Advanced Fiber Resources (Zhuhai) Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

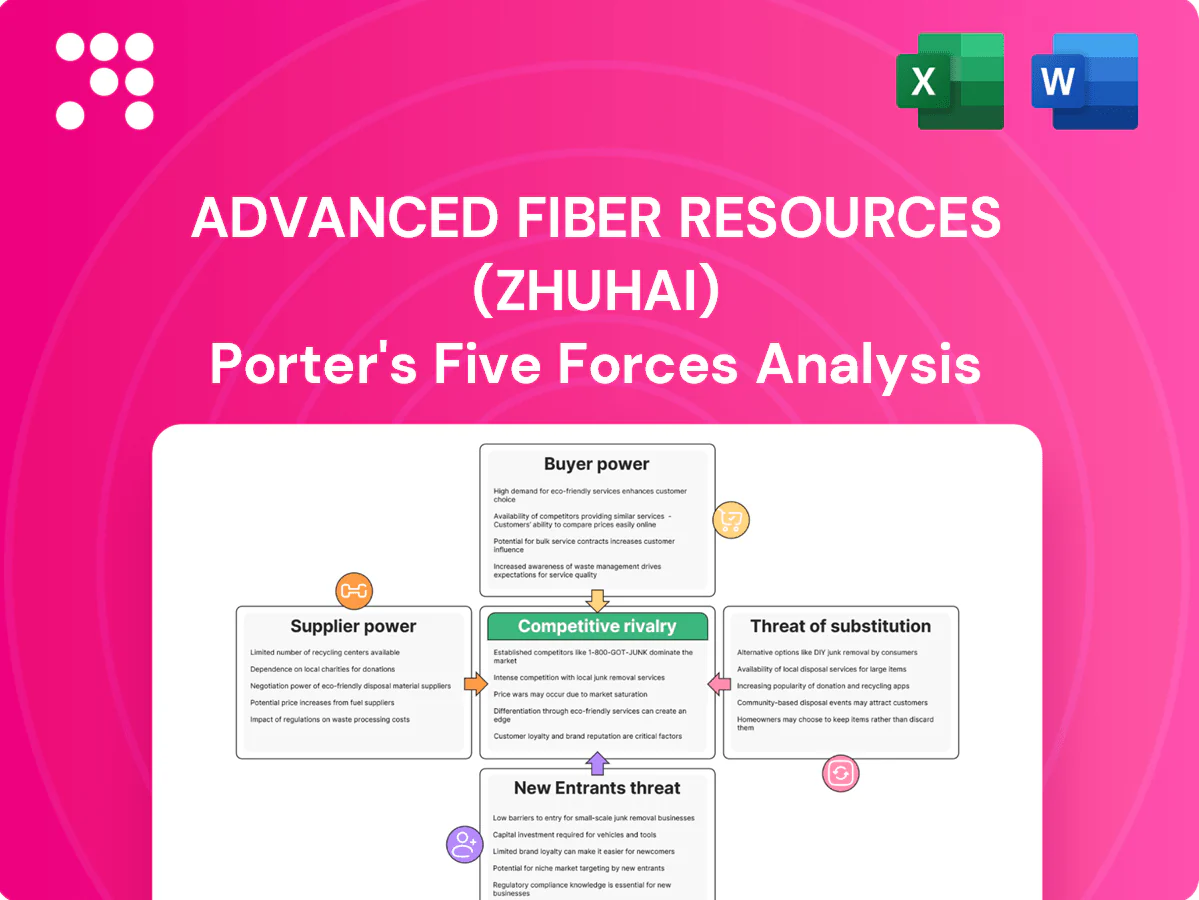

Advanced Fiber Resources (Zhuhai) faces moderate supplier power, rising buyer sophistication, and intensifying rivalry as capacity grows. Regulatory shifts and feedstock volatility increase strategic risk and margin pressure. Substitutes and moderate entry barriers further complicate long-term forecasting. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Advanced Fiber Resources (Zhuhai)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty fiber & glass concentration

High-purity fiber preforms, rare-earth–doped fibers and specialty glasses are sourced from a very small pool of qualified vendors, with the top five suppliers controlling roughly 60–70% of global supply in 2024, giving them leverage over 12–20 week lead times and pricing. AFR reduces risk via dual-sourcing and multi-year supply agreements but qualification cycles typically take 6–12 months. Any upstream disruption can directly throttle high-power component output.

Precision ceramics & coatings

Precision ceramics, isolator crystals and high-damage-threshold coatings are specification-heavy niches where suppliers with proprietary processes often command price premiums (commonly up to 20%) and long lead times; supplier yield variability (often causing >10% unit-cost swings) directly raises AFR Zhuhai’s COGS and delivery risk. Close process control, supplier audits and joint development programs materially reduce information asymmetry and stabilize yields and margins.

Semiconductor pump diodes

Pump laser diodes are critical to fiber lasers and amplifiers, with performance and reliability tightly vendor-linked; key suppliers in 2024 include II‑VI/Coherent, Lumentum, NICHIA and ams OSRAM, who set technical roadmaps and allocation priorities. A handful of global makers control sourcing windows and can shift price and availability with telecom/datacenter cycles. AFR secures lower unit costs via volume commitments but remains exposed to allocation risk and lead‑time variability.

Equipment & metrology dependence

Splicers, precision alignment rigs and interferometric test gear come from a concentrated set of OEMs (typically 3–5 suppliers), giving those vendors meaningful leverage; annual calibration cycles and multi-year service contracts raise switching costs and recurring spend. Major tool upgrades can lock AFR into OEM ecosystems through proprietary consumables and software, while strategic CAPEX timing and targeted in-house fixturing reduce supplier dependence.

- Concentrated OEM base: 3–5 suppliers

- Calibration cadence: typically annual

- Service contracts: increase switching costs

- Mitigation: CAPEX planning, in-house fixturing

Logistics & geopolitical exposure

Export-control expansions in 2024 tightened cross-border flows for photonics inputs, raising compliance risk and enabling suppliers to pass through higher costs to AFR; container freight volatility persisted despite a post-2022 decline, keeping landed-cost uncertainty elevated.

- Supply concentration: regional hubs increase resilience

- Cost drivers: tariffs, compliance pass‑through

- Mitigants: buffer stocks, dual sourcing

Top-five suppliers hold 60–70% of fiber; 12–20w lead times constrain output

Top-five suppliers control ~60–70% of high-purity fiber supply in 2024, with 12–20 week lead times that can throttle AFR output. Specialty items carry price premiums up to 20% and yield variability >10%, while pump diodes (II‑VI/Coherent, Lumentum, NICHIA, ams OSRAM) govern allocations. AFR mitigates via dual-sourcing, multi‑year contracts, buffer stock and 6–12 month qualification cycles.

| Component | Concentration | Metrics (2024) | Mitigant |

|---|---|---|---|

| Fiber preforms | Top5 60–70% | Lead 12–20w | Dual-source |

| Pump diodes | 4 majors | Allocation risk | Volume commits |

| Test gear | 3–5 OEMs | Annual cal | In-house fixtures |

What is included in the product

Provides a focused Porter's Five Forces assessment of Advanced Fiber Resources (Zhuhai), identifying competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers, with industry data and strategic implications to inform investor and management decisions.

Clear, one-sheet Porter’s Five Forces for Advanced Fiber Resources (Zhuhai) — concise pressure mapping and spider chart to pinpoint supplier/customer risks, entry threats and regulatory exposure, ready for pitch decks and simple to update with new market data.

Customers Bargaining Power

Large OEMs with volume leverage

Large OEMs in fiber laser, telecom and datacenter sectors buy at scale and enforce tight SLAs, using volume leverage to push pricing, extended payment terms and bespoke specs. Hyperscalers and major telcos—whose combined cloud/datacenter capex approached roughly $90 billion annually in the 2023–24 period—amplify this pressure. Losing a single key account can reduce factory utilization materially, so AFR must balance customer customization against platform economies to protect margins.

High qualification & switching costs

In 2024 AFR (Zhuhai) faces 12–24 month design-in cycles and rigorous reliability qualifications that drive switching costs (requalification often costing $0.5–5m), so buyers negotiate price post-qualification but rarely switch; AFR can trade performance for margin resilience, yet 60–70% of sophisticated OEMs maintain dual-qualification.

Price transparency in commoditized lines

Standard passive components are instantly price-benchmarked via 2024 distributor portals such as Digi-Key, Mouser and Avnet, enabling buyers to pit vendors and compress margins. AFR offsets this by selling performance-binned parts, value-added assemblies and bundled warranties that preserve higher ASPs. Despite this, spot bids on commoditized SKUs remain intensely competitive and price-driven.

Custom engineering requests

Enterprise customers demand bespoke wavelength, power-handling and packaging; custom NREs (typically tens to low hundreds of thousands USD) can offset margin pressure but commonly extend lead times by 4–12 weeks and raise delivery risk. Clear scope control and modular design lower cost-to-serve (~20% savings), while strong applications engineering increases customer stickiness and upsell rates.

- Custom NRE: tens–low hundreds k USD

- Lead-time impact: +4–12 weeks

- Cost-to-serve cut: ~20%

- Apps eng. boosts retention/upsell

Demand cyclicality

Capex cycles in lasers, telecom and datacenters drive volatile orders; global datacenter capex was about $200B in 2024 and telecom capex roughly $250B, creating demand swings where order volumes can shift >20% between peaks and troughs.

Buyers frequently cancel or defer to extract concessions, so AFR must keep agile capacity, strict ASP discipline and pursue framework agreements with take-or-pay clauses to stabilize volumes.

- Demand swing: >20% between cycles (2024)

- Datacenter capex: ≈$200B (2024)

- Telecom capex: ≈$250B (2024)

- Mitigants: agility, ASP discipline, take-or-pay contracts

Hyperscalers $90B capex and 12-24m design-ins raise OEM switching costs

Large OEMs and hyperscalers (≈$90B cloud/datacenter capex 2023–24) exert strong price and SLA leverage; losing a key account risks utilization. Long 12–24 month design-ins and $0.5–5m requalification raise switching costs; 60–70% of OEMs dual-qualify. Commoditized SKUs face spot-price pressure; bespoke NREs (tens–low hundreds k USD) and apps engineering preserve ASPs and stickiness.

| Metric | 2024 Value |

|---|---|

| Cloud/DC capex | $200B |

| Telecom capex | $250B |

| Hyperscaler cloud/DC spend | $90B |

| Requalification cost | $0.5–5M |

| NRE | tens–low hundreds k USD |

| Dual-qualify rate | 60–70% |

Preview Before You Purchase

Advanced Fiber Resources (Zhuhai) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Advanced Fiber Resources (Zhuhai) you'll receive—comprehensive evaluation of competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes. The document is fully formatted, ready to download and use immediately after purchase with no placeholders or mockups. Use it for strategic planning, investment review, or competitive benchmarking—what you see is what you get.

A Must-Have Tool for Decision-Makers

Advanced Fiber Resources (Zhuhai) faces moderate supplier power, rising buyer sophistication, and intensifying rivalry as capacity grows. Regulatory shifts and feedstock volatility increase strategic risk and margin pressure. Substitutes and moderate entry barriers further complicate long-term forecasting. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Advanced Fiber Resources (Zhuhai)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty fiber & glass concentration

High-purity fiber preforms, rare-earth–doped fibers and specialty glasses are sourced from a very small pool of qualified vendors, with the top five suppliers controlling roughly 60–70% of global supply in 2024, giving them leverage over 12–20 week lead times and pricing. AFR reduces risk via dual-sourcing and multi-year supply agreements but qualification cycles typically take 6–12 months. Any upstream disruption can directly throttle high-power component output.

Precision ceramics & coatings

Precision ceramics, isolator crystals and high-damage-threshold coatings are specification-heavy niches where suppliers with proprietary processes often command price premiums (commonly up to 20%) and long lead times; supplier yield variability (often causing >10% unit-cost swings) directly raises AFR Zhuhai’s COGS and delivery risk. Close process control, supplier audits and joint development programs materially reduce information asymmetry and stabilize yields and margins.

Semiconductor pump diodes

Pump laser diodes are critical to fiber lasers and amplifiers, with performance and reliability tightly vendor-linked; key suppliers in 2024 include II‑VI/Coherent, Lumentum, NICHIA and ams OSRAM, who set technical roadmaps and allocation priorities. A handful of global makers control sourcing windows and can shift price and availability with telecom/datacenter cycles. AFR secures lower unit costs via volume commitments but remains exposed to allocation risk and lead‑time variability.

Equipment & metrology dependence

Splicers, precision alignment rigs and interferometric test gear come from a concentrated set of OEMs (typically 3–5 suppliers), giving those vendors meaningful leverage; annual calibration cycles and multi-year service contracts raise switching costs and recurring spend. Major tool upgrades can lock AFR into OEM ecosystems through proprietary consumables and software, while strategic CAPEX timing and targeted in-house fixturing reduce supplier dependence.

- Concentrated OEM base: 3–5 suppliers

- Calibration cadence: typically annual

- Service contracts: increase switching costs

- Mitigation: CAPEX planning, in-house fixturing

Logistics & geopolitical exposure

Export-control expansions in 2024 tightened cross-border flows for photonics inputs, raising compliance risk and enabling suppliers to pass through higher costs to AFR; container freight volatility persisted despite a post-2022 decline, keeping landed-cost uncertainty elevated.

- Supply concentration: regional hubs increase resilience

- Cost drivers: tariffs, compliance pass‑through

- Mitigants: buffer stocks, dual sourcing

Top-five suppliers hold 60–70% of fiber; 12–20w lead times constrain output

Top-five suppliers control ~60–70% of high-purity fiber supply in 2024, with 12–20 week lead times that can throttle AFR output. Specialty items carry price premiums up to 20% and yield variability >10%, while pump diodes (II‑VI/Coherent, Lumentum, NICHIA, ams OSRAM) govern allocations. AFR mitigates via dual-sourcing, multi‑year contracts, buffer stock and 6–12 month qualification cycles.

| Component | Concentration | Metrics (2024) | Mitigant |

|---|---|---|---|

| Fiber preforms | Top5 60–70% | Lead 12–20w | Dual-source |

| Pump diodes | 4 majors | Allocation risk | Volume commits |

| Test gear | 3–5 OEMs | Annual cal | In-house fixtures |

What is included in the product

Provides a focused Porter's Five Forces assessment of Advanced Fiber Resources (Zhuhai), identifying competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers, with industry data and strategic implications to inform investor and management decisions.

Clear, one-sheet Porter’s Five Forces for Advanced Fiber Resources (Zhuhai) — concise pressure mapping and spider chart to pinpoint supplier/customer risks, entry threats and regulatory exposure, ready for pitch decks and simple to update with new market data.

Customers Bargaining Power

Large OEMs with volume leverage

Large OEMs in fiber laser, telecom and datacenter sectors buy at scale and enforce tight SLAs, using volume leverage to push pricing, extended payment terms and bespoke specs. Hyperscalers and major telcos—whose combined cloud/datacenter capex approached roughly $90 billion annually in the 2023–24 period—amplify this pressure. Losing a single key account can reduce factory utilization materially, so AFR must balance customer customization against platform economies to protect margins.

High qualification & switching costs

In 2024 AFR (Zhuhai) faces 12–24 month design-in cycles and rigorous reliability qualifications that drive switching costs (requalification often costing $0.5–5m), so buyers negotiate price post-qualification but rarely switch; AFR can trade performance for margin resilience, yet 60–70% of sophisticated OEMs maintain dual-qualification.

Price transparency in commoditized lines

Standard passive components are instantly price-benchmarked via 2024 distributor portals such as Digi-Key, Mouser and Avnet, enabling buyers to pit vendors and compress margins. AFR offsets this by selling performance-binned parts, value-added assemblies and bundled warranties that preserve higher ASPs. Despite this, spot bids on commoditized SKUs remain intensely competitive and price-driven.

Custom engineering requests

Enterprise customers demand bespoke wavelength, power-handling and packaging; custom NREs (typically tens to low hundreds of thousands USD) can offset margin pressure but commonly extend lead times by 4–12 weeks and raise delivery risk. Clear scope control and modular design lower cost-to-serve (~20% savings), while strong applications engineering increases customer stickiness and upsell rates.

- Custom NRE: tens–low hundreds k USD

- Lead-time impact: +4–12 weeks

- Cost-to-serve cut: ~20%

- Apps eng. boosts retention/upsell

Demand cyclicality

Capex cycles in lasers, telecom and datacenters drive volatile orders; global datacenter capex was about $200B in 2024 and telecom capex roughly $250B, creating demand swings where order volumes can shift >20% between peaks and troughs.

Buyers frequently cancel or defer to extract concessions, so AFR must keep agile capacity, strict ASP discipline and pursue framework agreements with take-or-pay clauses to stabilize volumes.

- Demand swing: >20% between cycles (2024)

- Datacenter capex: ≈$200B (2024)

- Telecom capex: ≈$250B (2024)

- Mitigants: agility, ASP discipline, take-or-pay contracts

Hyperscalers $90B capex and 12-24m design-ins raise OEM switching costs

Large OEMs and hyperscalers (≈$90B cloud/datacenter capex 2023–24) exert strong price and SLA leverage; losing a key account risks utilization. Long 12–24 month design-ins and $0.5–5m requalification raise switching costs; 60–70% of OEMs dual-qualify. Commoditized SKUs face spot-price pressure; bespoke NREs (tens–low hundreds k USD) and apps engineering preserve ASPs and stickiness.

| Metric | 2024 Value |

|---|---|

| Cloud/DC capex | $200B |

| Telecom capex | $250B |

| Hyperscaler cloud/DC spend | $90B |

| Requalification cost | $0.5–5M |

| NRE | tens–low hundreds k USD |

| Dual-qualify rate | 60–70% |

Preview Before You Purchase

Advanced Fiber Resources (Zhuhai) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Advanced Fiber Resources (Zhuhai) you'll receive—comprehensive evaluation of competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes. The document is fully formatted, ready to download and use immediately after purchase with no placeholders or mockups. Use it for strategic planning, investment review, or competitive benchmarking—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Advanced Fiber Resources (Zhuhai) faces moderate supplier power, rising buyer sophistication, and intensifying rivalry as capacity grows. Regulatory shifts and feedstock volatility increase strategic risk and margin pressure. Substitutes and moderate entry barriers further complicate long-term forecasting. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Advanced Fiber Resources (Zhuhai)’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialty fiber & glass concentration

High-purity fiber preforms, rare-earth–doped fibers and specialty glasses are sourced from a very small pool of qualified vendors, with the top five suppliers controlling roughly 60–70% of global supply in 2024, giving them leverage over 12–20 week lead times and pricing. AFR reduces risk via dual-sourcing and multi-year supply agreements but qualification cycles typically take 6–12 months. Any upstream disruption can directly throttle high-power component output.

Precision ceramics & coatings

Precision ceramics, isolator crystals and high-damage-threshold coatings are specification-heavy niches where suppliers with proprietary processes often command price premiums (commonly up to 20%) and long lead times; supplier yield variability (often causing >10% unit-cost swings) directly raises AFR Zhuhai’s COGS and delivery risk. Close process control, supplier audits and joint development programs materially reduce information asymmetry and stabilize yields and margins.

Semiconductor pump diodes

Pump laser diodes are critical to fiber lasers and amplifiers, with performance and reliability tightly vendor-linked; key suppliers in 2024 include II‑VI/Coherent, Lumentum, NICHIA and ams OSRAM, who set technical roadmaps and allocation priorities. A handful of global makers control sourcing windows and can shift price and availability with telecom/datacenter cycles. AFR secures lower unit costs via volume commitments but remains exposed to allocation risk and lead‑time variability.

Equipment & metrology dependence

Splicers, precision alignment rigs and interferometric test gear come from a concentrated set of OEMs (typically 3–5 suppliers), giving those vendors meaningful leverage; annual calibration cycles and multi-year service contracts raise switching costs and recurring spend. Major tool upgrades can lock AFR into OEM ecosystems through proprietary consumables and software, while strategic CAPEX timing and targeted in-house fixturing reduce supplier dependence.

- Concentrated OEM base: 3–5 suppliers

- Calibration cadence: typically annual

- Service contracts: increase switching costs

- Mitigation: CAPEX planning, in-house fixturing

Logistics & geopolitical exposure

Export-control expansions in 2024 tightened cross-border flows for photonics inputs, raising compliance risk and enabling suppliers to pass through higher costs to AFR; container freight volatility persisted despite a post-2022 decline, keeping landed-cost uncertainty elevated.

- Supply concentration: regional hubs increase resilience

- Cost drivers: tariffs, compliance pass‑through

- Mitigants: buffer stocks, dual sourcing

Top-five suppliers hold 60–70% of fiber; 12–20w lead times constrain output

Top-five suppliers control ~60–70% of high-purity fiber supply in 2024, with 12–20 week lead times that can throttle AFR output. Specialty items carry price premiums up to 20% and yield variability >10%, while pump diodes (II‑VI/Coherent, Lumentum, NICHIA, ams OSRAM) govern allocations. AFR mitigates via dual-sourcing, multi‑year contracts, buffer stock and 6–12 month qualification cycles.

| Component | Concentration | Metrics (2024) | Mitigant |

|---|---|---|---|

| Fiber preforms | Top5 60–70% | Lead 12–20w | Dual-source |

| Pump diodes | 4 majors | Allocation risk | Volume commits |

| Test gear | 3–5 OEMs | Annual cal | In-house fixtures |

What is included in the product

Provides a focused Porter's Five Forces assessment of Advanced Fiber Resources (Zhuhai), identifying competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers, with industry data and strategic implications to inform investor and management decisions.

Clear, one-sheet Porter’s Five Forces for Advanced Fiber Resources (Zhuhai) — concise pressure mapping and spider chart to pinpoint supplier/customer risks, entry threats and regulatory exposure, ready for pitch decks and simple to update with new market data.

Customers Bargaining Power

Large OEMs with volume leverage

Large OEMs in fiber laser, telecom and datacenter sectors buy at scale and enforce tight SLAs, using volume leverage to push pricing, extended payment terms and bespoke specs. Hyperscalers and major telcos—whose combined cloud/datacenter capex approached roughly $90 billion annually in the 2023–24 period—amplify this pressure. Losing a single key account can reduce factory utilization materially, so AFR must balance customer customization against platform economies to protect margins.

High qualification & switching costs

In 2024 AFR (Zhuhai) faces 12–24 month design-in cycles and rigorous reliability qualifications that drive switching costs (requalification often costing $0.5–5m), so buyers negotiate price post-qualification but rarely switch; AFR can trade performance for margin resilience, yet 60–70% of sophisticated OEMs maintain dual-qualification.

Price transparency in commoditized lines

Standard passive components are instantly price-benchmarked via 2024 distributor portals such as Digi-Key, Mouser and Avnet, enabling buyers to pit vendors and compress margins. AFR offsets this by selling performance-binned parts, value-added assemblies and bundled warranties that preserve higher ASPs. Despite this, spot bids on commoditized SKUs remain intensely competitive and price-driven.

Custom engineering requests

Enterprise customers demand bespoke wavelength, power-handling and packaging; custom NREs (typically tens to low hundreds of thousands USD) can offset margin pressure but commonly extend lead times by 4–12 weeks and raise delivery risk. Clear scope control and modular design lower cost-to-serve (~20% savings), while strong applications engineering increases customer stickiness and upsell rates.

- Custom NRE: tens–low hundreds k USD

- Lead-time impact: +4–12 weeks

- Cost-to-serve cut: ~20%

- Apps eng. boosts retention/upsell

Demand cyclicality

Capex cycles in lasers, telecom and datacenters drive volatile orders; global datacenter capex was about $200B in 2024 and telecom capex roughly $250B, creating demand swings where order volumes can shift >20% between peaks and troughs.

Buyers frequently cancel or defer to extract concessions, so AFR must keep agile capacity, strict ASP discipline and pursue framework agreements with take-or-pay clauses to stabilize volumes.

- Demand swing: >20% between cycles (2024)

- Datacenter capex: ≈$200B (2024)

- Telecom capex: ≈$250B (2024)

- Mitigants: agility, ASP discipline, take-or-pay contracts

Hyperscalers $90B capex and 12-24m design-ins raise OEM switching costs

Large OEMs and hyperscalers (≈$90B cloud/datacenter capex 2023–24) exert strong price and SLA leverage; losing a key account risks utilization. Long 12–24 month design-ins and $0.5–5m requalification raise switching costs; 60–70% of OEMs dual-qualify. Commoditized SKUs face spot-price pressure; bespoke NREs (tens–low hundreds k USD) and apps engineering preserve ASPs and stickiness.

| Metric | 2024 Value |

|---|---|

| Cloud/DC capex | $200B |

| Telecom capex | $250B |

| Hyperscaler cloud/DC spend | $90B |

| Requalification cost | $0.5–5M |

| NRE | tens–low hundreds k USD |

| Dual-qualify rate | 60–70% |

Preview Before You Purchase

Advanced Fiber Resources (Zhuhai) Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Advanced Fiber Resources (Zhuhai) you'll receive—comprehensive evaluation of competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes. The document is fully formatted, ready to download and use immediately after purchase with no placeholders or mockups. Use it for strategic planning, investment review, or competitive benchmarking—what you see is what you get.