Adris grupa d.d. Pref. Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

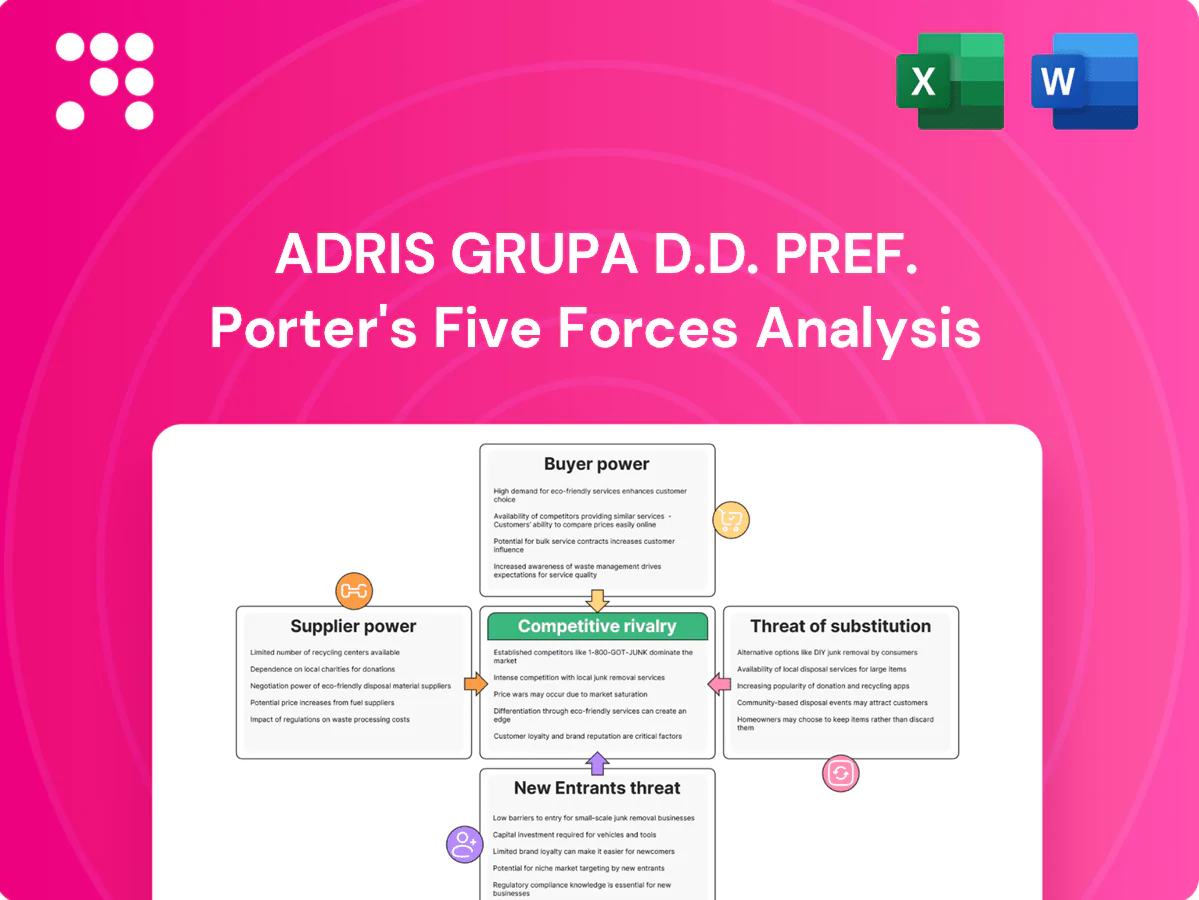

Adris grupa d.d. Pref. faces moderate buyer power and supplier concentration alongside niche rivalries in Croatian diversified sectors, with regulatory shifts and brand strength shaping competitive edges. Threats from new entrants and substitutes are tempered by scale and distribution networks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Seasonal labor tightness

Adriatic tourism’s reliance on seasonal staff means tight labor markets push up wage demands and constrain scheduling, especially after Croatia recorded roughly 20 million tourist arrivals in 2023. Limited local talent and staff housing shortages give labor suppliers leverage, raising recruitment costs for operators like Adris. Post-peak seasonality hampers retention and training economies, while a strong employer brand and multi-property staffing pools help mitigate wage spikes and shortages.

Aquafeed and fingerling dependence

Bargaining power of suppliers is high for Adris Grupa's aquaculture because feed and fingerlings are supplied by a few specialized firms; in 2024 input price volatility persisted, with fishmeal and soy shocks passing through to margins with multi-month lags. Strict biosecurity and certification restrict supplier switchability. Long-term purchase contracts and partial vertical integration (hatcheries) reduce, but do not eliminate, exposure.

Energy and utilities exposure

Hotels, processing plants and cold chains in Adris are highly energy-intensive, exposing the group to concentrated regional utilities—HEP controls around 90% of Croatian generation—giving suppliers strong leverage.

Volatile power and fuel costs (Croatia day-ahead averaged roughly €70/MWh in 2024) amplify risk; hedging and efficiency capex reduce but do not remove exposure.

Long‑term renewable PPAs and access to the Krk LNG terminal (≈2.6 bcm capacity) can stabilize pricing where policy permits.

Reinsurance and IT vendors

Insurance operations at Adris grupa d.d. Pref. rely heavily on reinsurers and specialized IT platforms; reinsurance market cycles and catastrophe-driven hardening can materially raise ceding costs, while vendor lock-in for core policy/admin systems increases switching costs and ongoing vendor bargaining power.

- Reinsurance dependence

- Catastrophe-driven pricing pressure

- Vendor lock-in raises switching costs

- Multi-panel reinsurers and modular tech reduce supplier power

Facilities and F&B procurement

Premium positioning at Adris grupa’s hospitality units demands consistent high-quality linens, premium F&B and maintenance inputs; niche suppliers therefore carry pricing power, but centralized, scale procurement typically improves terms—McKinsey estimates procurement consolidation can reduce COGS 5–15%—while local sourcing boosts resilience and brand value, often cutting lead times up to 30%.

Supplier power elevated: 20M tourists; energy €70/MWh

Supplier power for Adris Grupa is elevated: seasonal labor shortages after ~20M tourist arrivals (2023) push wages; aquaculture feed/fingerling supply is concentrated with input shocks in 2024; energy exposure is high (HEP ≈90% gen, Croatia day‑ahead ≈€70/MWh 2024); reinsurance cycles raise insurance ceding costs.

| Node | Key metric |

|---|---|

| Tourism labor | 20M arrivals (2023) |

| Energy | HEP ≈90% gen; €70/MWh (2024) |

| Aquaculture | Concentrated feed suppliers; input volatility 2024 |

| Insurance | Reinsurance hardening 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Adris grupa d.d. Pref. uncovering competitive drivers, buyer/supplier leverage, entry barriers, substitute threats, and strategic vulnerabilities to inform investor and management decisions.

Concise Porter's Five Forces for Adris grupa d.d.—one-sheet clarity that pinpoints supplier, buyer, competitor, entrant and regulatory pressures to relieve strategic blind spots. Ready to drop into decks for faster, confident decision-making.

Customers Bargaining Power

OTAs and meta-search transparency

OTAs and meta-search engines let guests compare prices instantly, increasing price sensitivity and booking churn. Commission structures, typically 15–25% for major OTAs in 2024, compress hotel margins and give platforms negotiating leverage. Strengthening direct-booking channels (website, CRM) can rebalance power by lowering distribution costs. Loyalty programs and bundled experiences reduce pure price comparisons and raise lifetime value.

Corporate and group insurance clients

Larger corporate buyers and brokers push hard on rates and coverage, with tender-based renewals used in over 60% of group placements, elevating switching ease and enabling data-driven benchmarking that compresses margins by ~5-10% on average. Broad cross-sell suites at Adris-owned Croatia osiguranje can raise retention by 8-12%, yet service quality and claims speed remain the primary differentiators for renewals and pricing.

Retailers and HORECA for fish

Large retail chains and HORECA buyers exert significant scale-driven bargaining power, with the top three Croatian retailers capturing roughly 60% of grocery sales in 2024, pressuring margins on fish products. Private-label and multi-sourcing options—private-label penetration near 30% in many fish categories—raise buyer leverage. Certifications and end-to-end traceability allow premiums of 5-15% for certified lots. Long-term volume agreements (commonly 3–5 years) stabilize volumes but compress prices during downturns.

Leisure travelers’ discretionary spend

Holidaymakers can defer, downgrade or switch destinations, raising price elasticity; UNWTO reported international arrivals at about 95% of 2019 levels in 2024, amplifying demand sensitivity for Adris’s leisure hotels. Macroeconomic swings compress booking windows (average lead time ~25–30 days in 2024) and lower ADR acceptance, while bundled packages and unique Croatian coast locations reduce pushback; flexible cancellation policies boost conversion.

- Elasticity: high — leisure share dominant in 2024 demand

- Booking window: ~25–30 days (2024)

- ADR sensitivity: elevated during downturns

- Mitigants: bundles, unique locations, flexible policies

SMEs and household policyholders

SMEs and household policyholders now compare offers online and via brokers, with 52% of buyers in 2024 using digital comparison tools, increasing price transparency and bargaining power; churn rises when competitors offer temporary discounts. Simpler products and fast digital claims processing improve retention, while multi-policy discounts materially reduce switching incentives.

- Digital comparison: 52% (2024)

- Churn sensitivity: higher with discounting

- Retention drivers: product simplicity, digital claims

- Switching cost: multi-policy discounts

OTAs 15–25% and 52% digital comparison raise churn; tenders >60% press margins

OTAs drive price sensitivity with commissions of 15–25% (2024), boosting churn. Corporate tenders (>60% group placements) compress margins ~5–10%. Top3 retailers hold ~60% grocery share; private-label ~30% and certified premiums 5–15%. Digital comparison use 52% and booking lead time ~25–30 days raise bargaining leverage.

| Metric | 2024 | Effect |

|---|---|---|

| OTA commission | 15–25% | Margin pressure |

| Corporate tenders | >60% | Rate compression 5–10% |

| Digital comparison | 52% | Higher churn |

Preview the Actual Deliverable

Adris grupa d.d. Pref. Porter's Five Forces Analysis

This preview shows the complete Porter’s Five Forces analysis for Adris grupa d.d. Pref., including industry context, competitive dynamics, bargaining power assessments, and strategic implications. The document displayed here is the exact file you’ll receive upon purchase. It is fully formatted and ready to use. No placeholders or samples—instant download after payment.

Go Beyond the Preview—Access the Full Strategic Report

Adris grupa d.d. Pref. faces moderate buyer power and supplier concentration alongside niche rivalries in Croatian diversified sectors, with regulatory shifts and brand strength shaping competitive edges. Threats from new entrants and substitutes are tempered by scale and distribution networks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Seasonal labor tightness

Adriatic tourism’s reliance on seasonal staff means tight labor markets push up wage demands and constrain scheduling, especially after Croatia recorded roughly 20 million tourist arrivals in 2023. Limited local talent and staff housing shortages give labor suppliers leverage, raising recruitment costs for operators like Adris. Post-peak seasonality hampers retention and training economies, while a strong employer brand and multi-property staffing pools help mitigate wage spikes and shortages.

Aquafeed and fingerling dependence

Bargaining power of suppliers is high for Adris Grupa's aquaculture because feed and fingerlings are supplied by a few specialized firms; in 2024 input price volatility persisted, with fishmeal and soy shocks passing through to margins with multi-month lags. Strict biosecurity and certification restrict supplier switchability. Long-term purchase contracts and partial vertical integration (hatcheries) reduce, but do not eliminate, exposure.

Energy and utilities exposure

Hotels, processing plants and cold chains in Adris are highly energy-intensive, exposing the group to concentrated regional utilities—HEP controls around 90% of Croatian generation—giving suppliers strong leverage.

Volatile power and fuel costs (Croatia day-ahead averaged roughly €70/MWh in 2024) amplify risk; hedging and efficiency capex reduce but do not remove exposure.

Long‑term renewable PPAs and access to the Krk LNG terminal (≈2.6 bcm capacity) can stabilize pricing where policy permits.

Reinsurance and IT vendors

Insurance operations at Adris grupa d.d. Pref. rely heavily on reinsurers and specialized IT platforms; reinsurance market cycles and catastrophe-driven hardening can materially raise ceding costs, while vendor lock-in for core policy/admin systems increases switching costs and ongoing vendor bargaining power.

- Reinsurance dependence

- Catastrophe-driven pricing pressure

- Vendor lock-in raises switching costs

- Multi-panel reinsurers and modular tech reduce supplier power

Facilities and F&B procurement

Premium positioning at Adris grupa’s hospitality units demands consistent high-quality linens, premium F&B and maintenance inputs; niche suppliers therefore carry pricing power, but centralized, scale procurement typically improves terms—McKinsey estimates procurement consolidation can reduce COGS 5–15%—while local sourcing boosts resilience and brand value, often cutting lead times up to 30%.

Supplier power elevated: 20M tourists; energy €70/MWh

Supplier power for Adris Grupa is elevated: seasonal labor shortages after ~20M tourist arrivals (2023) push wages; aquaculture feed/fingerling supply is concentrated with input shocks in 2024; energy exposure is high (HEP ≈90% gen, Croatia day‑ahead ≈€70/MWh 2024); reinsurance cycles raise insurance ceding costs.

| Node | Key metric |

|---|---|

| Tourism labor | 20M arrivals (2023) |

| Energy | HEP ≈90% gen; €70/MWh (2024) |

| Aquaculture | Concentrated feed suppliers; input volatility 2024 |

| Insurance | Reinsurance hardening 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Adris grupa d.d. Pref. uncovering competitive drivers, buyer/supplier leverage, entry barriers, substitute threats, and strategic vulnerabilities to inform investor and management decisions.

Concise Porter's Five Forces for Adris grupa d.d.—one-sheet clarity that pinpoints supplier, buyer, competitor, entrant and regulatory pressures to relieve strategic blind spots. Ready to drop into decks for faster, confident decision-making.

Customers Bargaining Power

OTAs and meta-search transparency

OTAs and meta-search engines let guests compare prices instantly, increasing price sensitivity and booking churn. Commission structures, typically 15–25% for major OTAs in 2024, compress hotel margins and give platforms negotiating leverage. Strengthening direct-booking channels (website, CRM) can rebalance power by lowering distribution costs. Loyalty programs and bundled experiences reduce pure price comparisons and raise lifetime value.

Corporate and group insurance clients

Larger corporate buyers and brokers push hard on rates and coverage, with tender-based renewals used in over 60% of group placements, elevating switching ease and enabling data-driven benchmarking that compresses margins by ~5-10% on average. Broad cross-sell suites at Adris-owned Croatia osiguranje can raise retention by 8-12%, yet service quality and claims speed remain the primary differentiators for renewals and pricing.

Retailers and HORECA for fish

Large retail chains and HORECA buyers exert significant scale-driven bargaining power, with the top three Croatian retailers capturing roughly 60% of grocery sales in 2024, pressuring margins on fish products. Private-label and multi-sourcing options—private-label penetration near 30% in many fish categories—raise buyer leverage. Certifications and end-to-end traceability allow premiums of 5-15% for certified lots. Long-term volume agreements (commonly 3–5 years) stabilize volumes but compress prices during downturns.

Leisure travelers’ discretionary spend

Holidaymakers can defer, downgrade or switch destinations, raising price elasticity; UNWTO reported international arrivals at about 95% of 2019 levels in 2024, amplifying demand sensitivity for Adris’s leisure hotels. Macroeconomic swings compress booking windows (average lead time ~25–30 days in 2024) and lower ADR acceptance, while bundled packages and unique Croatian coast locations reduce pushback; flexible cancellation policies boost conversion.

- Elasticity: high — leisure share dominant in 2024 demand

- Booking window: ~25–30 days (2024)

- ADR sensitivity: elevated during downturns

- Mitigants: bundles, unique locations, flexible policies

SMEs and household policyholders

SMEs and household policyholders now compare offers online and via brokers, with 52% of buyers in 2024 using digital comparison tools, increasing price transparency and bargaining power; churn rises when competitors offer temporary discounts. Simpler products and fast digital claims processing improve retention, while multi-policy discounts materially reduce switching incentives.

- Digital comparison: 52% (2024)

- Churn sensitivity: higher with discounting

- Retention drivers: product simplicity, digital claims

- Switching cost: multi-policy discounts

OTAs 15–25% and 52% digital comparison raise churn; tenders >60% press margins

OTAs drive price sensitivity with commissions of 15–25% (2024), boosting churn. Corporate tenders (>60% group placements) compress margins ~5–10%. Top3 retailers hold ~60% grocery share; private-label ~30% and certified premiums 5–15%. Digital comparison use 52% and booking lead time ~25–30 days raise bargaining leverage.

| Metric | 2024 | Effect |

|---|---|---|

| OTA commission | 15–25% | Margin pressure |

| Corporate tenders | >60% | Rate compression 5–10% |

| Digital comparison | 52% | Higher churn |

Preview the Actual Deliverable

Adris grupa d.d. Pref. Porter's Five Forces Analysis

This preview shows the complete Porter’s Five Forces analysis for Adris grupa d.d. Pref., including industry context, competitive dynamics, bargaining power assessments, and strategic implications. The document displayed here is the exact file you’ll receive upon purchase. It is fully formatted and ready to use. No placeholders or samples—instant download after payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Adris grupa d.d. Pref. faces moderate buyer power and supplier concentration alongside niche rivalries in Croatian diversified sectors, with regulatory shifts and brand strength shaping competitive edges. Threats from new entrants and substitutes are tempered by scale and distribution networks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Seasonal labor tightness

Adriatic tourism’s reliance on seasonal staff means tight labor markets push up wage demands and constrain scheduling, especially after Croatia recorded roughly 20 million tourist arrivals in 2023. Limited local talent and staff housing shortages give labor suppliers leverage, raising recruitment costs for operators like Adris. Post-peak seasonality hampers retention and training economies, while a strong employer brand and multi-property staffing pools help mitigate wage spikes and shortages.

Aquafeed and fingerling dependence

Bargaining power of suppliers is high for Adris Grupa's aquaculture because feed and fingerlings are supplied by a few specialized firms; in 2024 input price volatility persisted, with fishmeal and soy shocks passing through to margins with multi-month lags. Strict biosecurity and certification restrict supplier switchability. Long-term purchase contracts and partial vertical integration (hatcheries) reduce, but do not eliminate, exposure.

Energy and utilities exposure

Hotels, processing plants and cold chains in Adris are highly energy-intensive, exposing the group to concentrated regional utilities—HEP controls around 90% of Croatian generation—giving suppliers strong leverage.

Volatile power and fuel costs (Croatia day-ahead averaged roughly €70/MWh in 2024) amplify risk; hedging and efficiency capex reduce but do not remove exposure.

Long‑term renewable PPAs and access to the Krk LNG terminal (≈2.6 bcm capacity) can stabilize pricing where policy permits.

Reinsurance and IT vendors

Insurance operations at Adris grupa d.d. Pref. rely heavily on reinsurers and specialized IT platforms; reinsurance market cycles and catastrophe-driven hardening can materially raise ceding costs, while vendor lock-in for core policy/admin systems increases switching costs and ongoing vendor bargaining power.

- Reinsurance dependence

- Catastrophe-driven pricing pressure

- Vendor lock-in raises switching costs

- Multi-panel reinsurers and modular tech reduce supplier power

Facilities and F&B procurement

Premium positioning at Adris grupa’s hospitality units demands consistent high-quality linens, premium F&B and maintenance inputs; niche suppliers therefore carry pricing power, but centralized, scale procurement typically improves terms—McKinsey estimates procurement consolidation can reduce COGS 5–15%—while local sourcing boosts resilience and brand value, often cutting lead times up to 30%.

Supplier power elevated: 20M tourists; energy €70/MWh

Supplier power for Adris Grupa is elevated: seasonal labor shortages after ~20M tourist arrivals (2023) push wages; aquaculture feed/fingerling supply is concentrated with input shocks in 2024; energy exposure is high (HEP ≈90% gen, Croatia day‑ahead ≈€70/MWh 2024); reinsurance cycles raise insurance ceding costs.

| Node | Key metric |

|---|---|

| Tourism labor | 20M arrivals (2023) |

| Energy | HEP ≈90% gen; €70/MWh (2024) |

| Aquaculture | Concentrated feed suppliers; input volatility 2024 |

| Insurance | Reinsurance hardening 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Adris grupa d.d. Pref. uncovering competitive drivers, buyer/supplier leverage, entry barriers, substitute threats, and strategic vulnerabilities to inform investor and management decisions.

Concise Porter's Five Forces for Adris grupa d.d.—one-sheet clarity that pinpoints supplier, buyer, competitor, entrant and regulatory pressures to relieve strategic blind spots. Ready to drop into decks for faster, confident decision-making.

Customers Bargaining Power

OTAs and meta-search transparency

OTAs and meta-search engines let guests compare prices instantly, increasing price sensitivity and booking churn. Commission structures, typically 15–25% for major OTAs in 2024, compress hotel margins and give platforms negotiating leverage. Strengthening direct-booking channels (website, CRM) can rebalance power by lowering distribution costs. Loyalty programs and bundled experiences reduce pure price comparisons and raise lifetime value.

Corporate and group insurance clients

Larger corporate buyers and brokers push hard on rates and coverage, with tender-based renewals used in over 60% of group placements, elevating switching ease and enabling data-driven benchmarking that compresses margins by ~5-10% on average. Broad cross-sell suites at Adris-owned Croatia osiguranje can raise retention by 8-12%, yet service quality and claims speed remain the primary differentiators for renewals and pricing.

Retailers and HORECA for fish

Large retail chains and HORECA buyers exert significant scale-driven bargaining power, with the top three Croatian retailers capturing roughly 60% of grocery sales in 2024, pressuring margins on fish products. Private-label and multi-sourcing options—private-label penetration near 30% in many fish categories—raise buyer leverage. Certifications and end-to-end traceability allow premiums of 5-15% for certified lots. Long-term volume agreements (commonly 3–5 years) stabilize volumes but compress prices during downturns.

Leisure travelers’ discretionary spend

Holidaymakers can defer, downgrade or switch destinations, raising price elasticity; UNWTO reported international arrivals at about 95% of 2019 levels in 2024, amplifying demand sensitivity for Adris’s leisure hotels. Macroeconomic swings compress booking windows (average lead time ~25–30 days in 2024) and lower ADR acceptance, while bundled packages and unique Croatian coast locations reduce pushback; flexible cancellation policies boost conversion.

- Elasticity: high — leisure share dominant in 2024 demand

- Booking window: ~25–30 days (2024)

- ADR sensitivity: elevated during downturns

- Mitigants: bundles, unique locations, flexible policies

SMEs and household policyholders

SMEs and household policyholders now compare offers online and via brokers, with 52% of buyers in 2024 using digital comparison tools, increasing price transparency and bargaining power; churn rises when competitors offer temporary discounts. Simpler products and fast digital claims processing improve retention, while multi-policy discounts materially reduce switching incentives.

- Digital comparison: 52% (2024)

- Churn sensitivity: higher with discounting

- Retention drivers: product simplicity, digital claims

- Switching cost: multi-policy discounts

OTAs 15–25% and 52% digital comparison raise churn; tenders >60% press margins

OTAs drive price sensitivity with commissions of 15–25% (2024), boosting churn. Corporate tenders (>60% group placements) compress margins ~5–10%. Top3 retailers hold ~60% grocery share; private-label ~30% and certified premiums 5–15%. Digital comparison use 52% and booking lead time ~25–30 days raise bargaining leverage.

| Metric | 2024 | Effect |

|---|---|---|

| OTA commission | 15–25% | Margin pressure |

| Corporate tenders | >60% | Rate compression 5–10% |

| Digital comparison | 52% | Higher churn |

Preview the Actual Deliverable

Adris grupa d.d. Pref. Porter's Five Forces Analysis

This preview shows the complete Porter’s Five Forces analysis for Adris grupa d.d. Pref., including industry context, competitive dynamics, bargaining power assessments, and strategic implications. The document displayed here is the exact file you’ll receive upon purchase. It is fully formatted and ready to use. No placeholders or samples—instant download after payment.