenue: ~65% of group sales

- Supports distributor and OEM partnerships for scale

Regulatory and quality track record

Advanced Medical Solutions Group plc, an AIM-listed UK medtech, operates in surgical and wound care where stringent compliance is mandatory; its ISO 13485 certification and CE-marked portfolio underpin trust with surgeons and procurers. A sustained record of regulatory approvals and audits reduces switching costs for new launches and smooths entry into adjacent indications and markets.

- Regulatory credentials: ISO 13485, CE-marked portfolio

- Market trust: AIM-listed UK medtech

- Commercial impact: lowers switching costs for adopters

Vertical integration and CE-marked portfolio boost pricing; FY2024 revenue £114.5m

Vertical integration, ISO 13485 certification and CE-marked portfolio underpin reliable supply, quality and higher margins; FY2024 revenue £114.5m with ~65% international sales and presence in 80+ countries. Proprietary Silvercel silver alginates and adhesives drive clinician preference, infection-prevention positioning and premium pricing. Diversified product mix (wound dressings, adhesives, sutures, fixation) supports cross-selling and OEM partnerships.

| Metric | Value |

|---|---|

| FY2024 revenue | £114.5m |

| International sales | ~65% |

| Geographic reach | 80+ countries |

What is included in the product

Provides a concise SWOT overview of Advanced Medical Solutions Group, highlighting internal capabilities and operational gaps, identifying market opportunities and competitive threats that shape the company’s growth and strategic positioning.

Delivers a compact SWOT matrix tailored to Advanced Medical Solutions Group for rapid identification and mitigation of operational, regulatory, and market pain points.

Weaknesses

Limited brand versus medtech giants

Against large medtech incumbents, AMS has lower brand recognition and narrower direct sales coverage, slowing uptake in competitive hospital tenders and extending sales cycles.

This increases reliance on distribution partners for international reach, raising margin leakage and control risks in key markets.

Brand gaps also constrain pricing power as several product lines face commoditization and tender-driven price pressure.

Exposure to tender pricing pressure

Wound dressings and sutures face commoditization and large hospital tenders, with the global wound care market at about $20.2bn in 2023 and competitive pricing squeezing margins. Price competition in tenders can cut supplier margins materially, while hospitals increasingly focus on total cost of care. AMS must continuously prove clinical outcomes and economic value to defend pricing and avoid margin erosion.

Product concentration in wound care

Despite diversification, wound and surgical care still account for c.50% of AMS Group sales, concentrating revenue and making results vulnerable to market slowdowns or guideline changes; a 1% volume decline in this segment could cut group revenue materially. New entrants and private-label competition have pressured pricing in 2024, while reliance on public reimbursement increases sensitivity to tariff or policy shifts.

Regulatory and clinical evidence intensity

Adhesives and implantables demand robust clinical trials and ongoing post-market surveillance, often adding 12–24 months to development timelines and requiring multi-million-dollar evidence programs. Evidence generation is costly and time-consuming, and regulatory delays can stall pipeline launches and revenue recognition. Heavy resource allocation to compliance reduces commercial agility and limits capex for marketing and R&D expansion.

- 12–24 months added to development timelines

- Multi-million-dollar trial and surveillance costs

- Regulatory delays can postpone launches and revenues

- Compliance spending limits commercial flexibility

Scale constraints for direct sales

Building hospital-direct coverage is capital-intensive and AMS's limited feet-on-the-street restricts penetration in key metropolitan and tertiary markets, often ceding influence to distributor priorities and purchasing groups. Reliance on distributors can deprioritize AMS products versus larger principals, while slow rollout of clinician education hampers adoption of complex products requiring hands-on training and clinical support.

- High cost of direct hospital coverage

- Limited salesforce limits market penetration

- Distributor influence can deprioritize AMS

- Clinical-education needs slow adoption

Low brand recognition and distributor reliance slow tenders; wound sales ~50% in $20.2bn market

Lower brand recognition and limited hospital-direct coverage slow tender wins and extend sales cycles against larger medtech incumbents.

Heavy reliance on distributors raises margin leakage and control risk, constraining pricing power amid product commoditization.

Wound/surgical remains c.50% of Group sales, facing tender price pressure in a $20.2bn global wound market (2023); evidence programs add 12–24 months and multi-million-dollar costs.

| Weakness | Impact | Key metric |

|---|---|---|

| Revenue concentration | High sensitivity to market shifts | c.50% sales |

| Market pressure | Margin erosion | $20.2bn wound market (2023) |

| Evidence/regulatory | Delayed launches | 12–24 months; multi-million-$ trials |

Preview Before You Purchase

Advanced Medical Solutions Group SWOT Analysis

This is a real excerpt from the complete Advanced Medical Solutions Group SWOT analysis you'll receive upon purchase. The preview below is taken directly from the full report—no placeholders or samples. Buy now to unlock the full, editable, professional-quality document ready for use.