Air Products & Chemicals Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

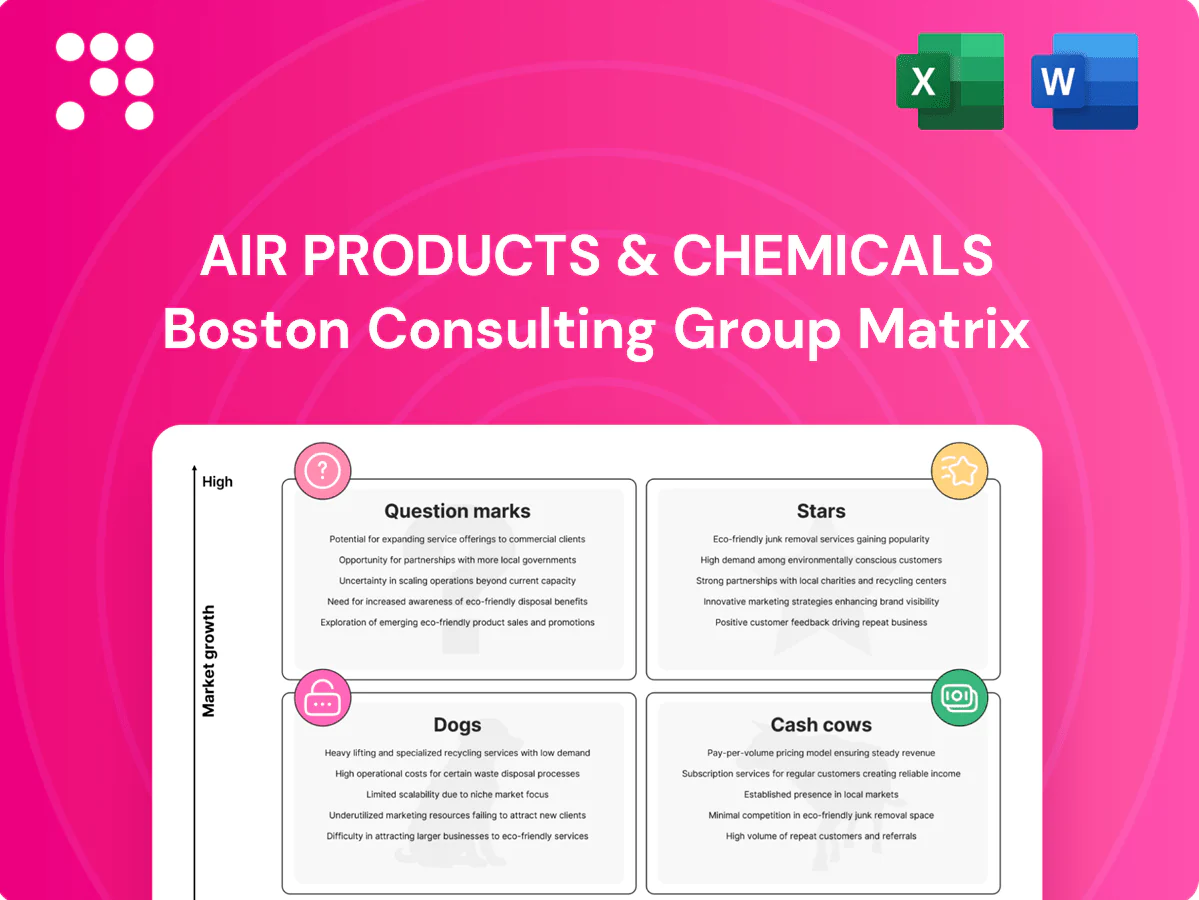

Air Products & Chemicals sits at an interesting crossroads—certain gas and industrial segments look like Stars, some legacy units behave like steady Cash Cows, and a few lines feel like Question Marks asking for capital and focus. This snapshot teases the strategic levers; the full BCG Matrix gives you quadrant-by-quadrant placement, clear recommendations, and the numbers behind the moves. Buy the complete report for a ready-to-use Word analysis plus a high-level Excel summary and start reallocating capital with confidence.

Stars

Large-scale hydrogen (energy transition)

Air Products is a front-runner in mega blue and green hydrogen projects, with announced multi‑billion dollar investments (cumulative project contracts reported above $10bn by 2024) positioned where demand is ramping.

Global hydrogen deployment for mobility, refining decarbonization and power blending is accelerating, with policy and offtake markets expanding rapidly through the mid-2020s.

Big capex is required, but APD’s project leadership and long-term offtake deals sustain high market share and de‑risk rollout.

Keep feeding this growth platform—today’s star has the scale and contracted revenues to become tomorrow’s cash cow.

On-site gases for refining & petrochem

On-site gases for refining & petrochem benefit from locked-in, long-term take-or-pay contracts and extensive pipeline networks that give Air Products real scale advantages. Customers upgrading to cleaner fuels are driving volume growth; Air Products reported FY2024 revenue of $12.9 billion, reflecting strength in industrial gases. Brutal switching costs and embedded infrastructure sustain high share in a growing market slice. Continued growth still requires disciplined capex and uptime excellence to protect margins and throughput.

Electronics specialty gases

Electronics specialty gases are a Star as semiconductor and display fabs continued to expand in 2024, with SEMI reporting elevated fab investment levels; ultra-high-purity gases scale with that expansion. Air Products is entrenched with global OEMs and fabs, holding strong share in key nodes. Growth is cyclical but structurally upward; continued investment in purity, logistics, and local fab capacity is required to lock in leadership.

Blue ammonia export platforms

Blue ammonia export platforms sit in Air Products BCG Matrix as high-growth, high-visibility stars: APD’s integrated H2-to-ammonia plays are early but scaled, leveraging SMR+CCS tech with ~90% CO2 capture potential and policy tailwinds such as the US IRA and EU REPowerEU that accelerate demand from energy-importing countries. First-mover sites and strategic offtake partnerships create a commercial moat; execution and contracted offtakes will determine cash conversion.

- High growth: rising export demand from energy-importing nations

- Visibility: policy support (IRA, REPowerEU) boosts project bankability

- Moat: first-mover sites, long-term offtakes

- Execution risk: delivery and CCS performance critical

Gasification-as-a-service

Gasification-as-a-service delivers turnkey syngas plants, financing, and operations so industrial and energy clients get syngas without owning complexity; Air Products’ integrated EPC+F model is operationally hard to copy.

Pipeline is concentrating in growth regions (Middle East, Asia) with rising demand for low-carbon fuels and chemicals; keeping the project machine humming is critical.

- Value proposition: turnkey + financing + O&M

- Moat: integrated project execution

- Growth focus: Middle East, Asia

Mega H2, electronics gases & blue ammonia; FY2024 rev $12.9bn

Air Products’ Stars (mega H2, on-site refining gases, electronics gases, blue ammonia, gasification-as-a-service) show high growth and scale: FY2024 revenue $12.9bn, cumulative project contracts >$10bn by 2024, blue ammonia ~90% CO2 capture potential; growth concentrated in Middle East and Asia with expanding offtakes and fab investments.

| Segment | 2024 metric |

|---|---|

| Revenue | $12.9bn |

| Project contracts | >$10bn |

| Blue ammonia CCS | ~90% capture |

What is included in the product

Air Products BCG Matrix: maps units into Stars, Cash Cows, Question Marks, Dogs with clear invest, hold or divest guidance.

One-page BCG Matrix placing Air Products & Chemicals units in quadrants for quick strategic clarity and exec-ready decisions.

Cash Cows

Merchant oxygen, nitrogen, argon

Merchant oxygen, nitrogen and argon are cash cows for Air Products in 2024, serving mature demand across metals, food and manufacturing with low growth but steady cash generation. A strong footprint and established bulk routes drive high utilization and pricing discipline. Focus on optimizing fill plants and logistics to extract incremental margin and improve free cash flow per ton. Maintain conservative capital deployment while maximizing operating efficiency.

Pipeline hydrogen (Gulf Coast and clusters)

Pipeline hydrogen (Gulf Coast and clusters) is a cash cow for Air Products, supplying stable volumes through an efficient, integrated network that spans roughly 1,400 miles in the US and supports over 1.0 Mtpa of delivered hydrogen; customers are sticky because connectivity and reliability are critical for refining and chemical clusters. Growth is modest (low-single-digit volume CAGR), but free cash generation is strong and incremental debottlenecking can lift returns materially.

On-site oxygen/nitrogen for steel and glass

Decades-long on-site contracts (commonly 10–20+ years) for oxygen/nitrogen in steel and glass carry >99% uptime expectations and very low customer churn, reflecting the slow single-digit market growth seen in industrial gases in 2024. Proven unit economics deliver double-digit operating margins across the on-site model; asset productivity — maximizing plant throughput and minimizing downtime — is the primary lever. Maintain high reliability and tight opex to protect cash generation.

Equipment—cryogenic ASUs (replacement/maintenance)

Equipment—cryogenic ASUs (replacement/maintenance) sit in Cash Cows: a large installed base drives recurring parts and service revenue; new ASU builds are episodic, but upkeep yields steady aftermarket margins. Air Products reported roughly $13.4 billion in 2024 revenue, with industrial gas services and equipment maintenance underpinning predictable cash flow and enabling funding for higher-risk growth projects.

- Installed base -> steady parts/service

- New builds episodic; upkeep consistent

- Know-how keeps APD top-of-list

- Cash flow funds bolder bets

Food & beverage gases

Food & beverage gases show consistent, recession-resistant demand for chilling, freezing and carbonation; APD’s dense route network in 2024 supports high asset utilization and low go-to-customer costs. Growth is tame (~low-single-digit CAGR), but the business generates strong free cash flow; disciplined price and mix management sustained margins through 2024.

- Route density: competitive moat

- Demand: recession-resistant

- Growth: low-single-digit

- Cash: significant FCF in 2024

2024 cash cows: industrial gases deliver steady FCF and sticky margins

Merchant O2/N2/Ar, pipeline H2, on-site contracts, ASU aftermarket and F&B gases are Air Products cash cows in 2024: mature low-single-digit growth but strong free cash flow supporting capex for growth projects. High route density, >99% uptime on-site, ~1,400 mi H2 network and $13.4B 2024 revenue underpin margins and customer stickiness.

| Cash Cow | 2024 | Growth | Role |

|---|---|---|---|

| Merchant O2/N2/Ar | $13.4B rev (group) | low‑SDG | High FCF |

| Pipeline H2 | >1.0 Mtpa; ~1,400 mi | low‑SDG | Stable cash |

| On‑site | Long‑term contracts | single‑digit | Sticky margins |

| ASU aftermarket | Recurring parts | flat | Predictable FCF |

Full Transparency, Always

Air Products & Chemicals BCG Matrix

The file you're previewing is the exact Air Products & Chemicals BCG Matrix report you'll receive after purchase—no watermarks, no demo slides, just the finished, fully formatted analysis. It's crafted for strategic clarity and immediate use. After buying you'll get the editable, print-ready document in your inbox—no surprises, no extra edits needed.

Visual. Strategic. Downloadable.

Air Products & Chemicals sits at an interesting crossroads—certain gas and industrial segments look like Stars, some legacy units behave like steady Cash Cows, and a few lines feel like Question Marks asking for capital and focus. This snapshot teases the strategic levers; the full BCG Matrix gives you quadrant-by-quadrant placement, clear recommendations, and the numbers behind the moves. Buy the complete report for a ready-to-use Word analysis plus a high-level Excel summary and start reallocating capital with confidence.

Stars

Large-scale hydrogen (energy transition)

Air Products is a front-runner in mega blue and green hydrogen projects, with announced multi‑billion dollar investments (cumulative project contracts reported above $10bn by 2024) positioned where demand is ramping.

Global hydrogen deployment for mobility, refining decarbonization and power blending is accelerating, with policy and offtake markets expanding rapidly through the mid-2020s.

Big capex is required, but APD’s project leadership and long-term offtake deals sustain high market share and de‑risk rollout.

Keep feeding this growth platform—today’s star has the scale and contracted revenues to become tomorrow’s cash cow.

On-site gases for refining & petrochem

On-site gases for refining & petrochem benefit from locked-in, long-term take-or-pay contracts and extensive pipeline networks that give Air Products real scale advantages. Customers upgrading to cleaner fuels are driving volume growth; Air Products reported FY2024 revenue of $12.9 billion, reflecting strength in industrial gases. Brutal switching costs and embedded infrastructure sustain high share in a growing market slice. Continued growth still requires disciplined capex and uptime excellence to protect margins and throughput.

Electronics specialty gases

Electronics specialty gases are a Star as semiconductor and display fabs continued to expand in 2024, with SEMI reporting elevated fab investment levels; ultra-high-purity gases scale with that expansion. Air Products is entrenched with global OEMs and fabs, holding strong share in key nodes. Growth is cyclical but structurally upward; continued investment in purity, logistics, and local fab capacity is required to lock in leadership.

Blue ammonia export platforms

Blue ammonia export platforms sit in Air Products BCG Matrix as high-growth, high-visibility stars: APD’s integrated H2-to-ammonia plays are early but scaled, leveraging SMR+CCS tech with ~90% CO2 capture potential and policy tailwinds such as the US IRA and EU REPowerEU that accelerate demand from energy-importing countries. First-mover sites and strategic offtake partnerships create a commercial moat; execution and contracted offtakes will determine cash conversion.

- High growth: rising export demand from energy-importing nations

- Visibility: policy support (IRA, REPowerEU) boosts project bankability

- Moat: first-mover sites, long-term offtakes

- Execution risk: delivery and CCS performance critical

Gasification-as-a-service

Gasification-as-a-service delivers turnkey syngas plants, financing, and operations so industrial and energy clients get syngas without owning complexity; Air Products’ integrated EPC+F model is operationally hard to copy.

Pipeline is concentrating in growth regions (Middle East, Asia) with rising demand for low-carbon fuels and chemicals; keeping the project machine humming is critical.

- Value proposition: turnkey + financing + O&M

- Moat: integrated project execution

- Growth focus: Middle East, Asia

Mega H2, electronics gases & blue ammonia; FY2024 rev $12.9bn

Air Products’ Stars (mega H2, on-site refining gases, electronics gases, blue ammonia, gasification-as-a-service) show high growth and scale: FY2024 revenue $12.9bn, cumulative project contracts >$10bn by 2024, blue ammonia ~90% CO2 capture potential; growth concentrated in Middle East and Asia with expanding offtakes and fab investments.

| Segment | 2024 metric |

|---|---|

| Revenue | $12.9bn |

| Project contracts | >$10bn |

| Blue ammonia CCS | ~90% capture |

What is included in the product

Air Products BCG Matrix: maps units into Stars, Cash Cows, Question Marks, Dogs with clear invest, hold or divest guidance.

One-page BCG Matrix placing Air Products & Chemicals units in quadrants for quick strategic clarity and exec-ready decisions.

Cash Cows

Merchant oxygen, nitrogen, argon

Merchant oxygen, nitrogen and argon are cash cows for Air Products in 2024, serving mature demand across metals, food and manufacturing with low growth but steady cash generation. A strong footprint and established bulk routes drive high utilization and pricing discipline. Focus on optimizing fill plants and logistics to extract incremental margin and improve free cash flow per ton. Maintain conservative capital deployment while maximizing operating efficiency.

Pipeline hydrogen (Gulf Coast and clusters)

Pipeline hydrogen (Gulf Coast and clusters) is a cash cow for Air Products, supplying stable volumes through an efficient, integrated network that spans roughly 1,400 miles in the US and supports over 1.0 Mtpa of delivered hydrogen; customers are sticky because connectivity and reliability are critical for refining and chemical clusters. Growth is modest (low-single-digit volume CAGR), but free cash generation is strong and incremental debottlenecking can lift returns materially.

On-site oxygen/nitrogen for steel and glass

Decades-long on-site contracts (commonly 10–20+ years) for oxygen/nitrogen in steel and glass carry >99% uptime expectations and very low customer churn, reflecting the slow single-digit market growth seen in industrial gases in 2024. Proven unit economics deliver double-digit operating margins across the on-site model; asset productivity — maximizing plant throughput and minimizing downtime — is the primary lever. Maintain high reliability and tight opex to protect cash generation.

Equipment—cryogenic ASUs (replacement/maintenance)

Equipment—cryogenic ASUs (replacement/maintenance) sit in Cash Cows: a large installed base drives recurring parts and service revenue; new ASU builds are episodic, but upkeep yields steady aftermarket margins. Air Products reported roughly $13.4 billion in 2024 revenue, with industrial gas services and equipment maintenance underpinning predictable cash flow and enabling funding for higher-risk growth projects.

- Installed base -> steady parts/service

- New builds episodic; upkeep consistent

- Know-how keeps APD top-of-list

- Cash flow funds bolder bets

Food & beverage gases

Food & beverage gases show consistent, recession-resistant demand for chilling, freezing and carbonation; APD’s dense route network in 2024 supports high asset utilization and low go-to-customer costs. Growth is tame (~low-single-digit CAGR), but the business generates strong free cash flow; disciplined price and mix management sustained margins through 2024.

- Route density: competitive moat

- Demand: recession-resistant

- Growth: low-single-digit

- Cash: significant FCF in 2024

2024 cash cows: industrial gases deliver steady FCF and sticky margins

Merchant O2/N2/Ar, pipeline H2, on-site contracts, ASU aftermarket and F&B gases are Air Products cash cows in 2024: mature low-single-digit growth but strong free cash flow supporting capex for growth projects. High route density, >99% uptime on-site, ~1,400 mi H2 network and $13.4B 2024 revenue underpin margins and customer stickiness.

| Cash Cow | 2024 | Growth | Role |

|---|---|---|---|

| Merchant O2/N2/Ar | $13.4B rev (group) | low‑SDG | High FCF |

| Pipeline H2 | >1.0 Mtpa; ~1,400 mi | low‑SDG | Stable cash |

| On‑site | Long‑term contracts | single‑digit | Sticky margins |

| ASU aftermarket | Recurring parts | flat | Predictable FCF |

Full Transparency, Always

Air Products & Chemicals BCG Matrix

The file you're previewing is the exact Air Products & Chemicals BCG Matrix report you'll receive after purchase—no watermarks, no demo slides, just the finished, fully formatted analysis. It's crafted for strategic clarity and immediate use. After buying you'll get the editable, print-ready document in your inbox—no surprises, no extra edits needed.

Description

Visual. Strategic. Downloadable.

Air Products & Chemicals sits at an interesting crossroads—certain gas and industrial segments look like Stars, some legacy units behave like steady Cash Cows, and a few lines feel like Question Marks asking for capital and focus. This snapshot teases the strategic levers; the full BCG Matrix gives you quadrant-by-quadrant placement, clear recommendations, and the numbers behind the moves. Buy the complete report for a ready-to-use Word analysis plus a high-level Excel summary and start reallocating capital with confidence.

Stars

Large-scale hydrogen (energy transition)

Air Products is a front-runner in mega blue and green hydrogen projects, with announced multi‑billion dollar investments (cumulative project contracts reported above $10bn by 2024) positioned where demand is ramping.

Global hydrogen deployment for mobility, refining decarbonization and power blending is accelerating, with policy and offtake markets expanding rapidly through the mid-2020s.

Big capex is required, but APD’s project leadership and long-term offtake deals sustain high market share and de‑risk rollout.

Keep feeding this growth platform—today’s star has the scale and contracted revenues to become tomorrow’s cash cow.

On-site gases for refining & petrochem

On-site gases for refining & petrochem benefit from locked-in, long-term take-or-pay contracts and extensive pipeline networks that give Air Products real scale advantages. Customers upgrading to cleaner fuels are driving volume growth; Air Products reported FY2024 revenue of $12.9 billion, reflecting strength in industrial gases. Brutal switching costs and embedded infrastructure sustain high share in a growing market slice. Continued growth still requires disciplined capex and uptime excellence to protect margins and throughput.

Electronics specialty gases

Electronics specialty gases are a Star as semiconductor and display fabs continued to expand in 2024, with SEMI reporting elevated fab investment levels; ultra-high-purity gases scale with that expansion. Air Products is entrenched with global OEMs and fabs, holding strong share in key nodes. Growth is cyclical but structurally upward; continued investment in purity, logistics, and local fab capacity is required to lock in leadership.

Blue ammonia export platforms

Blue ammonia export platforms sit in Air Products BCG Matrix as high-growth, high-visibility stars: APD’s integrated H2-to-ammonia plays are early but scaled, leveraging SMR+CCS tech with ~90% CO2 capture potential and policy tailwinds such as the US IRA and EU REPowerEU that accelerate demand from energy-importing countries. First-mover sites and strategic offtake partnerships create a commercial moat; execution and contracted offtakes will determine cash conversion.

- High growth: rising export demand from energy-importing nations

- Visibility: policy support (IRA, REPowerEU) boosts project bankability

- Moat: first-mover sites, long-term offtakes

- Execution risk: delivery and CCS performance critical

Gasification-as-a-service

Gasification-as-a-service delivers turnkey syngas plants, financing, and operations so industrial and energy clients get syngas without owning complexity; Air Products’ integrated EPC+F model is operationally hard to copy.

Pipeline is concentrating in growth regions (Middle East, Asia) with rising demand for low-carbon fuels and chemicals; keeping the project machine humming is critical.

- Value proposition: turnkey + financing + O&M

- Moat: integrated project execution

- Growth focus: Middle East, Asia

Mega H2, electronics gases & blue ammonia; FY2024 rev $12.9bn

Air Products’ Stars (mega H2, on-site refining gases, electronics gases, blue ammonia, gasification-as-a-service) show high growth and scale: FY2024 revenue $12.9bn, cumulative project contracts >$10bn by 2024, blue ammonia ~90% CO2 capture potential; growth concentrated in Middle East and Asia with expanding offtakes and fab investments.

| Segment | 2024 metric |

|---|---|

| Revenue | $12.9bn |

| Project contracts | >$10bn |

| Blue ammonia CCS | ~90% capture |

What is included in the product

Air Products BCG Matrix: maps units into Stars, Cash Cows, Question Marks, Dogs with clear invest, hold or divest guidance.

One-page BCG Matrix placing Air Products & Chemicals units in quadrants for quick strategic clarity and exec-ready decisions.

Cash Cows

Merchant oxygen, nitrogen, argon

Merchant oxygen, nitrogen and argon are cash cows for Air Products in 2024, serving mature demand across metals, food and manufacturing with low growth but steady cash generation. A strong footprint and established bulk routes drive high utilization and pricing discipline. Focus on optimizing fill plants and logistics to extract incremental margin and improve free cash flow per ton. Maintain conservative capital deployment while maximizing operating efficiency.

Pipeline hydrogen (Gulf Coast and clusters)

Pipeline hydrogen (Gulf Coast and clusters) is a cash cow for Air Products, supplying stable volumes through an efficient, integrated network that spans roughly 1,400 miles in the US and supports over 1.0 Mtpa of delivered hydrogen; customers are sticky because connectivity and reliability are critical for refining and chemical clusters. Growth is modest (low-single-digit volume CAGR), but free cash generation is strong and incremental debottlenecking can lift returns materially.

On-site oxygen/nitrogen for steel and glass

Decades-long on-site contracts (commonly 10–20+ years) for oxygen/nitrogen in steel and glass carry >99% uptime expectations and very low customer churn, reflecting the slow single-digit market growth seen in industrial gases in 2024. Proven unit economics deliver double-digit operating margins across the on-site model; asset productivity — maximizing plant throughput and minimizing downtime — is the primary lever. Maintain high reliability and tight opex to protect cash generation.

Equipment—cryogenic ASUs (replacement/maintenance)

Equipment—cryogenic ASUs (replacement/maintenance) sit in Cash Cows: a large installed base drives recurring parts and service revenue; new ASU builds are episodic, but upkeep yields steady aftermarket margins. Air Products reported roughly $13.4 billion in 2024 revenue, with industrial gas services and equipment maintenance underpinning predictable cash flow and enabling funding for higher-risk growth projects.

- Installed base -> steady parts/service

- New builds episodic; upkeep consistent

- Know-how keeps APD top-of-list

- Cash flow funds bolder bets

Food & beverage gases

Food & beverage gases show consistent, recession-resistant demand for chilling, freezing and carbonation; APD’s dense route network in 2024 supports high asset utilization and low go-to-customer costs. Growth is tame (~low-single-digit CAGR), but the business generates strong free cash flow; disciplined price and mix management sustained margins through 2024.

- Route density: competitive moat

- Demand: recession-resistant

- Growth: low-single-digit

- Cash: significant FCF in 2024

2024 cash cows: industrial gases deliver steady FCF and sticky margins

Merchant O2/N2/Ar, pipeline H2, on-site contracts, ASU aftermarket and F&B gases are Air Products cash cows in 2024: mature low-single-digit growth but strong free cash flow supporting capex for growth projects. High route density, >99% uptime on-site, ~1,400 mi H2 network and $13.4B 2024 revenue underpin margins and customer stickiness.

| Cash Cow | 2024 | Growth | Role |

|---|---|---|---|

| Merchant O2/N2/Ar | $13.4B rev (group) | low‑SDG | High FCF |

| Pipeline H2 | >1.0 Mtpa; ~1,400 mi | low‑SDG | Stable cash |

| On‑site | Long‑term contracts | single‑digit | Sticky margins |

| ASU aftermarket | Recurring parts | flat | Predictable FCF |

Full Transparency, Always

Air Products & Chemicals BCG Matrix

The file you're previewing is the exact Air Products & Chemicals BCG Matrix report you'll receive after purchase—no watermarks, no demo slides, just the finished, fully formatted analysis. It's crafted for strategic clarity and immediate use. After buying you'll get the editable, print-ready document in your inbox—no surprises, no extra edits needed.