AKWEL PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE analysis of AKWEL. Explore political, economic, social, technological, legal and environmental forces shaping its strategy and risk profile. Ideal for investors and strategists. Purchase the full, editable report to access deep-dive insights and download instantly.

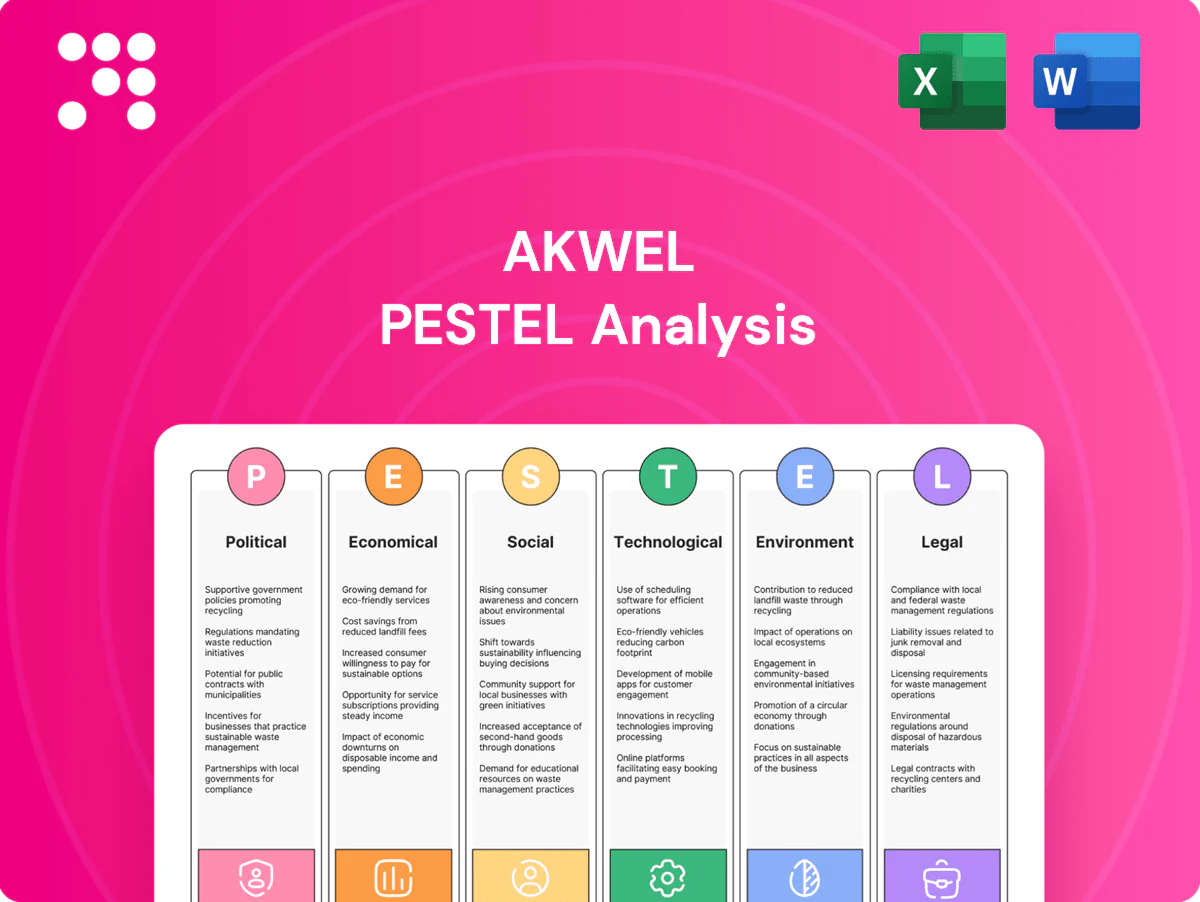

Political factors

EV industrial policy and subsidies

Government incentives shape OEM electrification roadmaps and steer demand to EV-specific thermal and fluid systems: the US IRA mobilized roughly $369bn in clean-energy support and a $7,500 EV tax credit, the EU enforces a 2035 new-ICE sales phase-out, while China remains the largest NEV market—these shifts can speed or delay AKWEL’s EV capex and capacity plans, so monitoring policy stability across EU/US/China and active industry-body engagement is essential.

Trade policy, tariffs, and localization

Tariffs such as US steel at 25% and aluminum at 10% and raw‑material duties shape AKWELs plant network and sourcing choices. Localization rules — US EV final assembly for tax credits, India PLI for auto components (₹25,938 crore/≈$3.1bn) and rising European localization pressures — push regional production and supplier development. Geopolitical frictions raise cross‑border disruption risk and buffer inventory needs; AKWEL must balance cost, resilience and compliance in its footprint strategy.

Public procurement and strategic autonomy

National agendas such as the EU Critical Raw Materials Act (adopted June 2023) boost preference for local suppliers in strategic tech, benefiting suppliers of EV thermal management tied to battery security. Thermal solutions can qualify for IPCEI-style support (battery IPCEI public backing ~€3.2bn) or grants often ranging €10–100m. Enhanced FDI screening in ~24 EU/partner jurisdictions (2024) can slow M&A approvals, so active dialogue with authorities has unlocked cooperative R&D and funding.

Labor policy and social dialogue

Changes in wage frameworks (eg IG Metall 2023 deal ~8%) and working-time rules reshape plant competitiveness and cost base; incentives for vocational training help close mechatronics/automation gaps while strikes in automotive hubs can delay OEM deliveries; proactive workforce planning across AKWELs c.50 plants preserves service levels and reduces volatility.

- Wage shock: IG Metall 2023 ~8%

- Skills focus: vocational incentives for mechatronics

- Risk: strikes disrupt OEM supply

- Mitigation: proactive workforce planning

Infrastructure and energy policy

Energy transition policies shift electricity mix and prices, affecting AKWEL plants' access to low‑carbon power; EU industrial electricity averaged about €0.10/kWh in 2024 while France's nuclear fleet supplies ~70% of national generation, insulating some sites. Grid reliability and industrial tariffs materially affect cost per part for polymer processing; gas TTF fell ~60% from 2022 to 2024. Policies for hydrogen (EU 10 Mt by 2030) and advanced cooling can open new applications; site selection should weigh energy‑mix trajectories and incentives.

- Energy price: EU industrial ~€0.10/kWh (2024)

- France nuclear ~70% (2024)

- Gas TTF -60% vs 2022

- EU hydrogen target: 10 Mt by 2030

Policy shifts, tariffs and incentives reshape automotive supplier footprints in US, EU and China

Policy shifts (US IRA $369bn, $7,500 EV credit; EU 2035 ICE phase‑out; China NEV leadership) reshape AKWEL demand, tariffs (US steel 25%/aluminium 10%) and localization rules force regional footprint choices, while EU CRM Act, IPCEI ~€3.2bn and energy mix (€0.10/kWh EU 2024) create funding and site selection advantages; labor deals (IG Metall ~8% 2023) affect costs.

| Metric | Value |

|---|---|

| US IRA | $369bn |

| EV credit | $7,500 |

| US steel tariff | 25% |

| EU industrial power | €0.10/kWh (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect AKWEL across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section uses current data and trends, offers forward-looking insights and detailed sub-points to help executives, investors and entrepreneurs identify threats, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for AKWEL that teams can drop into presentations, annotate for regional specifics, and share for quick alignment—streamlining external risk discussions and speeding strategic decision-making.

Economic factors

Auto demand cycles and platform mix

Global light-vehicle sales (about 70–80 million units annually) drive AKWEL volumes, while EV penetration around 15% of new-car sales in 2024 reduces thermal-system content per vehicle. OEM platform consolidation concentrates award risk but offers scale on won programs. Tight forecast accuracy is vital to avoid overcapacity or missed demand. AKWEL’s diversified program mix across powertrains buffers cyclicality.

Raw material and logistics costs

Polymer resins, elastomers and metals show high price volatility linked to oil and gas swings (Brent averaged about $83/bbl in 2024) and tight supply-demand cycles, pushing resin spot moves into double digits. Freight and container rates — roughly $1,500 per FEU on average in 2024 for key East–West lanes — raise global and plant-to-plant transfer costs. OEM indexation clauses often lag 1–3 months, squeezing margins during spikes, so strategic hedging and dual-sourcing are used to stabilize input costs.

FX exposure and geographic mix

Multicurrency revenues and costs expose AKWEL to translation and transaction risk across EUR, USD, CNY and emerging-market currencies, which can compress margins and shift pricing power between OEMs and suppliers. Local-for-local production in Europe, China and North America provides natural hedges that reduce forex volatility on operating profits. Treasury policy must coordinate netting, forwards and invoicing currency with OEM contract clauses and indexation mechanisms to protect margins.

Interest rates and capex affordability

Higher policy rates (Fed funds ~5.25–5.50% and ECB depo ~4.0% in mid‑2025) raise financing costs for tooling, automation and plant upgrades, tightening payback thresholds for new EV‑focused lines; global EV sales were ~14% of new car sales in 2024, concentrating investment pressure on high‑visibility platforms. OEM payment terms and longer working capital cycles amplify financing strain, so AKWEL prioritizes platforms with durable volume visibility to protect returns.

- Rates: Fed 5.25–5.50% / ECB ~4.0%

- EV share 2024: ~14% of new sales

- Result: stricter payback, higher capex hurdle

- Mitigation: focus on platforms with stable volume

OEM pricing pressure and consolidation

Automakers push 2-4% annual cost-downs and productivity gains, compressing supplier margins into mid-single digits and intensifying Tier-1 competition and vertical integration risks to content share; differentiation via performance, weight and sustainability KPIs (CO2, recyclability) supports pricing resilience and design-in leverage; long-term agreements (typically 3-7 years) secure revenue visibility.

Policy shifts, tariffs and incentives reshape automotive supplier footprints in US, EU and China

Global light-vehicle volumes (~70–80m units) and EV mix (~14–15% new sales in 2024) reduce thermal-system content but concentrate awarded programs. Input volatility (Brent ~$83/bbl in 2024; freight ~ $1,500/FEU) and OEM 1–3-month indexation squeeze margins, prompting hedging and dual‑sourcing. Higher rates (Fed 5.25–5.50% / ECB ~4.0% mid‑2025) raise capex payback hurdles; OEM cost‑down targets 2–4% p.a. compress supplier margins to mid‑single digits.

Full Version Awaits

AKWEL PESTLE Analysis

The AKWEL PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the real, final product.

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE analysis of AKWEL. Explore political, economic, social, technological, legal and environmental forces shaping its strategy and risk profile. Ideal for investors and strategists. Purchase the full, editable report to access deep-dive insights and download instantly.

Political factors

EV industrial policy and subsidies

Government incentives shape OEM electrification roadmaps and steer demand to EV-specific thermal and fluid systems: the US IRA mobilized roughly $369bn in clean-energy support and a $7,500 EV tax credit, the EU enforces a 2035 new-ICE sales phase-out, while China remains the largest NEV market—these shifts can speed or delay AKWEL’s EV capex and capacity plans, so monitoring policy stability across EU/US/China and active industry-body engagement is essential.

Trade policy, tariffs, and localization

Tariffs such as US steel at 25% and aluminum at 10% and raw‑material duties shape AKWELs plant network and sourcing choices. Localization rules — US EV final assembly for tax credits, India PLI for auto components (₹25,938 crore/≈$3.1bn) and rising European localization pressures — push regional production and supplier development. Geopolitical frictions raise cross‑border disruption risk and buffer inventory needs; AKWEL must balance cost, resilience and compliance in its footprint strategy.

Public procurement and strategic autonomy

National agendas such as the EU Critical Raw Materials Act (adopted June 2023) boost preference for local suppliers in strategic tech, benefiting suppliers of EV thermal management tied to battery security. Thermal solutions can qualify for IPCEI-style support (battery IPCEI public backing ~€3.2bn) or grants often ranging €10–100m. Enhanced FDI screening in ~24 EU/partner jurisdictions (2024) can slow M&A approvals, so active dialogue with authorities has unlocked cooperative R&D and funding.

Labor policy and social dialogue

Changes in wage frameworks (eg IG Metall 2023 deal ~8%) and working-time rules reshape plant competitiveness and cost base; incentives for vocational training help close mechatronics/automation gaps while strikes in automotive hubs can delay OEM deliveries; proactive workforce planning across AKWELs c.50 plants preserves service levels and reduces volatility.

- Wage shock: IG Metall 2023 ~8%

- Skills focus: vocational incentives for mechatronics

- Risk: strikes disrupt OEM supply

- Mitigation: proactive workforce planning

Infrastructure and energy policy

Energy transition policies shift electricity mix and prices, affecting AKWEL plants' access to low‑carbon power; EU industrial electricity averaged about €0.10/kWh in 2024 while France's nuclear fleet supplies ~70% of national generation, insulating some sites. Grid reliability and industrial tariffs materially affect cost per part for polymer processing; gas TTF fell ~60% from 2022 to 2024. Policies for hydrogen (EU 10 Mt by 2030) and advanced cooling can open new applications; site selection should weigh energy‑mix trajectories and incentives.

- Energy price: EU industrial ~€0.10/kWh (2024)

- France nuclear ~70% (2024)

- Gas TTF -60% vs 2022

- EU hydrogen target: 10 Mt by 2030

Policy shifts, tariffs and incentives reshape automotive supplier footprints in US, EU and China

Policy shifts (US IRA $369bn, $7,500 EV credit; EU 2035 ICE phase‑out; China NEV leadership) reshape AKWEL demand, tariffs (US steel 25%/aluminium 10%) and localization rules force regional footprint choices, while EU CRM Act, IPCEI ~€3.2bn and energy mix (€0.10/kWh EU 2024) create funding and site selection advantages; labor deals (IG Metall ~8% 2023) affect costs.

| Metric | Value |

|---|---|

| US IRA | $369bn |

| EV credit | $7,500 |

| US steel tariff | 25% |

| EU industrial power | €0.10/kWh (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect AKWEL across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section uses current data and trends, offers forward-looking insights and detailed sub-points to help executives, investors and entrepreneurs identify threats, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for AKWEL that teams can drop into presentations, annotate for regional specifics, and share for quick alignment—streamlining external risk discussions and speeding strategic decision-making.

Economic factors

Auto demand cycles and platform mix

Global light-vehicle sales (about 70–80 million units annually) drive AKWEL volumes, while EV penetration around 15% of new-car sales in 2024 reduces thermal-system content per vehicle. OEM platform consolidation concentrates award risk but offers scale on won programs. Tight forecast accuracy is vital to avoid overcapacity or missed demand. AKWEL’s diversified program mix across powertrains buffers cyclicality.

Raw material and logistics costs

Polymer resins, elastomers and metals show high price volatility linked to oil and gas swings (Brent averaged about $83/bbl in 2024) and tight supply-demand cycles, pushing resin spot moves into double digits. Freight and container rates — roughly $1,500 per FEU on average in 2024 for key East–West lanes — raise global and plant-to-plant transfer costs. OEM indexation clauses often lag 1–3 months, squeezing margins during spikes, so strategic hedging and dual-sourcing are used to stabilize input costs.

FX exposure and geographic mix

Multicurrency revenues and costs expose AKWEL to translation and transaction risk across EUR, USD, CNY and emerging-market currencies, which can compress margins and shift pricing power between OEMs and suppliers. Local-for-local production in Europe, China and North America provides natural hedges that reduce forex volatility on operating profits. Treasury policy must coordinate netting, forwards and invoicing currency with OEM contract clauses and indexation mechanisms to protect margins.

Interest rates and capex affordability

Higher policy rates (Fed funds ~5.25–5.50% and ECB depo ~4.0% in mid‑2025) raise financing costs for tooling, automation and plant upgrades, tightening payback thresholds for new EV‑focused lines; global EV sales were ~14% of new car sales in 2024, concentrating investment pressure on high‑visibility platforms. OEM payment terms and longer working capital cycles amplify financing strain, so AKWEL prioritizes platforms with durable volume visibility to protect returns.

- Rates: Fed 5.25–5.50% / ECB ~4.0%

- EV share 2024: ~14% of new sales

- Result: stricter payback, higher capex hurdle

- Mitigation: focus on platforms with stable volume

OEM pricing pressure and consolidation

Automakers push 2-4% annual cost-downs and productivity gains, compressing supplier margins into mid-single digits and intensifying Tier-1 competition and vertical integration risks to content share; differentiation via performance, weight and sustainability KPIs (CO2, recyclability) supports pricing resilience and design-in leverage; long-term agreements (typically 3-7 years) secure revenue visibility.

Policy shifts, tariffs and incentives reshape automotive supplier footprints in US, EU and China

Global light-vehicle volumes (~70–80m units) and EV mix (~14–15% new sales in 2024) reduce thermal-system content but concentrate awarded programs. Input volatility (Brent ~$83/bbl in 2024; freight ~ $1,500/FEU) and OEM 1–3-month indexation squeeze margins, prompting hedging and dual‑sourcing. Higher rates (Fed 5.25–5.50% / ECB ~4.0% mid‑2025) raise capex payback hurdles; OEM cost‑down targets 2–4% p.a. compress supplier margins to mid‑single digits.

Full Version Awaits

AKWEL PESTLE Analysis

The AKWEL PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the real, final product.

Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE analysis of AKWEL. Explore political, economic, social, technological, legal and environmental forces shaping its strategy and risk profile. Ideal for investors and strategists. Purchase the full, editable report to access deep-dive insights and download instantly.

Political factors

EV industrial policy and subsidies

Government incentives shape OEM electrification roadmaps and steer demand to EV-specific thermal and fluid systems: the US IRA mobilized roughly $369bn in clean-energy support and a $7,500 EV tax credit, the EU enforces a 2035 new-ICE sales phase-out, while China remains the largest NEV market—these shifts can speed or delay AKWEL’s EV capex and capacity plans, so monitoring policy stability across EU/US/China and active industry-body engagement is essential.

Trade policy, tariffs, and localization

Tariffs such as US steel at 25% and aluminum at 10% and raw‑material duties shape AKWELs plant network and sourcing choices. Localization rules — US EV final assembly for tax credits, India PLI for auto components (₹25,938 crore/≈$3.1bn) and rising European localization pressures — push regional production and supplier development. Geopolitical frictions raise cross‑border disruption risk and buffer inventory needs; AKWEL must balance cost, resilience and compliance in its footprint strategy.

Public procurement and strategic autonomy

National agendas such as the EU Critical Raw Materials Act (adopted June 2023) boost preference for local suppliers in strategic tech, benefiting suppliers of EV thermal management tied to battery security. Thermal solutions can qualify for IPCEI-style support (battery IPCEI public backing ~€3.2bn) or grants often ranging €10–100m. Enhanced FDI screening in ~24 EU/partner jurisdictions (2024) can slow M&A approvals, so active dialogue with authorities has unlocked cooperative R&D and funding.

Labor policy and social dialogue

Changes in wage frameworks (eg IG Metall 2023 deal ~8%) and working-time rules reshape plant competitiveness and cost base; incentives for vocational training help close mechatronics/automation gaps while strikes in automotive hubs can delay OEM deliveries; proactive workforce planning across AKWELs c.50 plants preserves service levels and reduces volatility.

- Wage shock: IG Metall 2023 ~8%

- Skills focus: vocational incentives for mechatronics

- Risk: strikes disrupt OEM supply

- Mitigation: proactive workforce planning

Infrastructure and energy policy

Energy transition policies shift electricity mix and prices, affecting AKWEL plants' access to low‑carbon power; EU industrial electricity averaged about €0.10/kWh in 2024 while France's nuclear fleet supplies ~70% of national generation, insulating some sites. Grid reliability and industrial tariffs materially affect cost per part for polymer processing; gas TTF fell ~60% from 2022 to 2024. Policies for hydrogen (EU 10 Mt by 2030) and advanced cooling can open new applications; site selection should weigh energy‑mix trajectories and incentives.

- Energy price: EU industrial ~€0.10/kWh (2024)

- France nuclear ~70% (2024)

- Gas TTF -60% vs 2022

- EU hydrogen target: 10 Mt by 2030

Policy shifts, tariffs and incentives reshape automotive supplier footprints in US, EU and China

Policy shifts (US IRA $369bn, $7,500 EV credit; EU 2035 ICE phase‑out; China NEV leadership) reshape AKWEL demand, tariffs (US steel 25%/aluminium 10%) and localization rules force regional footprint choices, while EU CRM Act, IPCEI ~€3.2bn and energy mix (€0.10/kWh EU 2024) create funding and site selection advantages; labor deals (IG Metall ~8% 2023) affect costs.

| Metric | Value |

|---|---|

| US IRA | $369bn |

| EV credit | $7,500 |

| US steel tariff | 25% |

| EU industrial power | €0.10/kWh (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect AKWEL across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section uses current data and trends, offers forward-looking insights and detailed sub-points to help executives, investors and entrepreneurs identify threats, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for AKWEL that teams can drop into presentations, annotate for regional specifics, and share for quick alignment—streamlining external risk discussions and speeding strategic decision-making.

Economic factors

Auto demand cycles and platform mix

Global light-vehicle sales (about 70–80 million units annually) drive AKWEL volumes, while EV penetration around 15% of new-car sales in 2024 reduces thermal-system content per vehicle. OEM platform consolidation concentrates award risk but offers scale on won programs. Tight forecast accuracy is vital to avoid overcapacity or missed demand. AKWEL’s diversified program mix across powertrains buffers cyclicality.

Raw material and logistics costs

Polymer resins, elastomers and metals show high price volatility linked to oil and gas swings (Brent averaged about $83/bbl in 2024) and tight supply-demand cycles, pushing resin spot moves into double digits. Freight and container rates — roughly $1,500 per FEU on average in 2024 for key East–West lanes — raise global and plant-to-plant transfer costs. OEM indexation clauses often lag 1–3 months, squeezing margins during spikes, so strategic hedging and dual-sourcing are used to stabilize input costs.

FX exposure and geographic mix

Multicurrency revenues and costs expose AKWEL to translation and transaction risk across EUR, USD, CNY and emerging-market currencies, which can compress margins and shift pricing power between OEMs and suppliers. Local-for-local production in Europe, China and North America provides natural hedges that reduce forex volatility on operating profits. Treasury policy must coordinate netting, forwards and invoicing currency with OEM contract clauses and indexation mechanisms to protect margins.

Interest rates and capex affordability

Higher policy rates (Fed funds ~5.25–5.50% and ECB depo ~4.0% in mid‑2025) raise financing costs for tooling, automation and plant upgrades, tightening payback thresholds for new EV‑focused lines; global EV sales were ~14% of new car sales in 2024, concentrating investment pressure on high‑visibility platforms. OEM payment terms and longer working capital cycles amplify financing strain, so AKWEL prioritizes platforms with durable volume visibility to protect returns.

- Rates: Fed 5.25–5.50% / ECB ~4.0%

- EV share 2024: ~14% of new sales

- Result: stricter payback, higher capex hurdle

- Mitigation: focus on platforms with stable volume

OEM pricing pressure and consolidation

Automakers push 2-4% annual cost-downs and productivity gains, compressing supplier margins into mid-single digits and intensifying Tier-1 competition and vertical integration risks to content share; differentiation via performance, weight and sustainability KPIs (CO2, recyclability) supports pricing resilience and design-in leverage; long-term agreements (typically 3-7 years) secure revenue visibility.

Policy shifts, tariffs and incentives reshape automotive supplier footprints in US, EU and China

Global light-vehicle volumes (~70–80m units) and EV mix (~14–15% new sales in 2024) reduce thermal-system content but concentrate awarded programs. Input volatility (Brent ~$83/bbl in 2024; freight ~ $1,500/FEU) and OEM 1–3-month indexation squeeze margins, prompting hedging and dual‑sourcing. Higher rates (Fed 5.25–5.50% / ECB ~4.0% mid‑2025) raise capex payback hurdles; OEM cost‑down targets 2–4% p.a. compress supplier margins to mid‑single digits.

Full Version Awaits

AKWEL PESTLE Analysis

The AKWEL PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the real, final product.