Aeon Porter's Five Forces Analysis

Don't Miss the Bigger Picture

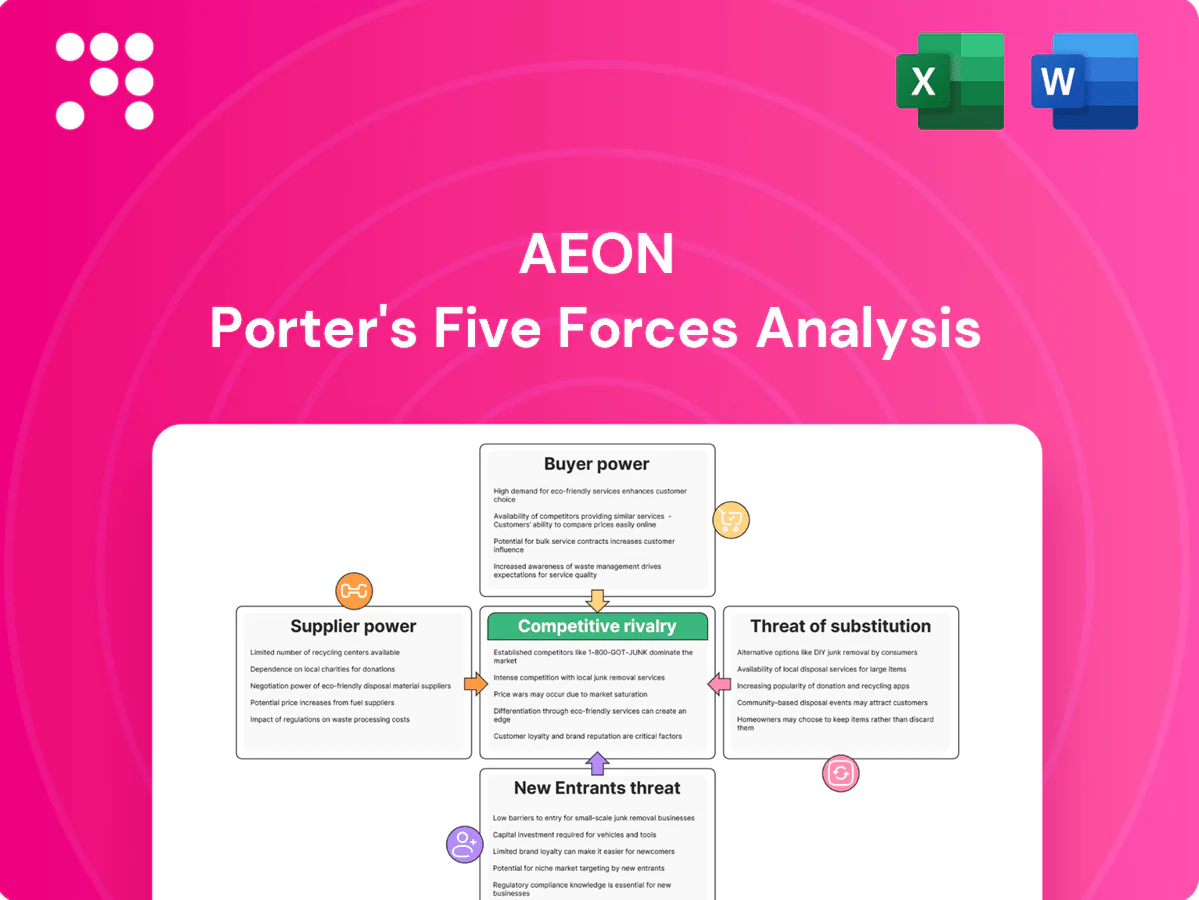

Aeon's Porter's Five Forces Analysis distills competitive pressures—supplier and buyer power, threat of entrants and substitutes, and industry rivalry—into actionable insights, showing where Aeon holds leverage and where market dynamics could compress margins for investors and strategists alike.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aeon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified sourcing base

AEON buys from thousands of FMCG, fresh and specialty suppliers across regions, diluting individual supplier leverage and spreading risk. Centralized procurement and scale—AEON recorded roughly 8 trillion yen in consolidated retail sales in 2024—enable substantial volume discounts. Premium global brands, however, retain negotiating clout on price and terms. Fresh produce seasonality can temporarily raise supplier power during peak shortages.

Private label leverage

Aeon’s strong private label TOPVALU (expanded in 2024) reduces reliance on national brands and anchors negotiations, with private-label penetration in Japanese groceries roughly 18% in 2024, boosting Aeon’s leverage. Backward integration into product development and QA expands switching options and squeezes branded suppliers on price and promo support. However, any TOPVALU quality missteps quickly erode trust, limiting overuse of private-label pressure.

Vertical integration in property

Vertical integration—ownership and operation of malls cuts reliance on third‑party landlords for prime space, strengthening negotiation leverage with fit‑out, facility and services vendors and often reducing external rent exposure versus fully leased peers. However, construction and utilities suppliers retained power during 2024 tight capacity cycles (construction input prices rose ~3% y/y), and high capex intensity increases vulnerability to input cost swings.

Logistics and tech vendors

Advanced DCs, cold chain and proprietary IT platforms create meaningful vendor switching costs for logistics and tech suppliers, while carrier consolidation—top 10 carriers control ~85% of global container capacity in 2024—gives carriers and systems integrators leverage to demand favorable SLAs. AEON’s scale reduces but does not remove dependency risk; multi-sourcing and growing in‑house capabilities buffer operational shocks.

- High switching costs: proprietary DCs, cold chain, IT

- Carrier leverage: top 10 control ~85% (2024)

- AEON scale mitigates but dependency remains

- Multi-sourcing and in‑house ops provide buffers

Regulatory and import exposure

Retail giant scale (~8T JPY) and 18% private-label curb supplier power amid 10% weaker JPY

AEON’s scale (≈8 trillion yen retail sales in 2024) and thousands of suppliers dilute supplier power, aided by TOPVALU private‑label penetration ~18% in 2024. High switching costs from proprietary DCs/cold chain and tech raise vendor leverage, while carrier concentration (top 10 ≈85% global capacity) and regulatory/ESG shifts (FAO index 121 in 2024) increase supplier bargaining. JPY ≈-10% vs USD in 2024 raised import cost pressure.

| Metric | 2024 |

|---|---|

| AEON sales | ≈8 trillion JPY |

| TOPVALU share | ≈18% |

| FAO Food Index | 121 |

| JPY vs USD | ≈-10% |

| Top10 carriers | ≈85% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Aeon that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary and industry data—fully editable for use in investor decks, business plans or internal strategy reports.

Aeon Porter's Five Forces delivers a single-sheet, customizable view that visualizes competitive pressure with an instant radar chart, supports scenario tabs and quick data swaps, and is ready for decks—no macros or finance expertise required.

Customers Bargaining Power

Price transparency and choice

Consumers now compare prices across supermarkets, discounters and e‑commerce instantly, with global online grocery penetration rising to about 8% in 2024, intensifying transparency. Low switching costs on staples raise buyer leverage, especially as frequent promotions train 40–60% of shoppers to wait for deals. Omni‑channel options further accelerate comparison shopping and price sensitivity.

Loyalty ecosystems

AEON’s loyalty ecosystem — over 25 million cardholders in 2024 — raises switching costs via AEON Card, WAON e-money and finance products, enabling data-driven personalization and bundled rewards that blunt buyer leverage; however if rivals replicate rewards the bargaining power shifts back to customers, while strict 2024 data-privacy expectations force more transparent, opt-in program designs.

Quality and freshness expectations

Japanese consumers demand high quality, safety and freshness and punish lapses quickly, forcing AEON—Japan's largest retailer—to impose tighter specs and supplier monitoring that raise procurement and compliance costs; AEON Group reported approximately ¥8.7 trillion in revenue in FY2024. Buyers can trade up or down across formats based on perceived value, and brand reputation constrains AEON’s pricing power.

Corporate tenants and merchants

Mall tenants negotiate rents, fit‑out contributions and marketing support, intensifying in soft demand; anchor tenants exert outsized leverage on terms while AEON counters with footfall, shopper analytics and mixed‑use curation to retain bargaining strength; rising e‑commerce (global online retail share ~22.7% in 2024) shifts tenant mix and increases sensitivity to vacancy rates, which directly swing negotiation outcomes.

- Tenant leverage: rent, fit‑out, marketing

- Anchor power: outsized bargaining

- AEON tools: footfall, analytics, mixed‑use

- Market fact: e‑commerce ~22.7% (2024)

- Vacancy: key determinant of concessions

Financial services customers

Cardholders and banking users can switch to banks, fintechs, or wallets offering better rates and user experience, making buyer power high; fee sensitivity and rewards programs drive churn risk as customers follow value and convenience. Cross-selling from retail traffic reduces acquisition costs but rarely creates full lock-in, while regulatory fee caps and consumer protection rules amplify buyer leverage.

- High switching leverage

- Fee/reward driven churn

- Cross-sell lowers CAC but not stickiness

- Regulatory caps increase buyer power

Price-sensitive shoppers as e-commerce hits 22.7%

Customers hold elevated leverage: instant price comparison (online grocery ~8% in 2024) and low switching costs drive price sensitivity, while AEON’s 25m cardholders and ¥8.7T FY2024 revenue partially mitigate but do not eliminate churn. Tenants and anchor retailers exert strong negotiation power as e‑commerce share (~22.7% in 2024) reshapes footfall and concessions.

| Metric | 2024 |

|---|---|

| Online grocery | ~8% |

| E‑commerce share | ~22.7% |

| AEON cardholders | 25M+ |

| AEON revenue | ¥8.7T |

Preview the Actual Deliverable

Aeon Porter's Five Forces Analysis

This preview shows the exact Aeon Porter Five Forces Analysis you’ll receive—no placeholders or mockups. The file is the final, professionally written document, fully formatted and ready for immediate download upon purchase. It contains the complete Five Forces assessment and actionable insights for strategic use.

Don't Miss the Bigger Picture

Aeon's Porter's Five Forces Analysis distills competitive pressures—supplier and buyer power, threat of entrants and substitutes, and industry rivalry—into actionable insights, showing where Aeon holds leverage and where market dynamics could compress margins for investors and strategists alike.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aeon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified sourcing base

AEON buys from thousands of FMCG, fresh and specialty suppliers across regions, diluting individual supplier leverage and spreading risk. Centralized procurement and scale—AEON recorded roughly 8 trillion yen in consolidated retail sales in 2024—enable substantial volume discounts. Premium global brands, however, retain negotiating clout on price and terms. Fresh produce seasonality can temporarily raise supplier power during peak shortages.

Private label leverage

Aeon’s strong private label TOPVALU (expanded in 2024) reduces reliance on national brands and anchors negotiations, with private-label penetration in Japanese groceries roughly 18% in 2024, boosting Aeon’s leverage. Backward integration into product development and QA expands switching options and squeezes branded suppliers on price and promo support. However, any TOPVALU quality missteps quickly erode trust, limiting overuse of private-label pressure.

Vertical integration in property

Vertical integration—ownership and operation of malls cuts reliance on third‑party landlords for prime space, strengthening negotiation leverage with fit‑out, facility and services vendors and often reducing external rent exposure versus fully leased peers. However, construction and utilities suppliers retained power during 2024 tight capacity cycles (construction input prices rose ~3% y/y), and high capex intensity increases vulnerability to input cost swings.

Logistics and tech vendors

Advanced DCs, cold chain and proprietary IT platforms create meaningful vendor switching costs for logistics and tech suppliers, while carrier consolidation—top 10 carriers control ~85% of global container capacity in 2024—gives carriers and systems integrators leverage to demand favorable SLAs. AEON’s scale reduces but does not remove dependency risk; multi-sourcing and growing in‑house capabilities buffer operational shocks.

- High switching costs: proprietary DCs, cold chain, IT

- Carrier leverage: top 10 control ~85% (2024)

- AEON scale mitigates but dependency remains

- Multi-sourcing and in‑house ops provide buffers

Regulatory and import exposure

Retail giant scale (~8T JPY) and 18% private-label curb supplier power amid 10% weaker JPY

AEON’s scale (≈8 trillion yen retail sales in 2024) and thousands of suppliers dilute supplier power, aided by TOPVALU private‑label penetration ~18% in 2024. High switching costs from proprietary DCs/cold chain and tech raise vendor leverage, while carrier concentration (top 10 ≈85% global capacity) and regulatory/ESG shifts (FAO index 121 in 2024) increase supplier bargaining. JPY ≈-10% vs USD in 2024 raised import cost pressure.

| Metric | 2024 |

|---|---|

| AEON sales | ≈8 trillion JPY |

| TOPVALU share | ≈18% |

| FAO Food Index | 121 |

| JPY vs USD | ≈-10% |

| Top10 carriers | ≈85% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Aeon that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary and industry data—fully editable for use in investor decks, business plans or internal strategy reports.

Aeon Porter's Five Forces delivers a single-sheet, customizable view that visualizes competitive pressure with an instant radar chart, supports scenario tabs and quick data swaps, and is ready for decks—no macros or finance expertise required.

Customers Bargaining Power

Price transparency and choice

Consumers now compare prices across supermarkets, discounters and e‑commerce instantly, with global online grocery penetration rising to about 8% in 2024, intensifying transparency. Low switching costs on staples raise buyer leverage, especially as frequent promotions train 40–60% of shoppers to wait for deals. Omni‑channel options further accelerate comparison shopping and price sensitivity.

Loyalty ecosystems

AEON’s loyalty ecosystem — over 25 million cardholders in 2024 — raises switching costs via AEON Card, WAON e-money and finance products, enabling data-driven personalization and bundled rewards that blunt buyer leverage; however if rivals replicate rewards the bargaining power shifts back to customers, while strict 2024 data-privacy expectations force more transparent, opt-in program designs.

Quality and freshness expectations

Japanese consumers demand high quality, safety and freshness and punish lapses quickly, forcing AEON—Japan's largest retailer—to impose tighter specs and supplier monitoring that raise procurement and compliance costs; AEON Group reported approximately ¥8.7 trillion in revenue in FY2024. Buyers can trade up or down across formats based on perceived value, and brand reputation constrains AEON’s pricing power.

Corporate tenants and merchants

Mall tenants negotiate rents, fit‑out contributions and marketing support, intensifying in soft demand; anchor tenants exert outsized leverage on terms while AEON counters with footfall, shopper analytics and mixed‑use curation to retain bargaining strength; rising e‑commerce (global online retail share ~22.7% in 2024) shifts tenant mix and increases sensitivity to vacancy rates, which directly swing negotiation outcomes.

- Tenant leverage: rent, fit‑out, marketing

- Anchor power: outsized bargaining

- AEON tools: footfall, analytics, mixed‑use

- Market fact: e‑commerce ~22.7% (2024)

- Vacancy: key determinant of concessions

Financial services customers

Cardholders and banking users can switch to banks, fintechs, or wallets offering better rates and user experience, making buyer power high; fee sensitivity and rewards programs drive churn risk as customers follow value and convenience. Cross-selling from retail traffic reduces acquisition costs but rarely creates full lock-in, while regulatory fee caps and consumer protection rules amplify buyer leverage.

- High switching leverage

- Fee/reward driven churn

- Cross-sell lowers CAC but not stickiness

- Regulatory caps increase buyer power

Price-sensitive shoppers as e-commerce hits 22.7%

Customers hold elevated leverage: instant price comparison (online grocery ~8% in 2024) and low switching costs drive price sensitivity, while AEON’s 25m cardholders and ¥8.7T FY2024 revenue partially mitigate but do not eliminate churn. Tenants and anchor retailers exert strong negotiation power as e‑commerce share (~22.7% in 2024) reshapes footfall and concessions.

| Metric | 2024 |

|---|---|

| Online grocery | ~8% |

| E‑commerce share | ~22.7% |

| AEON cardholders | 25M+ |

| AEON revenue | ¥8.7T |

Preview the Actual Deliverable

Aeon Porter's Five Forces Analysis

This preview shows the exact Aeon Porter Five Forces Analysis you’ll receive—no placeholders or mockups. The file is the final, professionally written document, fully formatted and ready for immediate download upon purchase. It contains the complete Five Forces assessment and actionable insights for strategic use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Aeon's Porter's Five Forces Analysis distills competitive pressures—supplier and buyer power, threat of entrants and substitutes, and industry rivalry—into actionable insights, showing where Aeon holds leverage and where market dynamics could compress margins for investors and strategists alike.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Aeon’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diversified sourcing base

AEON buys from thousands of FMCG, fresh and specialty suppliers across regions, diluting individual supplier leverage and spreading risk. Centralized procurement and scale—AEON recorded roughly 8 trillion yen in consolidated retail sales in 2024—enable substantial volume discounts. Premium global brands, however, retain negotiating clout on price and terms. Fresh produce seasonality can temporarily raise supplier power during peak shortages.

Private label leverage

Aeon’s strong private label TOPVALU (expanded in 2024) reduces reliance on national brands and anchors negotiations, with private-label penetration in Japanese groceries roughly 18% in 2024, boosting Aeon’s leverage. Backward integration into product development and QA expands switching options and squeezes branded suppliers on price and promo support. However, any TOPVALU quality missteps quickly erode trust, limiting overuse of private-label pressure.

Vertical integration in property

Vertical integration—ownership and operation of malls cuts reliance on third‑party landlords for prime space, strengthening negotiation leverage with fit‑out, facility and services vendors and often reducing external rent exposure versus fully leased peers. However, construction and utilities suppliers retained power during 2024 tight capacity cycles (construction input prices rose ~3% y/y), and high capex intensity increases vulnerability to input cost swings.

Logistics and tech vendors

Advanced DCs, cold chain and proprietary IT platforms create meaningful vendor switching costs for logistics and tech suppliers, while carrier consolidation—top 10 carriers control ~85% of global container capacity in 2024—gives carriers and systems integrators leverage to demand favorable SLAs. AEON’s scale reduces but does not remove dependency risk; multi-sourcing and growing in‑house capabilities buffer operational shocks.

- High switching costs: proprietary DCs, cold chain, IT

- Carrier leverage: top 10 control ~85% (2024)

- AEON scale mitigates but dependency remains

- Multi-sourcing and in‑house ops provide buffers

Regulatory and import exposure

Retail giant scale (~8T JPY) and 18% private-label curb supplier power amid 10% weaker JPY

AEON’s scale (≈8 trillion yen retail sales in 2024) and thousands of suppliers dilute supplier power, aided by TOPVALU private‑label penetration ~18% in 2024. High switching costs from proprietary DCs/cold chain and tech raise vendor leverage, while carrier concentration (top 10 ≈85% global capacity) and regulatory/ESG shifts (FAO index 121 in 2024) increase supplier bargaining. JPY ≈-10% vs USD in 2024 raised import cost pressure.

| Metric | 2024 |

|---|---|

| AEON sales | ≈8 trillion JPY |

| TOPVALU share | ≈18% |

| FAO Food Index | 121 |

| JPY vs USD | ≈-10% |

| Top10 carriers | ≈85% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Aeon that uncovers competitive intensity, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary and industry data—fully editable for use in investor decks, business plans or internal strategy reports.

Aeon Porter's Five Forces delivers a single-sheet, customizable view that visualizes competitive pressure with an instant radar chart, supports scenario tabs and quick data swaps, and is ready for decks—no macros or finance expertise required.

Customers Bargaining Power

Price transparency and choice

Consumers now compare prices across supermarkets, discounters and e‑commerce instantly, with global online grocery penetration rising to about 8% in 2024, intensifying transparency. Low switching costs on staples raise buyer leverage, especially as frequent promotions train 40–60% of shoppers to wait for deals. Omni‑channel options further accelerate comparison shopping and price sensitivity.

Loyalty ecosystems

AEON’s loyalty ecosystem — over 25 million cardholders in 2024 — raises switching costs via AEON Card, WAON e-money and finance products, enabling data-driven personalization and bundled rewards that blunt buyer leverage; however if rivals replicate rewards the bargaining power shifts back to customers, while strict 2024 data-privacy expectations force more transparent, opt-in program designs.

Quality and freshness expectations

Japanese consumers demand high quality, safety and freshness and punish lapses quickly, forcing AEON—Japan's largest retailer—to impose tighter specs and supplier monitoring that raise procurement and compliance costs; AEON Group reported approximately ¥8.7 trillion in revenue in FY2024. Buyers can trade up or down across formats based on perceived value, and brand reputation constrains AEON’s pricing power.

Corporate tenants and merchants

Mall tenants negotiate rents, fit‑out contributions and marketing support, intensifying in soft demand; anchor tenants exert outsized leverage on terms while AEON counters with footfall, shopper analytics and mixed‑use curation to retain bargaining strength; rising e‑commerce (global online retail share ~22.7% in 2024) shifts tenant mix and increases sensitivity to vacancy rates, which directly swing negotiation outcomes.

- Tenant leverage: rent, fit‑out, marketing

- Anchor power: outsized bargaining

- AEON tools: footfall, analytics, mixed‑use

- Market fact: e‑commerce ~22.7% (2024)

- Vacancy: key determinant of concessions

Financial services customers

Cardholders and banking users can switch to banks, fintechs, or wallets offering better rates and user experience, making buyer power high; fee sensitivity and rewards programs drive churn risk as customers follow value and convenience. Cross-selling from retail traffic reduces acquisition costs but rarely creates full lock-in, while regulatory fee caps and consumer protection rules amplify buyer leverage.

- High switching leverage

- Fee/reward driven churn

- Cross-sell lowers CAC but not stickiness

- Regulatory caps increase buyer power

Price-sensitive shoppers as e-commerce hits 22.7%

Customers hold elevated leverage: instant price comparison (online grocery ~8% in 2024) and low switching costs drive price sensitivity, while AEON’s 25m cardholders and ¥8.7T FY2024 revenue partially mitigate but do not eliminate churn. Tenants and anchor retailers exert strong negotiation power as e‑commerce share (~22.7% in 2024) reshapes footfall and concessions.

| Metric | 2024 |

|---|---|

| Online grocery | ~8% |

| E‑commerce share | ~22.7% |

| AEON cardholders | 25M+ |

| AEON revenue | ¥8.7T |

Preview the Actual Deliverable

Aeon Porter's Five Forces Analysis

This preview shows the exact Aeon Porter Five Forces Analysis you’ll receive—no placeholders or mockups. The file is the final, professionally written document, fully formatted and ready for immediate download upon purchase. It contains the complete Five Forces assessment and actionable insights for strategic use.