AKWEL Porter's Five Forces Analysis

Don't Miss the Bigger Picture

AKWEL’s Porter's Five Forces snapshot highlights supplier leverage, buyer concentration, competitive rivalry, barriers to entry, and substitute risks shaping its automotive components business. You’ll see where margins and strategic moves are most vulnerable and where growth can be defended. This brief teases actionable findings—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and tailored recommendations to inform investment or strategy.

Suppliers Bargaining Power

Specialized materials

AKWEL relies on engineered polymers, elastomers and precision metals sourced from few qualified suppliers, concentrating leverage in supply chains; AKWEL reported 2024 sales of about €1.6bn, amplifying exposure to input cost swings. Specialty resins and fluoropolymers remained price-volatile and capacity-constrained through 2024, while mechatronic modules add dependency on chips and sensors, increasing supplier bargaining power during tight cycles.

Tooling and equipment

Custom molds, extrusion lines and robotic cells for AKWEL typically face long lead times—custom molds 12–26 weeks and robotic cells 16–40 weeks—sourcing from niche vendors, which raises supplier leverage. Mid-program toolmaker switches often add months and can incur tens–hundreds of thousands of euros in requalification and warranty risk. Limited alternative vendors concentrate bargaining power; preventive maintenance and dual-tooling reduce but do not remove this exposure.

Energy and logistics

Polymer processing and metal forming in AKWEL are highly energy intensive; Eurostat reports EU industrial electricity averaged about €0.16/kWh in 2024, making margins sensitive to power-price swings.

Freight constraints and regionalization allow suppliers to pass through surcharges—container rates and BAF spikes in 2024 kept logistics costs elevated, boosting landed-cost volatility despite indexation clauses that typically cover only part of inputs.

Nearshoring trims transit exposure and average lead times, but cannot fully eliminate supplier leverage over energy- and transport-sensitive inputs, preserving residual pass-through risk.

Qualification barriers

OEs demand PPAP/IATF-qualified inputs, sharply narrowing approved supplier lists and elevating supplier leverage during launches; requalification commonly takes 3–6 months and can jeopardize SOP timelines. Approved vendors gain negotiating room in critical phases, extracting price or lead-time concessions. AKWEL’s multi-sourcing policy mitigates risk but is constrained by validation lead times.

- PPAP/IATF: narrows pool

- Requalification: 3–6 months

- Approved vendors: higher bargaining power

- AKWEL multi-sourcing: helpful but validation-limited

Volume counterweight

High, predictable call-offs give AKWEL negotiating scale—the group reported €1.57 billion revenue in 2024—while long-term contracts and resin hedges partially stabilize input costs; supplier performance scorecards enforce delivery and quality standards, yet episodic resin or component scarcity still shifts bargaining power back to upstream suppliers.

- Predictable call-offs: leverage

- Long-term contracts/resin hedges: price stability

- Supplier scorecards: accountability

- Scarcity periods: upstream power

Concentrated suppliers, long lead times and €1.57-1.6bn sales lift upstream bargaining power

AKWEL faces elevated supplier bargaining power due to concentrated sources for polymers, chips and custom tooling amid 2024 sales of €1.57–1.6bn; resin and chip shortages shifted leverage upstream. Long lead times (molds 12–26w, robotic cells 16–40w) and 3–6m requalification windows boost supplier negotiating room. Energy (€0.16/kWh EU avg 2024) and 2024 freight/BAF spikes further increase pass-through risk.

| Factor | Impact | 2024 data |

|---|---|---|

| Sales scale | Buyer leverage | €1.57–1.6bn |

| Lead times | Supplier power | Molds 12–26w; Robotic 16–40w |

| Energy/logistics | Cost pass-through | €0.16/kWh; freight/BAF spikes |

What is included in the product

Tailored Porter's Five Forces analysis for AKWEL that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic insights for investor and strategic use.

Clear one-sheet summary of AKWEL's five competitive forces—ideal for rapid supplier and OEM decision-making; editable pressure sliders and a radar chart let you model regulation, electrification, or supplier shifts instantly without complex tools.

Customers Bargaining Power

OEM consolidation

Global automakers and mega-Tier-1s concentrate purchasing—top 10 OEMs account for roughly 50% of global vehicle output (≈40–45M units in 2024) while leading Tier-1s hold ~40% of supplier sales, enabling aggressive RFQs. Their scale forces 2–4% annual price/productivity givebacks and frequent share shifts between qualified suppliers to extract concessions. This concentration heightens buyer power over AKWEL.

High switching costs

Once a line is validated, tooling and PPAP create lock‑in—tooling often exceeds €1m per line—so suppliers gain stickiness; AKWEL reported revenue of €1.36bn in 2023, underlining scale in secured programs. OEMs nonetheless dual‑source many critical parts to retain leverage, reallocating future platforms rather than switching mid‑cycle. The risk of losing the next platform keeps pricing pressure high.

Quality and penalty regimes

Strict PPM targets, commonly set below 1,000 ppm by OEMs, plus warranty and delivery KPIs create explicit chargeback mechanisms for defects or delays; suppliers can face chargebacks that materially hit margins. Just-in-time mandates transfer inventory risk to suppliers, shrinking buyers’ need to pay for stock and increasing bargaining leverage. These contractual terms shift value toward buyers beyond price alone, so disciplined performance management is essential to protect margins.

Design influence

OEM engineering choices set material specs, tolerances and integration levels, forcing AKWEL to meet precise standards; AKWEL reported around €1.1bn revenue in 2023, underscoring scale but limited pricing power. Standardized interfaces lower differentiation and enable competitive bidding, while co-development secures business but compresses margins. Buyers drive make-versus-buy for thermal modules, shaping AKWELs strategic choices and bargaining leverage.

- OEM specs → tight margins

- Standard interfaces → easier bidding

- Co-development → lock-in, lower margins

- Buyers dictate make-vs-buy on thermal systems

EV program cadence

Rapid EV platform launches drive frequent RFQs and redesigns, giving fleet and OEM buyers recurring leverage to renegotiate terms and demand cost and weight cuts; global electric car sales reached about 14.6 million in 2023 (IEA), intensifying supplier churn. Volume ramp uncertainty and forecast variability (often reported as large swing ranges by OEMs) increase price pressure and push liability-sharing clauses into contracts.

- Frequent RFQs → stronger buyer leverage

- Cost/weight reduction demands ↑

- Volume ramp uncertainty → price & liability pressure

- Forecast variability strengthens buyer negotiation power

OEMs concentrate ~50%: tooling stickiness and EV ramp squeeze suppliers

Buyer concentration is high: top 10 OEMs account for ~50% of vehicle output (~40–45M units in 2024), giving strong price leverage over AKWEL.

Tooling and PPAP create stickiness (tooling >€1m/line) but OEMs dual‑source and reallocate platforms, keeping pricing pressure.

Strict PPM targets (<1,000 ppm), JIT and chargebacks shift risk to suppliers and compress margins.

EV ramping (14.6M EVs sold in 2023) fuels frequent RFQs and recurrent cost-down demands.

| Metric | Value |

|---|---|

| Top10 OEM share | ~50% (~40–45M units, 2024) |

| AKWEL revenue | €1.36bn (2023) |

| EV sales | 14.6M (2023) |

| Tooling cost | >€1m/line |

| OEM PPM targets | <1,000 ppm |

Preview Before You Purchase

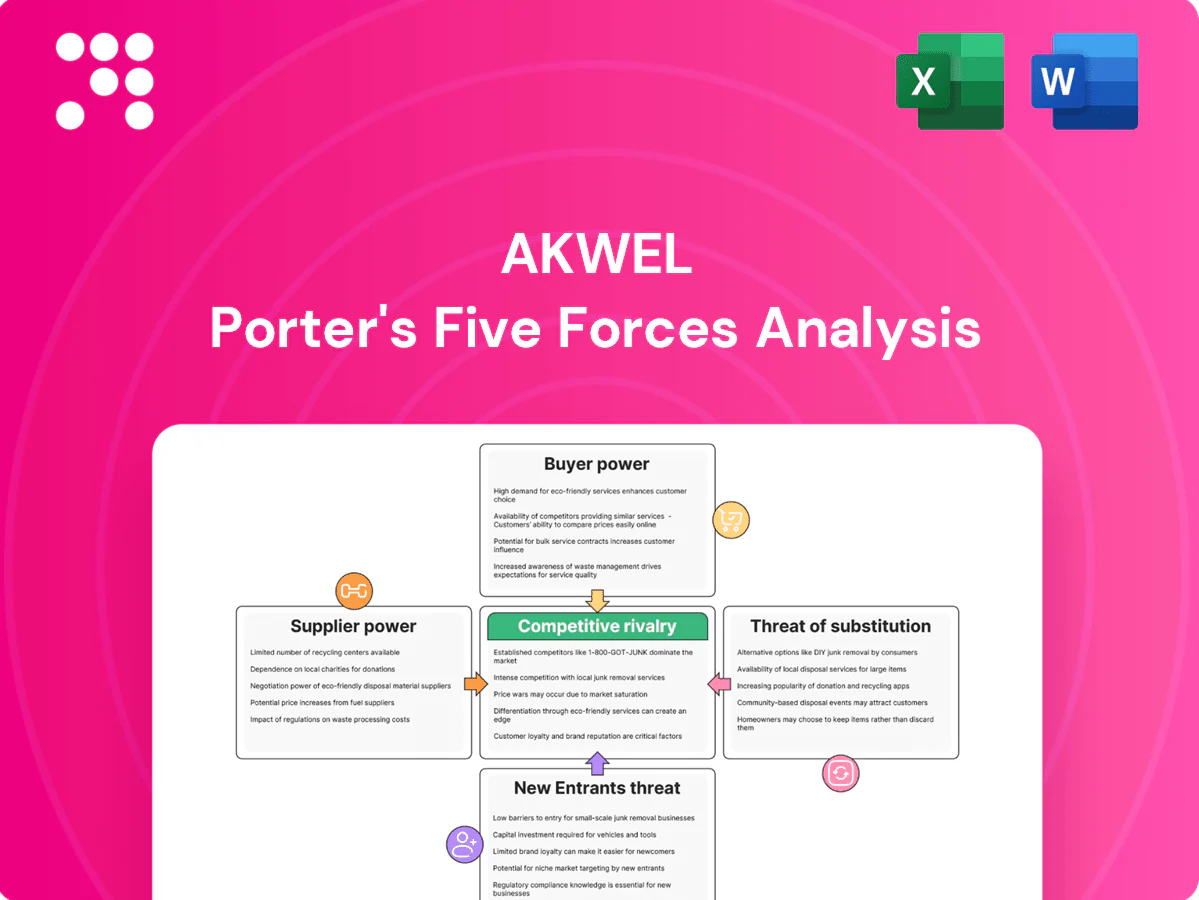

AKWEL Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of AKWEL you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry structure. It's professionally formatted and ready for download and use the moment you buy.

Don't Miss the Bigger Picture

AKWEL’s Porter's Five Forces snapshot highlights supplier leverage, buyer concentration, competitive rivalry, barriers to entry, and substitute risks shaping its automotive components business. You’ll see where margins and strategic moves are most vulnerable and where growth can be defended. This brief teases actionable findings—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and tailored recommendations to inform investment or strategy.

Suppliers Bargaining Power

Specialized materials

AKWEL relies on engineered polymers, elastomers and precision metals sourced from few qualified suppliers, concentrating leverage in supply chains; AKWEL reported 2024 sales of about €1.6bn, amplifying exposure to input cost swings. Specialty resins and fluoropolymers remained price-volatile and capacity-constrained through 2024, while mechatronic modules add dependency on chips and sensors, increasing supplier bargaining power during tight cycles.

Tooling and equipment

Custom molds, extrusion lines and robotic cells for AKWEL typically face long lead times—custom molds 12–26 weeks and robotic cells 16–40 weeks—sourcing from niche vendors, which raises supplier leverage. Mid-program toolmaker switches often add months and can incur tens–hundreds of thousands of euros in requalification and warranty risk. Limited alternative vendors concentrate bargaining power; preventive maintenance and dual-tooling reduce but do not remove this exposure.

Energy and logistics

Polymer processing and metal forming in AKWEL are highly energy intensive; Eurostat reports EU industrial electricity averaged about €0.16/kWh in 2024, making margins sensitive to power-price swings.

Freight constraints and regionalization allow suppliers to pass through surcharges—container rates and BAF spikes in 2024 kept logistics costs elevated, boosting landed-cost volatility despite indexation clauses that typically cover only part of inputs.

Nearshoring trims transit exposure and average lead times, but cannot fully eliminate supplier leverage over energy- and transport-sensitive inputs, preserving residual pass-through risk.

Qualification barriers

OEs demand PPAP/IATF-qualified inputs, sharply narrowing approved supplier lists and elevating supplier leverage during launches; requalification commonly takes 3–6 months and can jeopardize SOP timelines. Approved vendors gain negotiating room in critical phases, extracting price or lead-time concessions. AKWEL’s multi-sourcing policy mitigates risk but is constrained by validation lead times.

- PPAP/IATF: narrows pool

- Requalification: 3–6 months

- Approved vendors: higher bargaining power

- AKWEL multi-sourcing: helpful but validation-limited

Volume counterweight

High, predictable call-offs give AKWEL negotiating scale—the group reported €1.57 billion revenue in 2024—while long-term contracts and resin hedges partially stabilize input costs; supplier performance scorecards enforce delivery and quality standards, yet episodic resin or component scarcity still shifts bargaining power back to upstream suppliers.

- Predictable call-offs: leverage

- Long-term contracts/resin hedges: price stability

- Supplier scorecards: accountability

- Scarcity periods: upstream power

Concentrated suppliers, long lead times and €1.57-1.6bn sales lift upstream bargaining power

AKWEL faces elevated supplier bargaining power due to concentrated sources for polymers, chips and custom tooling amid 2024 sales of €1.57–1.6bn; resin and chip shortages shifted leverage upstream. Long lead times (molds 12–26w, robotic cells 16–40w) and 3–6m requalification windows boost supplier negotiating room. Energy (€0.16/kWh EU avg 2024) and 2024 freight/BAF spikes further increase pass-through risk.

| Factor | Impact | 2024 data |

|---|---|---|

| Sales scale | Buyer leverage | €1.57–1.6bn |

| Lead times | Supplier power | Molds 12–26w; Robotic 16–40w |

| Energy/logistics | Cost pass-through | €0.16/kWh; freight/BAF spikes |

What is included in the product

Tailored Porter's Five Forces analysis for AKWEL that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic insights for investor and strategic use.

Clear one-sheet summary of AKWEL's five competitive forces—ideal for rapid supplier and OEM decision-making; editable pressure sliders and a radar chart let you model regulation, electrification, or supplier shifts instantly without complex tools.

Customers Bargaining Power

OEM consolidation

Global automakers and mega-Tier-1s concentrate purchasing—top 10 OEMs account for roughly 50% of global vehicle output (≈40–45M units in 2024) while leading Tier-1s hold ~40% of supplier sales, enabling aggressive RFQs. Their scale forces 2–4% annual price/productivity givebacks and frequent share shifts between qualified suppliers to extract concessions. This concentration heightens buyer power over AKWEL.

High switching costs

Once a line is validated, tooling and PPAP create lock‑in—tooling often exceeds €1m per line—so suppliers gain stickiness; AKWEL reported revenue of €1.36bn in 2023, underlining scale in secured programs. OEMs nonetheless dual‑source many critical parts to retain leverage, reallocating future platforms rather than switching mid‑cycle. The risk of losing the next platform keeps pricing pressure high.

Quality and penalty regimes

Strict PPM targets, commonly set below 1,000 ppm by OEMs, plus warranty and delivery KPIs create explicit chargeback mechanisms for defects or delays; suppliers can face chargebacks that materially hit margins. Just-in-time mandates transfer inventory risk to suppliers, shrinking buyers’ need to pay for stock and increasing bargaining leverage. These contractual terms shift value toward buyers beyond price alone, so disciplined performance management is essential to protect margins.

Design influence

OEM engineering choices set material specs, tolerances and integration levels, forcing AKWEL to meet precise standards; AKWEL reported around €1.1bn revenue in 2023, underscoring scale but limited pricing power. Standardized interfaces lower differentiation and enable competitive bidding, while co-development secures business but compresses margins. Buyers drive make-versus-buy for thermal modules, shaping AKWELs strategic choices and bargaining leverage.

- OEM specs → tight margins

- Standard interfaces → easier bidding

- Co-development → lock-in, lower margins

- Buyers dictate make-vs-buy on thermal systems

EV program cadence

Rapid EV platform launches drive frequent RFQs and redesigns, giving fleet and OEM buyers recurring leverage to renegotiate terms and demand cost and weight cuts; global electric car sales reached about 14.6 million in 2023 (IEA), intensifying supplier churn. Volume ramp uncertainty and forecast variability (often reported as large swing ranges by OEMs) increase price pressure and push liability-sharing clauses into contracts.

- Frequent RFQs → stronger buyer leverage

- Cost/weight reduction demands ↑

- Volume ramp uncertainty → price & liability pressure

- Forecast variability strengthens buyer negotiation power

OEMs concentrate ~50%: tooling stickiness and EV ramp squeeze suppliers

Buyer concentration is high: top 10 OEMs account for ~50% of vehicle output (~40–45M units in 2024), giving strong price leverage over AKWEL.

Tooling and PPAP create stickiness (tooling >€1m/line) but OEMs dual‑source and reallocate platforms, keeping pricing pressure.

Strict PPM targets (<1,000 ppm), JIT and chargebacks shift risk to suppliers and compress margins.

EV ramping (14.6M EVs sold in 2023) fuels frequent RFQs and recurrent cost-down demands.

| Metric | Value |

|---|---|

| Top10 OEM share | ~50% (~40–45M units, 2024) |

| AKWEL revenue | €1.36bn (2023) |

| EV sales | 14.6M (2023) |

| Tooling cost | >€1m/line |

| OEM PPM targets | <1,000 ppm |

Preview Before You Purchase

AKWEL Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of AKWEL you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry structure. It's professionally formatted and ready for download and use the moment you buy.

Description

Don't Miss the Bigger Picture

AKWEL’s Porter's Five Forces snapshot highlights supplier leverage, buyer concentration, competitive rivalry, barriers to entry, and substitute risks shaping its automotive components business. You’ll see where margins and strategic moves are most vulnerable and where growth can be defended. This brief teases actionable findings—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and tailored recommendations to inform investment or strategy.

Suppliers Bargaining Power

Specialized materials

AKWEL relies on engineered polymers, elastomers and precision metals sourced from few qualified suppliers, concentrating leverage in supply chains; AKWEL reported 2024 sales of about €1.6bn, amplifying exposure to input cost swings. Specialty resins and fluoropolymers remained price-volatile and capacity-constrained through 2024, while mechatronic modules add dependency on chips and sensors, increasing supplier bargaining power during tight cycles.

Tooling and equipment

Custom molds, extrusion lines and robotic cells for AKWEL typically face long lead times—custom molds 12–26 weeks and robotic cells 16–40 weeks—sourcing from niche vendors, which raises supplier leverage. Mid-program toolmaker switches often add months and can incur tens–hundreds of thousands of euros in requalification and warranty risk. Limited alternative vendors concentrate bargaining power; preventive maintenance and dual-tooling reduce but do not remove this exposure.

Energy and logistics

Polymer processing and metal forming in AKWEL are highly energy intensive; Eurostat reports EU industrial electricity averaged about €0.16/kWh in 2024, making margins sensitive to power-price swings.

Freight constraints and regionalization allow suppliers to pass through surcharges—container rates and BAF spikes in 2024 kept logistics costs elevated, boosting landed-cost volatility despite indexation clauses that typically cover only part of inputs.

Nearshoring trims transit exposure and average lead times, but cannot fully eliminate supplier leverage over energy- and transport-sensitive inputs, preserving residual pass-through risk.

Qualification barriers

OEs demand PPAP/IATF-qualified inputs, sharply narrowing approved supplier lists and elevating supplier leverage during launches; requalification commonly takes 3–6 months and can jeopardize SOP timelines. Approved vendors gain negotiating room in critical phases, extracting price or lead-time concessions. AKWEL’s multi-sourcing policy mitigates risk but is constrained by validation lead times.

- PPAP/IATF: narrows pool

- Requalification: 3–6 months

- Approved vendors: higher bargaining power

- AKWEL multi-sourcing: helpful but validation-limited

Volume counterweight

High, predictable call-offs give AKWEL negotiating scale—the group reported €1.57 billion revenue in 2024—while long-term contracts and resin hedges partially stabilize input costs; supplier performance scorecards enforce delivery and quality standards, yet episodic resin or component scarcity still shifts bargaining power back to upstream suppliers.

- Predictable call-offs: leverage

- Long-term contracts/resin hedges: price stability

- Supplier scorecards: accountability

- Scarcity periods: upstream power

Concentrated suppliers, long lead times and €1.57-1.6bn sales lift upstream bargaining power

AKWEL faces elevated supplier bargaining power due to concentrated sources for polymers, chips and custom tooling amid 2024 sales of €1.57–1.6bn; resin and chip shortages shifted leverage upstream. Long lead times (molds 12–26w, robotic cells 16–40w) and 3–6m requalification windows boost supplier negotiating room. Energy (€0.16/kWh EU avg 2024) and 2024 freight/BAF spikes further increase pass-through risk.

| Factor | Impact | 2024 data |

|---|---|---|

| Sales scale | Buyer leverage | €1.57–1.6bn |

| Lead times | Supplier power | Molds 12–26w; Robotic 16–40w |

| Energy/logistics | Cost pass-through | €0.16/kWh; freight/BAF spikes |

What is included in the product

Tailored Porter's Five Forces analysis for AKWEL that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic insights for investor and strategic use.

Clear one-sheet summary of AKWEL's five competitive forces—ideal for rapid supplier and OEM decision-making; editable pressure sliders and a radar chart let you model regulation, electrification, or supplier shifts instantly without complex tools.

Customers Bargaining Power

OEM consolidation

Global automakers and mega-Tier-1s concentrate purchasing—top 10 OEMs account for roughly 50% of global vehicle output (≈40–45M units in 2024) while leading Tier-1s hold ~40% of supplier sales, enabling aggressive RFQs. Their scale forces 2–4% annual price/productivity givebacks and frequent share shifts between qualified suppliers to extract concessions. This concentration heightens buyer power over AKWEL.

High switching costs

Once a line is validated, tooling and PPAP create lock‑in—tooling often exceeds €1m per line—so suppliers gain stickiness; AKWEL reported revenue of €1.36bn in 2023, underlining scale in secured programs. OEMs nonetheless dual‑source many critical parts to retain leverage, reallocating future platforms rather than switching mid‑cycle. The risk of losing the next platform keeps pricing pressure high.

Quality and penalty regimes

Strict PPM targets, commonly set below 1,000 ppm by OEMs, plus warranty and delivery KPIs create explicit chargeback mechanisms for defects or delays; suppliers can face chargebacks that materially hit margins. Just-in-time mandates transfer inventory risk to suppliers, shrinking buyers’ need to pay for stock and increasing bargaining leverage. These contractual terms shift value toward buyers beyond price alone, so disciplined performance management is essential to protect margins.

Design influence

OEM engineering choices set material specs, tolerances and integration levels, forcing AKWEL to meet precise standards; AKWEL reported around €1.1bn revenue in 2023, underscoring scale but limited pricing power. Standardized interfaces lower differentiation and enable competitive bidding, while co-development secures business but compresses margins. Buyers drive make-versus-buy for thermal modules, shaping AKWELs strategic choices and bargaining leverage.

- OEM specs → tight margins

- Standard interfaces → easier bidding

- Co-development → lock-in, lower margins

- Buyers dictate make-vs-buy on thermal systems

EV program cadence

Rapid EV platform launches drive frequent RFQs and redesigns, giving fleet and OEM buyers recurring leverage to renegotiate terms and demand cost and weight cuts; global electric car sales reached about 14.6 million in 2023 (IEA), intensifying supplier churn. Volume ramp uncertainty and forecast variability (often reported as large swing ranges by OEMs) increase price pressure and push liability-sharing clauses into contracts.

- Frequent RFQs → stronger buyer leverage

- Cost/weight reduction demands ↑

- Volume ramp uncertainty → price & liability pressure

- Forecast variability strengthens buyer negotiation power

OEMs concentrate ~50%: tooling stickiness and EV ramp squeeze suppliers

Buyer concentration is high: top 10 OEMs account for ~50% of vehicle output (~40–45M units in 2024), giving strong price leverage over AKWEL.

Tooling and PPAP create stickiness (tooling >€1m/line) but OEMs dual‑source and reallocate platforms, keeping pricing pressure.

Strict PPM targets (<1,000 ppm), JIT and chargebacks shift risk to suppliers and compress margins.

EV ramping (14.6M EVs sold in 2023) fuels frequent RFQs and recurrent cost-down demands.

| Metric | Value |

|---|---|

| Top10 OEM share | ~50% (~40–45M units, 2024) |

| AKWEL revenue | €1.36bn (2023) |

| EV sales | 14.6M (2023) |

| Tooling cost | >€1m/line |

| OEM PPM targets | <1,000 ppm |

Preview Before You Purchase

AKWEL Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of AKWEL you'll receive immediately after purchase—no surprises, no placeholders. The document provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry structure. It's professionally formatted and ready for download and use the moment you buy.