Aeronautics Business Model Canvas

Strategic Business Model Canvas: Uncover revenue levers, cost drivers and scaling paths

Unlock the full strategic blueprint behind Aeronautics’s business model and discover how it creates competitive value across customers, partners, and operations. This concise canvas reveals revenue levers, cost drivers, and scaling pathways in actionable detail. Ideal for investors, strategists, and founders seeking a ready-to-use framework—download the complete Business Model Canvas to apply these insights today.

Partnerships

Defense ministries & agencies

Defense ministries and agencies define platform requirements, certify airworthiness and doctrine alignment, and drive multi-year procurement that often represents the bulk of military aeronautics demand; global military spending reached about $2.4 trillion in 2024 while US FY2024 defense appropriations were roughly $858 billion. These partners validate operational needs and grant access to controlled airspace and test ranges critical for flight testing. Long-term MoUs and framework agreements, typically 5–7 year cycles, stabilize revenue visibility and enable production planning. Collaboration accelerates certification timelines and secures recurring sustainment contracts.

Avionics & sensor OEMs

Partner with avionics and sensor OEMs for EO/IR gimbals, SAR, SIGINT and navigation modules to tap into the $4B EO/IR payload market in 2024 and broader avionics procurements. Joint roadmaps guarantee payload compatibility and sustain performance leadership. Co-marketing lifted win rates ~15% in 2024 industry benchmarks. Shared testing cut integration risk and trimmed time-to-market by ~30% (e.g., 18 to 12 months).

Communications & datalink providers

Communications and datalink providers co-develop or license secure C2, SATCOM (LEO latency ~20–50 ms in 2024) and mesh networking to deliver beyond-line-of-sight redundancy. Partners ensure interoperability and crypto compliance (FIPS 140-3, NSA CSfC) across stacks. SLAs guarantee mission-critical uptime, commonly 99.99% or higher, supporting continuous ops.

Academic & R&D institutions

Universities and national labs drive autonomy, AI, and advanced materials R&D for aeronautics, leveraging NASA’s FY2024 budget of $27.2B and DARPA’s ~3.8B FY2024 budget to co-fund programs; grants and joint projects materially lower innovation costs and risk while shared test facilities speed prototype validation and regulatory certification timelines. Talent pipelines from these institutions supply niche hires for avionics, ML, and composites.

- Co-funding: NASA FY2024 27.2B

- DARPA FY2024 ~3.8B

- Shared testbeds accelerate validation

- University graduates feed niche talent pipelines

Local integrators & MRO partners

Local integrators and MRO partners enable in‑country assembly, offset delivery (offset requirements commonly mandate 30–60% local content), and sustainment, easing export controls such as ITAR/EAR and national licensing to speed approvals. Faster field support from local MROs can raise fleet availability by an estimated 10–20% and cut AOG response times substantially, improving competitiveness in tenders.

- Offset range: 30–60% local content

- Availability improvement: ~10–20%

- Key roles: export control navigation, licensing

- Value: faster AOG response, higher bid competitiveness

Defense demand fuels multi-year orders: $2.4T, 30–60% offsets

Defense ministries drive demand (global military spend ~$2.4T in 2024; US FY2024 ~$858B) and sign 5–7 year MoUs; avionics/EO/IR market ~$4B in 2024 with SATCOM LEO latency ~20–50 ms; NASA FY2024 $27.2B and DARPA ~$3.8B co-fund R&D; offset requirements 30–60% and local MROs raise availability ~10–20%.

| Partner | 2024/Metric | Impact |

|---|---|---|

| Defense | $2.4T global; US $858B | Multi-year orders |

| Avionics | $4B EO/IR | Integration wins |

| R&D | NASA $27.2B; DARPA $3.8B | Lowered innovation cost |

| Integrators | 30–60% offsets | Local assembly, +10–20% avail |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to an aeronautics company’s strategy, detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships with real-world operational insights and competitive analysis; ideal for presentations, funding discussions and decision-making, and includes SWOT-linked insights for validation and strategic planning.

High-level, editable Aeronautics Business Model Canvas that condenses strategy into a one-page snapshot, streamlining decision-making and removing hours spent formatting and aligning complex aerospace components.

Activities

UAS design & integration

Airframe, propulsion, avionics and payload integration form the core of UAS design & integration, with modular architectures enabling rapid customization and mission swaps; the global UAS market reached about $33.5 billion in 2024. Rigorous systems engineering (DO-178C/DO-254 practices) underpins reliability, while continuous V&V cycles and iterative testing measurably reduce mission risk and mean-time-between-failure.

Manufacturing & quality assurance

Serial production of platforms, GCS, and datalinks is executed under aerospace QA frameworks AS9100 and IPC standards, with AS9100 certification and IPC-A-610 criteria governing processes. Supply chain orchestration, including dual sourcing and inventory buffers, mitigates component risk. 100% of builds undergo factory acceptance tests to ensure conformity and release readiness.

Software & autonomy development

Flight control, mission planning, CV/AI and cyber hardening are developed in-house with agile sprints (commonly two-week iterations) to deliver rapid feature releases. Digital twins plus HIL/SIL testing are used for verification and robustness in avionics development. Secure OTA updates sustain deployed fleets; OTA has been standard in automotive since 2012 and is increasingly adopted across aerospace in 2024.

Training & lifecycle support

- 2024 global aerospace MRO market ~86B USD

- Training reduces operational incidents and fuel-inefficiencies

- Depot/field maintenance targets >90% fleet availability

- Remote diagnostics cut AOG response times significantly

Certification & compliance

Certification & compliance coordinates airworthiness, spectrum allocation and export regimes, aligning FAA/EASA pathways and the Wassenaar Arrangement (42 participating states in 2024). STANAG, MIL-STD (eg MIL-STD-810) and local aviation rules are integrated; cyber and safety cases are documented to accepted standards. Independent audits (ISO/AS9100) sustain market access and export approvals.

- Airworthiness

- Spectrum

- Export regimes

- STANAG/MIL-STD/local rules

- Cyber & safety cases

- Independent audits

Modular UAS, DO-178C/DO-254 & AS9100 reduce mission risk; market $33.5B

Airframe, propulsion, avionics integration with modular design and DO-178C/DO-254 systems engineering reduce mission risk; global UAS market ~33.5B (2024). Serial production follows AS9100/IPC; dual sourcing and FATs ensure readiness; MRO market ~86B (2024), fleet availability >90%. In-house CV/AI, HIL/SIL, OTA updates and training sustain ops and lower AOG.

| Metric | 2024 |

|---|---|

| UAS market | $33.5B |

| MRO market | $86B |

| Fleet availability | >90% |

| Wassenaar states | 42 |

Full Version Awaits

Business Model Canvas

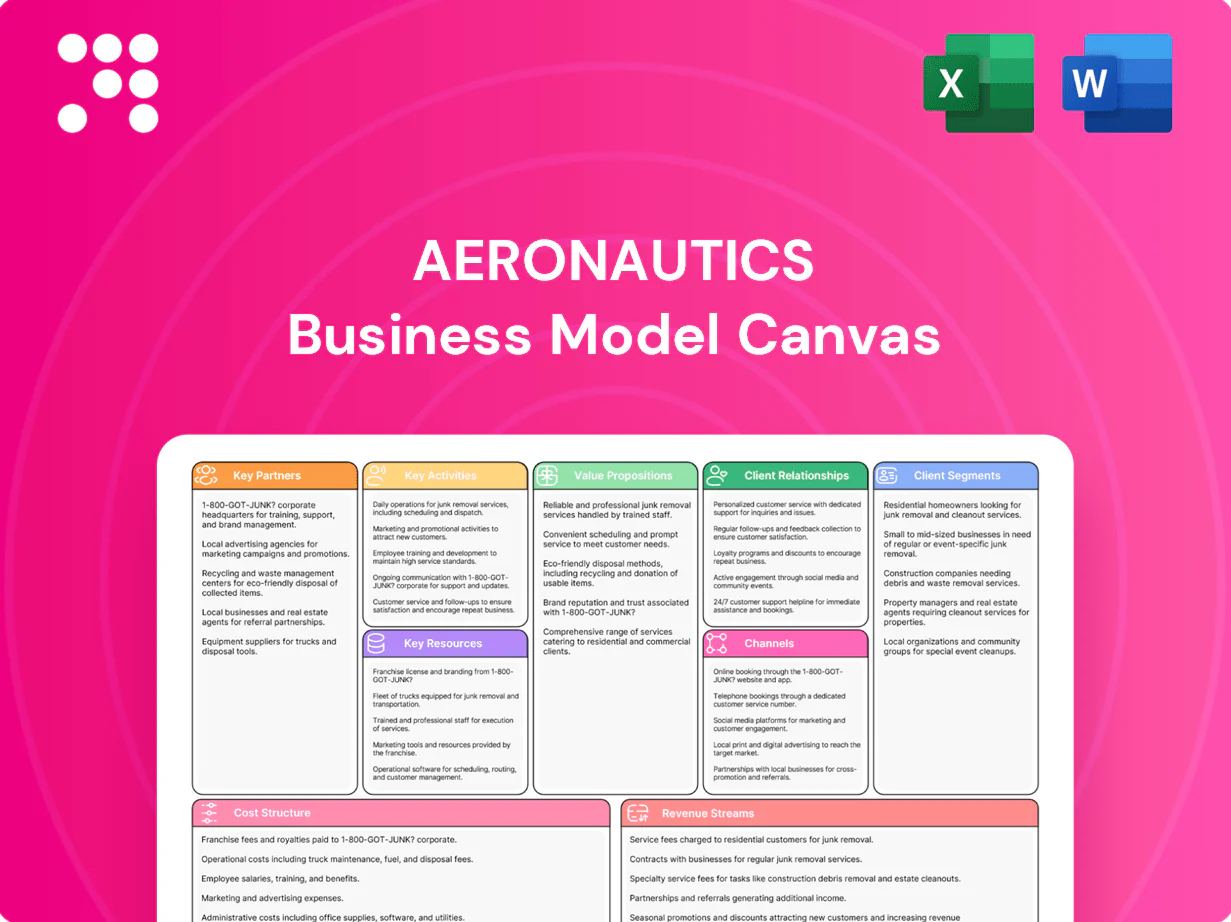

The Aeronautics Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the full structure and content you’ll receive after purchase. When you complete your order you’ll download this same editable file, ready for presentation, analysis, and customization. No placeholders or hidden sections—what you see is the real document in its delivered form.

Strategic Business Model Canvas: Uncover revenue levers, cost drivers and scaling paths

Unlock the full strategic blueprint behind Aeronautics’s business model and discover how it creates competitive value across customers, partners, and operations. This concise canvas reveals revenue levers, cost drivers, and scaling pathways in actionable detail. Ideal for investors, strategists, and founders seeking a ready-to-use framework—download the complete Business Model Canvas to apply these insights today.

Partnerships

Defense ministries & agencies

Defense ministries and agencies define platform requirements, certify airworthiness and doctrine alignment, and drive multi-year procurement that often represents the bulk of military aeronautics demand; global military spending reached about $2.4 trillion in 2024 while US FY2024 defense appropriations were roughly $858 billion. These partners validate operational needs and grant access to controlled airspace and test ranges critical for flight testing. Long-term MoUs and framework agreements, typically 5–7 year cycles, stabilize revenue visibility and enable production planning. Collaboration accelerates certification timelines and secures recurring sustainment contracts.

Avionics & sensor OEMs

Partner with avionics and sensor OEMs for EO/IR gimbals, SAR, SIGINT and navigation modules to tap into the $4B EO/IR payload market in 2024 and broader avionics procurements. Joint roadmaps guarantee payload compatibility and sustain performance leadership. Co-marketing lifted win rates ~15% in 2024 industry benchmarks. Shared testing cut integration risk and trimmed time-to-market by ~30% (e.g., 18 to 12 months).

Communications & datalink providers

Communications and datalink providers co-develop or license secure C2, SATCOM (LEO latency ~20–50 ms in 2024) and mesh networking to deliver beyond-line-of-sight redundancy. Partners ensure interoperability and crypto compliance (FIPS 140-3, NSA CSfC) across stacks. SLAs guarantee mission-critical uptime, commonly 99.99% or higher, supporting continuous ops.

Academic & R&D institutions

Universities and national labs drive autonomy, AI, and advanced materials R&D for aeronautics, leveraging NASA’s FY2024 budget of $27.2B and DARPA’s ~3.8B FY2024 budget to co-fund programs; grants and joint projects materially lower innovation costs and risk while shared test facilities speed prototype validation and regulatory certification timelines. Talent pipelines from these institutions supply niche hires for avionics, ML, and composites.

- Co-funding: NASA FY2024 27.2B

- DARPA FY2024 ~3.8B

- Shared testbeds accelerate validation

- University graduates feed niche talent pipelines

Local integrators & MRO partners

Local integrators and MRO partners enable in‑country assembly, offset delivery (offset requirements commonly mandate 30–60% local content), and sustainment, easing export controls such as ITAR/EAR and national licensing to speed approvals. Faster field support from local MROs can raise fleet availability by an estimated 10–20% and cut AOG response times substantially, improving competitiveness in tenders.

- Offset range: 30–60% local content

- Availability improvement: ~10–20%

- Key roles: export control navigation, licensing

- Value: faster AOG response, higher bid competitiveness

Defense demand fuels multi-year orders: $2.4T, 30–60% offsets

Defense ministries drive demand (global military spend ~$2.4T in 2024; US FY2024 ~$858B) and sign 5–7 year MoUs; avionics/EO/IR market ~$4B in 2024 with SATCOM LEO latency ~20–50 ms; NASA FY2024 $27.2B and DARPA ~$3.8B co-fund R&D; offset requirements 30–60% and local MROs raise availability ~10–20%.

| Partner | 2024/Metric | Impact |

|---|---|---|

| Defense | $2.4T global; US $858B | Multi-year orders |

| Avionics | $4B EO/IR | Integration wins |

| R&D | NASA $27.2B; DARPA $3.8B | Lowered innovation cost |

| Integrators | 30–60% offsets | Local assembly, +10–20% avail |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to an aeronautics company’s strategy, detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships with real-world operational insights and competitive analysis; ideal for presentations, funding discussions and decision-making, and includes SWOT-linked insights for validation and strategic planning.

High-level, editable Aeronautics Business Model Canvas that condenses strategy into a one-page snapshot, streamlining decision-making and removing hours spent formatting and aligning complex aerospace components.

Activities

UAS design & integration

Airframe, propulsion, avionics and payload integration form the core of UAS design & integration, with modular architectures enabling rapid customization and mission swaps; the global UAS market reached about $33.5 billion in 2024. Rigorous systems engineering (DO-178C/DO-254 practices) underpins reliability, while continuous V&V cycles and iterative testing measurably reduce mission risk and mean-time-between-failure.

Manufacturing & quality assurance

Serial production of platforms, GCS, and datalinks is executed under aerospace QA frameworks AS9100 and IPC standards, with AS9100 certification and IPC-A-610 criteria governing processes. Supply chain orchestration, including dual sourcing and inventory buffers, mitigates component risk. 100% of builds undergo factory acceptance tests to ensure conformity and release readiness.

Software & autonomy development

Flight control, mission planning, CV/AI and cyber hardening are developed in-house with agile sprints (commonly two-week iterations) to deliver rapid feature releases. Digital twins plus HIL/SIL testing are used for verification and robustness in avionics development. Secure OTA updates sustain deployed fleets; OTA has been standard in automotive since 2012 and is increasingly adopted across aerospace in 2024.

Training & lifecycle support

- 2024 global aerospace MRO market ~86B USD

- Training reduces operational incidents and fuel-inefficiencies

- Depot/field maintenance targets >90% fleet availability

- Remote diagnostics cut AOG response times significantly

Certification & compliance

Certification & compliance coordinates airworthiness, spectrum allocation and export regimes, aligning FAA/EASA pathways and the Wassenaar Arrangement (42 participating states in 2024). STANAG, MIL-STD (eg MIL-STD-810) and local aviation rules are integrated; cyber and safety cases are documented to accepted standards. Independent audits (ISO/AS9100) sustain market access and export approvals.

- Airworthiness

- Spectrum

- Export regimes

- STANAG/MIL-STD/local rules

- Cyber & safety cases

- Independent audits

Modular UAS, DO-178C/DO-254 & AS9100 reduce mission risk; market $33.5B

Airframe, propulsion, avionics integration with modular design and DO-178C/DO-254 systems engineering reduce mission risk; global UAS market ~33.5B (2024). Serial production follows AS9100/IPC; dual sourcing and FATs ensure readiness; MRO market ~86B (2024), fleet availability >90%. In-house CV/AI, HIL/SIL, OTA updates and training sustain ops and lower AOG.

| Metric | 2024 |

|---|---|

| UAS market | $33.5B |

| MRO market | $86B |

| Fleet availability | >90% |

| Wassenaar states | 42 |

Full Version Awaits

Business Model Canvas

The Aeronautics Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the full structure and content you’ll receive after purchase. When you complete your order you’ll download this same editable file, ready for presentation, analysis, and customization. No placeholders or hidden sections—what you see is the real document in its delivered form.

Description

Strategic Business Model Canvas: Uncover revenue levers, cost drivers and scaling paths

Unlock the full strategic blueprint behind Aeronautics’s business model and discover how it creates competitive value across customers, partners, and operations. This concise canvas reveals revenue levers, cost drivers, and scaling pathways in actionable detail. Ideal for investors, strategists, and founders seeking a ready-to-use framework—download the complete Business Model Canvas to apply these insights today.

Partnerships

Defense ministries & agencies

Defense ministries and agencies define platform requirements, certify airworthiness and doctrine alignment, and drive multi-year procurement that often represents the bulk of military aeronautics demand; global military spending reached about $2.4 trillion in 2024 while US FY2024 defense appropriations were roughly $858 billion. These partners validate operational needs and grant access to controlled airspace and test ranges critical for flight testing. Long-term MoUs and framework agreements, typically 5–7 year cycles, stabilize revenue visibility and enable production planning. Collaboration accelerates certification timelines and secures recurring sustainment contracts.

Avionics & sensor OEMs

Partner with avionics and sensor OEMs for EO/IR gimbals, SAR, SIGINT and navigation modules to tap into the $4B EO/IR payload market in 2024 and broader avionics procurements. Joint roadmaps guarantee payload compatibility and sustain performance leadership. Co-marketing lifted win rates ~15% in 2024 industry benchmarks. Shared testing cut integration risk and trimmed time-to-market by ~30% (e.g., 18 to 12 months).

Communications & datalink providers

Communications and datalink providers co-develop or license secure C2, SATCOM (LEO latency ~20–50 ms in 2024) and mesh networking to deliver beyond-line-of-sight redundancy. Partners ensure interoperability and crypto compliance (FIPS 140-3, NSA CSfC) across stacks. SLAs guarantee mission-critical uptime, commonly 99.99% or higher, supporting continuous ops.

Academic & R&D institutions

Universities and national labs drive autonomy, AI, and advanced materials R&D for aeronautics, leveraging NASA’s FY2024 budget of $27.2B and DARPA’s ~3.8B FY2024 budget to co-fund programs; grants and joint projects materially lower innovation costs and risk while shared test facilities speed prototype validation and regulatory certification timelines. Talent pipelines from these institutions supply niche hires for avionics, ML, and composites.

- Co-funding: NASA FY2024 27.2B

- DARPA FY2024 ~3.8B

- Shared testbeds accelerate validation

- University graduates feed niche talent pipelines

Local integrators & MRO partners

Local integrators and MRO partners enable in‑country assembly, offset delivery (offset requirements commonly mandate 30–60% local content), and sustainment, easing export controls such as ITAR/EAR and national licensing to speed approvals. Faster field support from local MROs can raise fleet availability by an estimated 10–20% and cut AOG response times substantially, improving competitiveness in tenders.

- Offset range: 30–60% local content

- Availability improvement: ~10–20%

- Key roles: export control navigation, licensing

- Value: faster AOG response, higher bid competitiveness

Defense demand fuels multi-year orders: $2.4T, 30–60% offsets

Defense ministries drive demand (global military spend ~$2.4T in 2024; US FY2024 ~$858B) and sign 5–7 year MoUs; avionics/EO/IR market ~$4B in 2024 with SATCOM LEO latency ~20–50 ms; NASA FY2024 $27.2B and DARPA ~$3.8B co-fund R&D; offset requirements 30–60% and local MROs raise availability ~10–20%.

| Partner | 2024/Metric | Impact |

|---|---|---|

| Defense | $2.4T global; US $858B | Multi-year orders |

| Avionics | $4B EO/IR | Integration wins |

| R&D | NASA $27.2B; DARPA $3.8B | Lowered innovation cost |

| Integrators | 30–60% offsets | Local assembly, +10–20% avail |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to an aeronautics company’s strategy, detailing customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure and customer relationships with real-world operational insights and competitive analysis; ideal for presentations, funding discussions and decision-making, and includes SWOT-linked insights for validation and strategic planning.

High-level, editable Aeronautics Business Model Canvas that condenses strategy into a one-page snapshot, streamlining decision-making and removing hours spent formatting and aligning complex aerospace components.

Activities

UAS design & integration

Airframe, propulsion, avionics and payload integration form the core of UAS design & integration, with modular architectures enabling rapid customization and mission swaps; the global UAS market reached about $33.5 billion in 2024. Rigorous systems engineering (DO-178C/DO-254 practices) underpins reliability, while continuous V&V cycles and iterative testing measurably reduce mission risk and mean-time-between-failure.

Manufacturing & quality assurance

Serial production of platforms, GCS, and datalinks is executed under aerospace QA frameworks AS9100 and IPC standards, with AS9100 certification and IPC-A-610 criteria governing processes. Supply chain orchestration, including dual sourcing and inventory buffers, mitigates component risk. 100% of builds undergo factory acceptance tests to ensure conformity and release readiness.

Software & autonomy development

Flight control, mission planning, CV/AI and cyber hardening are developed in-house with agile sprints (commonly two-week iterations) to deliver rapid feature releases. Digital twins plus HIL/SIL testing are used for verification and robustness in avionics development. Secure OTA updates sustain deployed fleets; OTA has been standard in automotive since 2012 and is increasingly adopted across aerospace in 2024.

Training & lifecycle support

- 2024 global aerospace MRO market ~86B USD

- Training reduces operational incidents and fuel-inefficiencies

- Depot/field maintenance targets >90% fleet availability

- Remote diagnostics cut AOG response times significantly

Certification & compliance

Certification & compliance coordinates airworthiness, spectrum allocation and export regimes, aligning FAA/EASA pathways and the Wassenaar Arrangement (42 participating states in 2024). STANAG, MIL-STD (eg MIL-STD-810) and local aviation rules are integrated; cyber and safety cases are documented to accepted standards. Independent audits (ISO/AS9100) sustain market access and export approvals.

- Airworthiness

- Spectrum

- Export regimes

- STANAG/MIL-STD/local rules

- Cyber & safety cases

- Independent audits

Modular UAS, DO-178C/DO-254 & AS9100 reduce mission risk; market $33.5B

Airframe, propulsion, avionics integration with modular design and DO-178C/DO-254 systems engineering reduce mission risk; global UAS market ~33.5B (2024). Serial production follows AS9100/IPC; dual sourcing and FATs ensure readiness; MRO market ~86B (2024), fleet availability >90%. In-house CV/AI, HIL/SIL, OTA updates and training sustain ops and lower AOG.

| Metric | 2024 |

|---|---|

| UAS market | $33.5B |

| MRO market | $86B |

| Fleet availability | >90% |

| Wassenaar states | 42 |

Full Version Awaits

Business Model Canvas

The Aeronautics Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the full structure and content you’ll receive after purchase. When you complete your order you’ll download this same editable file, ready for presentation, analysis, and customization. No placeholders or hidden sections—what you see is the real document in its delivered form.