Ageas Porter's Five Forces Analysis

Don't Miss the Bigger Picture

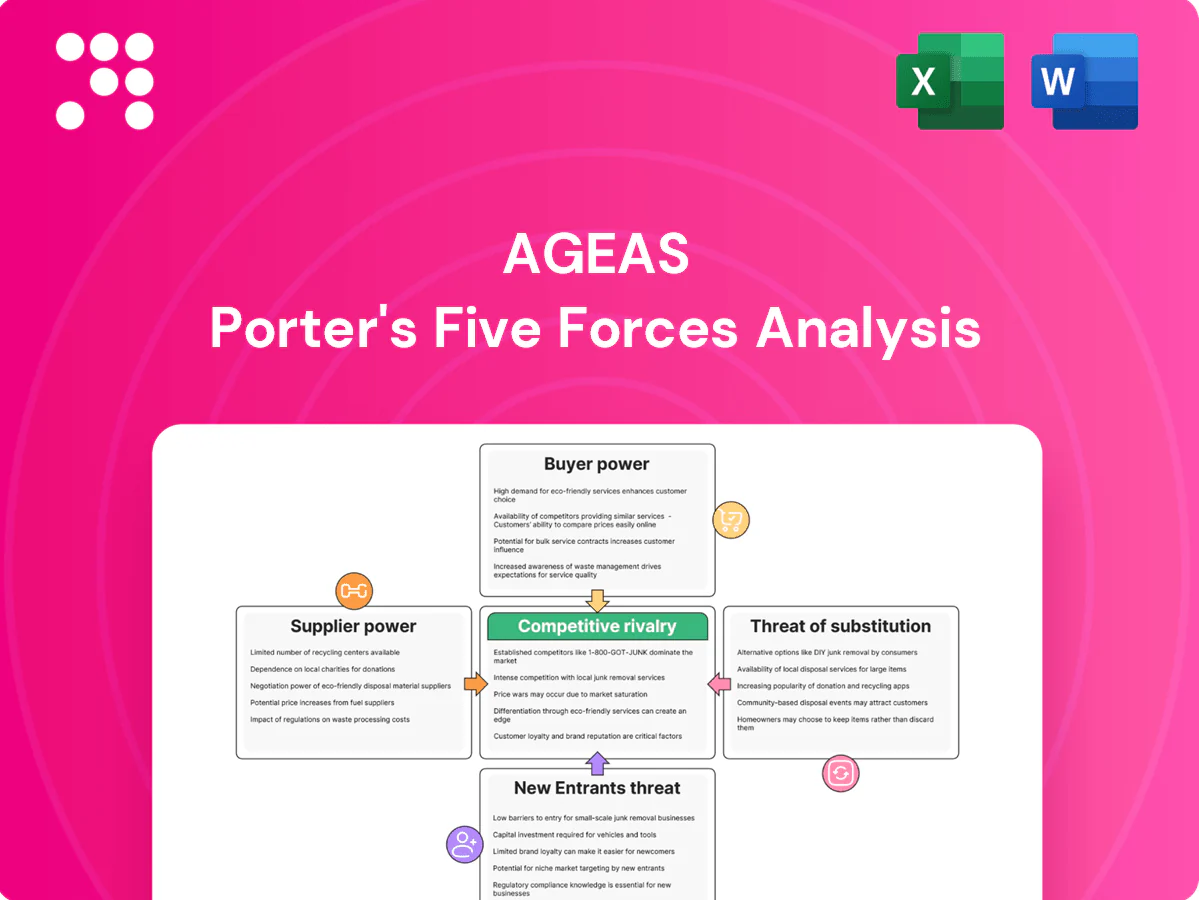

Ageas’s Porter's Five Forces snapshot highlights moderate buyer power, regulatory-driven barriers to entry, and intense rivalry in mature insurance markets; supplier and substitute threats vary by product and region. This brief teases strategic insights and risk drivers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations for Ageas.

Suppliers Bargaining Power

Reinsurers’ pricing clout

Reinsurance is a critical input for life and non-life risk transfer, and the hard market into 2024 pushed ceded-premium costs materially higher, with 2024 property-cat renewals showing median rate-on-line increases near 15% in many regions. Large global reinsurers now dictate exclusions, attachment points and capital-relief structures. Ageas can multi-source, tap alternative capital and raise retentions to soften impact, but peak-cat and mortality shocks still shift bargaining power toward reinsurers.

IT and data vendor dependence

Ageas faces concentrated dependence on core platforms and cloud/data providers, with AWS 32%, Microsoft Azure 23% and Google Cloud 11% of the cloud market in 2024, raising switching costs and integration risk. Vendors influence roadmaps, pricing escalators and cybersecurity standards (eg NIS2 implications). Long-term contracts and compliance limits Ageas’s leverage. Strategic partnerships and modular architectures can partially rebalance power.

Distribution intermediaries

Brokers, banks and affinity partners act as quasi-suppliers of customer access in bancassurance and JV markets, with bancassurance channels accounting for roughly 50% of life-premium flows in several Asian markets in 2024, giving high-volume partners scope to negotiate commissions, exclusivity and product features.

Ageas’s multi-channel model reduces single-partner dependence but does not eliminate it; large partners can still leverage local relationships—especially in Asia where tied distribution often concentrates risk and bargaining power.

Specialist service networks

Specialist service networks—auto repairers, medical networks, TPAs and loss adjusters—directly drive claims costs and customer experience; over 50% of motor repairs in key Ageas markets use preferred-provider networks in 2024, concentrating pricing power.

In concentrated markets service rates and SLAs are less flexible, so preferred-provider agreements and outcome-based contracts regained control, while digital FNOL and straight-through processing reduced manual-service reliance by ~30% in 2024.

- concentration: >50% preferred repairs

- efficiency: ~30% fewer manual interventions (2024)

- levers: preferred-provider + outcome-based contracts

Human capital and actuarial talent

Qualified actuaries, data scientists and underwriters remain scarce in 2024, especially with IFRS 17 and Solvency II expertise, fueling wage inflation and poaching that raise supplier-like power of talent markets; Ageas’s employer brand and targeted upskilling partially ease the pressure, while nearshoring and centers of excellence diversify sourcing and lower concentration risk.

- Scarcity: advanced analytics, IFRS 17/Solvency II

- Market pressure: wage inflation and poaching

- Mitigation: Ageas employer brand & upskilling

- Sourcing: nearshoring & centers of excellence

Reinsurance hikes, cloud concentration and talent scarcity shift supplier bargaining power

Reinsurance cost hikes in 2024 (median RoL +15% on property-cat renewals) shifted bargaining power toward large global reinsurers that now set exclusions and attachment points. Cloud concentration (AWS 32%, Azure 23%, Google 11% in 2024) raises switching costs and vendor leverage. Bancassurance and preferred repair networks (over 50% motor repairs via preferred providers) further concentrate supplier power, while talent scarcity (actuaries/data scientists) increases wage pressure.

| Supplier | 2024 metric |

|---|---|

| Reinsurance RoL | +15% median |

| Cloud market share | AWS 32% / Azure 23% / GCP 11% |

| Preferred repairs | >50% motor repairs |

| Talent scarcity | High — IFRS17/SolvencyII skills |

What is included in the product

Concise Porter’s Five Forces analysis of Ageas highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/disruptive risks shaping its pricing and profitability.

Concise Porter's Five Forces for Ageas—one-sheet clarity to quickly spot competitive pressures and strategic levers; ideal for rapid decision-making. Customizable pressure levels and a ready-to-copy layout make it effortless to tailor for decks, scenarios, or regulatory shifts.

Customers Bargaining Power

Price-sensitive retail customers

Motor and home policies are highly comparable and 2024 data shows around 60% of UK shoppers use aggregators, boosting transparency and switching pressure on premiums. Buyers increasingly push for lower premiums and richer cover, compressing insurer margins and contributing to mid-teen renewal switching rates. Loyalty remains moderate without strong service differentiation, though usage-based and personalized pricing (telematics) can blunt pure price competition.

Corporate and SME negotiators

Corporate and SME negotiators bundle lines and demand tailored cover and risk engineering, using scale to secure favorable rates, service levels and multi-year agreements (commonly 3 years). Intensified tendering in the 2024 renewal season amplified pricing pressure across markets. Value-added services, captive support and bespoke risk engineering materially defend pricing and retention. Large clients increasingly drive contract terms.

Bancassurance and JV channel buyers

Bank partners heavily shape product design, pricing cadence and campaign priorities, with bancassurance channels accounting for c.40% of life new business in several EU markets in 2024, giving banks leverage over distribution terms.

They can demand higher revenue shares—commonly 20–50%—and broader data access, forcing Ageas into trade-offs between margin and volume.

Ageas’s JV structures align incentives but still create recurring negotiation moments; performance‑based, sliding‑scale commissions tied to persistency and claims ratios help rebalance economics.

Regulated transparency and claims experience

Regulated transparency under the EU IDD and national consumer rules boosts disclosure and comparability, increasing buyer leverage; in 2024 digital quote/comparison use exceeded 60% in several EU markets, raising price sensitivity. Claims handling quality and speed drive retention—poor outcomes amplify churn and bargaining power, while proactive communication and digitized claims platforms sustain loyalty and reduce attrition.

Multi-policy and lifetime value leverage

Customers holding bundled life and non-life policies exert greater renewal leverage, and in 2024 Ageas observed increased cross-sell scrutiny as customers used multi-policy status to press for price and service gains. Deep cross-sell raises switching power if perceived value drops, while Ageas mitigates this with ecosystem benefits, loyalty rewards and data-driven retention offers that lower effective buyer power.

- Bundled renewal leverage — 2024 trend

- Cross-sell depth = higher switch risk

- Ecosystem rewards counter bargaining

- Data-led offers reduce churn

Aggregators ~60%, 20–50% commissions drive mid-teen churn

Customers have high price transparency: ~60% use aggregators in 2024, driving mid-teen renewal switching and margin pressure. Large corporates/SMEs and banks exert strong negotiating leverage via bundling and commission demands (20–50%). Data-led retention, telematics and ecosystem rewards reduce churn while regulatory disclosure raises comparability.

| Metric | 2024 |

|---|---|

| Aggregator use | ~60% |

| Renewal switching | mid-teens |

| Commission range | 20–50% |

Preview Before You Purchase

Ageas Porter's Five Forces Analysis

This preview shows the exact Ageas Porter’s Five Forces Analysis you’ll receive—no placeholders or samples. Once you complete your purchase you’ll get instant access to this fully formatted, ready-to-use document. It’s the final deliverable, suitable for download and immediate application in your strategic or investment work.

Don't Miss the Bigger Picture

Ageas’s Porter's Five Forces snapshot highlights moderate buyer power, regulatory-driven barriers to entry, and intense rivalry in mature insurance markets; supplier and substitute threats vary by product and region. This brief teases strategic insights and risk drivers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations for Ageas.

Suppliers Bargaining Power

Reinsurers’ pricing clout

Reinsurance is a critical input for life and non-life risk transfer, and the hard market into 2024 pushed ceded-premium costs materially higher, with 2024 property-cat renewals showing median rate-on-line increases near 15% in many regions. Large global reinsurers now dictate exclusions, attachment points and capital-relief structures. Ageas can multi-source, tap alternative capital and raise retentions to soften impact, but peak-cat and mortality shocks still shift bargaining power toward reinsurers.

IT and data vendor dependence

Ageas faces concentrated dependence on core platforms and cloud/data providers, with AWS 32%, Microsoft Azure 23% and Google Cloud 11% of the cloud market in 2024, raising switching costs and integration risk. Vendors influence roadmaps, pricing escalators and cybersecurity standards (eg NIS2 implications). Long-term contracts and compliance limits Ageas’s leverage. Strategic partnerships and modular architectures can partially rebalance power.

Distribution intermediaries

Brokers, banks and affinity partners act as quasi-suppliers of customer access in bancassurance and JV markets, with bancassurance channels accounting for roughly 50% of life-premium flows in several Asian markets in 2024, giving high-volume partners scope to negotiate commissions, exclusivity and product features.

Ageas’s multi-channel model reduces single-partner dependence but does not eliminate it; large partners can still leverage local relationships—especially in Asia where tied distribution often concentrates risk and bargaining power.

Specialist service networks

Specialist service networks—auto repairers, medical networks, TPAs and loss adjusters—directly drive claims costs and customer experience; over 50% of motor repairs in key Ageas markets use preferred-provider networks in 2024, concentrating pricing power.

In concentrated markets service rates and SLAs are less flexible, so preferred-provider agreements and outcome-based contracts regained control, while digital FNOL and straight-through processing reduced manual-service reliance by ~30% in 2024.

- concentration: >50% preferred repairs

- efficiency: ~30% fewer manual interventions (2024)

- levers: preferred-provider + outcome-based contracts

Human capital and actuarial talent

Qualified actuaries, data scientists and underwriters remain scarce in 2024, especially with IFRS 17 and Solvency II expertise, fueling wage inflation and poaching that raise supplier-like power of talent markets; Ageas’s employer brand and targeted upskilling partially ease the pressure, while nearshoring and centers of excellence diversify sourcing and lower concentration risk.

- Scarcity: advanced analytics, IFRS 17/Solvency II

- Market pressure: wage inflation and poaching

- Mitigation: Ageas employer brand & upskilling

- Sourcing: nearshoring & centers of excellence

Reinsurance hikes, cloud concentration and talent scarcity shift supplier bargaining power

Reinsurance cost hikes in 2024 (median RoL +15% on property-cat renewals) shifted bargaining power toward large global reinsurers that now set exclusions and attachment points. Cloud concentration (AWS 32%, Azure 23%, Google 11% in 2024) raises switching costs and vendor leverage. Bancassurance and preferred repair networks (over 50% motor repairs via preferred providers) further concentrate supplier power, while talent scarcity (actuaries/data scientists) increases wage pressure.

| Supplier | 2024 metric |

|---|---|

| Reinsurance RoL | +15% median |

| Cloud market share | AWS 32% / Azure 23% / GCP 11% |

| Preferred repairs | >50% motor repairs |

| Talent scarcity | High — IFRS17/SolvencyII skills |

What is included in the product

Concise Porter’s Five Forces analysis of Ageas highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/disruptive risks shaping its pricing and profitability.

Concise Porter's Five Forces for Ageas—one-sheet clarity to quickly spot competitive pressures and strategic levers; ideal for rapid decision-making. Customizable pressure levels and a ready-to-copy layout make it effortless to tailor for decks, scenarios, or regulatory shifts.

Customers Bargaining Power

Price-sensitive retail customers

Motor and home policies are highly comparable and 2024 data shows around 60% of UK shoppers use aggregators, boosting transparency and switching pressure on premiums. Buyers increasingly push for lower premiums and richer cover, compressing insurer margins and contributing to mid-teen renewal switching rates. Loyalty remains moderate without strong service differentiation, though usage-based and personalized pricing (telematics) can blunt pure price competition.

Corporate and SME negotiators

Corporate and SME negotiators bundle lines and demand tailored cover and risk engineering, using scale to secure favorable rates, service levels and multi-year agreements (commonly 3 years). Intensified tendering in the 2024 renewal season amplified pricing pressure across markets. Value-added services, captive support and bespoke risk engineering materially defend pricing and retention. Large clients increasingly drive contract terms.

Bancassurance and JV channel buyers

Bank partners heavily shape product design, pricing cadence and campaign priorities, with bancassurance channels accounting for c.40% of life new business in several EU markets in 2024, giving banks leverage over distribution terms.

They can demand higher revenue shares—commonly 20–50%—and broader data access, forcing Ageas into trade-offs between margin and volume.

Ageas’s JV structures align incentives but still create recurring negotiation moments; performance‑based, sliding‑scale commissions tied to persistency and claims ratios help rebalance economics.

Regulated transparency and claims experience

Regulated transparency under the EU IDD and national consumer rules boosts disclosure and comparability, increasing buyer leverage; in 2024 digital quote/comparison use exceeded 60% in several EU markets, raising price sensitivity. Claims handling quality and speed drive retention—poor outcomes amplify churn and bargaining power, while proactive communication and digitized claims platforms sustain loyalty and reduce attrition.

Multi-policy and lifetime value leverage

Customers holding bundled life and non-life policies exert greater renewal leverage, and in 2024 Ageas observed increased cross-sell scrutiny as customers used multi-policy status to press for price and service gains. Deep cross-sell raises switching power if perceived value drops, while Ageas mitigates this with ecosystem benefits, loyalty rewards and data-driven retention offers that lower effective buyer power.

- Bundled renewal leverage — 2024 trend

- Cross-sell depth = higher switch risk

- Ecosystem rewards counter bargaining

- Data-led offers reduce churn

Aggregators ~60%, 20–50% commissions drive mid-teen churn

Customers have high price transparency: ~60% use aggregators in 2024, driving mid-teen renewal switching and margin pressure. Large corporates/SMEs and banks exert strong negotiating leverage via bundling and commission demands (20–50%). Data-led retention, telematics and ecosystem rewards reduce churn while regulatory disclosure raises comparability.

| Metric | 2024 |

|---|---|

| Aggregator use | ~60% |

| Renewal switching | mid-teens |

| Commission range | 20–50% |

Preview Before You Purchase

Ageas Porter's Five Forces Analysis

This preview shows the exact Ageas Porter’s Five Forces Analysis you’ll receive—no placeholders or samples. Once you complete your purchase you’ll get instant access to this fully formatted, ready-to-use document. It’s the final deliverable, suitable for download and immediate application in your strategic or investment work.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Ageas’s Porter's Five Forces snapshot highlights moderate buyer power, regulatory-driven barriers to entry, and intense rivalry in mature insurance markets; supplier and substitute threats vary by product and region. This brief teases strategic insights and risk drivers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations for Ageas.

Suppliers Bargaining Power

Reinsurers’ pricing clout

Reinsurance is a critical input for life and non-life risk transfer, and the hard market into 2024 pushed ceded-premium costs materially higher, with 2024 property-cat renewals showing median rate-on-line increases near 15% in many regions. Large global reinsurers now dictate exclusions, attachment points and capital-relief structures. Ageas can multi-source, tap alternative capital and raise retentions to soften impact, but peak-cat and mortality shocks still shift bargaining power toward reinsurers.

IT and data vendor dependence

Ageas faces concentrated dependence on core platforms and cloud/data providers, with AWS 32%, Microsoft Azure 23% and Google Cloud 11% of the cloud market in 2024, raising switching costs and integration risk. Vendors influence roadmaps, pricing escalators and cybersecurity standards (eg NIS2 implications). Long-term contracts and compliance limits Ageas’s leverage. Strategic partnerships and modular architectures can partially rebalance power.

Distribution intermediaries

Brokers, banks and affinity partners act as quasi-suppliers of customer access in bancassurance and JV markets, with bancassurance channels accounting for roughly 50% of life-premium flows in several Asian markets in 2024, giving high-volume partners scope to negotiate commissions, exclusivity and product features.

Ageas’s multi-channel model reduces single-partner dependence but does not eliminate it; large partners can still leverage local relationships—especially in Asia where tied distribution often concentrates risk and bargaining power.

Specialist service networks

Specialist service networks—auto repairers, medical networks, TPAs and loss adjusters—directly drive claims costs and customer experience; over 50% of motor repairs in key Ageas markets use preferred-provider networks in 2024, concentrating pricing power.

In concentrated markets service rates and SLAs are less flexible, so preferred-provider agreements and outcome-based contracts regained control, while digital FNOL and straight-through processing reduced manual-service reliance by ~30% in 2024.

- concentration: >50% preferred repairs

- efficiency: ~30% fewer manual interventions (2024)

- levers: preferred-provider + outcome-based contracts

Human capital and actuarial talent

Qualified actuaries, data scientists and underwriters remain scarce in 2024, especially with IFRS 17 and Solvency II expertise, fueling wage inflation and poaching that raise supplier-like power of talent markets; Ageas’s employer brand and targeted upskilling partially ease the pressure, while nearshoring and centers of excellence diversify sourcing and lower concentration risk.

- Scarcity: advanced analytics, IFRS 17/Solvency II

- Market pressure: wage inflation and poaching

- Mitigation: Ageas employer brand & upskilling

- Sourcing: nearshoring & centers of excellence

Reinsurance hikes, cloud concentration and talent scarcity shift supplier bargaining power

Reinsurance cost hikes in 2024 (median RoL +15% on property-cat renewals) shifted bargaining power toward large global reinsurers that now set exclusions and attachment points. Cloud concentration (AWS 32%, Azure 23%, Google 11% in 2024) raises switching costs and vendor leverage. Bancassurance and preferred repair networks (over 50% motor repairs via preferred providers) further concentrate supplier power, while talent scarcity (actuaries/data scientists) increases wage pressure.

| Supplier | 2024 metric |

|---|---|

| Reinsurance RoL | +15% median |

| Cloud market share | AWS 32% / Azure 23% / GCP 11% |

| Preferred repairs | >50% motor repairs |

| Talent scarcity | High — IFRS17/SolvencyII skills |

What is included in the product

Concise Porter’s Five Forces analysis of Ageas highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/disruptive risks shaping its pricing and profitability.

Concise Porter's Five Forces for Ageas—one-sheet clarity to quickly spot competitive pressures and strategic levers; ideal for rapid decision-making. Customizable pressure levels and a ready-to-copy layout make it effortless to tailor for decks, scenarios, or regulatory shifts.

Customers Bargaining Power

Price-sensitive retail customers

Motor and home policies are highly comparable and 2024 data shows around 60% of UK shoppers use aggregators, boosting transparency and switching pressure on premiums. Buyers increasingly push for lower premiums and richer cover, compressing insurer margins and contributing to mid-teen renewal switching rates. Loyalty remains moderate without strong service differentiation, though usage-based and personalized pricing (telematics) can blunt pure price competition.

Corporate and SME negotiators

Corporate and SME negotiators bundle lines and demand tailored cover and risk engineering, using scale to secure favorable rates, service levels and multi-year agreements (commonly 3 years). Intensified tendering in the 2024 renewal season amplified pricing pressure across markets. Value-added services, captive support and bespoke risk engineering materially defend pricing and retention. Large clients increasingly drive contract terms.

Bancassurance and JV channel buyers

Bank partners heavily shape product design, pricing cadence and campaign priorities, with bancassurance channels accounting for c.40% of life new business in several EU markets in 2024, giving banks leverage over distribution terms.

They can demand higher revenue shares—commonly 20–50%—and broader data access, forcing Ageas into trade-offs between margin and volume.

Ageas’s JV structures align incentives but still create recurring negotiation moments; performance‑based, sliding‑scale commissions tied to persistency and claims ratios help rebalance economics.

Regulated transparency and claims experience

Regulated transparency under the EU IDD and national consumer rules boosts disclosure and comparability, increasing buyer leverage; in 2024 digital quote/comparison use exceeded 60% in several EU markets, raising price sensitivity. Claims handling quality and speed drive retention—poor outcomes amplify churn and bargaining power, while proactive communication and digitized claims platforms sustain loyalty and reduce attrition.

Multi-policy and lifetime value leverage

Customers holding bundled life and non-life policies exert greater renewal leverage, and in 2024 Ageas observed increased cross-sell scrutiny as customers used multi-policy status to press for price and service gains. Deep cross-sell raises switching power if perceived value drops, while Ageas mitigates this with ecosystem benefits, loyalty rewards and data-driven retention offers that lower effective buyer power.

- Bundled renewal leverage — 2024 trend

- Cross-sell depth = higher switch risk

- Ecosystem rewards counter bargaining

- Data-led offers reduce churn

Aggregators ~60%, 20–50% commissions drive mid-teen churn

Customers have high price transparency: ~60% use aggregators in 2024, driving mid-teen renewal switching and margin pressure. Large corporates/SMEs and banks exert strong negotiating leverage via bundling and commission demands (20–50%). Data-led retention, telematics and ecosystem rewards reduce churn while regulatory disclosure raises comparability.

| Metric | 2024 |

|---|---|

| Aggregator use | ~60% |

| Renewal switching | mid-teens |

| Commission range | 20–50% |

Preview Before You Purchase

Ageas Porter's Five Forces Analysis

This preview shows the exact Ageas Porter’s Five Forces Analysis you’ll receive—no placeholders or samples. Once you complete your purchase you’ll get instant access to this fully formatted, ready-to-use document. It’s the final deliverable, suitable for download and immediate application in your strategic or investment work.