Adven Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

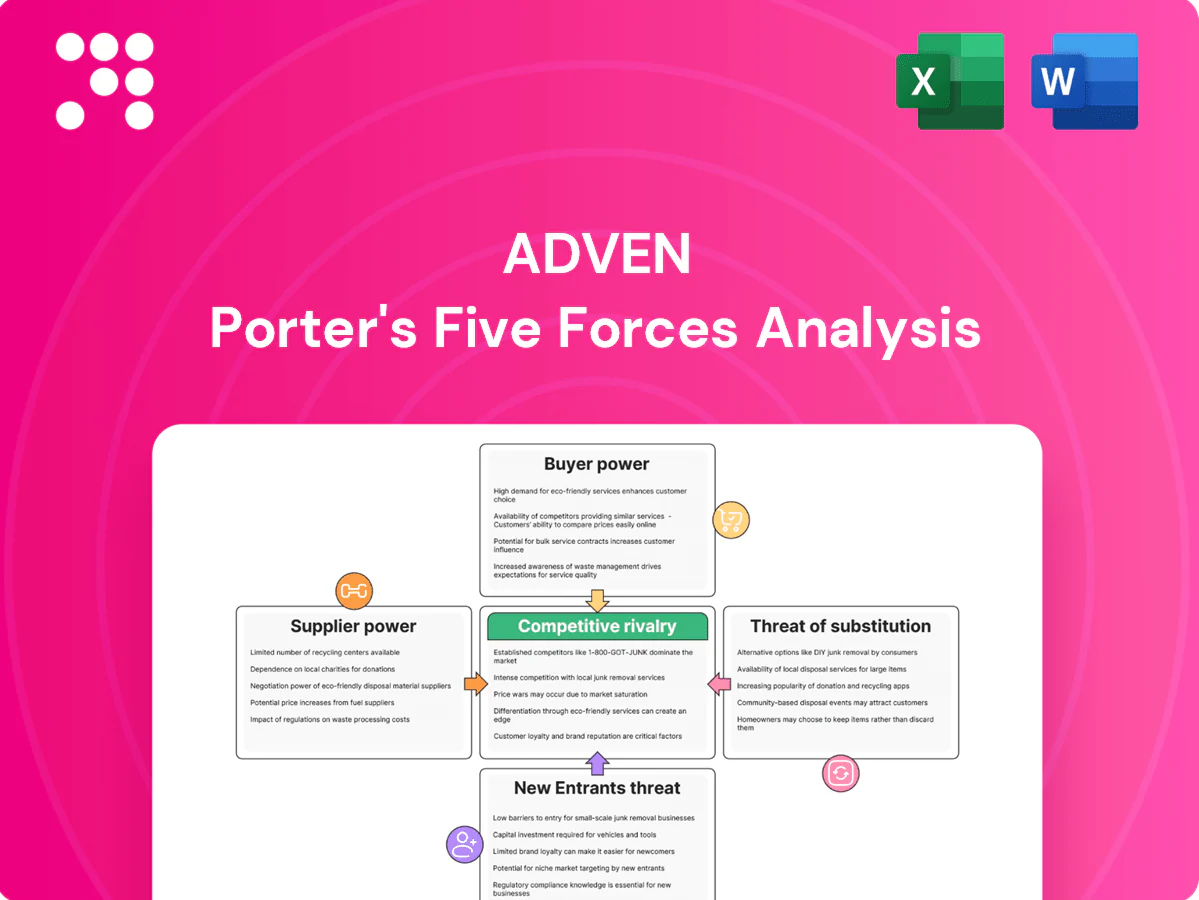

Adven’s Porter's Five Forces snapshot highlights key pressures shaping its competitive landscape—supplier leverage, buyer power, rivalry intensity, threat of entrants, and substitutes. This concise view uncovers where Adven holds advantages and where risks lurk. Ready for actionable strategy? Purchase the full report for force-by-force ratings, visuals, and tailored implications to inform investment or strategic moves.

Suppliers Bargaining Power

Concentrated fuel and tech OEM base

Adven relies on fuel suppliers (biomass, gas) and specialized OEMs for boilers, CHP and heat pumps, and concentration among critical equipment vendors gives those suppliers potential pricing and lead-time leverage.

Dual-sourcing, standardized technical specs and longer-term service contracts reduce supplier bargaining power and procurement risk.

Local biomass markets are often fragmented and regional, which softens supplier clout compared with global gas/OEM supply chains.

Long-term input contracts and indexation

Long-duration input contracts stabilize baseline costs but indexation to commodities and inflation can shift spike risk to Adven, seen when EU carbon prices exceeded €100/t in 2024 and power markets spiked. Clear CO2 and power-price pass-through clauses are vital to avoid margin erosion. Negotiation strength depends on Adven’s aggregated volume and multi-site contracting scale.

Logistics and seasonal constraints

Fuel logistics—biomass moisture levels of 30–50% and long transport distances (often >100 km) tighten supply and raise costs, especially during winter peaks when sourcing becomes harder. Seasonal demand during cold months increases supplier bargaining power as outages or quality shortfalls have immediate effects. Investments in on-site storage to cover several weeks of demand reduce exposure. Diversifying into waste heat and electricity-driven technologies cuts fuel reliance and weakens supplier leverage.

Technological lock-in and spare parts

- OEM premiums: 15-30%

- Service share: 10-25% of lifecycle cost

- Response SLAs: 24-72 hours

- Open design reduces switching costs

Regulatory and sustainability criteria

Regulatory and sustainability criteria narrow eligible suppliers for Adven as ISCC and RSB certification requirements raise qualification costs and concentrate approved vendors; EU RED III raised the 2030 renewables target to 42.5% (2023), accelerating supplier compliance pressure. Green mandates expand alternatives — recovered heat and biogas — shifting bargaining leverage back toward buyers as supplier audits become routine.

- Fewer certified suppliers — higher entry costs

- EU RED III 42.5% by 2030 — compliance pressure

- Alternatives (recovered heat, biogas) expand supply base

- Supplier audits rebalance negotiation power

Resilient procurement: 15-30% OEM premiums, 10-25% services; EU carbon > €100/t

Supplier power is moderate: concentrated OEMs and gas suppliers can demand 15–30% equipment premiums and 10–25% service shares, but Adven’s scale, dual-sourcing and long contracts lower risk. Biomass logistics (moisture 30–50%, transport >100 km) and seasonal peaks raise short-term leverage. Regulatory certs narrow vendors, while alternatives and pass-through clauses offset margin exposure (EU carbon > €100/t in 2024).

| Metric | 2024/value |

|---|---|

| OEM premium | 15–30% |

| Service share | 10–25% |

| EU carbon price | > €100/t |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Adven, with detailed appraisal of supplier and buyer power, substitutes, and disruptive threats. Fully editable for reports or investor materials.

Adven’s Porter Five Forces one-sheet maps competitive pressure visually and lets you tweak force intensity for scenario analysis—ideal for fast strategic decisions and slide-ready reports.

Customers Bargaining Power

Large industrial and municipal anchors

Adven’s large industrial and municipal anchors bring strong bargaining power because they use dedicated procurement teams and tight budget controls; in 2024 increased public tendering amplified competitive pressure. Their high-volume demand and public procurement processes push pricing and contract terms, while multi-year agreements reduce churn yet concentrate negotiating leverage at signing. Peer referenceability materially shapes commercial terms and renewal leverage.

High switching costs and site integration

Deep physical integration of plants and networks creates high switching barriers, with 2024 industry surveys reporting over 60% of operators citing integration complexity as a top deterrent to supplier changes. Decommissioning and re-specification expenses — commonly running into multi-million-dollar projects — deter rapid exits and blunt day-2–3 price pressure. Performance SLAs and availability guarantees therefore remain the primary negotiation levers for customers.

Ability to self-build as BATNA

Many customers can in-source energy plants using EPCs, and a 2024 industry survey found 38% of large industrial buyers consider self-build a credible BATNA, strengthening their bargaining power. Adven counters by offering risk transfer, lifecycle optimization and financing packages that shift capex and execution risk. TCO analyses and decarbonization roadmaps—showing lifecycle savings up to 20%—erode the attractiveness of the self-build alternative.

Price transparency and index-linked tariffs

Energy market price transparency gives buyers visibility into fuel and power costs, increasing customer leverage and making Adven’s margins sensitive to market moves; EU ETS carbon averaged about €85/tonne in 2024, emphasising carbon pass-through importance. Index-linked tariffs reduce upside for Adven when wholesale spikes occur, while efficiency-sharing and carbon performance fees align incentives and clear pass-through rules limit disputes.

- Visible wholesale pricing increases buyer bargaining power

- Index-linked contracts cap Adven upside

- Efficiency-sharing and carbon fees align incentives

- Transparent pass-through lowers contractual disputes

Demand elasticity and multi-utility bundling

Industrial customers increasingly flex steam/heat demand or shift to electrification, compressing short-term tariffs and forcing longer-term term tradeoffs; electrification investments grew markedly in 2024, tightening supplier negotiating power.

- Bundling: heating+cooling+steam+water raises stickiness and reduces churn

- Portfolio deals: trade ~5–15% lower price for scale and 5–15‑yr tenure

- Co‑invest: lowers headline tariff in exchange for extended term

Large buyers gain leverage as 2024 procurement, integration and €85/t ETS pressure prices

Adven’s large industrial and municipal customers hold strong bargaining power via dedicated procurement, volume and multi‑year contracting; 2024 public procurement intensity increased negotiation leverage. High integration raises switching costs (2024 survey: 60% cite integration as top deterrent) but 38% of large buyers view self‑build as credible. Transparent markets and EU ETS at ~€85/t in 2024 increase pass‑through disputes and price sensitivity.

| Metric | 2024 value |

|---|---|

| Integration deterrent | 60% |

| Buyers citing self‑build BATNA | 38% |

| EU ETS carbon price | ~€85/t |

Preview Before You Purchase

Adven Porter's Five Forces Analysis

This preview shows the exact Adven Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download and use. What you see is the deliverable you'll get upon payment.

A Must-Have Tool for Decision-Makers

Adven’s Porter's Five Forces snapshot highlights key pressures shaping its competitive landscape—supplier leverage, buyer power, rivalry intensity, threat of entrants, and substitutes. This concise view uncovers where Adven holds advantages and where risks lurk. Ready for actionable strategy? Purchase the full report for force-by-force ratings, visuals, and tailored implications to inform investment or strategic moves.

Suppliers Bargaining Power

Concentrated fuel and tech OEM base

Adven relies on fuel suppliers (biomass, gas) and specialized OEMs for boilers, CHP and heat pumps, and concentration among critical equipment vendors gives those suppliers potential pricing and lead-time leverage.

Dual-sourcing, standardized technical specs and longer-term service contracts reduce supplier bargaining power and procurement risk.

Local biomass markets are often fragmented and regional, which softens supplier clout compared with global gas/OEM supply chains.

Long-term input contracts and indexation

Long-duration input contracts stabilize baseline costs but indexation to commodities and inflation can shift spike risk to Adven, seen when EU carbon prices exceeded €100/t in 2024 and power markets spiked. Clear CO2 and power-price pass-through clauses are vital to avoid margin erosion. Negotiation strength depends on Adven’s aggregated volume and multi-site contracting scale.

Logistics and seasonal constraints

Fuel logistics—biomass moisture levels of 30–50% and long transport distances (often >100 km) tighten supply and raise costs, especially during winter peaks when sourcing becomes harder. Seasonal demand during cold months increases supplier bargaining power as outages or quality shortfalls have immediate effects. Investments in on-site storage to cover several weeks of demand reduce exposure. Diversifying into waste heat and electricity-driven technologies cuts fuel reliance and weakens supplier leverage.

Technological lock-in and spare parts

- OEM premiums: 15-30%

- Service share: 10-25% of lifecycle cost

- Response SLAs: 24-72 hours

- Open design reduces switching costs

Regulatory and sustainability criteria

Regulatory and sustainability criteria narrow eligible suppliers for Adven as ISCC and RSB certification requirements raise qualification costs and concentrate approved vendors; EU RED III raised the 2030 renewables target to 42.5% (2023), accelerating supplier compliance pressure. Green mandates expand alternatives — recovered heat and biogas — shifting bargaining leverage back toward buyers as supplier audits become routine.

- Fewer certified suppliers — higher entry costs

- EU RED III 42.5% by 2030 — compliance pressure

- Alternatives (recovered heat, biogas) expand supply base

- Supplier audits rebalance negotiation power

Resilient procurement: 15-30% OEM premiums, 10-25% services; EU carbon > €100/t

Supplier power is moderate: concentrated OEMs and gas suppliers can demand 15–30% equipment premiums and 10–25% service shares, but Adven’s scale, dual-sourcing and long contracts lower risk. Biomass logistics (moisture 30–50%, transport >100 km) and seasonal peaks raise short-term leverage. Regulatory certs narrow vendors, while alternatives and pass-through clauses offset margin exposure (EU carbon > €100/t in 2024).

| Metric | 2024/value |

|---|---|

| OEM premium | 15–30% |

| Service share | 10–25% |

| EU carbon price | > €100/t |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Adven, with detailed appraisal of supplier and buyer power, substitutes, and disruptive threats. Fully editable for reports or investor materials.

Adven’s Porter Five Forces one-sheet maps competitive pressure visually and lets you tweak force intensity for scenario analysis—ideal for fast strategic decisions and slide-ready reports.

Customers Bargaining Power

Large industrial and municipal anchors

Adven’s large industrial and municipal anchors bring strong bargaining power because they use dedicated procurement teams and tight budget controls; in 2024 increased public tendering amplified competitive pressure. Their high-volume demand and public procurement processes push pricing and contract terms, while multi-year agreements reduce churn yet concentrate negotiating leverage at signing. Peer referenceability materially shapes commercial terms and renewal leverage.

High switching costs and site integration

Deep physical integration of plants and networks creates high switching barriers, with 2024 industry surveys reporting over 60% of operators citing integration complexity as a top deterrent to supplier changes. Decommissioning and re-specification expenses — commonly running into multi-million-dollar projects — deter rapid exits and blunt day-2–3 price pressure. Performance SLAs and availability guarantees therefore remain the primary negotiation levers for customers.

Ability to self-build as BATNA

Many customers can in-source energy plants using EPCs, and a 2024 industry survey found 38% of large industrial buyers consider self-build a credible BATNA, strengthening their bargaining power. Adven counters by offering risk transfer, lifecycle optimization and financing packages that shift capex and execution risk. TCO analyses and decarbonization roadmaps—showing lifecycle savings up to 20%—erode the attractiveness of the self-build alternative.

Price transparency and index-linked tariffs

Energy market price transparency gives buyers visibility into fuel and power costs, increasing customer leverage and making Adven’s margins sensitive to market moves; EU ETS carbon averaged about €85/tonne in 2024, emphasising carbon pass-through importance. Index-linked tariffs reduce upside for Adven when wholesale spikes occur, while efficiency-sharing and carbon performance fees align incentives and clear pass-through rules limit disputes.

- Visible wholesale pricing increases buyer bargaining power

- Index-linked contracts cap Adven upside

- Efficiency-sharing and carbon fees align incentives

- Transparent pass-through lowers contractual disputes

Demand elasticity and multi-utility bundling

Industrial customers increasingly flex steam/heat demand or shift to electrification, compressing short-term tariffs and forcing longer-term term tradeoffs; electrification investments grew markedly in 2024, tightening supplier negotiating power.

- Bundling: heating+cooling+steam+water raises stickiness and reduces churn

- Portfolio deals: trade ~5–15% lower price for scale and 5–15‑yr tenure

- Co‑invest: lowers headline tariff in exchange for extended term

Large buyers gain leverage as 2024 procurement, integration and €85/t ETS pressure prices

Adven’s large industrial and municipal customers hold strong bargaining power via dedicated procurement, volume and multi‑year contracting; 2024 public procurement intensity increased negotiation leverage. High integration raises switching costs (2024 survey: 60% cite integration as top deterrent) but 38% of large buyers view self‑build as credible. Transparent markets and EU ETS at ~€85/t in 2024 increase pass‑through disputes and price sensitivity.

| Metric | 2024 value |

|---|---|

| Integration deterrent | 60% |

| Buyers citing self‑build BATNA | 38% |

| EU ETS carbon price | ~€85/t |

Preview Before You Purchase

Adven Porter's Five Forces Analysis

This preview shows the exact Adven Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download and use. What you see is the deliverable you'll get upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Adven’s Porter's Five Forces snapshot highlights key pressures shaping its competitive landscape—supplier leverage, buyer power, rivalry intensity, threat of entrants, and substitutes. This concise view uncovers where Adven holds advantages and where risks lurk. Ready for actionable strategy? Purchase the full report for force-by-force ratings, visuals, and tailored implications to inform investment or strategic moves.

Suppliers Bargaining Power

Concentrated fuel and tech OEM base

Adven relies on fuel suppliers (biomass, gas) and specialized OEMs for boilers, CHP and heat pumps, and concentration among critical equipment vendors gives those suppliers potential pricing and lead-time leverage.

Dual-sourcing, standardized technical specs and longer-term service contracts reduce supplier bargaining power and procurement risk.

Local biomass markets are often fragmented and regional, which softens supplier clout compared with global gas/OEM supply chains.

Long-term input contracts and indexation

Long-duration input contracts stabilize baseline costs but indexation to commodities and inflation can shift spike risk to Adven, seen when EU carbon prices exceeded €100/t in 2024 and power markets spiked. Clear CO2 and power-price pass-through clauses are vital to avoid margin erosion. Negotiation strength depends on Adven’s aggregated volume and multi-site contracting scale.

Logistics and seasonal constraints

Fuel logistics—biomass moisture levels of 30–50% and long transport distances (often >100 km) tighten supply and raise costs, especially during winter peaks when sourcing becomes harder. Seasonal demand during cold months increases supplier bargaining power as outages or quality shortfalls have immediate effects. Investments in on-site storage to cover several weeks of demand reduce exposure. Diversifying into waste heat and electricity-driven technologies cuts fuel reliance and weakens supplier leverage.

Technological lock-in and spare parts

- OEM premiums: 15-30%

- Service share: 10-25% of lifecycle cost

- Response SLAs: 24-72 hours

- Open design reduces switching costs

Regulatory and sustainability criteria

Regulatory and sustainability criteria narrow eligible suppliers for Adven as ISCC and RSB certification requirements raise qualification costs and concentrate approved vendors; EU RED III raised the 2030 renewables target to 42.5% (2023), accelerating supplier compliance pressure. Green mandates expand alternatives — recovered heat and biogas — shifting bargaining leverage back toward buyers as supplier audits become routine.

- Fewer certified suppliers — higher entry costs

- EU RED III 42.5% by 2030 — compliance pressure

- Alternatives (recovered heat, biogas) expand supply base

- Supplier audits rebalance negotiation power

Resilient procurement: 15-30% OEM premiums, 10-25% services; EU carbon > €100/t

Supplier power is moderate: concentrated OEMs and gas suppliers can demand 15–30% equipment premiums and 10–25% service shares, but Adven’s scale, dual-sourcing and long contracts lower risk. Biomass logistics (moisture 30–50%, transport >100 km) and seasonal peaks raise short-term leverage. Regulatory certs narrow vendors, while alternatives and pass-through clauses offset margin exposure (EU carbon > €100/t in 2024).

| Metric | 2024/value |

|---|---|

| OEM premium | 15–30% |

| Service share | 10–25% |

| EU carbon price | > €100/t |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Adven, with detailed appraisal of supplier and buyer power, substitutes, and disruptive threats. Fully editable for reports or investor materials.

Adven’s Porter Five Forces one-sheet maps competitive pressure visually and lets you tweak force intensity for scenario analysis—ideal for fast strategic decisions and slide-ready reports.

Customers Bargaining Power

Large industrial and municipal anchors

Adven’s large industrial and municipal anchors bring strong bargaining power because they use dedicated procurement teams and tight budget controls; in 2024 increased public tendering amplified competitive pressure. Their high-volume demand and public procurement processes push pricing and contract terms, while multi-year agreements reduce churn yet concentrate negotiating leverage at signing. Peer referenceability materially shapes commercial terms and renewal leverage.

High switching costs and site integration

Deep physical integration of plants and networks creates high switching barriers, with 2024 industry surveys reporting over 60% of operators citing integration complexity as a top deterrent to supplier changes. Decommissioning and re-specification expenses — commonly running into multi-million-dollar projects — deter rapid exits and blunt day-2–3 price pressure. Performance SLAs and availability guarantees therefore remain the primary negotiation levers for customers.

Ability to self-build as BATNA

Many customers can in-source energy plants using EPCs, and a 2024 industry survey found 38% of large industrial buyers consider self-build a credible BATNA, strengthening their bargaining power. Adven counters by offering risk transfer, lifecycle optimization and financing packages that shift capex and execution risk. TCO analyses and decarbonization roadmaps—showing lifecycle savings up to 20%—erode the attractiveness of the self-build alternative.

Price transparency and index-linked tariffs

Energy market price transparency gives buyers visibility into fuel and power costs, increasing customer leverage and making Adven’s margins sensitive to market moves; EU ETS carbon averaged about €85/tonne in 2024, emphasising carbon pass-through importance. Index-linked tariffs reduce upside for Adven when wholesale spikes occur, while efficiency-sharing and carbon performance fees align incentives and clear pass-through rules limit disputes.

- Visible wholesale pricing increases buyer bargaining power

- Index-linked contracts cap Adven upside

- Efficiency-sharing and carbon fees align incentives

- Transparent pass-through lowers contractual disputes

Demand elasticity and multi-utility bundling

Industrial customers increasingly flex steam/heat demand or shift to electrification, compressing short-term tariffs and forcing longer-term term tradeoffs; electrification investments grew markedly in 2024, tightening supplier negotiating power.

- Bundling: heating+cooling+steam+water raises stickiness and reduces churn

- Portfolio deals: trade ~5–15% lower price for scale and 5–15‑yr tenure

- Co‑invest: lowers headline tariff in exchange for extended term

Large buyers gain leverage as 2024 procurement, integration and €85/t ETS pressure prices

Adven’s large industrial and municipal customers hold strong bargaining power via dedicated procurement, volume and multi‑year contracting; 2024 public procurement intensity increased negotiation leverage. High integration raises switching costs (2024 survey: 60% cite integration as top deterrent) but 38% of large buyers view self‑build as credible. Transparent markets and EU ETS at ~€85/t in 2024 increase pass‑through disputes and price sensitivity.

| Metric | 2024 value |

|---|---|

| Integration deterrent | 60% |

| Buyers citing self‑build BATNA | 38% |

| EU ETS carbon price | ~€85/t |

Preview Before You Purchase

Adven Porter's Five Forces Analysis

This preview shows the exact Adven Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written and ready for immediate download and use. What you see is the deliverable you'll get upon payment.