AirBoss Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

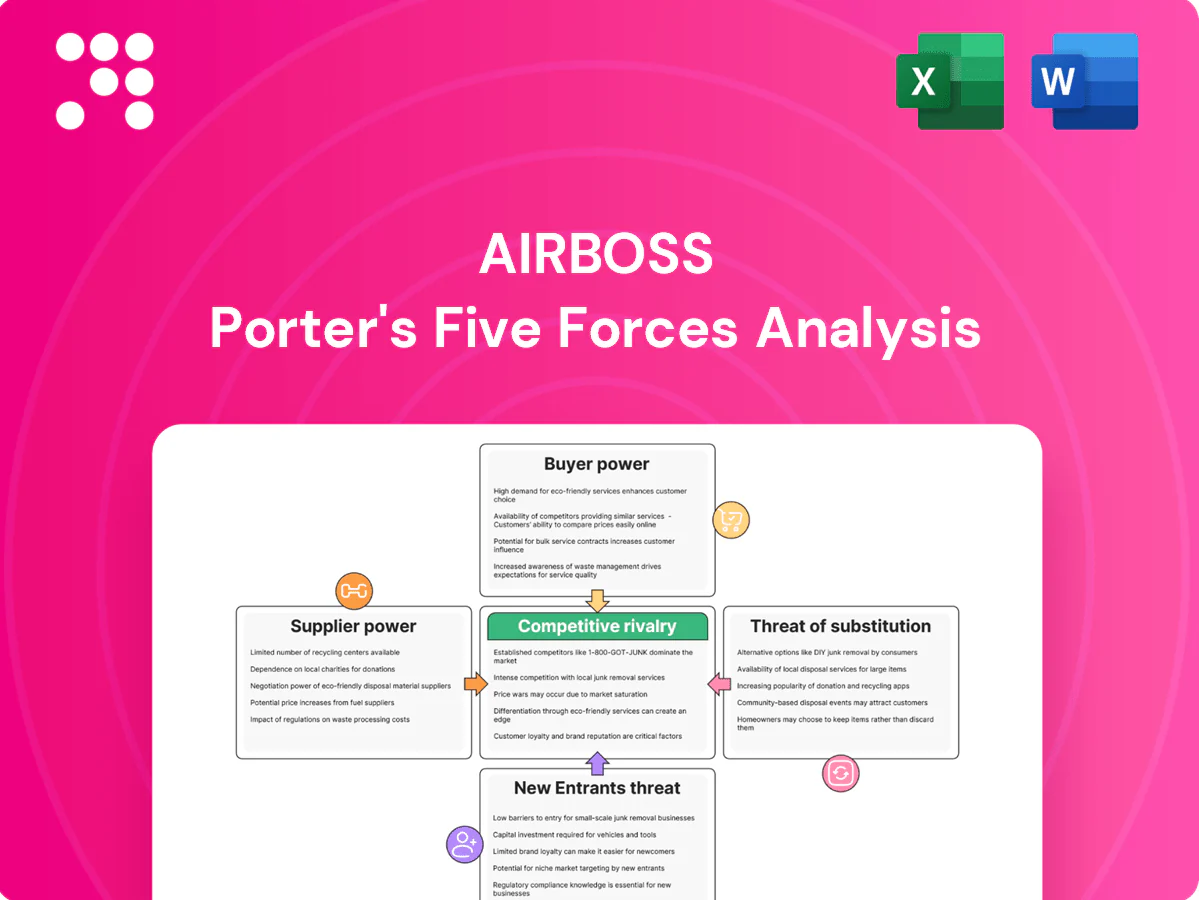

AirBoss faces moderate supplier power due to specialized materials, while buyer power is tempered by niche industrial customers; competitive rivalry is intense from global PPE and rubber firms. Barriers to entry are moderate—scale and regulatory compliance matter—and substitutes pose a limited but growing threat. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AirBoss’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated petrochemical feedstocks

AirBoss depends on synthetic rubbers, carbon black and specialty chemicals from a concentrated petrochemical base, where supply tightness or outages rapidly translate into pricing leverage for upstream suppliers. Hedging and long-term contracts mitigate some risk but notable spot exposure remains, leaving margins sensitive to feedstock swings; Brent crude averaged about $86/bbl in 2024. Volatility in oil and natural latex amplifies suppliers’ bargaining power, pressuring input costs and pass-through flexibility.

Specialty CBRN materials scarcity

CBRN filters, impregnated activated carbon adsorbents and aramid textiles are sourced from a narrow, often single-digit pool of qualified vendors, and strict security and qualification requirements further thin that pool. Certification and testing timelines typically take 6–12 months, so dual-sourcing is possible but slow. Niche sorbent suppliers command meaningful premiums in surge periods, tightening supplier clout and margin pressure on AirBoss.

Energy and logistics cost pass-through

Rubber compounding is energy-intensive and freight-heavy, so utilities and carriers exert indirect leverage over AirBoss; European TTF gas surged over 300% in 2022, underpinning pervasive energy pass-throughs. Suppliers routinely levy energy surcharges during spikes, and although AirBoss negotiates tiered rates, timing mismatches between spot spikes and contract tiers squeeze margins. Nearshoring and inventory buffers blunt but do not eliminate this pressure.

Switching costs from formulation lock-in

Compound performance depends on precise ingredient specs; changing suppliers forces reformulation and validation, creating technical lock-in that strengthens incumbent suppliers. In defense PPE requalification routinely takes months (commonly 3–6 months) and can incur six-figure costs, limiting rapid supplier substitution during price disputes.

- 3–6 months requalification

- Six-figure reformulation/validation costs

- Technical lock-in raises supplier leverage

Commodity vs. specialty mix

For commodity inputs global supply offers negotiating leverage; world natural rubber production was about 13 million tonnes in 2024 (IRSG), increasing sourcing options and price competition. Specialty additives and bespoke textiles remain concentrated among few suppliers, raising switching costs and limiting competition. The blended basket yields moderate overall supplier power, mitigated by mix management and strategic partnerships.

- Commodity leverage: global rubber ~13 Mt (2024)

- Specialty constraint: few bespoke additive/textile vendors

- Mitigants: supplier mix, long-term partnerships, strategic sourcing

Supplier power rises as Brent $86/bbl and technical lock-in increase costs

AirBoss faces moderate-to-high supplier power: feedstock price swings (Brent ~$86/bbl in 2024) and concentrated specialty vendors raise costs and switching barriers. Requalification (3–6 months) and six-figure validation costs create technical lock-in, while global rubber supply (~13 Mt in 2024) provides some commodity leverage. Strategic contracts and nearshoring partially mitigate supplier clout.

| Metric | 2024 value |

|---|---|

| Brent crude | $86/bbl |

| Natural rubber production | ~13 Mt |

| Requalification time | 3–6 months |

| Reformulation cost | Six-figure USD |

What is included in the product

Tailored Porter's Five Forces analysis for AirBoss that uncovers key drivers of competition, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and disruptive substitutes—supported by industry data and strategic commentary for use in investor materials or internal strategy decks.

AirBoss Porter's Five Forces packs a clear one-sheet summary of competitive pressures to remove analysis bottlenecks, with customizable force levels and a ready-to-use radar chart for instant strategic clarity. Designed for easy slide insertion and non-technical use, it speeds decisions across scenarios without macros or coding.

Customers Bargaining Power

Automotive OEMs’ scale and pricing pressure

Automotive OEMs buy at high volumes and run aggressive competitive bids, typically driving annual cost-downs of about 2–5% and demanding just-in-time OTIF performance often targeted at 95–99% in 2024. They exert strong price pressure through consolidated purchasing and multi-sourcing programs. Approved-vendor status plus tooling and qualification — frequently costing upwards of $250k and taking 6–12 months — create switching frictions. Buyer power is high but mitigated by technical lock-in and long qualification cycles.

Defense procurement concentration

Government agencies and a handful of large prime contractors concentrate demand—US DoD budget reached about 858 billion USD in 2024, channeling significant procurement through few buyers. ID/IQ and competitive tender frameworks give these buyers leverage on pricing, terms and compliance. CBRN mission-critical performance shifts focus from lowest price, and long testing cycles plus past-performance records materially limit supplier switching.

Customization reduces comparability

Bespoke rubber compounds and PPE configurations make apples-to-apples price comparisons difficult, reducing buyers' ability to push for commodity-like discounts. Engineering collaboration embeds AirBoss (AirBoss of America, ticker AIR.TO/BOSS) early in design cycles, creating product and process stickiness. Higher switching costs from validated specs and supply-chain qualifications weaken customer bargaining power. This dynamic shifts leverage toward the supplier.

Demand cyclicality and budget cycles

Auto and industrial downturns intensify buyer push for concessions, while defense budget allocations and surge purchases periodically shift buyers into allocation mode, reducing leverage; AirBoss therefore faces alternating tight and loose buyer power that raises margin volatility. Contract mix diversification across defense, industrial, and specialty rubber products smooths revenue swings and bargaining exposure.

- Buyers: cyclical pressure vs allocation relief

- Risk: margin volatility

- Mitigation: diversified contract mix

Quality, delivery, and compliance dependencies

Buyers demand stringent QA, traceability, and regulatory compliance (NIOSH, FDA, ISO 13485/9001), narrowing viable suppliers and raising switching costs; in PPE markets failure risk and liability make price-based switching unlikely.

Contracts emphasize performance guarantees and penalties, shaping margins and negotiation leverage, while reliable on‑time delivery histories gradually erode buyer power.

- QA/regulatory: NIOSH/FDA/ISO compliance required

- Switching barrier: high due to liability and traceability

- Negotiation drivers: performance guarantees, penalties

- Delivery: consistent performance reduces buyer leverage

OEMs & DoD squeeze suppliers: 2–5% cuts, 95–99% OTIF, tooling > $250k

Automotive OEMs exert high buyer power via large-volume competitive bids driving 2–5% annual cost‑downs and requiring 95–99% OTIF in 2024. US DoD procurement (≈858bn USD in 2024) concentrates demand and negotiates terms, though CBRN performance needs limit pure price plays. Tooling/qualification costs (often >250k USD, 6–12 months) and regulatory QA (NIOSH/FDA/ISO) raise switching costs. Net: strong buyer pressure offset by technical lock‑in and long qualification cycles.

Same Document Delivered

AirBoss Porter's Five Forces Analysis

This preview shows the exact AirBoss Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The full, professionally formatted document is downloadable immediately after payment and ready for use in presentations or due diligence. What you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

AirBoss faces moderate supplier power due to specialized materials, while buyer power is tempered by niche industrial customers; competitive rivalry is intense from global PPE and rubber firms. Barriers to entry are moderate—scale and regulatory compliance matter—and substitutes pose a limited but growing threat. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AirBoss’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated petrochemical feedstocks

AirBoss depends on synthetic rubbers, carbon black and specialty chemicals from a concentrated petrochemical base, where supply tightness or outages rapidly translate into pricing leverage for upstream suppliers. Hedging and long-term contracts mitigate some risk but notable spot exposure remains, leaving margins sensitive to feedstock swings; Brent crude averaged about $86/bbl in 2024. Volatility in oil and natural latex amplifies suppliers’ bargaining power, pressuring input costs and pass-through flexibility.

Specialty CBRN materials scarcity

CBRN filters, impregnated activated carbon adsorbents and aramid textiles are sourced from a narrow, often single-digit pool of qualified vendors, and strict security and qualification requirements further thin that pool. Certification and testing timelines typically take 6–12 months, so dual-sourcing is possible but slow. Niche sorbent suppliers command meaningful premiums in surge periods, tightening supplier clout and margin pressure on AirBoss.

Energy and logistics cost pass-through

Rubber compounding is energy-intensive and freight-heavy, so utilities and carriers exert indirect leverage over AirBoss; European TTF gas surged over 300% in 2022, underpinning pervasive energy pass-throughs. Suppliers routinely levy energy surcharges during spikes, and although AirBoss negotiates tiered rates, timing mismatches between spot spikes and contract tiers squeeze margins. Nearshoring and inventory buffers blunt but do not eliminate this pressure.

Switching costs from formulation lock-in

Compound performance depends on precise ingredient specs; changing suppliers forces reformulation and validation, creating technical lock-in that strengthens incumbent suppliers. In defense PPE requalification routinely takes months (commonly 3–6 months) and can incur six-figure costs, limiting rapid supplier substitution during price disputes.

- 3–6 months requalification

- Six-figure reformulation/validation costs

- Technical lock-in raises supplier leverage

Commodity vs. specialty mix

For commodity inputs global supply offers negotiating leverage; world natural rubber production was about 13 million tonnes in 2024 (IRSG), increasing sourcing options and price competition. Specialty additives and bespoke textiles remain concentrated among few suppliers, raising switching costs and limiting competition. The blended basket yields moderate overall supplier power, mitigated by mix management and strategic partnerships.

- Commodity leverage: global rubber ~13 Mt (2024)

- Specialty constraint: few bespoke additive/textile vendors

- Mitigants: supplier mix, long-term partnerships, strategic sourcing

Supplier power rises as Brent $86/bbl and technical lock-in increase costs

AirBoss faces moderate-to-high supplier power: feedstock price swings (Brent ~$86/bbl in 2024) and concentrated specialty vendors raise costs and switching barriers. Requalification (3–6 months) and six-figure validation costs create technical lock-in, while global rubber supply (~13 Mt in 2024) provides some commodity leverage. Strategic contracts and nearshoring partially mitigate supplier clout.

| Metric | 2024 value |

|---|---|

| Brent crude | $86/bbl |

| Natural rubber production | ~13 Mt |

| Requalification time | 3–6 months |

| Reformulation cost | Six-figure USD |

What is included in the product

Tailored Porter's Five Forces analysis for AirBoss that uncovers key drivers of competition, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and disruptive substitutes—supported by industry data and strategic commentary for use in investor materials or internal strategy decks.

AirBoss Porter's Five Forces packs a clear one-sheet summary of competitive pressures to remove analysis bottlenecks, with customizable force levels and a ready-to-use radar chart for instant strategic clarity. Designed for easy slide insertion and non-technical use, it speeds decisions across scenarios without macros or coding.

Customers Bargaining Power

Automotive OEMs’ scale and pricing pressure

Automotive OEMs buy at high volumes and run aggressive competitive bids, typically driving annual cost-downs of about 2–5% and demanding just-in-time OTIF performance often targeted at 95–99% in 2024. They exert strong price pressure through consolidated purchasing and multi-sourcing programs. Approved-vendor status plus tooling and qualification — frequently costing upwards of $250k and taking 6–12 months — create switching frictions. Buyer power is high but mitigated by technical lock-in and long qualification cycles.

Defense procurement concentration

Government agencies and a handful of large prime contractors concentrate demand—US DoD budget reached about 858 billion USD in 2024, channeling significant procurement through few buyers. ID/IQ and competitive tender frameworks give these buyers leverage on pricing, terms and compliance. CBRN mission-critical performance shifts focus from lowest price, and long testing cycles plus past-performance records materially limit supplier switching.

Customization reduces comparability

Bespoke rubber compounds and PPE configurations make apples-to-apples price comparisons difficult, reducing buyers' ability to push for commodity-like discounts. Engineering collaboration embeds AirBoss (AirBoss of America, ticker AIR.TO/BOSS) early in design cycles, creating product and process stickiness. Higher switching costs from validated specs and supply-chain qualifications weaken customer bargaining power. This dynamic shifts leverage toward the supplier.

Demand cyclicality and budget cycles

Auto and industrial downturns intensify buyer push for concessions, while defense budget allocations and surge purchases periodically shift buyers into allocation mode, reducing leverage; AirBoss therefore faces alternating tight and loose buyer power that raises margin volatility. Contract mix diversification across defense, industrial, and specialty rubber products smooths revenue swings and bargaining exposure.

- Buyers: cyclical pressure vs allocation relief

- Risk: margin volatility

- Mitigation: diversified contract mix

Quality, delivery, and compliance dependencies

Buyers demand stringent QA, traceability, and regulatory compliance (NIOSH, FDA, ISO 13485/9001), narrowing viable suppliers and raising switching costs; in PPE markets failure risk and liability make price-based switching unlikely.

Contracts emphasize performance guarantees and penalties, shaping margins and negotiation leverage, while reliable on‑time delivery histories gradually erode buyer power.

- QA/regulatory: NIOSH/FDA/ISO compliance required

- Switching barrier: high due to liability and traceability

- Negotiation drivers: performance guarantees, penalties

- Delivery: consistent performance reduces buyer leverage

OEMs & DoD squeeze suppliers: 2–5% cuts, 95–99% OTIF, tooling > $250k

Automotive OEMs exert high buyer power via large-volume competitive bids driving 2–5% annual cost‑downs and requiring 95–99% OTIF in 2024. US DoD procurement (≈858bn USD in 2024) concentrates demand and negotiates terms, though CBRN performance needs limit pure price plays. Tooling/qualification costs (often >250k USD, 6–12 months) and regulatory QA (NIOSH/FDA/ISO) raise switching costs. Net: strong buyer pressure offset by technical lock‑in and long qualification cycles.

Same Document Delivered

AirBoss Porter's Five Forces Analysis

This preview shows the exact AirBoss Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The full, professionally formatted document is downloadable immediately after payment and ready for use in presentations or due diligence. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

AirBoss faces moderate supplier power due to specialized materials, while buyer power is tempered by niche industrial customers; competitive rivalry is intense from global PPE and rubber firms. Barriers to entry are moderate—scale and regulatory compliance matter—and substitutes pose a limited but growing threat. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AirBoss’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated petrochemical feedstocks

AirBoss depends on synthetic rubbers, carbon black and specialty chemicals from a concentrated petrochemical base, where supply tightness or outages rapidly translate into pricing leverage for upstream suppliers. Hedging and long-term contracts mitigate some risk but notable spot exposure remains, leaving margins sensitive to feedstock swings; Brent crude averaged about $86/bbl in 2024. Volatility in oil and natural latex amplifies suppliers’ bargaining power, pressuring input costs and pass-through flexibility.

Specialty CBRN materials scarcity

CBRN filters, impregnated activated carbon adsorbents and aramid textiles are sourced from a narrow, often single-digit pool of qualified vendors, and strict security and qualification requirements further thin that pool. Certification and testing timelines typically take 6–12 months, so dual-sourcing is possible but slow. Niche sorbent suppliers command meaningful premiums in surge periods, tightening supplier clout and margin pressure on AirBoss.

Energy and logistics cost pass-through

Rubber compounding is energy-intensive and freight-heavy, so utilities and carriers exert indirect leverage over AirBoss; European TTF gas surged over 300% in 2022, underpinning pervasive energy pass-throughs. Suppliers routinely levy energy surcharges during spikes, and although AirBoss negotiates tiered rates, timing mismatches between spot spikes and contract tiers squeeze margins. Nearshoring and inventory buffers blunt but do not eliminate this pressure.

Switching costs from formulation lock-in

Compound performance depends on precise ingredient specs; changing suppliers forces reformulation and validation, creating technical lock-in that strengthens incumbent suppliers. In defense PPE requalification routinely takes months (commonly 3–6 months) and can incur six-figure costs, limiting rapid supplier substitution during price disputes.

- 3–6 months requalification

- Six-figure reformulation/validation costs

- Technical lock-in raises supplier leverage

Commodity vs. specialty mix

For commodity inputs global supply offers negotiating leverage; world natural rubber production was about 13 million tonnes in 2024 (IRSG), increasing sourcing options and price competition. Specialty additives and bespoke textiles remain concentrated among few suppliers, raising switching costs and limiting competition. The blended basket yields moderate overall supplier power, mitigated by mix management and strategic partnerships.

- Commodity leverage: global rubber ~13 Mt (2024)

- Specialty constraint: few bespoke additive/textile vendors

- Mitigants: supplier mix, long-term partnerships, strategic sourcing

Supplier power rises as Brent $86/bbl and technical lock-in increase costs

AirBoss faces moderate-to-high supplier power: feedstock price swings (Brent ~$86/bbl in 2024) and concentrated specialty vendors raise costs and switching barriers. Requalification (3–6 months) and six-figure validation costs create technical lock-in, while global rubber supply (~13 Mt in 2024) provides some commodity leverage. Strategic contracts and nearshoring partially mitigate supplier clout.

| Metric | 2024 value |

|---|---|

| Brent crude | $86/bbl |

| Natural rubber production | ~13 Mt |

| Requalification time | 3–6 months |

| Reformulation cost | Six-figure USD |

What is included in the product

Tailored Porter's Five Forces analysis for AirBoss that uncovers key drivers of competition, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and disruptive substitutes—supported by industry data and strategic commentary for use in investor materials or internal strategy decks.

AirBoss Porter's Five Forces packs a clear one-sheet summary of competitive pressures to remove analysis bottlenecks, with customizable force levels and a ready-to-use radar chart for instant strategic clarity. Designed for easy slide insertion and non-technical use, it speeds decisions across scenarios without macros or coding.

Customers Bargaining Power

Automotive OEMs’ scale and pricing pressure

Automotive OEMs buy at high volumes and run aggressive competitive bids, typically driving annual cost-downs of about 2–5% and demanding just-in-time OTIF performance often targeted at 95–99% in 2024. They exert strong price pressure through consolidated purchasing and multi-sourcing programs. Approved-vendor status plus tooling and qualification — frequently costing upwards of $250k and taking 6–12 months — create switching frictions. Buyer power is high but mitigated by technical lock-in and long qualification cycles.

Defense procurement concentration

Government agencies and a handful of large prime contractors concentrate demand—US DoD budget reached about 858 billion USD in 2024, channeling significant procurement through few buyers. ID/IQ and competitive tender frameworks give these buyers leverage on pricing, terms and compliance. CBRN mission-critical performance shifts focus from lowest price, and long testing cycles plus past-performance records materially limit supplier switching.

Customization reduces comparability

Bespoke rubber compounds and PPE configurations make apples-to-apples price comparisons difficult, reducing buyers' ability to push for commodity-like discounts. Engineering collaboration embeds AirBoss (AirBoss of America, ticker AIR.TO/BOSS) early in design cycles, creating product and process stickiness. Higher switching costs from validated specs and supply-chain qualifications weaken customer bargaining power. This dynamic shifts leverage toward the supplier.

Demand cyclicality and budget cycles

Auto and industrial downturns intensify buyer push for concessions, while defense budget allocations and surge purchases periodically shift buyers into allocation mode, reducing leverage; AirBoss therefore faces alternating tight and loose buyer power that raises margin volatility. Contract mix diversification across defense, industrial, and specialty rubber products smooths revenue swings and bargaining exposure.

- Buyers: cyclical pressure vs allocation relief

- Risk: margin volatility

- Mitigation: diversified contract mix

Quality, delivery, and compliance dependencies

Buyers demand stringent QA, traceability, and regulatory compliance (NIOSH, FDA, ISO 13485/9001), narrowing viable suppliers and raising switching costs; in PPE markets failure risk and liability make price-based switching unlikely.

Contracts emphasize performance guarantees and penalties, shaping margins and negotiation leverage, while reliable on‑time delivery histories gradually erode buyer power.

- QA/regulatory: NIOSH/FDA/ISO compliance required

- Switching barrier: high due to liability and traceability

- Negotiation drivers: performance guarantees, penalties

- Delivery: consistent performance reduces buyer leverage

OEMs & DoD squeeze suppliers: 2–5% cuts, 95–99% OTIF, tooling > $250k

Automotive OEMs exert high buyer power via large-volume competitive bids driving 2–5% annual cost‑downs and requiring 95–99% OTIF in 2024. US DoD procurement (≈858bn USD in 2024) concentrates demand and negotiates terms, though CBRN performance needs limit pure price plays. Tooling/qualification costs (often >250k USD, 6–12 months) and regulatory QA (NIOSH/FDA/ISO) raise switching costs. Net: strong buyer pressure offset by technical lock‑in and long qualification cycles.

Same Document Delivered

AirBoss Porter's Five Forces Analysis

This preview shows the exact AirBoss Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The full, professionally formatted document is downloadable immediately after payment and ready for use in presentations or due diligence. What you see is what you get.