Aichi Financial Group Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

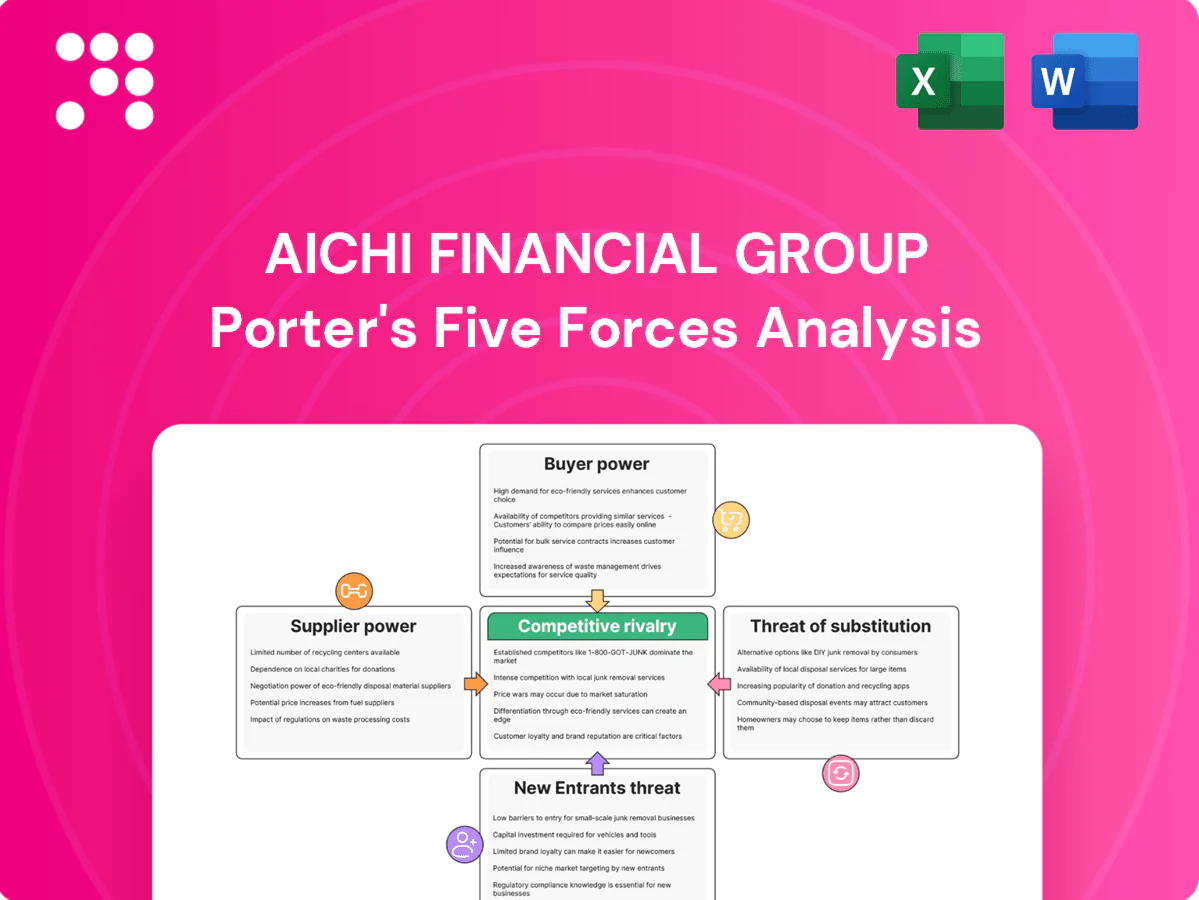

Aichi Financial Group faces moderate competitive rivalry within regional banking, constrained by strong incumbents and regulatory oversight. Buyer power is rising with fintech alternatives, while supplier and substitute threats remain manageable. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Rate-sensitive regional deposit base

Depositors are the primary funding suppliers and remain rate-sensitive as global and Japanese rates normalized by 2024, compressing margins and pressuring funding costs. Concentration in Aichi Prefecture (population ~7.5 million in 2024) exposes the group to local cycles, which can amplify deposit volatility. Long-standing retail relationships and sticky balances temper supplier power. Diversified product holdings help anchor deposits despite pricing moves.

Wholesale funding and BoJ policy

Access to interbank and bond markets gives Aichi Financial Group funding flexibility but exposes it to spread widening—10-year JGB yields averaged about 0.9% in 2024, amplifying wholesale repricing risk. Rapid Bank of Japan policy shifts can quickly raise wholesale costs, increasing suppliers’ leverage. Strong credit ratings and liquidity buffers (cash and liquid assets covering several months of wholesale rollovers) mitigate reliance on any single channel.

Skilled talent and IT contractors

Engineers, risk specialists and compliance talent are scarce around Nagoya and command premium pay, with IT contractor day rates commonly exceeding 100,000 JPY in 2024. Competition from megabanks and fintechs raises supplier power in labor and increases hiring costs. Unionized or legacy staffing models reduce flexibility and slow redeployment. Upskilling programs and captive tech centers can lower external contractor spend by as much as 15–20%.

Core tech and cloud vendors

Core banking, payments and cybersecurity platforms show high switching costs, strengthening vendor leverage; AWS and Microsoft together held over 50% of the global cloud market in 2024 (Synergy Research). Few viable alternatives and 12–24 month implementation cycles lock in terms, while Japan's FISC/FSA security guidelines (2023) further narrow vendor choice. Multi-vendor and open architectures can reduce single-vendor power over time.

- High switching costs

- AWS+MSFT >50% (2024)

- 12–24 month cycles

- FISC/FSA security rules

Card networks and leasing OEM partners

Visa and Mastercard jointly dominate roughly 80% of global card scheme volumes in 2024, and their rules and fees create non-negotiable cost floors that compress card margins (scheme+interchange commonly range around 1–3% of TPV). Dependency on processors and mandatory scheme compliance raises switching costs and complicates renegotiations for Aichi Financial Group. In leasing, OEMs and captive finance arms materially influence inventory allocation and residual-value assumptions, while broader partner ecosystems enhance bargaining leverage and product availability.

- Scheme concentration ~80% (Visa+Mastercard, 2024)

- Fees/interchange ~1–3% of transaction value

- OEM captives shape residuals & inventory access

Rate-sensitive depositors squeeze margins; wholesale repricing and vendor concentration raise costs

Depositors remain rate-sensitive, compressing margins as 10Y JGB averaged ~0.9% in 2024; wholesale access offsets but raises repricing risk. Vendor and scheme concentration (AWS+MSFT >50%; Visa+Mastercard ~80% in 2024) increases switching costs. Skilled IT/labor scarcity (contractor rates >100,000 JPY/day in 2024) elevates supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Depositors | Local pop ~7.5M | Rate sensitivity, liquidity volatility |

| Wholesale | 10Y JGB ~0.9% | Repricing risk |

| Cloud | AWS+MSFT >50% | High switching costs |

| Card schemes | Visa+MC ~80% | Fee floor 1–3% TPV |

| Labor | >100,000 JPY/day | Higher OPEX |

What is included in the product

Comprehensive Porter's Five Forces analysis for Aichi Financial Group, uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitute threats, with strategic commentary and industry data tailored to its regional banking position.

Clear, one-sheet Porter's Five Forces for Aichi Financial Group—instantly highlights competitive pressures and regulatory risks for faster decisions. Customize scores, swap data, and export a clean radar chart for decks without macros.

Customers Bargaining Power

Multi-banked retail customers

Japanese retail customers are frequently multi-banked—about 68% holding two or more accounts—using digital tools to compare rates and exert price pressure. Low switching costs for deposits and cards, with online account openings up roughly 25% year-on-year in 2023–24, raise bargaining power. Convenience factors—branch access and app UX—still sway choices, while rewards and bundled services reduce elasticity by improving retention.

SMEs in auto-supply clusters

SMEs in Aichi’s dense auto-supply clusters, anchored by Toyota (≈10 million vehicles produced in 2023) can leverage competition among lenders to negotiate loan spreads, collateral, and covenants. Aichi Financial Group’s relationship banking and local knowledge partially offset this bargaining power by providing tailored credit and fast decision-making. Cross-selling cash management and leasing deepens ties and reduces churn. Manufacturing cyclicality, however, can swing negotiating leverage further toward borrowers in downturns.

Mid-market and local corporates

Mid-market and local corporate clients increasingly run RFPs across regional banks and megabanks, tightening pricing and covenants; in 2024 many deals shifted to competitive bid processes. Access to syndications and capital markets provides clear alternatives, pressuring margins. Bundled treasury, FX and supply-chain finance solutions are essential, while data-driven pricing and strict SLAs help defend fee income.

Transparent pricing and aggregators

Comparison sites and fintech interfaces make deposit, loan and card pricing visible, and by 2024 aggregator use in Japan reached roughly 40% of digitally active consumers, amplifying buyer power and accelerating repricing cycles for Aichi Financial Group.

Non-price factors—speed, quality of advice and ecosystem integrations—remain differentiators; loyalty programs and tiered packages help retain value-seeking customers and slow churn.

- Visible pricing → faster repricing

- 40% aggregator reach (2024)

- Non-price service differentiation

- Loyalty/tiered retention

Public sector and institutions

Prefectural and municipal accounts are sizable and often require competitive tenders, giving public customers strong bargaining power; selection hinges on pricing, service reliability, and strict compliance. Securing these institutional clients yields stable, low-cost deposits for Aichi Financial Group but compresses margins due to tender-driven pricing. Long contract tenures and institutional inertia lower churn once accounts are onboarded.

- High bargaining power: tender-led selection

- Key drivers: price, reliability, compliance

- Impact: stable deposits, tight margins, low churn

68% multi-banked customers, 40% aggregator reach and +25% online growth tighten bank margins

Customers hold multiple banks (≈68%), use aggregators (≈40% reach in 2024) and grew online account openings ~25% YoY (2023–24), increasing price sensitivity; SMEs around Toyota clusters (Toyota ~10m vehicles in 2023) extract better loan terms, while tenders for public deposits compress margins; Aichi’s relationship banking, cross-sell and service quality partly defend margins.

| Metric | Value |

|---|---|

| Multi-banked customers | 68% |

| Aggregator reach (2024) | 40% |

| Online account openings YoY | +25% (2023–24) |

| Toyota production (2023) | ≈10m vehicles |

Same Document Delivered

Aichi Financial Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Aichi Financial Group is the full, professionally prepared document you see in the preview, covering competitive rivalry, supplier and buyer power, threats of entry and substitution. The preview is the exact file delivered upon purchase, fully formatted and ready to use instantly. No samples, placeholders, or edits are needed—what you see is what you get.

A Must-Have Tool for Decision-Makers

Aichi Financial Group faces moderate competitive rivalry within regional banking, constrained by strong incumbents and regulatory oversight. Buyer power is rising with fintech alternatives, while supplier and substitute threats remain manageable. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Rate-sensitive regional deposit base

Depositors are the primary funding suppliers and remain rate-sensitive as global and Japanese rates normalized by 2024, compressing margins and pressuring funding costs. Concentration in Aichi Prefecture (population ~7.5 million in 2024) exposes the group to local cycles, which can amplify deposit volatility. Long-standing retail relationships and sticky balances temper supplier power. Diversified product holdings help anchor deposits despite pricing moves.

Wholesale funding and BoJ policy

Access to interbank and bond markets gives Aichi Financial Group funding flexibility but exposes it to spread widening—10-year JGB yields averaged about 0.9% in 2024, amplifying wholesale repricing risk. Rapid Bank of Japan policy shifts can quickly raise wholesale costs, increasing suppliers’ leverage. Strong credit ratings and liquidity buffers (cash and liquid assets covering several months of wholesale rollovers) mitigate reliance on any single channel.

Skilled talent and IT contractors

Engineers, risk specialists and compliance talent are scarce around Nagoya and command premium pay, with IT contractor day rates commonly exceeding 100,000 JPY in 2024. Competition from megabanks and fintechs raises supplier power in labor and increases hiring costs. Unionized or legacy staffing models reduce flexibility and slow redeployment. Upskilling programs and captive tech centers can lower external contractor spend by as much as 15–20%.

Core tech and cloud vendors

Core banking, payments and cybersecurity platforms show high switching costs, strengthening vendor leverage; AWS and Microsoft together held over 50% of the global cloud market in 2024 (Synergy Research). Few viable alternatives and 12–24 month implementation cycles lock in terms, while Japan's FISC/FSA security guidelines (2023) further narrow vendor choice. Multi-vendor and open architectures can reduce single-vendor power over time.

- High switching costs

- AWS+MSFT >50% (2024)

- 12–24 month cycles

- FISC/FSA security rules

Card networks and leasing OEM partners

Visa and Mastercard jointly dominate roughly 80% of global card scheme volumes in 2024, and their rules and fees create non-negotiable cost floors that compress card margins (scheme+interchange commonly range around 1–3% of TPV). Dependency on processors and mandatory scheme compliance raises switching costs and complicates renegotiations for Aichi Financial Group. In leasing, OEMs and captive finance arms materially influence inventory allocation and residual-value assumptions, while broader partner ecosystems enhance bargaining leverage and product availability.

- Scheme concentration ~80% (Visa+Mastercard, 2024)

- Fees/interchange ~1–3% of transaction value

- OEM captives shape residuals & inventory access

Rate-sensitive depositors squeeze margins; wholesale repricing and vendor concentration raise costs

Depositors remain rate-sensitive, compressing margins as 10Y JGB averaged ~0.9% in 2024; wholesale access offsets but raises repricing risk. Vendor and scheme concentration (AWS+MSFT >50%; Visa+Mastercard ~80% in 2024) increases switching costs. Skilled IT/labor scarcity (contractor rates >100,000 JPY/day in 2024) elevates supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Depositors | Local pop ~7.5M | Rate sensitivity, liquidity volatility |

| Wholesale | 10Y JGB ~0.9% | Repricing risk |

| Cloud | AWS+MSFT >50% | High switching costs |

| Card schemes | Visa+MC ~80% | Fee floor 1–3% TPV |

| Labor | >100,000 JPY/day | Higher OPEX |

What is included in the product

Comprehensive Porter's Five Forces analysis for Aichi Financial Group, uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitute threats, with strategic commentary and industry data tailored to its regional banking position.

Clear, one-sheet Porter's Five Forces for Aichi Financial Group—instantly highlights competitive pressures and regulatory risks for faster decisions. Customize scores, swap data, and export a clean radar chart for decks without macros.

Customers Bargaining Power

Multi-banked retail customers

Japanese retail customers are frequently multi-banked—about 68% holding two or more accounts—using digital tools to compare rates and exert price pressure. Low switching costs for deposits and cards, with online account openings up roughly 25% year-on-year in 2023–24, raise bargaining power. Convenience factors—branch access and app UX—still sway choices, while rewards and bundled services reduce elasticity by improving retention.

SMEs in auto-supply clusters

SMEs in Aichi’s dense auto-supply clusters, anchored by Toyota (≈10 million vehicles produced in 2023) can leverage competition among lenders to negotiate loan spreads, collateral, and covenants. Aichi Financial Group’s relationship banking and local knowledge partially offset this bargaining power by providing tailored credit and fast decision-making. Cross-selling cash management and leasing deepens ties and reduces churn. Manufacturing cyclicality, however, can swing negotiating leverage further toward borrowers in downturns.

Mid-market and local corporates

Mid-market and local corporate clients increasingly run RFPs across regional banks and megabanks, tightening pricing and covenants; in 2024 many deals shifted to competitive bid processes. Access to syndications and capital markets provides clear alternatives, pressuring margins. Bundled treasury, FX and supply-chain finance solutions are essential, while data-driven pricing and strict SLAs help defend fee income.

Transparent pricing and aggregators

Comparison sites and fintech interfaces make deposit, loan and card pricing visible, and by 2024 aggregator use in Japan reached roughly 40% of digitally active consumers, amplifying buyer power and accelerating repricing cycles for Aichi Financial Group.

Non-price factors—speed, quality of advice and ecosystem integrations—remain differentiators; loyalty programs and tiered packages help retain value-seeking customers and slow churn.

- Visible pricing → faster repricing

- 40% aggregator reach (2024)

- Non-price service differentiation

- Loyalty/tiered retention

Public sector and institutions

Prefectural and municipal accounts are sizable and often require competitive tenders, giving public customers strong bargaining power; selection hinges on pricing, service reliability, and strict compliance. Securing these institutional clients yields stable, low-cost deposits for Aichi Financial Group but compresses margins due to tender-driven pricing. Long contract tenures and institutional inertia lower churn once accounts are onboarded.

- High bargaining power: tender-led selection

- Key drivers: price, reliability, compliance

- Impact: stable deposits, tight margins, low churn

68% multi-banked customers, 40% aggregator reach and +25% online growth tighten bank margins

Customers hold multiple banks (≈68%), use aggregators (≈40% reach in 2024) and grew online account openings ~25% YoY (2023–24), increasing price sensitivity; SMEs around Toyota clusters (Toyota ~10m vehicles in 2023) extract better loan terms, while tenders for public deposits compress margins; Aichi’s relationship banking, cross-sell and service quality partly defend margins.

| Metric | Value |

|---|---|

| Multi-banked customers | 68% |

| Aggregator reach (2024) | 40% |

| Online account openings YoY | +25% (2023–24) |

| Toyota production (2023) | ≈10m vehicles |

Same Document Delivered

Aichi Financial Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Aichi Financial Group is the full, professionally prepared document you see in the preview, covering competitive rivalry, supplier and buyer power, threats of entry and substitution. The preview is the exact file delivered upon purchase, fully formatted and ready to use instantly. No samples, placeholders, or edits are needed—what you see is what you get.

Description

A Must-Have Tool for Decision-Makers

Aichi Financial Group faces moderate competitive rivalry within regional banking, constrained by strong incumbents and regulatory oversight. Buyer power is rising with fintech alternatives, while supplier and substitute threats remain manageable. This snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Rate-sensitive regional deposit base

Depositors are the primary funding suppliers and remain rate-sensitive as global and Japanese rates normalized by 2024, compressing margins and pressuring funding costs. Concentration in Aichi Prefecture (population ~7.5 million in 2024) exposes the group to local cycles, which can amplify deposit volatility. Long-standing retail relationships and sticky balances temper supplier power. Diversified product holdings help anchor deposits despite pricing moves.

Wholesale funding and BoJ policy

Access to interbank and bond markets gives Aichi Financial Group funding flexibility but exposes it to spread widening—10-year JGB yields averaged about 0.9% in 2024, amplifying wholesale repricing risk. Rapid Bank of Japan policy shifts can quickly raise wholesale costs, increasing suppliers’ leverage. Strong credit ratings and liquidity buffers (cash and liquid assets covering several months of wholesale rollovers) mitigate reliance on any single channel.

Skilled talent and IT contractors

Engineers, risk specialists and compliance talent are scarce around Nagoya and command premium pay, with IT contractor day rates commonly exceeding 100,000 JPY in 2024. Competition from megabanks and fintechs raises supplier power in labor and increases hiring costs. Unionized or legacy staffing models reduce flexibility and slow redeployment. Upskilling programs and captive tech centers can lower external contractor spend by as much as 15–20%.

Core tech and cloud vendors

Core banking, payments and cybersecurity platforms show high switching costs, strengthening vendor leverage; AWS and Microsoft together held over 50% of the global cloud market in 2024 (Synergy Research). Few viable alternatives and 12–24 month implementation cycles lock in terms, while Japan's FISC/FSA security guidelines (2023) further narrow vendor choice. Multi-vendor and open architectures can reduce single-vendor power over time.

- High switching costs

- AWS+MSFT >50% (2024)

- 12–24 month cycles

- FISC/FSA security rules

Card networks and leasing OEM partners

Visa and Mastercard jointly dominate roughly 80% of global card scheme volumes in 2024, and their rules and fees create non-negotiable cost floors that compress card margins (scheme+interchange commonly range around 1–3% of TPV). Dependency on processors and mandatory scheme compliance raises switching costs and complicates renegotiations for Aichi Financial Group. In leasing, OEMs and captive finance arms materially influence inventory allocation and residual-value assumptions, while broader partner ecosystems enhance bargaining leverage and product availability.

- Scheme concentration ~80% (Visa+Mastercard, 2024)

- Fees/interchange ~1–3% of transaction value

- OEM captives shape residuals & inventory access

Rate-sensitive depositors squeeze margins; wholesale repricing and vendor concentration raise costs

Depositors remain rate-sensitive, compressing margins as 10Y JGB averaged ~0.9% in 2024; wholesale access offsets but raises repricing risk. Vendor and scheme concentration (AWS+MSFT >50%; Visa+Mastercard ~80% in 2024) increases switching costs. Skilled IT/labor scarcity (contractor rates >100,000 JPY/day in 2024) elevates supplier leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Depositors | Local pop ~7.5M | Rate sensitivity, liquidity volatility |

| Wholesale | 10Y JGB ~0.9% | Repricing risk |

| Cloud | AWS+MSFT >50% | High switching costs |

| Card schemes | Visa+MC ~80% | Fee floor 1–3% TPV |

| Labor | >100,000 JPY/day | Higher OPEX |

What is included in the product

Comprehensive Porter's Five Forces analysis for Aichi Financial Group, uncovering competitive rivalry, buyer and supplier power, entry barriers, and substitute threats, with strategic commentary and industry data tailored to its regional banking position.

Clear, one-sheet Porter's Five Forces for Aichi Financial Group—instantly highlights competitive pressures and regulatory risks for faster decisions. Customize scores, swap data, and export a clean radar chart for decks without macros.

Customers Bargaining Power

Multi-banked retail customers

Japanese retail customers are frequently multi-banked—about 68% holding two or more accounts—using digital tools to compare rates and exert price pressure. Low switching costs for deposits and cards, with online account openings up roughly 25% year-on-year in 2023–24, raise bargaining power. Convenience factors—branch access and app UX—still sway choices, while rewards and bundled services reduce elasticity by improving retention.

SMEs in auto-supply clusters

SMEs in Aichi’s dense auto-supply clusters, anchored by Toyota (≈10 million vehicles produced in 2023) can leverage competition among lenders to negotiate loan spreads, collateral, and covenants. Aichi Financial Group’s relationship banking and local knowledge partially offset this bargaining power by providing tailored credit and fast decision-making. Cross-selling cash management and leasing deepens ties and reduces churn. Manufacturing cyclicality, however, can swing negotiating leverage further toward borrowers in downturns.

Mid-market and local corporates

Mid-market and local corporate clients increasingly run RFPs across regional banks and megabanks, tightening pricing and covenants; in 2024 many deals shifted to competitive bid processes. Access to syndications and capital markets provides clear alternatives, pressuring margins. Bundled treasury, FX and supply-chain finance solutions are essential, while data-driven pricing and strict SLAs help defend fee income.

Transparent pricing and aggregators

Comparison sites and fintech interfaces make deposit, loan and card pricing visible, and by 2024 aggregator use in Japan reached roughly 40% of digitally active consumers, amplifying buyer power and accelerating repricing cycles for Aichi Financial Group.

Non-price factors—speed, quality of advice and ecosystem integrations—remain differentiators; loyalty programs and tiered packages help retain value-seeking customers and slow churn.

- Visible pricing → faster repricing

- 40% aggregator reach (2024)

- Non-price service differentiation

- Loyalty/tiered retention

Public sector and institutions

Prefectural and municipal accounts are sizable and often require competitive tenders, giving public customers strong bargaining power; selection hinges on pricing, service reliability, and strict compliance. Securing these institutional clients yields stable, low-cost deposits for Aichi Financial Group but compresses margins due to tender-driven pricing. Long contract tenures and institutional inertia lower churn once accounts are onboarded.

- High bargaining power: tender-led selection

- Key drivers: price, reliability, compliance

- Impact: stable deposits, tight margins, low churn

68% multi-banked customers, 40% aggregator reach and +25% online growth tighten bank margins

Customers hold multiple banks (≈68%), use aggregators (≈40% reach in 2024) and grew online account openings ~25% YoY (2023–24), increasing price sensitivity; SMEs around Toyota clusters (Toyota ~10m vehicles in 2023) extract better loan terms, while tenders for public deposits compress margins; Aichi’s relationship banking, cross-sell and service quality partly defend margins.

| Metric | Value |

|---|---|

| Multi-banked customers | 68% |

| Aggregator reach (2024) | 40% |

| Online account openings YoY | +25% (2023–24) |

| Toyota production (2023) | ≈10m vehicles |

Same Document Delivered

Aichi Financial Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Aichi Financial Group is the full, professionally prepared document you see in the preview, covering competitive rivalry, supplier and buyer power, threats of entry and substitution. The preview is the exact file delivered upon purchase, fully formatted and ready to use instantly. No samples, placeholders, or edits are needed—what you see is what you get.