Air Lease Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

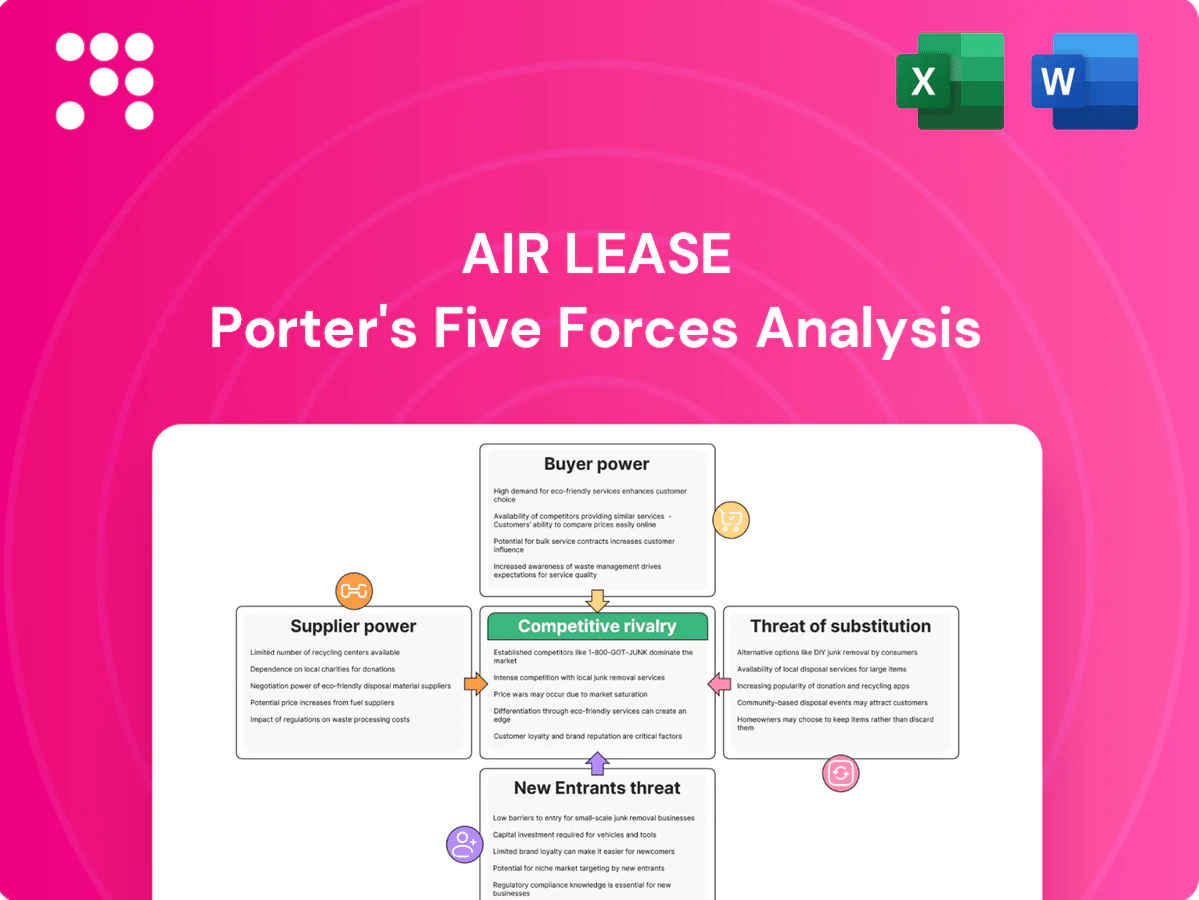

Air Lease’s Porter’s Five Forces snapshot highlights supplier leverage, buyer concentration, moderate threat of new entrants, substitution risks, and intense competitive rivalry in aircraft leasing. This brief teases strategic implications and risk hotspots. Unlock the full Porter’s Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to Air Lease.

Suppliers Bargaining Power

OEM duopoly limits choice

Airbus and Boeing together supply roughly 90% of new commercial narrowbody and widebody aircraft, concentrating bargaining power upstream; limited alternative airframe producers restrict ALC’s ability to play vendors off each other. Multi-year delivery lead times often extend 5–7 years, and slot scarcity forces acceptance of OEM terms to secure timelines. This concentration can push up pricing (A320neo list ~US$110m) and limit customization of commercial terms for ALC.

Engine makers’ leverage via tech

Engine OEMs shape total lifecycle cost and residuals through engine-centric aftermarket packages; in 2024 OEM aftermarket control remained central to lessors’ cost forecasts. Power-by-the-hour and maintenance program tie-ins can lock Air Lease into specific cost structures and cashflow timings. Certification and warranty rules limit switching across variants, giving engine suppliers meaningful negotiating leverage over specifications and pricing.

Delivery slot scarcity premium

Backlogs and production volatility make early delivery slots scarce and valuable, with OEM backlogs exceeding 6,000 aircraft in 2024, especially for high-demand models. ALC, with roughly 550 aircraft owned or managed in 2024, may accept higher prices or tighter terms to secure timely deliveries for airline clients. Schedule delays shift risk to lessors, compressing lease start yields, and scarcity elevates supplier power during demand upcycles.

Contractual escalators and terms

OEM pricing commonly includes escalation clauses tied to labor and material indices such as producer price indices; these pass-throughs can raise capex mid-production and pressure target lease rate factors. Penalties, progressive deposit payment (PDP) schedules and cancellation terms typically favor OEMs, reducing Air Lease Corporations ability to renegotiate when market conditions change.

- Escalators tied to labor/material indices

- Mid-production capex increases

- PDPs and cancellation penalties favor OEMs

- Limits ALC renegotiation flexibility

Switching and spec constraints

Changing aircraft types late in the cycle is costly: certification and pilot type‑rating programs commonly take 12–24 months and cost $10k–$50k per pilot, plus lease and customer rebooking penalties; Boeing and Airbus accounted for over 95% of 2023 commercial jet orders, concentrating supplier power. Custom specs tied to airline orders limit interchangeability across lessees, and technical commonality needs further narrow pivot options, raising dependence on incumbent suppliers’ roadmaps.

- Certification delay: 12–24 months

- Type‑rating cost: $10k–$50k per pilot

- Market concentration: >95% orders to Boeing/Airbus (2023)

OEM duopoly, >6,000 backlog and power-by-the-hour engines squeeze lessors' flexibility

Airbus and Boeing supply ~90% of new jets, concentrating supplier leverage; 2024 OEM backlogs exceeded 6,000 aircraft, forcing ALC (≈550 aircraft owned/managed in 2024) to accept OEM terms. Engine OEM aftermarket control remained central in 2024, with power-by-the-hour tie-ins affecting lifecycle costs. A320neo list ≈US$110m and certification delays (12–24 months) limit ALC flexibility.

| Metric | 2024 |

|---|---|

| OEM market share | ~90% |

| OEM backlog | >6,000 |

| ALC fleet (owned/managed) | ≈550 |

| A320neo list | ~US$110m |

What is included in the product

Provides a tailored Porter’s Five Forces analysis for Air Lease, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and regulatory risks while highlighting disruptive trends and strategic levers affecting pricing, profitability and market positioning.

A concise, one-sheet Porter's Five Forces for Air Lease—instantly highlights competitive pressures and actionable relief points for strategic decisions and investor briefings.

Customers Bargaining Power

Airline consolidation scale

IATA reported global RPKs recovered to 2019 levels in 2024, and US Big Three carriers (Delta, American, United) held roughly 70% of US domestic capacity in 2024, enabling mega-carriers and alliances to negotiate at scale and press lease rates and incentives. Large buyers frequently place multi-aircraft deals, demanding better economics, and their traffic rights and market share make them highly attractive counterparties ALC must compete to win, boosting buyer power in key regions.

Alternatives: SLB and debt

Airlines can use sale-leasebacks, bank loans or ECA-backed debt as credible alternatives to ALC leases, with global SLB activity remaining in the multi-billion dollar range in 2024 while US 10-year yields averaged about 4.5% mid-year, making borrowing more accessible. These outside options intensify pricing pressure, compress lease rate factors and force longer or deeper concessions as capital markets availability raises customer leverage.

Rate sensitivity to macro

Interest rates, fuel prices and residual outlooks flow directly into lease pricing — 10‑yr UST moves in 2024 (~4.5% to ~3.9%) and Brent ~84 USD/bbl tightened LRF negotiations. When funding costs fall or values rise, airlines push for lower LRFs; conversely weak airline credits demand higher yields or security packages. Buyers time deals to sign when terms are most favorable, exploiting 2024 windows.

Credit risk and terms

Weaker airline credits accept stricter covenants, higher deposits and maintenance reserves, diluting customer bargaining power, while stronger credits extract lower deposits and more flexible return conditions; global demand backdrop (IMF 2024 global GDP ~3.1%) supports stronger carriers' leverage. Repossession jurisdiction and ground infrastructure materially affect enforceability and pricing, and credit dispersion creates uneven buyer power across ALC’s customer base.

- Weaker credits: higher covenants/deposits

- Strong credits: lower deposits, flexible returns

- Jurisdiction and infrastructure drive repo risk/pricing

- Credit dispersion = uneven bargaining power

Fleet commonality preferences

Airlines prioritize fleet commonality to match pilot training and MRO footprints, narrowing acceptable models and constraining ALC’s placement options; in 2024 narrowbody delivery backlogs exceeded four years, tightening acceptable swaps and increasing the value of common-type placements.

Buyers press specification fit to extract better pricing, but unique or late-cycle placements give airlines less leverage when supply is tight.

- Commonality limits acceptable alternatives

- ALC placement subset shrinks

- Specification fit used to negotiate price

- Supply tightness reduces buyer leverage

Customers gain leverage as RPKs recover and US Big Three capacity sits at ~70%

In 2024 customers held elevated bargaining power: global RPKs back to 2019 and US Big Three ~70% domestic capacity enabled large airlines to demand lower LRFs and incentives. Sale-leasebacks stayed multi-billion, and 10y UST ~4.5% mid-2024 gave airlines credible financing alternatives, compressing lease spreads. Credit dispersion meant strong carriers secured softer terms while weak credits accepted higher deposits and covenants.

| Metric | 2024 |

|---|---|

| RPK vs 2019 | Recovered |

| US Big Three capacity | ~70% |

| 10y UST (mid-2024) | ~4.5% |

| Brent | ~84 USD/bbl |

Same Document Delivered

Air Lease Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Air Lease you'll receive immediately after purchase—fully formatted and ready to use. The content covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with supporting evidence and strategic implications. No placeholders or samples—this file is the final deliverable available for instant download.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Air Lease’s Porter’s Five Forces snapshot highlights supplier leverage, buyer concentration, moderate threat of new entrants, substitution risks, and intense competitive rivalry in aircraft leasing. This brief teases strategic implications and risk hotspots. Unlock the full Porter’s Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to Air Lease.

Suppliers Bargaining Power

OEM duopoly limits choice

Airbus and Boeing together supply roughly 90% of new commercial narrowbody and widebody aircraft, concentrating bargaining power upstream; limited alternative airframe producers restrict ALC’s ability to play vendors off each other. Multi-year delivery lead times often extend 5–7 years, and slot scarcity forces acceptance of OEM terms to secure timelines. This concentration can push up pricing (A320neo list ~US$110m) and limit customization of commercial terms for ALC.

Engine makers’ leverage via tech

Engine OEMs shape total lifecycle cost and residuals through engine-centric aftermarket packages; in 2024 OEM aftermarket control remained central to lessors’ cost forecasts. Power-by-the-hour and maintenance program tie-ins can lock Air Lease into specific cost structures and cashflow timings. Certification and warranty rules limit switching across variants, giving engine suppliers meaningful negotiating leverage over specifications and pricing.

Delivery slot scarcity premium

Backlogs and production volatility make early delivery slots scarce and valuable, with OEM backlogs exceeding 6,000 aircraft in 2024, especially for high-demand models. ALC, with roughly 550 aircraft owned or managed in 2024, may accept higher prices or tighter terms to secure timely deliveries for airline clients. Schedule delays shift risk to lessors, compressing lease start yields, and scarcity elevates supplier power during demand upcycles.

Contractual escalators and terms

OEM pricing commonly includes escalation clauses tied to labor and material indices such as producer price indices; these pass-throughs can raise capex mid-production and pressure target lease rate factors. Penalties, progressive deposit payment (PDP) schedules and cancellation terms typically favor OEMs, reducing Air Lease Corporations ability to renegotiate when market conditions change.

- Escalators tied to labor/material indices

- Mid-production capex increases

- PDPs and cancellation penalties favor OEMs

- Limits ALC renegotiation flexibility

Switching and spec constraints

Changing aircraft types late in the cycle is costly: certification and pilot type‑rating programs commonly take 12–24 months and cost $10k–$50k per pilot, plus lease and customer rebooking penalties; Boeing and Airbus accounted for over 95% of 2023 commercial jet orders, concentrating supplier power. Custom specs tied to airline orders limit interchangeability across lessees, and technical commonality needs further narrow pivot options, raising dependence on incumbent suppliers’ roadmaps.

- Certification delay: 12–24 months

- Type‑rating cost: $10k–$50k per pilot

- Market concentration: >95% orders to Boeing/Airbus (2023)

OEM duopoly, >6,000 backlog and power-by-the-hour engines squeeze lessors' flexibility

Airbus and Boeing supply ~90% of new jets, concentrating supplier leverage; 2024 OEM backlogs exceeded 6,000 aircraft, forcing ALC (≈550 aircraft owned/managed in 2024) to accept OEM terms. Engine OEM aftermarket control remained central in 2024, with power-by-the-hour tie-ins affecting lifecycle costs. A320neo list ≈US$110m and certification delays (12–24 months) limit ALC flexibility.

| Metric | 2024 |

|---|---|

| OEM market share | ~90% |

| OEM backlog | >6,000 |

| ALC fleet (owned/managed) | ≈550 |

| A320neo list | ~US$110m |

What is included in the product

Provides a tailored Porter’s Five Forces analysis for Air Lease, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and regulatory risks while highlighting disruptive trends and strategic levers affecting pricing, profitability and market positioning.

A concise, one-sheet Porter's Five Forces for Air Lease—instantly highlights competitive pressures and actionable relief points for strategic decisions and investor briefings.

Customers Bargaining Power

Airline consolidation scale

IATA reported global RPKs recovered to 2019 levels in 2024, and US Big Three carriers (Delta, American, United) held roughly 70% of US domestic capacity in 2024, enabling mega-carriers and alliances to negotiate at scale and press lease rates and incentives. Large buyers frequently place multi-aircraft deals, demanding better economics, and their traffic rights and market share make them highly attractive counterparties ALC must compete to win, boosting buyer power in key regions.

Alternatives: SLB and debt

Airlines can use sale-leasebacks, bank loans or ECA-backed debt as credible alternatives to ALC leases, with global SLB activity remaining in the multi-billion dollar range in 2024 while US 10-year yields averaged about 4.5% mid-year, making borrowing more accessible. These outside options intensify pricing pressure, compress lease rate factors and force longer or deeper concessions as capital markets availability raises customer leverage.

Rate sensitivity to macro

Interest rates, fuel prices and residual outlooks flow directly into lease pricing — 10‑yr UST moves in 2024 (~4.5% to ~3.9%) and Brent ~84 USD/bbl tightened LRF negotiations. When funding costs fall or values rise, airlines push for lower LRFs; conversely weak airline credits demand higher yields or security packages. Buyers time deals to sign when terms are most favorable, exploiting 2024 windows.

Credit risk and terms

Weaker airline credits accept stricter covenants, higher deposits and maintenance reserves, diluting customer bargaining power, while stronger credits extract lower deposits and more flexible return conditions; global demand backdrop (IMF 2024 global GDP ~3.1%) supports stronger carriers' leverage. Repossession jurisdiction and ground infrastructure materially affect enforceability and pricing, and credit dispersion creates uneven buyer power across ALC’s customer base.

- Weaker credits: higher covenants/deposits

- Strong credits: lower deposits, flexible returns

- Jurisdiction and infrastructure drive repo risk/pricing

- Credit dispersion = uneven bargaining power

Fleet commonality preferences

Airlines prioritize fleet commonality to match pilot training and MRO footprints, narrowing acceptable models and constraining ALC’s placement options; in 2024 narrowbody delivery backlogs exceeded four years, tightening acceptable swaps and increasing the value of common-type placements.

Buyers press specification fit to extract better pricing, but unique or late-cycle placements give airlines less leverage when supply is tight.

- Commonality limits acceptable alternatives

- ALC placement subset shrinks

- Specification fit used to negotiate price

- Supply tightness reduces buyer leverage

Customers gain leverage as RPKs recover and US Big Three capacity sits at ~70%

In 2024 customers held elevated bargaining power: global RPKs back to 2019 and US Big Three ~70% domestic capacity enabled large airlines to demand lower LRFs and incentives. Sale-leasebacks stayed multi-billion, and 10y UST ~4.5% mid-2024 gave airlines credible financing alternatives, compressing lease spreads. Credit dispersion meant strong carriers secured softer terms while weak credits accepted higher deposits and covenants.

| Metric | 2024 |

|---|---|

| RPK vs 2019 | Recovered |

| US Big Three capacity | ~70% |

| 10y UST (mid-2024) | ~4.5% |

| Brent | ~84 USD/bbl |

Same Document Delivered

Air Lease Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Air Lease you'll receive immediately after purchase—fully formatted and ready to use. The content covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with supporting evidence and strategic implications. No placeholders or samples—this file is the final deliverable available for instant download.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Air Lease’s Porter’s Five Forces snapshot highlights supplier leverage, buyer concentration, moderate threat of new entrants, substitution risks, and intense competitive rivalry in aircraft leasing. This brief teases strategic implications and risk hotspots. Unlock the full Porter’s Five Forces Analysis to get force-by-force ratings, visuals, and actionable recommendations tailored to Air Lease.

Suppliers Bargaining Power

OEM duopoly limits choice

Airbus and Boeing together supply roughly 90% of new commercial narrowbody and widebody aircraft, concentrating bargaining power upstream; limited alternative airframe producers restrict ALC’s ability to play vendors off each other. Multi-year delivery lead times often extend 5–7 years, and slot scarcity forces acceptance of OEM terms to secure timelines. This concentration can push up pricing (A320neo list ~US$110m) and limit customization of commercial terms for ALC.

Engine makers’ leverage via tech

Engine OEMs shape total lifecycle cost and residuals through engine-centric aftermarket packages; in 2024 OEM aftermarket control remained central to lessors’ cost forecasts. Power-by-the-hour and maintenance program tie-ins can lock Air Lease into specific cost structures and cashflow timings. Certification and warranty rules limit switching across variants, giving engine suppliers meaningful negotiating leverage over specifications and pricing.

Delivery slot scarcity premium

Backlogs and production volatility make early delivery slots scarce and valuable, with OEM backlogs exceeding 6,000 aircraft in 2024, especially for high-demand models. ALC, with roughly 550 aircraft owned or managed in 2024, may accept higher prices or tighter terms to secure timely deliveries for airline clients. Schedule delays shift risk to lessors, compressing lease start yields, and scarcity elevates supplier power during demand upcycles.

Contractual escalators and terms

OEM pricing commonly includes escalation clauses tied to labor and material indices such as producer price indices; these pass-throughs can raise capex mid-production and pressure target lease rate factors. Penalties, progressive deposit payment (PDP) schedules and cancellation terms typically favor OEMs, reducing Air Lease Corporations ability to renegotiate when market conditions change.

- Escalators tied to labor/material indices

- Mid-production capex increases

- PDPs and cancellation penalties favor OEMs

- Limits ALC renegotiation flexibility

Switching and spec constraints

Changing aircraft types late in the cycle is costly: certification and pilot type‑rating programs commonly take 12–24 months and cost $10k–$50k per pilot, plus lease and customer rebooking penalties; Boeing and Airbus accounted for over 95% of 2023 commercial jet orders, concentrating supplier power. Custom specs tied to airline orders limit interchangeability across lessees, and technical commonality needs further narrow pivot options, raising dependence on incumbent suppliers’ roadmaps.

- Certification delay: 12–24 months

- Type‑rating cost: $10k–$50k per pilot

- Market concentration: >95% orders to Boeing/Airbus (2023)

OEM duopoly, >6,000 backlog and power-by-the-hour engines squeeze lessors' flexibility

Airbus and Boeing supply ~90% of new jets, concentrating supplier leverage; 2024 OEM backlogs exceeded 6,000 aircraft, forcing ALC (≈550 aircraft owned/managed in 2024) to accept OEM terms. Engine OEM aftermarket control remained central in 2024, with power-by-the-hour tie-ins affecting lifecycle costs. A320neo list ≈US$110m and certification delays (12–24 months) limit ALC flexibility.

| Metric | 2024 |

|---|---|

| OEM market share | ~90% |

| OEM backlog | >6,000 |

| ALC fleet (owned/managed) | ≈550 |

| A320neo list | ~US$110m |

What is included in the product

Provides a tailored Porter’s Five Forces analysis for Air Lease, uncovering competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and regulatory risks while highlighting disruptive trends and strategic levers affecting pricing, profitability and market positioning.

A concise, one-sheet Porter's Five Forces for Air Lease—instantly highlights competitive pressures and actionable relief points for strategic decisions and investor briefings.

Customers Bargaining Power

Airline consolidation scale

IATA reported global RPKs recovered to 2019 levels in 2024, and US Big Three carriers (Delta, American, United) held roughly 70% of US domestic capacity in 2024, enabling mega-carriers and alliances to negotiate at scale and press lease rates and incentives. Large buyers frequently place multi-aircraft deals, demanding better economics, and their traffic rights and market share make them highly attractive counterparties ALC must compete to win, boosting buyer power in key regions.

Alternatives: SLB and debt

Airlines can use sale-leasebacks, bank loans or ECA-backed debt as credible alternatives to ALC leases, with global SLB activity remaining in the multi-billion dollar range in 2024 while US 10-year yields averaged about 4.5% mid-year, making borrowing more accessible. These outside options intensify pricing pressure, compress lease rate factors and force longer or deeper concessions as capital markets availability raises customer leverage.

Rate sensitivity to macro

Interest rates, fuel prices and residual outlooks flow directly into lease pricing — 10‑yr UST moves in 2024 (~4.5% to ~3.9%) and Brent ~84 USD/bbl tightened LRF negotiations. When funding costs fall or values rise, airlines push for lower LRFs; conversely weak airline credits demand higher yields or security packages. Buyers time deals to sign when terms are most favorable, exploiting 2024 windows.

Credit risk and terms

Weaker airline credits accept stricter covenants, higher deposits and maintenance reserves, diluting customer bargaining power, while stronger credits extract lower deposits and more flexible return conditions; global demand backdrop (IMF 2024 global GDP ~3.1%) supports stronger carriers' leverage. Repossession jurisdiction and ground infrastructure materially affect enforceability and pricing, and credit dispersion creates uneven buyer power across ALC’s customer base.

- Weaker credits: higher covenants/deposits

- Strong credits: lower deposits, flexible returns

- Jurisdiction and infrastructure drive repo risk/pricing

- Credit dispersion = uneven bargaining power

Fleet commonality preferences

Airlines prioritize fleet commonality to match pilot training and MRO footprints, narrowing acceptable models and constraining ALC’s placement options; in 2024 narrowbody delivery backlogs exceeded four years, tightening acceptable swaps and increasing the value of common-type placements.

Buyers press specification fit to extract better pricing, but unique or late-cycle placements give airlines less leverage when supply is tight.

- Commonality limits acceptable alternatives

- ALC placement subset shrinks

- Specification fit used to negotiate price

- Supply tightness reduces buyer leverage

Customers gain leverage as RPKs recover and US Big Three capacity sits at ~70%

In 2024 customers held elevated bargaining power: global RPKs back to 2019 and US Big Three ~70% domestic capacity enabled large airlines to demand lower LRFs and incentives. Sale-leasebacks stayed multi-billion, and 10y UST ~4.5% mid-2024 gave airlines credible financing alternatives, compressing lease spreads. Credit dispersion meant strong carriers secured softer terms while weak credits accepted higher deposits and covenants.

| Metric | 2024 |

|---|---|

| RPK vs 2019 | Recovered |

| US Big Three capacity | ~70% |

| 10y UST (mid-2024) | ~4.5% |

| Brent | ~84 USD/bbl |

Same Document Delivered

Air Lease Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Air Lease you'll receive immediately after purchase—fully formatted and ready to use. The content covers supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry with supporting evidence and strategic implications. No placeholders or samples—this file is the final deliverable available for instant download.