Aeronautics Boston Consulting Group Matrix

Unlock Strategic Clarity

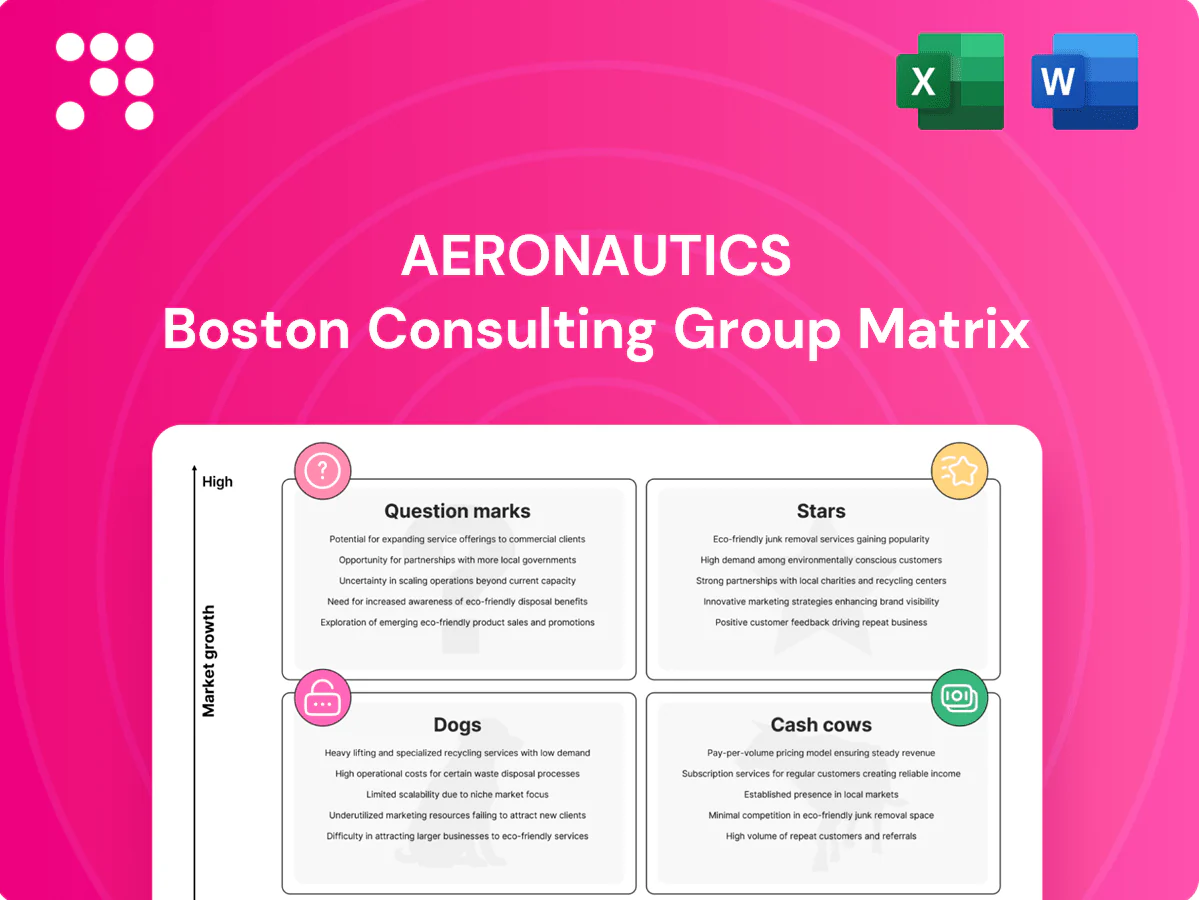

The Aeronautics BCG Matrix snapshot shows which of its product lines are soaring, which need cash to climb, and which are holding the company back — a fast, clear way to see where your capital really matters. This preview highlights key quadrant placements, but the full BCG Matrix gives you the exact data points, quadrant-by-quadrant strategy, and actionable recommendations tailored to Aeronautics’ market dynamics. Buy the full report for a ready-to-use Word analysis and Excel summary that lets you decide where to invest, divest, or double down—fast.

Stars

Flagship tactical UAS platform

Flagship tactical UAS platform holds high market share with defense customers and, as of 2024, sits in a fast-growing tactical UAS category. It leads bids but consumes cash for trials, certifications and establishing global support infrastructures. Continued promotional spend and field deployments are being used to lock in doctrine and procurement pipelines. Maintain share now; it is positioned to fold into a future cash cow.

Multi-mission ISR payload suite

EO/IR, SAR and light SIGINT bundles dominate recent ISR tenders and are key growth drivers in the multi-mission payload segment. Integration cycles and NRE often run into tens of millions of dollars but serve to lock in platform contracts and lifecycle revenues. Prioritize performance upgrades and export approvals, including ITAR-free options, to expand addressable markets by improving procurement competitiveness. Own the sensor slot and the airframe follows.

Border security turnkey UAS packages

National programs (US CBP, Frontex, India BSF) are scaling UAS procurements and Aeronautics frequently lists as a finalist; border security UAS demand helped drive the military/UAS market to an estimated $22B in 2023 and continued strong 2024 procurement. Growth is hot but delivery, training, and CONOPS support raise lifecycle costs materially, often 20-30% of program budgets. Invest to standardize turnkey kits and accelerate deployments to reduce per-deployment cost and shorten ramp. Keep wins compounding and recurring service contracts convert the business into annuity-like revenue streams.

Loitering-capable UAS family

Loitering-capable UAS family is a Star in Aeronautics BCG: 2024 operational demand is spiking and early customers report clear product-market fit. Rapid R&D, safety-case development, and munitions integration drive heavy cash burn; prioritize CAPEX for manufacturing scale and reliability metrics. Maintain technological lead to convert share into sustained margins.

- Market: 2024 demand spike

- Investment: high R&D and safety costs

- Priority: scale manufacturing, reliability stats

- Outcome: lead → sustained margins

Cloud-native multi-UAS C2 platform

Cloud-native multi-UAS C2 sits in Stars: command-and-control wins RFP points and user base grew ~35% in 2024; uptime SLAs target 99.95% while cyber hardening and integrations consume ~40% of engineering hours, pressuring margins; push roadmap velocity (+25% feature cadence) and partner ecosystem to scale; lock platform standards and it becomes the control layer everyone builds on.

- RFP wins: command-and-control advantage

- Uptime SLA: 99.95%

- Eng hours: ~40% on cyber/integrations

- Roadmap velocity: +25%

- Adoption: platform-as-control-layer

Flagship UAS, sensors & cloud C2 surge with 30%+ CAGR - scale & exports

Flagship tactical and loitering UAS, multi-mission sensors, and cloud-native C2 are Stars in 2024: high share in a fast-growing tactical UAS market, strong procurement (border security drove ~$22B military/UAS spend in 2023, strong 2024), rapid user growth (~35% C2), but heavy cash burn (R&D/safety/integrations 20–40% of spend). Prioritize scale, reliability, export approvals and recurring service conversion.

| Metric | 2024 |

|---|---|

| Market signal | Fast growth; >30% segment CAGR |

| R&D/Eng | 20–40% of spend |

| C2 adoption | +35% users |

| 2023 spend | $22B military/UAS (baseline) |

What is included in the product

Concise BCG analysis of aeronautics portfolio, naming Stars, Cash Cows, Questions, Dogs with investment, hold, divest guidance.

One-page Aeronautics BCG Matrix mapping units to quadrants for quick strategic clarity and stakeholder buy-in

Cash Cows

Legacy mini‑UAS installed base

Legacy mini-UAS sit in a mature market with high share and predictable reorder patterns, and in 2024 the installed base now drives roughly 30% of recurring service revenue for the business unit. Margins remain healthy and capex needs are modest, keeping EBITDA contribution strong while firmware refreshes are kept light and highly reliable. The company monetizes through service kits and incremental upgrades, extracting steady cash without major reinvestment.

Line‑of‑sight tactical datalinks

Proven line‑of‑sight tactical datalinks—with over 3,000 units fielded by 2024—sit in a slow‑growth category (market CAGR ~2–3% 2024 estimate), delivering high gross margins (>40%) with minimal promotional spend. Maintain certifications and backward compatibility to protect installed base and reduce R&D churn. Optimize production throughput and supply chain to harvest steady cash flow.

Training and operator certification

Training and operator certification are cash cows tied to recurring courses aligned with fleet renewals across a global commercial fleet of roughly 26,000 jets in 2024, delivering steady, high utilization and needing minimal R&D. Market growth is flat but sticky, roughly low-single-digit percent yearly, enabling predictable cash flows. Standardize curricula and expand virtual modules to cut delivery costs and scale. Reinvest excess cash into emerging autonomy bets to capture future upside.

MRO and depot‑level maintenance contracts

Long-term MRO and depot‑level maintenance contracts deliver steady, multi‑customer volume and predictable cash flow; the global commercial MRO market was about 92 billion USD in 2024, underscoring scale. Focus on operational efficiency to lift margins rather than chasing growth; targeted investment in tooling and faster turnaround directly reduces costs and improves SLA adherence. Bank the cash and keep SLAs spotless to protect renewal rates and backlog value.

- Long-term service agreements

- Steady volume, predictable cash

- Efficiency = margin, not growth

- Invest in tooling & TAT

- Bank cash; flawless SLAs

Spares and sustainment kits

Spares and sustainment kits deliver consistent pull-through from the installed base with predictable demand; 2024 industry benchmarks show recurring service revenues often representing 40-60% of aftermarket sales and contribution margins of 30-45% due to low selling costs. Bundle parts, forecast aggressively and keep inventory tight (8-12 turns) to preserve margin uplift and >95% service-level targets.

- Installed-base pull-through: 40-60% (2024)

- Contribution margin: 30-45% (2024)

- Inventory turns target: 8-12/yr

- Service level goal: >95%

Mini-UAS datalinks & spares = steady cash; 30% service, turns 8-12

Legacy mini-UAS, proven tactical datalinks and MRO/spares are cash cows: steady recurring revenue (~30% BU service rev), high margins (datalinks >40%, spares 30–45%), low reinvestment and predictable demand (datalinks >3,000 units; market CAGR ~2–3% in 2024). Prioritize efficiency, certification upkeep and inventory turns (8–12) to maximize free cash for autonomy bets.

| Metric | Value (2024) |

|---|---|

| Service rev from installed base | ~30% |

| Fielded datalinks | >3,000 units |

| Market CAGR | 2–3% |

| Gross margins | 40%+ (datalinks) |

| MRO market | $92B |

| Spares recurring | 40–60% |

| Inventory turns target | 8–12/yr |

| Service level goal | >95% |

What You’re Viewing Is Included

Aeronautics BCG Matrix

The Aeronautics BCG Matrix you're previewing here is the exact same file you'll receive after purchase—no watermarks, no placeholders, just the finished, fully formatted report. It's built for immediate use: edit, print, or drop into a pitch deck without fiddling. Crafted by strategy pros with aviation market insights, the matrix highlights stars, cash cows, question marks, and dogs with clear visuals and actionable notes. Buy once and download instantly—no surprises, just clarity for your next strategic move.

Unlock Strategic Clarity

The Aeronautics BCG Matrix snapshot shows which of its product lines are soaring, which need cash to climb, and which are holding the company back — a fast, clear way to see where your capital really matters. This preview highlights key quadrant placements, but the full BCG Matrix gives you the exact data points, quadrant-by-quadrant strategy, and actionable recommendations tailored to Aeronautics’ market dynamics. Buy the full report for a ready-to-use Word analysis and Excel summary that lets you decide where to invest, divest, or double down—fast.

Stars

Flagship tactical UAS platform

Flagship tactical UAS platform holds high market share with defense customers and, as of 2024, sits in a fast-growing tactical UAS category. It leads bids but consumes cash for trials, certifications and establishing global support infrastructures. Continued promotional spend and field deployments are being used to lock in doctrine and procurement pipelines. Maintain share now; it is positioned to fold into a future cash cow.

Multi-mission ISR payload suite

EO/IR, SAR and light SIGINT bundles dominate recent ISR tenders and are key growth drivers in the multi-mission payload segment. Integration cycles and NRE often run into tens of millions of dollars but serve to lock in platform contracts and lifecycle revenues. Prioritize performance upgrades and export approvals, including ITAR-free options, to expand addressable markets by improving procurement competitiveness. Own the sensor slot and the airframe follows.

Border security turnkey UAS packages

National programs (US CBP, Frontex, India BSF) are scaling UAS procurements and Aeronautics frequently lists as a finalist; border security UAS demand helped drive the military/UAS market to an estimated $22B in 2023 and continued strong 2024 procurement. Growth is hot but delivery, training, and CONOPS support raise lifecycle costs materially, often 20-30% of program budgets. Invest to standardize turnkey kits and accelerate deployments to reduce per-deployment cost and shorten ramp. Keep wins compounding and recurring service contracts convert the business into annuity-like revenue streams.

Loitering-capable UAS family

Loitering-capable UAS family is a Star in Aeronautics BCG: 2024 operational demand is spiking and early customers report clear product-market fit. Rapid R&D, safety-case development, and munitions integration drive heavy cash burn; prioritize CAPEX for manufacturing scale and reliability metrics. Maintain technological lead to convert share into sustained margins.

- Market: 2024 demand spike

- Investment: high R&D and safety costs

- Priority: scale manufacturing, reliability stats

- Outcome: lead → sustained margins

Cloud-native multi-UAS C2 platform

Cloud-native multi-UAS C2 sits in Stars: command-and-control wins RFP points and user base grew ~35% in 2024; uptime SLAs target 99.95% while cyber hardening and integrations consume ~40% of engineering hours, pressuring margins; push roadmap velocity (+25% feature cadence) and partner ecosystem to scale; lock platform standards and it becomes the control layer everyone builds on.

- RFP wins: command-and-control advantage

- Uptime SLA: 99.95%

- Eng hours: ~40% on cyber/integrations

- Roadmap velocity: +25%

- Adoption: platform-as-control-layer

Flagship UAS, sensors & cloud C2 surge with 30%+ CAGR - scale & exports

Flagship tactical and loitering UAS, multi-mission sensors, and cloud-native C2 are Stars in 2024: high share in a fast-growing tactical UAS market, strong procurement (border security drove ~$22B military/UAS spend in 2023, strong 2024), rapid user growth (~35% C2), but heavy cash burn (R&D/safety/integrations 20–40% of spend). Prioritize scale, reliability, export approvals and recurring service conversion.

| Metric | 2024 |

|---|---|

| Market signal | Fast growth; >30% segment CAGR |

| R&D/Eng | 20–40% of spend |

| C2 adoption | +35% users |

| 2023 spend | $22B military/UAS (baseline) |

What is included in the product

Concise BCG analysis of aeronautics portfolio, naming Stars, Cash Cows, Questions, Dogs with investment, hold, divest guidance.

One-page Aeronautics BCG Matrix mapping units to quadrants for quick strategic clarity and stakeholder buy-in

Cash Cows

Legacy mini‑UAS installed base

Legacy mini-UAS sit in a mature market with high share and predictable reorder patterns, and in 2024 the installed base now drives roughly 30% of recurring service revenue for the business unit. Margins remain healthy and capex needs are modest, keeping EBITDA contribution strong while firmware refreshes are kept light and highly reliable. The company monetizes through service kits and incremental upgrades, extracting steady cash without major reinvestment.

Line‑of‑sight tactical datalinks

Proven line‑of‑sight tactical datalinks—with over 3,000 units fielded by 2024—sit in a slow‑growth category (market CAGR ~2–3% 2024 estimate), delivering high gross margins (>40%) with minimal promotional spend. Maintain certifications and backward compatibility to protect installed base and reduce R&D churn. Optimize production throughput and supply chain to harvest steady cash flow.

Training and operator certification

Training and operator certification are cash cows tied to recurring courses aligned with fleet renewals across a global commercial fleet of roughly 26,000 jets in 2024, delivering steady, high utilization and needing minimal R&D. Market growth is flat but sticky, roughly low-single-digit percent yearly, enabling predictable cash flows. Standardize curricula and expand virtual modules to cut delivery costs and scale. Reinvest excess cash into emerging autonomy bets to capture future upside.

MRO and depot‑level maintenance contracts

Long-term MRO and depot‑level maintenance contracts deliver steady, multi‑customer volume and predictable cash flow; the global commercial MRO market was about 92 billion USD in 2024, underscoring scale. Focus on operational efficiency to lift margins rather than chasing growth; targeted investment in tooling and faster turnaround directly reduces costs and improves SLA adherence. Bank the cash and keep SLAs spotless to protect renewal rates and backlog value.

- Long-term service agreements

- Steady volume, predictable cash

- Efficiency = margin, not growth

- Invest in tooling & TAT

- Bank cash; flawless SLAs

Spares and sustainment kits

Spares and sustainment kits deliver consistent pull-through from the installed base with predictable demand; 2024 industry benchmarks show recurring service revenues often representing 40-60% of aftermarket sales and contribution margins of 30-45% due to low selling costs. Bundle parts, forecast aggressively and keep inventory tight (8-12 turns) to preserve margin uplift and >95% service-level targets.

- Installed-base pull-through: 40-60% (2024)

- Contribution margin: 30-45% (2024)

- Inventory turns target: 8-12/yr

- Service level goal: >95%

Mini-UAS datalinks & spares = steady cash; 30% service, turns 8-12

Legacy mini-UAS, proven tactical datalinks and MRO/spares are cash cows: steady recurring revenue (~30% BU service rev), high margins (datalinks >40%, spares 30–45%), low reinvestment and predictable demand (datalinks >3,000 units; market CAGR ~2–3% in 2024). Prioritize efficiency, certification upkeep and inventory turns (8–12) to maximize free cash for autonomy bets.

| Metric | Value (2024) |

|---|---|

| Service rev from installed base | ~30% |

| Fielded datalinks | >3,000 units |

| Market CAGR | 2–3% |

| Gross margins | 40%+ (datalinks) |

| MRO market | $92B |

| Spares recurring | 40–60% |

| Inventory turns target | 8–12/yr |

| Service level goal | >95% |

What You’re Viewing Is Included

Aeronautics BCG Matrix

The Aeronautics BCG Matrix you're previewing here is the exact same file you'll receive after purchase—no watermarks, no placeholders, just the finished, fully formatted report. It's built for immediate use: edit, print, or drop into a pitch deck without fiddling. Crafted by strategy pros with aviation market insights, the matrix highlights stars, cash cows, question marks, and dogs with clear visuals and actionable notes. Buy once and download instantly—no surprises, just clarity for your next strategic move.

Description

Unlock Strategic Clarity

The Aeronautics BCG Matrix snapshot shows which of its product lines are soaring, which need cash to climb, and which are holding the company back — a fast, clear way to see where your capital really matters. This preview highlights key quadrant placements, but the full BCG Matrix gives you the exact data points, quadrant-by-quadrant strategy, and actionable recommendations tailored to Aeronautics’ market dynamics. Buy the full report for a ready-to-use Word analysis and Excel summary that lets you decide where to invest, divest, or double down—fast.

Stars

Flagship tactical UAS platform

Flagship tactical UAS platform holds high market share with defense customers and, as of 2024, sits in a fast-growing tactical UAS category. It leads bids but consumes cash for trials, certifications and establishing global support infrastructures. Continued promotional spend and field deployments are being used to lock in doctrine and procurement pipelines. Maintain share now; it is positioned to fold into a future cash cow.

Multi-mission ISR payload suite

EO/IR, SAR and light SIGINT bundles dominate recent ISR tenders and are key growth drivers in the multi-mission payload segment. Integration cycles and NRE often run into tens of millions of dollars but serve to lock in platform contracts and lifecycle revenues. Prioritize performance upgrades and export approvals, including ITAR-free options, to expand addressable markets by improving procurement competitiveness. Own the sensor slot and the airframe follows.

Border security turnkey UAS packages

National programs (US CBP, Frontex, India BSF) are scaling UAS procurements and Aeronautics frequently lists as a finalist; border security UAS demand helped drive the military/UAS market to an estimated $22B in 2023 and continued strong 2024 procurement. Growth is hot but delivery, training, and CONOPS support raise lifecycle costs materially, often 20-30% of program budgets. Invest to standardize turnkey kits and accelerate deployments to reduce per-deployment cost and shorten ramp. Keep wins compounding and recurring service contracts convert the business into annuity-like revenue streams.

Loitering-capable UAS family

Loitering-capable UAS family is a Star in Aeronautics BCG: 2024 operational demand is spiking and early customers report clear product-market fit. Rapid R&D, safety-case development, and munitions integration drive heavy cash burn; prioritize CAPEX for manufacturing scale and reliability metrics. Maintain technological lead to convert share into sustained margins.

- Market: 2024 demand spike

- Investment: high R&D and safety costs

- Priority: scale manufacturing, reliability stats

- Outcome: lead → sustained margins

Cloud-native multi-UAS C2 platform

Cloud-native multi-UAS C2 sits in Stars: command-and-control wins RFP points and user base grew ~35% in 2024; uptime SLAs target 99.95% while cyber hardening and integrations consume ~40% of engineering hours, pressuring margins; push roadmap velocity (+25% feature cadence) and partner ecosystem to scale; lock platform standards and it becomes the control layer everyone builds on.

- RFP wins: command-and-control advantage

- Uptime SLA: 99.95%

- Eng hours: ~40% on cyber/integrations

- Roadmap velocity: +25%

- Adoption: platform-as-control-layer

Flagship UAS, sensors & cloud C2 surge with 30%+ CAGR - scale & exports

Flagship tactical and loitering UAS, multi-mission sensors, and cloud-native C2 are Stars in 2024: high share in a fast-growing tactical UAS market, strong procurement (border security drove ~$22B military/UAS spend in 2023, strong 2024), rapid user growth (~35% C2), but heavy cash burn (R&D/safety/integrations 20–40% of spend). Prioritize scale, reliability, export approvals and recurring service conversion.

| Metric | 2024 |

|---|---|

| Market signal | Fast growth; >30% segment CAGR |

| R&D/Eng | 20–40% of spend |

| C2 adoption | +35% users |

| 2023 spend | $22B military/UAS (baseline) |

What is included in the product

Concise BCG analysis of aeronautics portfolio, naming Stars, Cash Cows, Questions, Dogs with investment, hold, divest guidance.

One-page Aeronautics BCG Matrix mapping units to quadrants for quick strategic clarity and stakeholder buy-in

Cash Cows

Legacy mini‑UAS installed base

Legacy mini-UAS sit in a mature market with high share and predictable reorder patterns, and in 2024 the installed base now drives roughly 30% of recurring service revenue for the business unit. Margins remain healthy and capex needs are modest, keeping EBITDA contribution strong while firmware refreshes are kept light and highly reliable. The company monetizes through service kits and incremental upgrades, extracting steady cash without major reinvestment.

Line‑of‑sight tactical datalinks

Proven line‑of‑sight tactical datalinks—with over 3,000 units fielded by 2024—sit in a slow‑growth category (market CAGR ~2–3% 2024 estimate), delivering high gross margins (>40%) with minimal promotional spend. Maintain certifications and backward compatibility to protect installed base and reduce R&D churn. Optimize production throughput and supply chain to harvest steady cash flow.

Training and operator certification

Training and operator certification are cash cows tied to recurring courses aligned with fleet renewals across a global commercial fleet of roughly 26,000 jets in 2024, delivering steady, high utilization and needing minimal R&D. Market growth is flat but sticky, roughly low-single-digit percent yearly, enabling predictable cash flows. Standardize curricula and expand virtual modules to cut delivery costs and scale. Reinvest excess cash into emerging autonomy bets to capture future upside.

MRO and depot‑level maintenance contracts

Long-term MRO and depot‑level maintenance contracts deliver steady, multi‑customer volume and predictable cash flow; the global commercial MRO market was about 92 billion USD in 2024, underscoring scale. Focus on operational efficiency to lift margins rather than chasing growth; targeted investment in tooling and faster turnaround directly reduces costs and improves SLA adherence. Bank the cash and keep SLAs spotless to protect renewal rates and backlog value.

- Long-term service agreements

- Steady volume, predictable cash

- Efficiency = margin, not growth

- Invest in tooling & TAT

- Bank cash; flawless SLAs

Spares and sustainment kits

Spares and sustainment kits deliver consistent pull-through from the installed base with predictable demand; 2024 industry benchmarks show recurring service revenues often representing 40-60% of aftermarket sales and contribution margins of 30-45% due to low selling costs. Bundle parts, forecast aggressively and keep inventory tight (8-12 turns) to preserve margin uplift and >95% service-level targets.

- Installed-base pull-through: 40-60% (2024)

- Contribution margin: 30-45% (2024)

- Inventory turns target: 8-12/yr

- Service level goal: >95%

Mini-UAS datalinks & spares = steady cash; 30% service, turns 8-12

Legacy mini-UAS, proven tactical datalinks and MRO/spares are cash cows: steady recurring revenue (~30% BU service rev), high margins (datalinks >40%, spares 30–45%), low reinvestment and predictable demand (datalinks >3,000 units; market CAGR ~2–3% in 2024). Prioritize efficiency, certification upkeep and inventory turns (8–12) to maximize free cash for autonomy bets.

| Metric | Value (2024) |

|---|---|

| Service rev from installed base | ~30% |

| Fielded datalinks | >3,000 units |

| Market CAGR | 2–3% |

| Gross margins | 40%+ (datalinks) |

| MRO market | $92B |

| Spares recurring | 40–60% |

| Inventory turns target | 8–12/yr |

| Service level goal | >95% |

What You’re Viewing Is Included

Aeronautics BCG Matrix

The Aeronautics BCG Matrix you're previewing here is the exact same file you'll receive after purchase—no watermarks, no placeholders, just the finished, fully formatted report. It's built for immediate use: edit, print, or drop into a pitch deck without fiddling. Crafted by strategy pros with aviation market insights, the matrix highlights stars, cash cows, question marks, and dogs with clear visuals and actionable notes. Buy once and download instantly—no surprises, just clarity for your next strategic move.