AIB Group Business Model Canvas

Unlock a strategic Business Model Canvas: three customer segments, core value props, revenue levers

Unlock AIB Group’s strategic playbook with our concise Business Model Canvas—three key customer segments, core value propositions, and revenue levers explained. This actionable snapshot reveals where AIB creates value and scales profitably. Purchase the full editable Canvas for a section-by-section guide, templates, and investor-ready insights.

Partnerships

Global payment networks and processors

Partnerships with card schemes and processors enable AIB to scale issuance, acquiring and seamless payments across retail and digital channels. Networks like Visa and Mastercard provide global acceptance in 200+ countries, plus risk tools and standardized interchange frameworks. Joint product development accelerates digital wallets, tokenization and fraud controls, while co-marketing drives card penetration and spend growth.

Fintechs, core banking, and cloud technology vendors

Technology partners power AIB’s core systems, cloud hosting, analytics and AI, accelerating digital rollouts from onboarding to automated lending decisioning. APIs and microservices improve agility and time-to-market, enabling iterative feature delivery. Major cloud vendors offer SLAs of 99.95%+ availability and maintain certifications such as ISO 27001 and SOC 2, strengthening resilience and regulatory compliance.

Regulators, central banks, and industry bodies

Strong relationships with the Central Bank of Ireland, the UK PRA and EU bodies ensure AIB aligns with evolving regulation and supervision. Access to payment rails like TARGET2 and the €100,000 EU deposit guarantee supports funding stability. Engagement in consultations helps shape policy and prudential standards. Close compliance partnerships reduce systemic and conduct risk.

Correspondent banks and capital markets counterparties

Correspondent banks and capital markets counterparties enable AIB Group to execute cross-border payments and trade finance efficiently, supporting multinational clients and diaspora flows.

Market counterparties provide access to funding, hedging and liquidity management tools, while syndication partners expand lending capacity for large corporate and project financings.

These relationships enhance pricing, reduce execution risk and increase certainty on large transactions.

- Cross-border payments

- Trade finance

- Funding & hedging

- Syndication for large deals

- Improved pricing & execution certainty

Distribution partners, brokers, and affinity groups

Third-party distribution partners introduce mortgages, insurance and SME loans, accounting for 35% of new mortgage originations and 28% of SME loan volumes in 2024; affinity and employer programs drove 22% of payroll accounts and benefits-linked product uptake. Marketplace and platform integrations delivered 18% digital customer growth while revenue-sharing models reduced CAC by ~25%.

- Distribution: 35% mortgages, 28% SME loans (2024)

- Affinity/employer: 22% payroll accounts (2024)

- Marketplace reach: +18% digital customers (2024)

- Revenue-share: CAC down ~25% (2024)

Partnerships power growth — 35% mortgages, 28% SME loans, 18% digital growth; CAC -25% (2024)

Partnerships with card schemes and processors drive global acceptance, tokenization and fraud tools, supporting card volume growth and interchange income.

Tech and cloud partners deliver 99.95%+ SLAs, ISO 27001/SOC2 compliance and faster digital launches, cutting time-to-market.

Distribution and correspondent banks provided 35% mortgage originations, 28% SME loans, 18% digital customer growth and CAC down ~25% in 2024.

| Metric | 2024 |

|---|---|

| Mortgages via partners | 35% |

| SME loans via partners | 28% |

| Digital growth (marketplaces) | 18% |

| CAC reduction | ~25% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for AIB Group that details customer segments, value propositions, channels and revenue streams across the 9 BMC blocks, integrates competitive advantages and SWOT analysis, and is suited for presentations, investor discussions and strategic decision-making.

Condenses AIB Group’s banking strategy into a digestible, editable one-page canvas to quickly identify core components and relieve reporting and alignment pain points for teams and executives.

Activities

Credit origination, underwriting, and portfolio management

The bank sources, underwrites and prices consumer, SME and corporate credit across a €70bn+ loan book (2024), applying risk models, collateral management and covenant structures to set pricing and limits. Ongoing monitoring and early‑warning systems, including portfolio stress testing and sector overlays, protect asset quality and keep NPLs below c.1.5% (2024). Workout and remediation teams optimise recoveries where needed.

Deposit gathering and liquidity management

AIB attracts and retains current and savings accounts across segments, with customer deposits >€120bn in 2024. Treasury manages liquidity buffers, funding mix and interest-rate risk through wholesale and retail funding allocation. Pricing strategies are calibrated to balance volume growth with margin compression. Regular stress testing quantifies resilience under adverse macro and liquidity scenarios.

Payments processing and digital banking operations

AIB runs real-time payments, card issuing and merchant acquiring across retail and business segments, supporting over 2 million digital customers in Ireland and the UK. Digital channels manage onboarding, servicing and self-service journeys with embedded fraud detection and multi-factor authentication end-to-end. Operational monitoring targets >99.9% availability and continuous incident response to protect transaction flows.

Risk, compliance, and regulatory reporting

AIB manages credit, market, liquidity and operational risks across a balance sheet exceeding €100bn, maintaining capital buffers (CET1 >14%) to satisfy supervisors and stress tests. It enforces AML, KYC and conduct standards via transaction monitoring and enhanced due diligence for over 2.5m retail customers. Regulatory reporting meets local and cross-border requirements with regular ICAAP/IFRS submissions; controls and audits ensure governance and accountability.

- Risk types: credit, market, liquidity, operational

- Compliance: AML, KYC, conduct

- Scale: >€100bn balance sheet; CET1 >14%

- Controls: internal audit, regulatory reporting cadence

Wealth management, treasury, and advisory services

Wealth management, treasury and advisory deliver investment advice, funds and retirement solutions while treasury provides FX, rates hedging and cash management for corporates; sector specialists supply insights and structured solutions and customer outcomes drive suitability and fiduciary care.

- Investment advice, funds, retirement solutions

- FX, rates hedging, cash management

- Sector specialists, structured solutions, fiduciary suitability

Retail bank: loans €70bn+, deposits €120bn+, CET1>14%

Originate, underwrite and price €70bn+ loan book (2024) with risk models, collateral and covenants; NPLs ~1.5% (2024) and specialised workout teams.

Gather deposits >€120bn (2024); treasury manages liquidity, funding mix and IR risk with regular stress tests.

Operate payments, cards and digital banking for >2m users; maintain >99.9% availability and strong fraud controls.

| Metric | 2024 |

|---|---|

| Loan book | €70bn+ |

| Deposits | €120bn+ |

| NPLs | ~1.5% |

| Digital users | >2m |

| Balance sheet | >€100bn; CET1>14% |

Full Version Awaits

Business Model Canvas

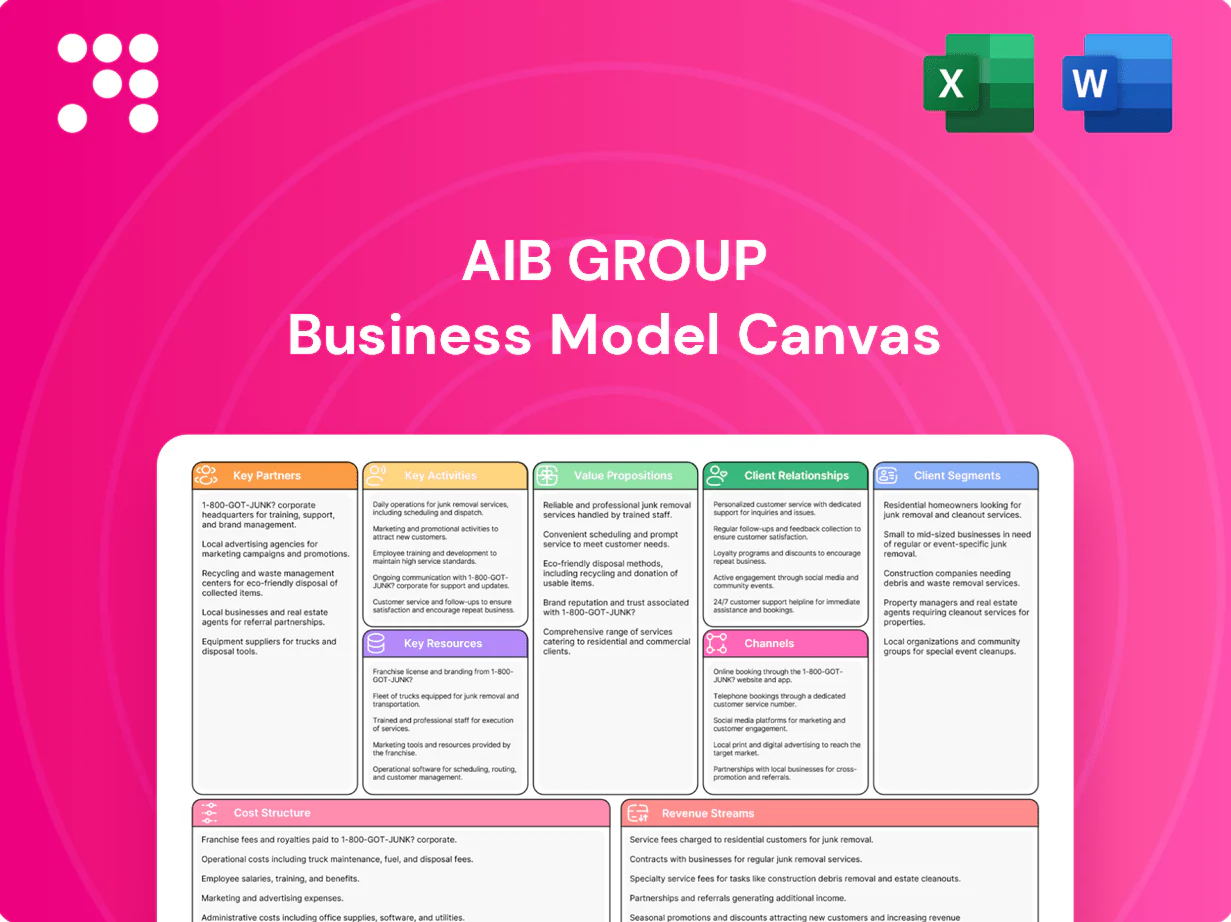

The AIB Group Business Model Canvas you see here is the actual deliverable, not a mockup or sample. Upon purchase you’ll receive this exact document—fully formatted and complete—in editable Word and Excel files. No surprises: what’s previewed is what you’ll download and use immediately.

Unlock a strategic Business Model Canvas: three customer segments, core value props, revenue levers

Unlock AIB Group’s strategic playbook with our concise Business Model Canvas—three key customer segments, core value propositions, and revenue levers explained. This actionable snapshot reveals where AIB creates value and scales profitably. Purchase the full editable Canvas for a section-by-section guide, templates, and investor-ready insights.

Partnerships

Global payment networks and processors

Partnerships with card schemes and processors enable AIB to scale issuance, acquiring and seamless payments across retail and digital channels. Networks like Visa and Mastercard provide global acceptance in 200+ countries, plus risk tools and standardized interchange frameworks. Joint product development accelerates digital wallets, tokenization and fraud controls, while co-marketing drives card penetration and spend growth.

Fintechs, core banking, and cloud technology vendors

Technology partners power AIB’s core systems, cloud hosting, analytics and AI, accelerating digital rollouts from onboarding to automated lending decisioning. APIs and microservices improve agility and time-to-market, enabling iterative feature delivery. Major cloud vendors offer SLAs of 99.95%+ availability and maintain certifications such as ISO 27001 and SOC 2, strengthening resilience and regulatory compliance.

Regulators, central banks, and industry bodies

Strong relationships with the Central Bank of Ireland, the UK PRA and EU bodies ensure AIB aligns with evolving regulation and supervision. Access to payment rails like TARGET2 and the €100,000 EU deposit guarantee supports funding stability. Engagement in consultations helps shape policy and prudential standards. Close compliance partnerships reduce systemic and conduct risk.

Correspondent banks and capital markets counterparties

Correspondent banks and capital markets counterparties enable AIB Group to execute cross-border payments and trade finance efficiently, supporting multinational clients and diaspora flows.

Market counterparties provide access to funding, hedging and liquidity management tools, while syndication partners expand lending capacity for large corporate and project financings.

These relationships enhance pricing, reduce execution risk and increase certainty on large transactions.

- Cross-border payments

- Trade finance

- Funding & hedging

- Syndication for large deals

- Improved pricing & execution certainty

Distribution partners, brokers, and affinity groups

Third-party distribution partners introduce mortgages, insurance and SME loans, accounting for 35% of new mortgage originations and 28% of SME loan volumes in 2024; affinity and employer programs drove 22% of payroll accounts and benefits-linked product uptake. Marketplace and platform integrations delivered 18% digital customer growth while revenue-sharing models reduced CAC by ~25%.

- Distribution: 35% mortgages, 28% SME loans (2024)

- Affinity/employer: 22% payroll accounts (2024)

- Marketplace reach: +18% digital customers (2024)

- Revenue-share: CAC down ~25% (2024)

Partnerships power growth — 35% mortgages, 28% SME loans, 18% digital growth; CAC -25% (2024)

Partnerships with card schemes and processors drive global acceptance, tokenization and fraud tools, supporting card volume growth and interchange income.

Tech and cloud partners deliver 99.95%+ SLAs, ISO 27001/SOC2 compliance and faster digital launches, cutting time-to-market.

Distribution and correspondent banks provided 35% mortgage originations, 28% SME loans, 18% digital customer growth and CAC down ~25% in 2024.

| Metric | 2024 |

|---|---|

| Mortgages via partners | 35% |

| SME loans via partners | 28% |

| Digital growth (marketplaces) | 18% |

| CAC reduction | ~25% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for AIB Group that details customer segments, value propositions, channels and revenue streams across the 9 BMC blocks, integrates competitive advantages and SWOT analysis, and is suited for presentations, investor discussions and strategic decision-making.

Condenses AIB Group’s banking strategy into a digestible, editable one-page canvas to quickly identify core components and relieve reporting and alignment pain points for teams and executives.

Activities

Credit origination, underwriting, and portfolio management

The bank sources, underwrites and prices consumer, SME and corporate credit across a €70bn+ loan book (2024), applying risk models, collateral management and covenant structures to set pricing and limits. Ongoing monitoring and early‑warning systems, including portfolio stress testing and sector overlays, protect asset quality and keep NPLs below c.1.5% (2024). Workout and remediation teams optimise recoveries where needed.

Deposit gathering and liquidity management

AIB attracts and retains current and savings accounts across segments, with customer deposits >€120bn in 2024. Treasury manages liquidity buffers, funding mix and interest-rate risk through wholesale and retail funding allocation. Pricing strategies are calibrated to balance volume growth with margin compression. Regular stress testing quantifies resilience under adverse macro and liquidity scenarios.

Payments processing and digital banking operations

AIB runs real-time payments, card issuing and merchant acquiring across retail and business segments, supporting over 2 million digital customers in Ireland and the UK. Digital channels manage onboarding, servicing and self-service journeys with embedded fraud detection and multi-factor authentication end-to-end. Operational monitoring targets >99.9% availability and continuous incident response to protect transaction flows.

Risk, compliance, and regulatory reporting

AIB manages credit, market, liquidity and operational risks across a balance sheet exceeding €100bn, maintaining capital buffers (CET1 >14%) to satisfy supervisors and stress tests. It enforces AML, KYC and conduct standards via transaction monitoring and enhanced due diligence for over 2.5m retail customers. Regulatory reporting meets local and cross-border requirements with regular ICAAP/IFRS submissions; controls and audits ensure governance and accountability.

- Risk types: credit, market, liquidity, operational

- Compliance: AML, KYC, conduct

- Scale: >€100bn balance sheet; CET1 >14%

- Controls: internal audit, regulatory reporting cadence

Wealth management, treasury, and advisory services

Wealth management, treasury and advisory deliver investment advice, funds and retirement solutions while treasury provides FX, rates hedging and cash management for corporates; sector specialists supply insights and structured solutions and customer outcomes drive suitability and fiduciary care.

- Investment advice, funds, retirement solutions

- FX, rates hedging, cash management

- Sector specialists, structured solutions, fiduciary suitability

Retail bank: loans €70bn+, deposits €120bn+, CET1>14%

Originate, underwrite and price €70bn+ loan book (2024) with risk models, collateral and covenants; NPLs ~1.5% (2024) and specialised workout teams.

Gather deposits >€120bn (2024); treasury manages liquidity, funding mix and IR risk with regular stress tests.

Operate payments, cards and digital banking for >2m users; maintain >99.9% availability and strong fraud controls.

| Metric | 2024 |

|---|---|

| Loan book | €70bn+ |

| Deposits | €120bn+ |

| NPLs | ~1.5% |

| Digital users | >2m |

| Balance sheet | >€100bn; CET1>14% |

Full Version Awaits

Business Model Canvas

The AIB Group Business Model Canvas you see here is the actual deliverable, not a mockup or sample. Upon purchase you’ll receive this exact document—fully formatted and complete—in editable Word and Excel files. No surprises: what’s previewed is what you’ll download and use immediately.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a strategic Business Model Canvas: three customer segments, core value props, revenue levers

Unlock AIB Group’s strategic playbook with our concise Business Model Canvas—three key customer segments, core value propositions, and revenue levers explained. This actionable snapshot reveals where AIB creates value and scales profitably. Purchase the full editable Canvas for a section-by-section guide, templates, and investor-ready insights.

Partnerships

Global payment networks and processors

Partnerships with card schemes and processors enable AIB to scale issuance, acquiring and seamless payments across retail and digital channels. Networks like Visa and Mastercard provide global acceptance in 200+ countries, plus risk tools and standardized interchange frameworks. Joint product development accelerates digital wallets, tokenization and fraud controls, while co-marketing drives card penetration and spend growth.

Fintechs, core banking, and cloud technology vendors

Technology partners power AIB’s core systems, cloud hosting, analytics and AI, accelerating digital rollouts from onboarding to automated lending decisioning. APIs and microservices improve agility and time-to-market, enabling iterative feature delivery. Major cloud vendors offer SLAs of 99.95%+ availability and maintain certifications such as ISO 27001 and SOC 2, strengthening resilience and regulatory compliance.

Regulators, central banks, and industry bodies

Strong relationships with the Central Bank of Ireland, the UK PRA and EU bodies ensure AIB aligns with evolving regulation and supervision. Access to payment rails like TARGET2 and the €100,000 EU deposit guarantee supports funding stability. Engagement in consultations helps shape policy and prudential standards. Close compliance partnerships reduce systemic and conduct risk.

Correspondent banks and capital markets counterparties

Correspondent banks and capital markets counterparties enable AIB Group to execute cross-border payments and trade finance efficiently, supporting multinational clients and diaspora flows.

Market counterparties provide access to funding, hedging and liquidity management tools, while syndication partners expand lending capacity for large corporate and project financings.

These relationships enhance pricing, reduce execution risk and increase certainty on large transactions.

- Cross-border payments

- Trade finance

- Funding & hedging

- Syndication for large deals

- Improved pricing & execution certainty

Distribution partners, brokers, and affinity groups

Third-party distribution partners introduce mortgages, insurance and SME loans, accounting for 35% of new mortgage originations and 28% of SME loan volumes in 2024; affinity and employer programs drove 22% of payroll accounts and benefits-linked product uptake. Marketplace and platform integrations delivered 18% digital customer growth while revenue-sharing models reduced CAC by ~25%.

- Distribution: 35% mortgages, 28% SME loans (2024)

- Affinity/employer: 22% payroll accounts (2024)

- Marketplace reach: +18% digital customers (2024)

- Revenue-share: CAC down ~25% (2024)

Partnerships power growth — 35% mortgages, 28% SME loans, 18% digital growth; CAC -25% (2024)

Partnerships with card schemes and processors drive global acceptance, tokenization and fraud tools, supporting card volume growth and interchange income.

Tech and cloud partners deliver 99.95%+ SLAs, ISO 27001/SOC2 compliance and faster digital launches, cutting time-to-market.

Distribution and correspondent banks provided 35% mortgage originations, 28% SME loans, 18% digital customer growth and CAC down ~25% in 2024.

| Metric | 2024 |

|---|---|

| Mortgages via partners | 35% |

| SME loans via partners | 28% |

| Digital growth (marketplaces) | 18% |

| CAC reduction | ~25% |

What is included in the product

A comprehensive, pre-written Business Model Canvas for AIB Group that details customer segments, value propositions, channels and revenue streams across the 9 BMC blocks, integrates competitive advantages and SWOT analysis, and is suited for presentations, investor discussions and strategic decision-making.

Condenses AIB Group’s banking strategy into a digestible, editable one-page canvas to quickly identify core components and relieve reporting and alignment pain points for teams and executives.

Activities

Credit origination, underwriting, and portfolio management

The bank sources, underwrites and prices consumer, SME and corporate credit across a €70bn+ loan book (2024), applying risk models, collateral management and covenant structures to set pricing and limits. Ongoing monitoring and early‑warning systems, including portfolio stress testing and sector overlays, protect asset quality and keep NPLs below c.1.5% (2024). Workout and remediation teams optimise recoveries where needed.

Deposit gathering and liquidity management

AIB attracts and retains current and savings accounts across segments, with customer deposits >€120bn in 2024. Treasury manages liquidity buffers, funding mix and interest-rate risk through wholesale and retail funding allocation. Pricing strategies are calibrated to balance volume growth with margin compression. Regular stress testing quantifies resilience under adverse macro and liquidity scenarios.

Payments processing and digital banking operations

AIB runs real-time payments, card issuing and merchant acquiring across retail and business segments, supporting over 2 million digital customers in Ireland and the UK. Digital channels manage onboarding, servicing and self-service journeys with embedded fraud detection and multi-factor authentication end-to-end. Operational monitoring targets >99.9% availability and continuous incident response to protect transaction flows.

Risk, compliance, and regulatory reporting

AIB manages credit, market, liquidity and operational risks across a balance sheet exceeding €100bn, maintaining capital buffers (CET1 >14%) to satisfy supervisors and stress tests. It enforces AML, KYC and conduct standards via transaction monitoring and enhanced due diligence for over 2.5m retail customers. Regulatory reporting meets local and cross-border requirements with regular ICAAP/IFRS submissions; controls and audits ensure governance and accountability.

- Risk types: credit, market, liquidity, operational

- Compliance: AML, KYC, conduct

- Scale: >€100bn balance sheet; CET1 >14%

- Controls: internal audit, regulatory reporting cadence

Wealth management, treasury, and advisory services

Wealth management, treasury and advisory deliver investment advice, funds and retirement solutions while treasury provides FX, rates hedging and cash management for corporates; sector specialists supply insights and structured solutions and customer outcomes drive suitability and fiduciary care.

- Investment advice, funds, retirement solutions

- FX, rates hedging, cash management

- Sector specialists, structured solutions, fiduciary suitability

Retail bank: loans €70bn+, deposits €120bn+, CET1>14%

Originate, underwrite and price €70bn+ loan book (2024) with risk models, collateral and covenants; NPLs ~1.5% (2024) and specialised workout teams.

Gather deposits >€120bn (2024); treasury manages liquidity, funding mix and IR risk with regular stress tests.

Operate payments, cards and digital banking for >2m users; maintain >99.9% availability and strong fraud controls.

| Metric | 2024 |

|---|---|

| Loan book | €70bn+ |

| Deposits | €120bn+ |

| NPLs | ~1.5% |

| Digital users | >2m |

| Balance sheet | >€100bn; CET1>14% |

Full Version Awaits

Business Model Canvas

The AIB Group Business Model Canvas you see here is the actual deliverable, not a mockup or sample. Upon purchase you’ll receive this exact document—fully formatted and complete—in editable Word and Excel files. No surprises: what’s previewed is what you’ll download and use immediately.