AIXTRON Porter's Five Forces Analysis

From Overview to Strategy Blueprint

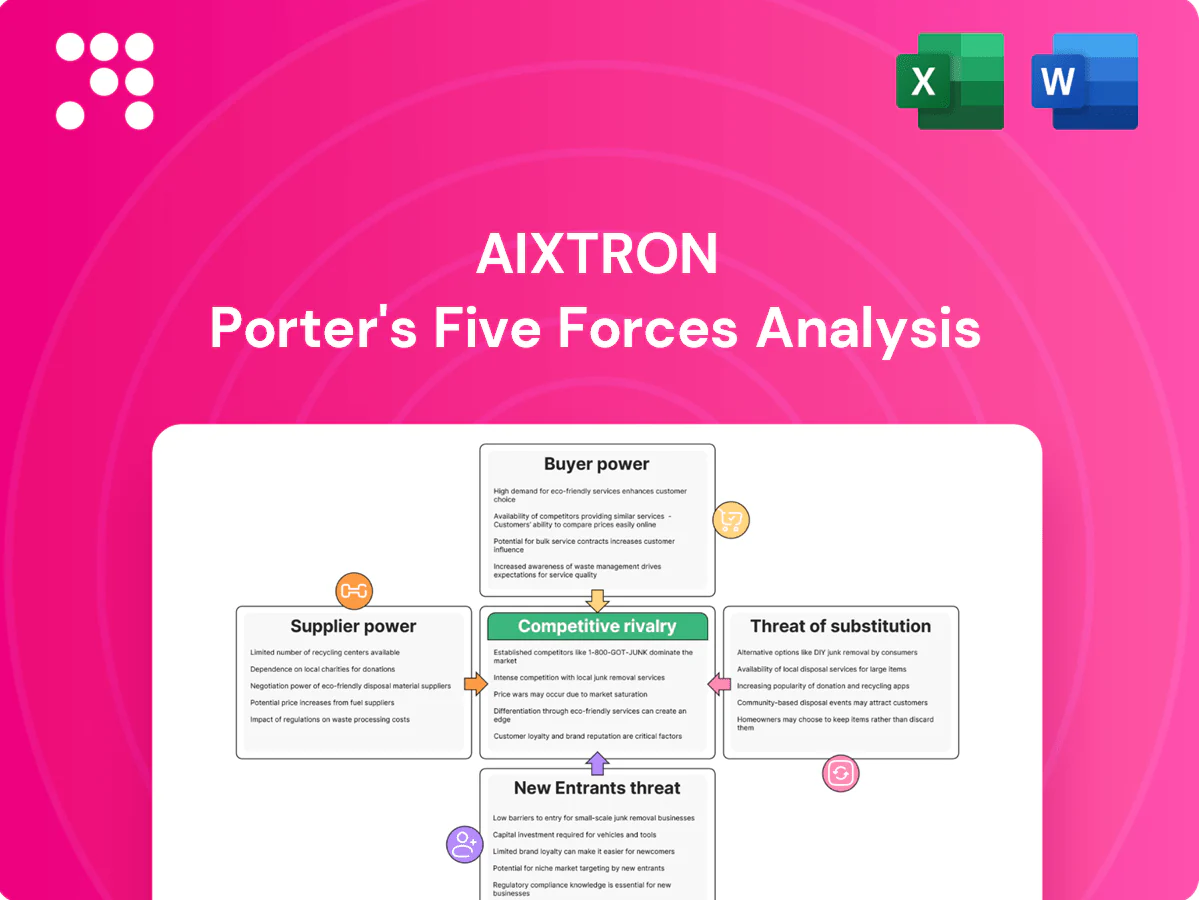

AIXTRON’s Porter’s Five Forces snapshot highlights moderate supplier power, high rivalry, capital-intensive entry barriers, shifting buyer dynamics, and a manageable threat of substitutes. This brief frames competitive tensions and strategic levers. The full report quantifies each force with visuals and business implications. Unlock the comprehensive analysis to inform smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical components

Core subsystems such as vacuum pumps, mass-flow controllers, RF power supplies and precision valves come from a small set of specialized vendors, concentrating supplier power and raising switching costs and delivery risk for AIXTRON. Vendors supplying unique specifications can negotiate stronger commercial and technical terms, and while dual-sourcing is sometimes used to mitigate risk, alternatives are not always technically equivalent or immediately qualified.

Specialty precursor and materials reliance

Metal-organic precursors (TMGa, TMAl), high-purity gases and specialty liners are sourced from a narrow global supplier pool subject to ISO/SEMI purity and safety certifications, constraining alternatives. In 2024 supply tightness linked to logistics and feedstock issues continued to cause tool-build and customer-acceptance delays of weeks to months. Long-term supply agreements reduce volatility but do not remove supplier leverage or single-source risks.

Precision machining and lead-time exposure

Custom chambers, showerheads and thermal components require tight tolerances and often face lead times exceeding 12 weeks, tying up AIXTRON’s production cycle. Capacity constraints at precision manufacturers in 2024 amplified cycle-time risk, enabling suppliers to leverage backlogs to negotiate higher prices. Early capacity reservations and long‑term purchase agreements reduce this vulnerability and stabilize input costs.

Geopolitics, export controls, and logistics

Controls on semiconductor equipment and materials (eg tighter US export rules through 2024) restrict cross-border sourcing and force licensing, concentrating approved suppliers—top 5 equipment vendors hold roughly 70% market share—boosting their leverage over AIXTRON. Freight and customs volatility (container rates swung >100% in 2020–22 and remained unstable into 2024) raises costs and delays. Regionalized supply chains in China, Taiwan, and the US increase local vendor bargaining power.

- Export controls concentrate approved suppliers → higher supplier leverage

- Top 5 vendors ≈70% market share → limited alternatives

- Freight/customs volatility (rates swung >100%) → higher cost/schedule risk

- Regionalized chains → greater local supplier bargaining power

Embedded software and electronics dependencies

Controllers, sensors and embedded software modules are often locked into proprietary ecosystems, and firmware compatibility plus safety and industry certifications commonly cause integration delays of 3–12 months. Obsolescence cycles frequently force product redesigns on supplier-driven timelines, and strategic partnerships to align roadmaps give key suppliers outsized influence over AIXTRON’s module choices and timing.

- Proprietary controllers limit replacement

- Firmware & certifications: 3–12 month delays

- Obsolescence forces supplier-timed redesigns

- Strategic partnerships increase supplier influence

Concentrated suppliers (Top-5 ≈70%) and >12-week lead times amplify delivery and cost risks

Specialized subsystems and materials concentrate supplier power (top 5 vendors ≈70% share), raising switching costs and delivery risk. Key inputs face lead times >12 weeks and 2–12+ week customer-acceptance delays in 2024. Export controls and >100% freight volatility since 2020 increase regional supplier leverage and pricing pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Top-5 vendor share | ≈70% | Limited alternatives |

| Lead times | >12 weeks | Production risk |

| Supply delays | 2–12+ weeks | Customer delays |

| Freight volatility | >100% swing (2020–22) | Cost/schedule |

What is included in the product

Concise Porter's Five Forces analysis for AIXTRON, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers protecting its semiconductor equipment niche.

A concise one-sheet Porter's Five Forces for AIXTRON that visualizes competitive pressure with a radar chart and customizable inputs—ideal for quick strategic decisions, slide-ready reports, and swapping in real-time data to relieve analysis bottlenecks.

Customers Bargaining Power

Customer concentration and scale

In 2024 major LED, power-electronics, RF and photonics producers accounted for the majority of AIXTRON’s order volumes, with top customers representing >50% of intake. Large IDMs and foundries can drive hard negotiations on price, customization and service terms. A few program wins or losses materially affect equipment utilization and revenue volatility. Volume bundling by buyers further increases their leverage.

High switching costs and qualifications

Epitaxy tools require lengthy process qualification and recipe transfer, commonly taking 6–18 months, which locks buyers in and raises effective switching costs. Once integrated, downtime and yield risks deter mid-cycle vendor changes, reducing price sensitivity. In 2024, buyers nonetheless leveraged new-node procurement windows to extract concessions and favorable service terms. This dynamic limits customer bargaining power except at node-transition points.

Cyclical and project-based demand

Capex for AIXTRON is tightly tied to end-market cycles (LED, GaN/SiC power, microLED, datacom), so in downcycles buyers commonly defer or cancel orders, intensifying price pressure and bargaining leverage. In upcycles, customers prioritize delivery speed and supplier installed base over discounts, shifting leverage back to suppliers. Framework agreements smooth ordering patterns but do not remove underlying cyclicality, leaving bargaining power highly seasonal.

Customization and performance metrics

Buyers require specific throughput, uniformity, uptime and cost-of-ownership guarantees, with acceptance tied to milestone-based testing that conditions AIXTRON cash flows; performance-linked warranties transfer operational and financial risk onto AIXTRON while successful field deployments can weaken buyer leverage on follow-on orders.

- Milestone-based acceptance limits cash flow flexibility

- Warranties shift risk to AIXTRON

- Strong field results reduce future buyer bargaining

Service, spares, and lifecycle leverage

Aftermarket contracts and spares pricing are key negotiation levers for buyers, with multi-year fleet deals commonly achieving 5–15% off list spares in practice. Large fleets standardize SLAs and push multi-year guarantees; uptime targets of 98–99.5% make renewals high-stakes. Proprietary parts temper buyer power but drew increased regulatory scrutiny on repair monopolies in 2024.

- spares discounts: 5–15%

- uptime targets: 98–99.5%

- trend: 2024 rise in repair/antitrust scrutiny

Foundries set terms; top customers >50%, 6-18m qual, uptime 98–99.5%

Large IDMs/foundries drive pricing and terms, with top customers >50% of orders in 2024. Long 6–18 month qualification and high downtime risk raise switching costs, except at node transitions where buyers extract concessions. Aftermarket leverage yields 5–15% spares discounts and 98–99.5% uptime SLAs; 2024 saw rising repair/antitrust scrutiny.

| Metric | 2024 Value |

|---|---|

| Top-customer share | >50% |

| Qualification time | 6–18 months |

| Spares discount | 5–15% |

| Uptime targets | 98–99.5% |

Same Document Delivered

AIXTRON Porter's Five Forces Analysis

This preview shows the actual AIXTRON Porter's Five Forces analysis you'll receive—no placeholders or excerpts. It is the complete, professionally formatted document ready for immediate download upon purchase. The file contains the full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. What you see is exactly what you'll get.

From Overview to Strategy Blueprint

AIXTRON’s Porter’s Five Forces snapshot highlights moderate supplier power, high rivalry, capital-intensive entry barriers, shifting buyer dynamics, and a manageable threat of substitutes. This brief frames competitive tensions and strategic levers. The full report quantifies each force with visuals and business implications. Unlock the comprehensive analysis to inform smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical components

Core subsystems such as vacuum pumps, mass-flow controllers, RF power supplies and precision valves come from a small set of specialized vendors, concentrating supplier power and raising switching costs and delivery risk for AIXTRON. Vendors supplying unique specifications can negotiate stronger commercial and technical terms, and while dual-sourcing is sometimes used to mitigate risk, alternatives are not always technically equivalent or immediately qualified.

Specialty precursor and materials reliance

Metal-organic precursors (TMGa, TMAl), high-purity gases and specialty liners are sourced from a narrow global supplier pool subject to ISO/SEMI purity and safety certifications, constraining alternatives. In 2024 supply tightness linked to logistics and feedstock issues continued to cause tool-build and customer-acceptance delays of weeks to months. Long-term supply agreements reduce volatility but do not remove supplier leverage or single-source risks.

Precision machining and lead-time exposure

Custom chambers, showerheads and thermal components require tight tolerances and often face lead times exceeding 12 weeks, tying up AIXTRON’s production cycle. Capacity constraints at precision manufacturers in 2024 amplified cycle-time risk, enabling suppliers to leverage backlogs to negotiate higher prices. Early capacity reservations and long‑term purchase agreements reduce this vulnerability and stabilize input costs.

Geopolitics, export controls, and logistics

Controls on semiconductor equipment and materials (eg tighter US export rules through 2024) restrict cross-border sourcing and force licensing, concentrating approved suppliers—top 5 equipment vendors hold roughly 70% market share—boosting their leverage over AIXTRON. Freight and customs volatility (container rates swung >100% in 2020–22 and remained unstable into 2024) raises costs and delays. Regionalized supply chains in China, Taiwan, and the US increase local vendor bargaining power.

- Export controls concentrate approved suppliers → higher supplier leverage

- Top 5 vendors ≈70% market share → limited alternatives

- Freight/customs volatility (rates swung >100%) → higher cost/schedule risk

- Regionalized chains → greater local supplier bargaining power

Embedded software and electronics dependencies

Controllers, sensors and embedded software modules are often locked into proprietary ecosystems, and firmware compatibility plus safety and industry certifications commonly cause integration delays of 3–12 months. Obsolescence cycles frequently force product redesigns on supplier-driven timelines, and strategic partnerships to align roadmaps give key suppliers outsized influence over AIXTRON’s module choices and timing.

- Proprietary controllers limit replacement

- Firmware & certifications: 3–12 month delays

- Obsolescence forces supplier-timed redesigns

- Strategic partnerships increase supplier influence

Concentrated suppliers (Top-5 ≈70%) and >12-week lead times amplify delivery and cost risks

Specialized subsystems and materials concentrate supplier power (top 5 vendors ≈70% share), raising switching costs and delivery risk. Key inputs face lead times >12 weeks and 2–12+ week customer-acceptance delays in 2024. Export controls and >100% freight volatility since 2020 increase regional supplier leverage and pricing pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Top-5 vendor share | ≈70% | Limited alternatives |

| Lead times | >12 weeks | Production risk |

| Supply delays | 2–12+ weeks | Customer delays |

| Freight volatility | >100% swing (2020–22) | Cost/schedule |

What is included in the product

Concise Porter's Five Forces analysis for AIXTRON, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers protecting its semiconductor equipment niche.

A concise one-sheet Porter's Five Forces for AIXTRON that visualizes competitive pressure with a radar chart and customizable inputs—ideal for quick strategic decisions, slide-ready reports, and swapping in real-time data to relieve analysis bottlenecks.

Customers Bargaining Power

Customer concentration and scale

In 2024 major LED, power-electronics, RF and photonics producers accounted for the majority of AIXTRON’s order volumes, with top customers representing >50% of intake. Large IDMs and foundries can drive hard negotiations on price, customization and service terms. A few program wins or losses materially affect equipment utilization and revenue volatility. Volume bundling by buyers further increases their leverage.

High switching costs and qualifications

Epitaxy tools require lengthy process qualification and recipe transfer, commonly taking 6–18 months, which locks buyers in and raises effective switching costs. Once integrated, downtime and yield risks deter mid-cycle vendor changes, reducing price sensitivity. In 2024, buyers nonetheless leveraged new-node procurement windows to extract concessions and favorable service terms. This dynamic limits customer bargaining power except at node-transition points.

Cyclical and project-based demand

Capex for AIXTRON is tightly tied to end-market cycles (LED, GaN/SiC power, microLED, datacom), so in downcycles buyers commonly defer or cancel orders, intensifying price pressure and bargaining leverage. In upcycles, customers prioritize delivery speed and supplier installed base over discounts, shifting leverage back to suppliers. Framework agreements smooth ordering patterns but do not remove underlying cyclicality, leaving bargaining power highly seasonal.

Customization and performance metrics

Buyers require specific throughput, uniformity, uptime and cost-of-ownership guarantees, with acceptance tied to milestone-based testing that conditions AIXTRON cash flows; performance-linked warranties transfer operational and financial risk onto AIXTRON while successful field deployments can weaken buyer leverage on follow-on orders.

- Milestone-based acceptance limits cash flow flexibility

- Warranties shift risk to AIXTRON

- Strong field results reduce future buyer bargaining

Service, spares, and lifecycle leverage

Aftermarket contracts and spares pricing are key negotiation levers for buyers, with multi-year fleet deals commonly achieving 5–15% off list spares in practice. Large fleets standardize SLAs and push multi-year guarantees; uptime targets of 98–99.5% make renewals high-stakes. Proprietary parts temper buyer power but drew increased regulatory scrutiny on repair monopolies in 2024.

- spares discounts: 5–15%

- uptime targets: 98–99.5%

- trend: 2024 rise in repair/antitrust scrutiny

Foundries set terms; top customers >50%, 6-18m qual, uptime 98–99.5%

Large IDMs/foundries drive pricing and terms, with top customers >50% of orders in 2024. Long 6–18 month qualification and high downtime risk raise switching costs, except at node transitions where buyers extract concessions. Aftermarket leverage yields 5–15% spares discounts and 98–99.5% uptime SLAs; 2024 saw rising repair/antitrust scrutiny.

| Metric | 2024 Value |

|---|---|

| Top-customer share | >50% |

| Qualification time | 6–18 months |

| Spares discount | 5–15% |

| Uptime targets | 98–99.5% |

Same Document Delivered

AIXTRON Porter's Five Forces Analysis

This preview shows the actual AIXTRON Porter's Five Forces analysis you'll receive—no placeholders or excerpts. It is the complete, professionally formatted document ready for immediate download upon purchase. The file contains the full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. What you see is exactly what you'll get.

Description

From Overview to Strategy Blueprint

AIXTRON’s Porter’s Five Forces snapshot highlights moderate supplier power, high rivalry, capital-intensive entry barriers, shifting buyer dynamics, and a manageable threat of substitutes. This brief frames competitive tensions and strategic levers. The full report quantifies each force with visuals and business implications. Unlock the comprehensive analysis to inform smarter investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical components

Core subsystems such as vacuum pumps, mass-flow controllers, RF power supplies and precision valves come from a small set of specialized vendors, concentrating supplier power and raising switching costs and delivery risk for AIXTRON. Vendors supplying unique specifications can negotiate stronger commercial and technical terms, and while dual-sourcing is sometimes used to mitigate risk, alternatives are not always technically equivalent or immediately qualified.

Specialty precursor and materials reliance

Metal-organic precursors (TMGa, TMAl), high-purity gases and specialty liners are sourced from a narrow global supplier pool subject to ISO/SEMI purity and safety certifications, constraining alternatives. In 2024 supply tightness linked to logistics and feedstock issues continued to cause tool-build and customer-acceptance delays of weeks to months. Long-term supply agreements reduce volatility but do not remove supplier leverage or single-source risks.

Precision machining and lead-time exposure

Custom chambers, showerheads and thermal components require tight tolerances and often face lead times exceeding 12 weeks, tying up AIXTRON’s production cycle. Capacity constraints at precision manufacturers in 2024 amplified cycle-time risk, enabling suppliers to leverage backlogs to negotiate higher prices. Early capacity reservations and long‑term purchase agreements reduce this vulnerability and stabilize input costs.

Geopolitics, export controls, and logistics

Controls on semiconductor equipment and materials (eg tighter US export rules through 2024) restrict cross-border sourcing and force licensing, concentrating approved suppliers—top 5 equipment vendors hold roughly 70% market share—boosting their leverage over AIXTRON. Freight and customs volatility (container rates swung >100% in 2020–22 and remained unstable into 2024) raises costs and delays. Regionalized supply chains in China, Taiwan, and the US increase local vendor bargaining power.

- Export controls concentrate approved suppliers → higher supplier leverage

- Top 5 vendors ≈70% market share → limited alternatives

- Freight/customs volatility (rates swung >100%) → higher cost/schedule risk

- Regionalized chains → greater local supplier bargaining power

Embedded software and electronics dependencies

Controllers, sensors and embedded software modules are often locked into proprietary ecosystems, and firmware compatibility plus safety and industry certifications commonly cause integration delays of 3–12 months. Obsolescence cycles frequently force product redesigns on supplier-driven timelines, and strategic partnerships to align roadmaps give key suppliers outsized influence over AIXTRON’s module choices and timing.

- Proprietary controllers limit replacement

- Firmware & certifications: 3–12 month delays

- Obsolescence forces supplier-timed redesigns

- Strategic partnerships increase supplier influence

Concentrated suppliers (Top-5 ≈70%) and >12-week lead times amplify delivery and cost risks

Specialized subsystems and materials concentrate supplier power (top 5 vendors ≈70% share), raising switching costs and delivery risk. Key inputs face lead times >12 weeks and 2–12+ week customer-acceptance delays in 2024. Export controls and >100% freight volatility since 2020 increase regional supplier leverage and pricing pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Top-5 vendor share | ≈70% | Limited alternatives |

| Lead times | >12 weeks | Production risk |

| Supply delays | 2–12+ weeks | Customer delays |

| Freight volatility | >100% swing (2020–22) | Cost/schedule |

What is included in the product

Concise Porter's Five Forces analysis for AIXTRON, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic barriers protecting its semiconductor equipment niche.

A concise one-sheet Porter's Five Forces for AIXTRON that visualizes competitive pressure with a radar chart and customizable inputs—ideal for quick strategic decisions, slide-ready reports, and swapping in real-time data to relieve analysis bottlenecks.

Customers Bargaining Power

Customer concentration and scale

In 2024 major LED, power-electronics, RF and photonics producers accounted for the majority of AIXTRON’s order volumes, with top customers representing >50% of intake. Large IDMs and foundries can drive hard negotiations on price, customization and service terms. A few program wins or losses materially affect equipment utilization and revenue volatility. Volume bundling by buyers further increases their leverage.

High switching costs and qualifications

Epitaxy tools require lengthy process qualification and recipe transfer, commonly taking 6–18 months, which locks buyers in and raises effective switching costs. Once integrated, downtime and yield risks deter mid-cycle vendor changes, reducing price sensitivity. In 2024, buyers nonetheless leveraged new-node procurement windows to extract concessions and favorable service terms. This dynamic limits customer bargaining power except at node-transition points.

Cyclical and project-based demand

Capex for AIXTRON is tightly tied to end-market cycles (LED, GaN/SiC power, microLED, datacom), so in downcycles buyers commonly defer or cancel orders, intensifying price pressure and bargaining leverage. In upcycles, customers prioritize delivery speed and supplier installed base over discounts, shifting leverage back to suppliers. Framework agreements smooth ordering patterns but do not remove underlying cyclicality, leaving bargaining power highly seasonal.

Customization and performance metrics

Buyers require specific throughput, uniformity, uptime and cost-of-ownership guarantees, with acceptance tied to milestone-based testing that conditions AIXTRON cash flows; performance-linked warranties transfer operational and financial risk onto AIXTRON while successful field deployments can weaken buyer leverage on follow-on orders.

- Milestone-based acceptance limits cash flow flexibility

- Warranties shift risk to AIXTRON

- Strong field results reduce future buyer bargaining

Service, spares, and lifecycle leverage

Aftermarket contracts and spares pricing are key negotiation levers for buyers, with multi-year fleet deals commonly achieving 5–15% off list spares in practice. Large fleets standardize SLAs and push multi-year guarantees; uptime targets of 98–99.5% make renewals high-stakes. Proprietary parts temper buyer power but drew increased regulatory scrutiny on repair monopolies in 2024.

- spares discounts: 5–15%

- uptime targets: 98–99.5%

- trend: 2024 rise in repair/antitrust scrutiny

Foundries set terms; top customers >50%, 6-18m qual, uptime 98–99.5%

Large IDMs/foundries drive pricing and terms, with top customers >50% of orders in 2024. Long 6–18 month qualification and high downtime risk raise switching costs, except at node transitions where buyers extract concessions. Aftermarket leverage yields 5–15% spares discounts and 98–99.5% uptime SLAs; 2024 saw rising repair/antitrust scrutiny.

| Metric | 2024 Value |

|---|---|

| Top-customer share | >50% |

| Qualification time | 6–18 months |

| Spares discount | 5–15% |

| Uptime targets | 98–99.5% |

Same Document Delivered

AIXTRON Porter's Five Forces Analysis

This preview shows the actual AIXTRON Porter's Five Forces analysis you'll receive—no placeholders or excerpts. It is the complete, professionally formatted document ready for immediate download upon purchase. The file contains the full assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. What you see is exactly what you'll get.