AES Porter's Five Forces Analysis

Don't Miss the Bigger Picture

AES faces moderate supplier power, rising competition from renewables, and evolving regulatory pressures that reshape margins and strategic choices; buyer leverage and substitute threats vary by region and service mix. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to AES.

Suppliers Bargaining Power

Concentrated OEMs for turbines and batteries

Major equipment is concentrated: top wind OEMs (Vestas, Siemens Gamesa, GE) held ~68% of 2024 installations and top battery cell makers (CATL, LGES, BYD, Panasonic, SK On) ~85% of 2024 capacity, giving suppliers pricing and delivery power. Long lead times (turbines 12–30 months, batteries 6–12 months) raise switching costs. AES mitigates via multi-vendor frameworks, long-term master supply agreements and co-investments (AES co-founded Fluence) but dependence persists.

Fuel and commodity suppliers

Gas and coal suppliers exert leverage via price volatility and transport constraints, with Henry Hub averaging about $2.80/MMBtu in 2024 and spot coal remaining intermittently tight. Indexed fuel contracts pass through some costs but not exposure to sudden spikes. AES’s pivot to renewables and storage (growing to ~30 GW by 2024) reduces long-run fuel dependence, though regional pipeline capacity still shapes dispatch economics.

Grid access and interconnection providers

Transmission operators and ISOs act as bottleneck suppliers, controlling interconnection timing and cost—US interconnection queues exceeded 2,000 GW in 2024 and average wait times of 3–7 years. Queue backlogs and upgrade fees, often ranging from tens to over 100 million dollars per project, can delay cash flows and compress returns. AES needs early queue positions and grid-friendly designs to lower curtailment and re-study risk. Shifts in cost-allocation rules at FERC and state levels can materially change project viability.

EPC and critical balance-of-plant contractors

EPC capacity cycles give suppliers leverage when demand climbs and labor tightness rises; in 2024 skilled-labor shortfalls in key markets were reported at roughly 10–15%, boosting bid premiums. Fixed-price EPC contracts shift execution risk to contractors but increase change-order pressure and margin volatility. AES mitigates this via repeatable designs and preferred-contractor panels and faces localization and labor-rule constraints in certain countries.

- EPC cycles: higher supplier leverage

- 2024 labor tightness ~10–15%

- Fixed-price → change-order risk

- AES: repeatable designs, preferred panels

- Localization/labor rules limit options

Materials and component inputs

Supplier concentration and long lead times drive cost risk in renewables and storage

Suppliers hold strong leverage: top wind OEMs ~68% share and top battery cell makers ~85% of 2024 capacity, long lead times raise switching costs; AES mitigates via multi-vendor deals and partnerships. Fuel and grid suppliers can swing costs—Henry Hub ~2.80 USD/MMBtu (2024); US interconnection queue >2,000 GW. Commodity pressure persists: copper ~9,000 USD/ton (2024).

| Metric | 2024 |

|---|---|

| Top wind OEM share | ~68% |

| Top battery cell share | ~85% |

| Henry Hub | ~2.80 USD/MMBtu |

| US interconnection queue | >2,000 GW |

| Copper price | ~9,000 USD/ton |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitutes, and entry barriers specific to AES, highlighting disruptive threats, market dynamics that protect incumbents, and actionable insights for strategic and investor use.

A concise, one-sheet Porter's Five Forces for AES that visualizes competitive pressure with an editable radar chart for quick strategic decisions. No macros and fully customizable labels/scenarios—drop into decks or dashboards to eliminate analysis bottlenecks.

Customers Bargaining Power

Utility and offtaker concentration

Large utilities, governments and corporate offtakers negotiate PPAs with significant leverage, and concentrated offtaker pools force AES to match aggressive terms. Competitive tenders and auctions pushed utility-scale solar PPA lows to roughly $20–30/MWh in 2024, intensifying price pressure. AES counters with differentiated solutions, a reliability track record and bundled services. Creditworthy counterparties reduce counterparty risk but demand sharper pricing.

Price sensitivity and renewable auctions

Reverse auctions (BNEF 2024: corporate PPA avg ~USD 30/MWh) compress bid prices and margins as buyers compare many similar-technology offers, forcing AES to sharpen cost of capital and construction execution to win without destroying value. Effective hedging and solar-plus-storage hybridization — storage premiums reported up to ~USD 20/MWh — can secure premium pricing and differentiate AES offers.

Switching and termination clauses

Long-term contracts (typically 10–25 years) create customer stickiness for AES but include performance, curtailment and termination provisions that keep buyers' leverage alive. Buyers exert power via strict SLAs and penalties often in the 5–10% range of contract value. AES mitigates risk through robust O&M, performance guarantees and risk-sharing clauses. Broad portfolio diversification reduces exposure to any single buyer or market.

Green attributes and customization

C&I buyers increasingly demand 24/7 carbon-free profiles and flexible delivery; AES in 2024 used roughly 5 GW of battery storage, software platforms and virtual PPAs to tailor solutions, raising switching costs but lengthening sales cycles as customization becomes table stakes.

Buyers now expect transparent emissions intensity data in procurement, shifting power toward sophisticated purchasers who value verified hourly carbon metrics.

- 24/7 carbon-free demand: rising expectation

- AES 2024: ~5 GW storage + software + vPPAs

- Customization increases value and switching costs

- Emissions transparency (hourly) now expected

Regulatory and tariff influence

Regulated buyers shape tariffs, interconnection rules and curtailment practices, directly affecting AES project revenues and dispatch economics. Policy-driven procurements—capacity markets, long-term PPAs and clean energy tenders—often embed buyer priorities that shift pricing and risk to suppliers. AES participates in policy and stakeholder processes to mitigate adverse terms and align procurements with commercial viability. Stable regulation reduces buyer opportunism and lowers financing costs for AES projects.

- Regulatory tariffs determine dispatch and revenue certainty

- Procurements set contract length and risk allocation

- AES engages regulators to protect project bankability

PPAs at USD 20–30/MWh; storage and SLA premiums up to USD 20/MWh

Large utility and corporate buyers exert high leverage: competitive tenders pushed utility-scale solar PPAs to ~USD 20–30/MWh in 2024 (BNEF corporate avg ~USD 30/MWh), compressing margins. AES counters with ~5 GW storage, bundled services and 24/7 offers; storage premiums up to ~USD 20/MWh and SLAs/penalties (5–10%) shape pricing. Buyers demand hourly emissions transparency and long-term contracts (10–25 yrs) that both lock and constrain AES.

| Metric | 2024 Value |

|---|---|

| Utility-scale PPA | USD 20–30/MWh |

| Corporate PPA avg (BNEF) | ~USD 30/MWh |

| AES storage capacity | ~5 GW |

| Storage premium | Up to USD 20/MWh |

| SLA penalties | 5–10% of contract value |

Preview Before You Purchase

AES Porter's Five Forces Analysis

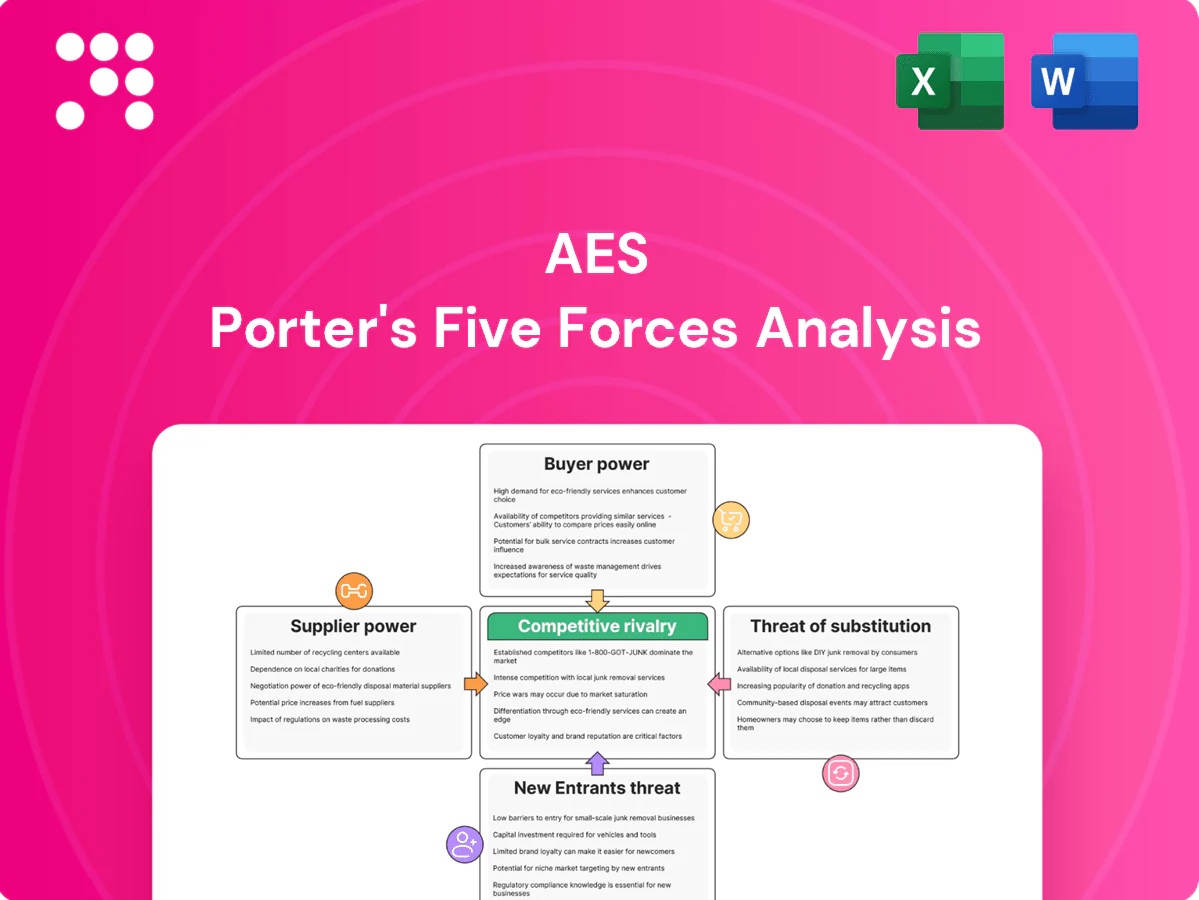

This preview shows the exact AES Porter's Five Forces analysis you’ll receive after purchase—no placeholders, no mockups. It’s the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes. Purchase grants immediate access to this same ready-to-use file.

Don't Miss the Bigger Picture

AES faces moderate supplier power, rising competition from renewables, and evolving regulatory pressures that reshape margins and strategic choices; buyer leverage and substitute threats vary by region and service mix. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to AES.

Suppliers Bargaining Power

Concentrated OEMs for turbines and batteries

Major equipment is concentrated: top wind OEMs (Vestas, Siemens Gamesa, GE) held ~68% of 2024 installations and top battery cell makers (CATL, LGES, BYD, Panasonic, SK On) ~85% of 2024 capacity, giving suppliers pricing and delivery power. Long lead times (turbines 12–30 months, batteries 6–12 months) raise switching costs. AES mitigates via multi-vendor frameworks, long-term master supply agreements and co-investments (AES co-founded Fluence) but dependence persists.

Fuel and commodity suppliers

Gas and coal suppliers exert leverage via price volatility and transport constraints, with Henry Hub averaging about $2.80/MMBtu in 2024 and spot coal remaining intermittently tight. Indexed fuel contracts pass through some costs but not exposure to sudden spikes. AES’s pivot to renewables and storage (growing to ~30 GW by 2024) reduces long-run fuel dependence, though regional pipeline capacity still shapes dispatch economics.

Grid access and interconnection providers

Transmission operators and ISOs act as bottleneck suppliers, controlling interconnection timing and cost—US interconnection queues exceeded 2,000 GW in 2024 and average wait times of 3–7 years. Queue backlogs and upgrade fees, often ranging from tens to over 100 million dollars per project, can delay cash flows and compress returns. AES needs early queue positions and grid-friendly designs to lower curtailment and re-study risk. Shifts in cost-allocation rules at FERC and state levels can materially change project viability.

EPC and critical balance-of-plant contractors

EPC capacity cycles give suppliers leverage when demand climbs and labor tightness rises; in 2024 skilled-labor shortfalls in key markets were reported at roughly 10–15%, boosting bid premiums. Fixed-price EPC contracts shift execution risk to contractors but increase change-order pressure and margin volatility. AES mitigates this via repeatable designs and preferred-contractor panels and faces localization and labor-rule constraints in certain countries.

- EPC cycles: higher supplier leverage

- 2024 labor tightness ~10–15%

- Fixed-price → change-order risk

- AES: repeatable designs, preferred panels

- Localization/labor rules limit options

Materials and component inputs

Supplier concentration and long lead times drive cost risk in renewables and storage

Suppliers hold strong leverage: top wind OEMs ~68% share and top battery cell makers ~85% of 2024 capacity, long lead times raise switching costs; AES mitigates via multi-vendor deals and partnerships. Fuel and grid suppliers can swing costs—Henry Hub ~2.80 USD/MMBtu (2024); US interconnection queue >2,000 GW. Commodity pressure persists: copper ~9,000 USD/ton (2024).

| Metric | 2024 |

|---|---|

| Top wind OEM share | ~68% |

| Top battery cell share | ~85% |

| Henry Hub | ~2.80 USD/MMBtu |

| US interconnection queue | >2,000 GW |

| Copper price | ~9,000 USD/ton |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitutes, and entry barriers specific to AES, highlighting disruptive threats, market dynamics that protect incumbents, and actionable insights for strategic and investor use.

A concise, one-sheet Porter's Five Forces for AES that visualizes competitive pressure with an editable radar chart for quick strategic decisions. No macros and fully customizable labels/scenarios—drop into decks or dashboards to eliminate analysis bottlenecks.

Customers Bargaining Power

Utility and offtaker concentration

Large utilities, governments and corporate offtakers negotiate PPAs with significant leverage, and concentrated offtaker pools force AES to match aggressive terms. Competitive tenders and auctions pushed utility-scale solar PPA lows to roughly $20–30/MWh in 2024, intensifying price pressure. AES counters with differentiated solutions, a reliability track record and bundled services. Creditworthy counterparties reduce counterparty risk but demand sharper pricing.

Price sensitivity and renewable auctions

Reverse auctions (BNEF 2024: corporate PPA avg ~USD 30/MWh) compress bid prices and margins as buyers compare many similar-technology offers, forcing AES to sharpen cost of capital and construction execution to win without destroying value. Effective hedging and solar-plus-storage hybridization — storage premiums reported up to ~USD 20/MWh — can secure premium pricing and differentiate AES offers.

Switching and termination clauses

Long-term contracts (typically 10–25 years) create customer stickiness for AES but include performance, curtailment and termination provisions that keep buyers' leverage alive. Buyers exert power via strict SLAs and penalties often in the 5–10% range of contract value. AES mitigates risk through robust O&M, performance guarantees and risk-sharing clauses. Broad portfolio diversification reduces exposure to any single buyer or market.

Green attributes and customization

C&I buyers increasingly demand 24/7 carbon-free profiles and flexible delivery; AES in 2024 used roughly 5 GW of battery storage, software platforms and virtual PPAs to tailor solutions, raising switching costs but lengthening sales cycles as customization becomes table stakes.

Buyers now expect transparent emissions intensity data in procurement, shifting power toward sophisticated purchasers who value verified hourly carbon metrics.

- 24/7 carbon-free demand: rising expectation

- AES 2024: ~5 GW storage + software + vPPAs

- Customization increases value and switching costs

- Emissions transparency (hourly) now expected

Regulatory and tariff influence

Regulated buyers shape tariffs, interconnection rules and curtailment practices, directly affecting AES project revenues and dispatch economics. Policy-driven procurements—capacity markets, long-term PPAs and clean energy tenders—often embed buyer priorities that shift pricing and risk to suppliers. AES participates in policy and stakeholder processes to mitigate adverse terms and align procurements with commercial viability. Stable regulation reduces buyer opportunism and lowers financing costs for AES projects.

- Regulatory tariffs determine dispatch and revenue certainty

- Procurements set contract length and risk allocation

- AES engages regulators to protect project bankability

PPAs at USD 20–30/MWh; storage and SLA premiums up to USD 20/MWh

Large utility and corporate buyers exert high leverage: competitive tenders pushed utility-scale solar PPAs to ~USD 20–30/MWh in 2024 (BNEF corporate avg ~USD 30/MWh), compressing margins. AES counters with ~5 GW storage, bundled services and 24/7 offers; storage premiums up to ~USD 20/MWh and SLAs/penalties (5–10%) shape pricing. Buyers demand hourly emissions transparency and long-term contracts (10–25 yrs) that both lock and constrain AES.

| Metric | 2024 Value |

|---|---|

| Utility-scale PPA | USD 20–30/MWh |

| Corporate PPA avg (BNEF) | ~USD 30/MWh |

| AES storage capacity | ~5 GW |

| Storage premium | Up to USD 20/MWh |

| SLA penalties | 5–10% of contract value |

Preview Before You Purchase

AES Porter's Five Forces Analysis

This preview shows the exact AES Porter's Five Forces analysis you’ll receive after purchase—no placeholders, no mockups. It’s the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes. Purchase grants immediate access to this same ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

AES faces moderate supplier power, rising competition from renewables, and evolving regulatory pressures that reshape margins and strategic choices; buyer leverage and substitute threats vary by region and service mix. This snapshot highlights key tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to AES.

Suppliers Bargaining Power

Concentrated OEMs for turbines and batteries

Major equipment is concentrated: top wind OEMs (Vestas, Siemens Gamesa, GE) held ~68% of 2024 installations and top battery cell makers (CATL, LGES, BYD, Panasonic, SK On) ~85% of 2024 capacity, giving suppliers pricing and delivery power. Long lead times (turbines 12–30 months, batteries 6–12 months) raise switching costs. AES mitigates via multi-vendor frameworks, long-term master supply agreements and co-investments (AES co-founded Fluence) but dependence persists.

Fuel and commodity suppliers

Gas and coal suppliers exert leverage via price volatility and transport constraints, with Henry Hub averaging about $2.80/MMBtu in 2024 and spot coal remaining intermittently tight. Indexed fuel contracts pass through some costs but not exposure to sudden spikes. AES’s pivot to renewables and storage (growing to ~30 GW by 2024) reduces long-run fuel dependence, though regional pipeline capacity still shapes dispatch economics.

Grid access and interconnection providers

Transmission operators and ISOs act as bottleneck suppliers, controlling interconnection timing and cost—US interconnection queues exceeded 2,000 GW in 2024 and average wait times of 3–7 years. Queue backlogs and upgrade fees, often ranging from tens to over 100 million dollars per project, can delay cash flows and compress returns. AES needs early queue positions and grid-friendly designs to lower curtailment and re-study risk. Shifts in cost-allocation rules at FERC and state levels can materially change project viability.

EPC and critical balance-of-plant contractors

EPC capacity cycles give suppliers leverage when demand climbs and labor tightness rises; in 2024 skilled-labor shortfalls in key markets were reported at roughly 10–15%, boosting bid premiums. Fixed-price EPC contracts shift execution risk to contractors but increase change-order pressure and margin volatility. AES mitigates this via repeatable designs and preferred-contractor panels and faces localization and labor-rule constraints in certain countries.

- EPC cycles: higher supplier leverage

- 2024 labor tightness ~10–15%

- Fixed-price → change-order risk

- AES: repeatable designs, preferred panels

- Localization/labor rules limit options

Materials and component inputs

Supplier concentration and long lead times drive cost risk in renewables and storage

Suppliers hold strong leverage: top wind OEMs ~68% share and top battery cell makers ~85% of 2024 capacity, long lead times raise switching costs; AES mitigates via multi-vendor deals and partnerships. Fuel and grid suppliers can swing costs—Henry Hub ~2.80 USD/MMBtu (2024); US interconnection queue >2,000 GW. Commodity pressure persists: copper ~9,000 USD/ton (2024).

| Metric | 2024 |

|---|---|

| Top wind OEM share | ~68% |

| Top battery cell share | ~85% |

| Henry Hub | ~2.80 USD/MMBtu |

| US interconnection queue | >2,000 GW |

| Copper price | ~9,000 USD/ton |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, substitutes, and entry barriers specific to AES, highlighting disruptive threats, market dynamics that protect incumbents, and actionable insights for strategic and investor use.

A concise, one-sheet Porter's Five Forces for AES that visualizes competitive pressure with an editable radar chart for quick strategic decisions. No macros and fully customizable labels/scenarios—drop into decks or dashboards to eliminate analysis bottlenecks.

Customers Bargaining Power

Utility and offtaker concentration

Large utilities, governments and corporate offtakers negotiate PPAs with significant leverage, and concentrated offtaker pools force AES to match aggressive terms. Competitive tenders and auctions pushed utility-scale solar PPA lows to roughly $20–30/MWh in 2024, intensifying price pressure. AES counters with differentiated solutions, a reliability track record and bundled services. Creditworthy counterparties reduce counterparty risk but demand sharper pricing.

Price sensitivity and renewable auctions

Reverse auctions (BNEF 2024: corporate PPA avg ~USD 30/MWh) compress bid prices and margins as buyers compare many similar-technology offers, forcing AES to sharpen cost of capital and construction execution to win without destroying value. Effective hedging and solar-plus-storage hybridization — storage premiums reported up to ~USD 20/MWh — can secure premium pricing and differentiate AES offers.

Switching and termination clauses

Long-term contracts (typically 10–25 years) create customer stickiness for AES but include performance, curtailment and termination provisions that keep buyers' leverage alive. Buyers exert power via strict SLAs and penalties often in the 5–10% range of contract value. AES mitigates risk through robust O&M, performance guarantees and risk-sharing clauses. Broad portfolio diversification reduces exposure to any single buyer or market.

Green attributes and customization

C&I buyers increasingly demand 24/7 carbon-free profiles and flexible delivery; AES in 2024 used roughly 5 GW of battery storage, software platforms and virtual PPAs to tailor solutions, raising switching costs but lengthening sales cycles as customization becomes table stakes.

Buyers now expect transparent emissions intensity data in procurement, shifting power toward sophisticated purchasers who value verified hourly carbon metrics.

- 24/7 carbon-free demand: rising expectation

- AES 2024: ~5 GW storage + software + vPPAs

- Customization increases value and switching costs

- Emissions transparency (hourly) now expected

Regulatory and tariff influence

Regulated buyers shape tariffs, interconnection rules and curtailment practices, directly affecting AES project revenues and dispatch economics. Policy-driven procurements—capacity markets, long-term PPAs and clean energy tenders—often embed buyer priorities that shift pricing and risk to suppliers. AES participates in policy and stakeholder processes to mitigate adverse terms and align procurements with commercial viability. Stable regulation reduces buyer opportunism and lowers financing costs for AES projects.

- Regulatory tariffs determine dispatch and revenue certainty

- Procurements set contract length and risk allocation

- AES engages regulators to protect project bankability

PPAs at USD 20–30/MWh; storage and SLA premiums up to USD 20/MWh

Large utility and corporate buyers exert high leverage: competitive tenders pushed utility-scale solar PPAs to ~USD 20–30/MWh in 2024 (BNEF corporate avg ~USD 30/MWh), compressing margins. AES counters with ~5 GW storage, bundled services and 24/7 offers; storage premiums up to ~USD 20/MWh and SLAs/penalties (5–10%) shape pricing. Buyers demand hourly emissions transparency and long-term contracts (10–25 yrs) that both lock and constrain AES.

| Metric | 2024 Value |

|---|---|

| Utility-scale PPA | USD 20–30/MWh |

| Corporate PPA avg (BNEF) | ~USD 30/MWh |

| AES storage capacity | ~5 GW |

| Storage premium | Up to USD 20/MWh |

| SLA penalties | 5–10% of contract value |

Preview Before You Purchase

AES Porter's Five Forces Analysis

This preview shows the exact AES Porter's Five Forces analysis you’ll receive after purchase—no placeholders, no mockups. It’s the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threat of new entrants, and substitutes. Purchase grants immediate access to this same ready-to-use file.