AKWEL SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

AKWEL's SWOT snapshot highlights resilient automotive-components expertise, exposure to EV transition, supply-chain risks and margin pressure—yet clear opportunities in electrification and aftermarket growth remain. Purchase the full SWOT analysis for a research-backed, editable Word + Excel report to plan investments and strategy with confidence.

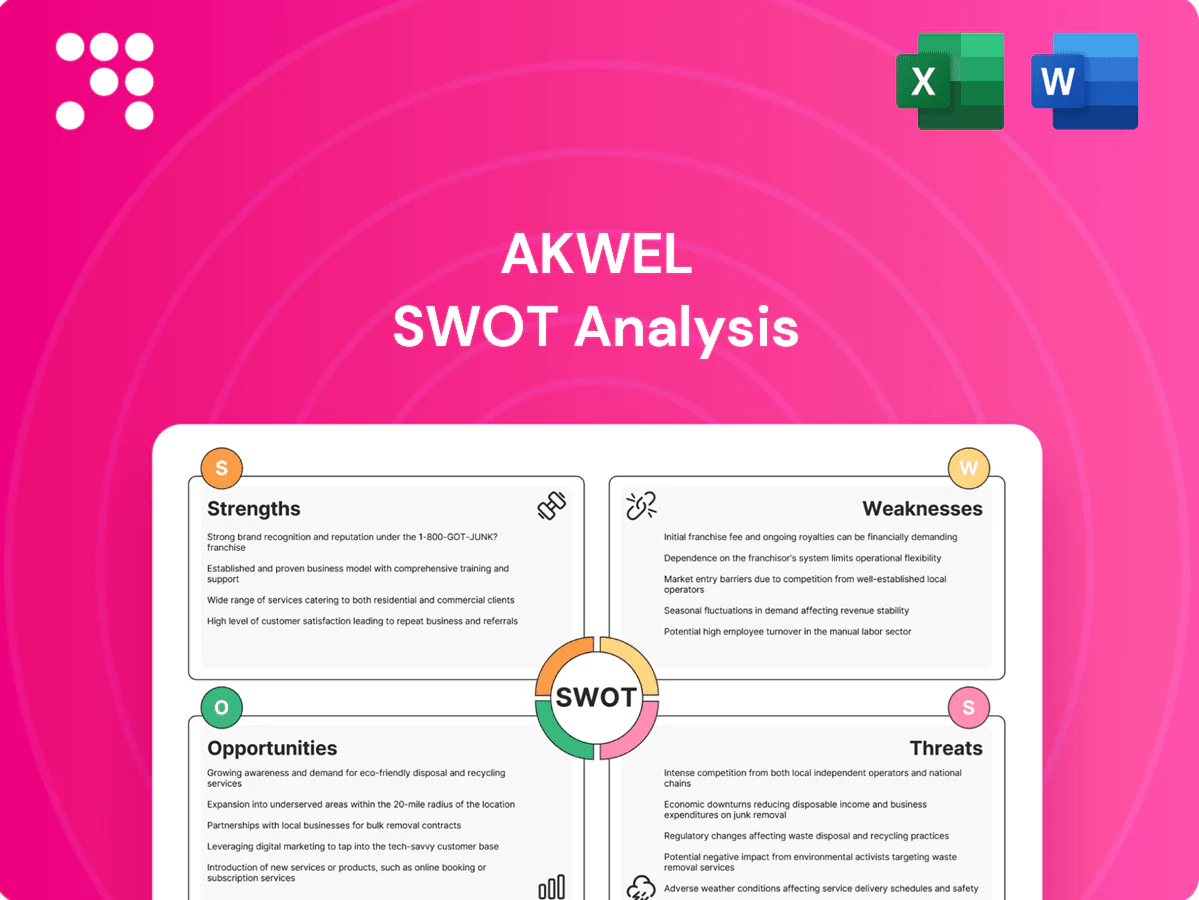

Strengths

Deep fluid and thermal expertise

Decades of know‑how in fluid conveyance and thermal management enable AKWEL to deliver robust, efficient designs; 2024 revenues near €1.1bn reflect strong commercial validation. This specialization creates technical moats in complex routing, sealing and heat exchange, supporting high reliability under harsh automotive conditions. OEMs such as Stellantis and Renault value this domain depth for platform‑critical components.

Integrated polymer, metal, mechatronics

Vertical competencies across polymers, metals and mechatronics shorten development cycles and, combined with integrated design-to-manufacture, optimize cost, weight and performance trade-offs; this system-level offering raises switching costs versus single-part suppliers and demonstrably improves RFQ win rates for AKWEL in recent program bids.

Global OEM customer base

Supplying major OEMs diversifies AKWELs revenue and stabilizes volumes, underpinning group sales of about €1.2bn in 2023. Early involvement in platform programs secures multi‑year demand visibility and repeat awards across global platforms. A footprint of production and engineering sites near assembly plants supports JIT delivery and co‑development with OEMs, strengthening long‑term partnerships.

EV-ready thermal solutions

AKWELs EV-ready thermal solutions cover battery, e-motor and power electronics with multi-loop, low-glycol and refrigerant architectures, matching the precise thermal control OEMs demand and positioning the firm to capture industry content-per-vehicle growth as global EV sales topped ~14 million in 2024.

- Proven industrialization reduces launch risk

- Multi-loop & low-glycol expertise

- Targets rising per-vehicle thermal content

Cost and sustainability orientation

AKWEL's process efficiency and lightweighting lower OEM total cost of ownership by reducing fuel consumption and part counts, with industry studies showing up to 10% TCO savings from component weight cuts; AKWEL reports recyclable polymers and CO2-reduction programs aligned with EU zero-emission new-car targets for 2035.

Design-for-manufacture practices cut scrap and energy use on the shopfloor, improving margins and shortening lead times, while sustainability credentials strengthen bid competitiveness in electrification contracts.

- up to 10% TCO savings

- aligned with EU 2035 zero-emission new-car mandate

- recyclable polymers & CO2 programs

- lower scrap, energy, and faster bids

Decades of thermal expertise, €1.1bn; EV sales ~14M

Decades of fluid and thermal know‑how drive robust designs; 2024 revenues ~€1.1bn and repeat OEM clients (Stellantis, Renault) validate platform relevance. Vertical polymers-to-mechatronics shorten cycles and raise switching costs, boosting RFQ wins. EV thermal systems cover battery/e‑motor/electronics as global EV sales ~14M (2024).

| Metric | Value |

|---|---|

| 2024 revenue | ~€1.1bn |

| 2023 revenue | ~€1.2bn |

| Global EV sales (2024) | ~14M |

| Key OEMs | Stellantis, Renault |

What is included in the product

Delivers a strategic overview of AKWEL’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats shaping its competitive position in automotive components, fluid management systems and electrification-driven growth.

Provides a concise AKWEL-focused SWOT matrix that relieves strategic alignment pain points by delivering fast, visual insights for clear communication and quick decision-making across teams.

Weaknesses

High OEM concentration

High OEM concentration leaves AKWEL exposed to a limited set of automotive customers, concentrating counterparty and demand risk. OEM bargaining leverage constrains AKWELs pricing power, limiting margin recovery. Program cancellations or platform shifts can materially reduce revenues, and lifecycle negotiations typically compress margins as production ramps and updates occur.

Exposure to ICE component mix

Legacy ICE fluid systems still account for a meaningful portion of AKWELs sales, leaving near-term exposure as OEMs shift to EVs. The EV transition risks cannibalizing specific product lines before volume from electrification fully compensates. Re-tooling plants and pruning the portfolio demand significant capital expenditure and lead time. Temporary utilization dips during the shift could compress margins and cash conversion.

Commodity input sensitivity

AKWEL’s cost base is exposed to resins, elastomers and aluminium volatility—FY2024 sales ~€1.3bn magnify COGS swings after aluminium rose ~18% in 2024 and polymer spot prices moved 10–25% in some months. Pass-through clauses often lag OEM contracts, compressing short-term margins by an observed 200–300 basis points during 2023–24 episodes. Hedging programs mitigate standard commodity risk but are imperfect for specialty polymers, and price volatility complicates quoting and inventory planning.

Scale vs mega-suppliers

Compared with Tier‑1 giants such as Bosch (Group sales €88.4bn in 2023), AKWEL's smaller scale (circa €1.1bn sales in 2024) limits bargaining power and R&D firepower, constraining ability to support global simultaneous launches; some OEMs still favor larger single‑source partners, so winning mega‑platforms often requires strategic alliances or consortium bids.

- Scale gap: Bosch €88.4bn (2023) vs AKWEL ~€1.1bn (2024)

- R&D/bargaining power: relatively limited

- Go‑to‑market: alliances needed for mega‑platforms

Capital intensity and tooling

Capital-intensive tooling and frequent program-specific investments tie up cash and extend payback periods, while steep ramp-up curves for PPAP and inventory builds strain working capital during platform launches. Ongoing plant network optimization and capacity realignment remain costly, and ROIC is often cyclical across vehicle platform lifecycles, compressing returns in early ramp phases.

- High cash tie-up: tooling and program spend

- Working capital pressure: PPAP & inventory ramps

- Costly plant optimization

- ROIC volatility across platform cycles

OEM concentration, ICE exposure and commodity swings squeeze margins despite €1.3bn sales

High OEM concentration limits pricing power and raises counterparty risk; program cancellations/platform shifts can materially hit revenue. Heavy exposure to ICE fluid systems risks near‑term product cannibalization as EV adoption rises, requiring costly retooling and causing utilization dips. Commodity volatility (aluminium +18% in 2024; polymers 10–25% swings) and capital‑intensive tooling compressed margins ~200–300bps in 2023–24, while scale lags peers (FY2024 sales €1.3bn vs Bosch €88.4bn).

| Metric | Value |

|---|---|

| FY2024 sales | €1.3bn |

| Bosch (peer) | €88.4bn (2023) |

| Aluminium 2024 | +18% |

| Polymer swings | 10–25% |

| Margin impact | 200–300bps (2023–24) |

Full Version Awaits

AKWEL SWOT Analysis

This is the actual AKWEL SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. Buy now to access the full, detailed file.

Dive Deeper Into the Company’s Strategic Blueprint

AKWEL's SWOT snapshot highlights resilient automotive-components expertise, exposure to EV transition, supply-chain risks and margin pressure—yet clear opportunities in electrification and aftermarket growth remain. Purchase the full SWOT analysis for a research-backed, editable Word + Excel report to plan investments and strategy with confidence.

Strengths

Deep fluid and thermal expertise

Decades of know‑how in fluid conveyance and thermal management enable AKWEL to deliver robust, efficient designs; 2024 revenues near €1.1bn reflect strong commercial validation. This specialization creates technical moats in complex routing, sealing and heat exchange, supporting high reliability under harsh automotive conditions. OEMs such as Stellantis and Renault value this domain depth for platform‑critical components.

Integrated polymer, metal, mechatronics

Vertical competencies across polymers, metals and mechatronics shorten development cycles and, combined with integrated design-to-manufacture, optimize cost, weight and performance trade-offs; this system-level offering raises switching costs versus single-part suppliers and demonstrably improves RFQ win rates for AKWEL in recent program bids.

Global OEM customer base

Supplying major OEMs diversifies AKWELs revenue and stabilizes volumes, underpinning group sales of about €1.2bn in 2023. Early involvement in platform programs secures multi‑year demand visibility and repeat awards across global platforms. A footprint of production and engineering sites near assembly plants supports JIT delivery and co‑development with OEMs, strengthening long‑term partnerships.

EV-ready thermal solutions

AKWELs EV-ready thermal solutions cover battery, e-motor and power electronics with multi-loop, low-glycol and refrigerant architectures, matching the precise thermal control OEMs demand and positioning the firm to capture industry content-per-vehicle growth as global EV sales topped ~14 million in 2024.

- Proven industrialization reduces launch risk

- Multi-loop & low-glycol expertise

- Targets rising per-vehicle thermal content

Cost and sustainability orientation

AKWEL's process efficiency and lightweighting lower OEM total cost of ownership by reducing fuel consumption and part counts, with industry studies showing up to 10% TCO savings from component weight cuts; AKWEL reports recyclable polymers and CO2-reduction programs aligned with EU zero-emission new-car targets for 2035.

Design-for-manufacture practices cut scrap and energy use on the shopfloor, improving margins and shortening lead times, while sustainability credentials strengthen bid competitiveness in electrification contracts.

- up to 10% TCO savings

- aligned with EU 2035 zero-emission new-car mandate

- recyclable polymers & CO2 programs

- lower scrap, energy, and faster bids

Decades of thermal expertise, €1.1bn; EV sales ~14M

Decades of fluid and thermal know‑how drive robust designs; 2024 revenues ~€1.1bn and repeat OEM clients (Stellantis, Renault) validate platform relevance. Vertical polymers-to-mechatronics shorten cycles and raise switching costs, boosting RFQ wins. EV thermal systems cover battery/e‑motor/electronics as global EV sales ~14M (2024).

| Metric | Value |

|---|---|

| 2024 revenue | ~€1.1bn |

| 2023 revenue | ~€1.2bn |

| Global EV sales (2024) | ~14M |

| Key OEMs | Stellantis, Renault |

What is included in the product

Delivers a strategic overview of AKWEL’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats shaping its competitive position in automotive components, fluid management systems and electrification-driven growth.

Provides a concise AKWEL-focused SWOT matrix that relieves strategic alignment pain points by delivering fast, visual insights for clear communication and quick decision-making across teams.

Weaknesses

High OEM concentration

High OEM concentration leaves AKWEL exposed to a limited set of automotive customers, concentrating counterparty and demand risk. OEM bargaining leverage constrains AKWELs pricing power, limiting margin recovery. Program cancellations or platform shifts can materially reduce revenues, and lifecycle negotiations typically compress margins as production ramps and updates occur.

Exposure to ICE component mix

Legacy ICE fluid systems still account for a meaningful portion of AKWELs sales, leaving near-term exposure as OEMs shift to EVs. The EV transition risks cannibalizing specific product lines before volume from electrification fully compensates. Re-tooling plants and pruning the portfolio demand significant capital expenditure and lead time. Temporary utilization dips during the shift could compress margins and cash conversion.

Commodity input sensitivity

AKWEL’s cost base is exposed to resins, elastomers and aluminium volatility—FY2024 sales ~€1.3bn magnify COGS swings after aluminium rose ~18% in 2024 and polymer spot prices moved 10–25% in some months. Pass-through clauses often lag OEM contracts, compressing short-term margins by an observed 200–300 basis points during 2023–24 episodes. Hedging programs mitigate standard commodity risk but are imperfect for specialty polymers, and price volatility complicates quoting and inventory planning.

Scale vs mega-suppliers

Compared with Tier‑1 giants such as Bosch (Group sales €88.4bn in 2023), AKWEL's smaller scale (circa €1.1bn sales in 2024) limits bargaining power and R&D firepower, constraining ability to support global simultaneous launches; some OEMs still favor larger single‑source partners, so winning mega‑platforms often requires strategic alliances or consortium bids.

- Scale gap: Bosch €88.4bn (2023) vs AKWEL ~€1.1bn (2024)

- R&D/bargaining power: relatively limited

- Go‑to‑market: alliances needed for mega‑platforms

Capital intensity and tooling

Capital-intensive tooling and frequent program-specific investments tie up cash and extend payback periods, while steep ramp-up curves for PPAP and inventory builds strain working capital during platform launches. Ongoing plant network optimization and capacity realignment remain costly, and ROIC is often cyclical across vehicle platform lifecycles, compressing returns in early ramp phases.

- High cash tie-up: tooling and program spend

- Working capital pressure: PPAP & inventory ramps

- Costly plant optimization

- ROIC volatility across platform cycles

OEM concentration, ICE exposure and commodity swings squeeze margins despite €1.3bn sales

High OEM concentration limits pricing power and raises counterparty risk; program cancellations/platform shifts can materially hit revenue. Heavy exposure to ICE fluid systems risks near‑term product cannibalization as EV adoption rises, requiring costly retooling and causing utilization dips. Commodity volatility (aluminium +18% in 2024; polymers 10–25% swings) and capital‑intensive tooling compressed margins ~200–300bps in 2023–24, while scale lags peers (FY2024 sales €1.3bn vs Bosch €88.4bn).

| Metric | Value |

|---|---|

| FY2024 sales | €1.3bn |

| Bosch (peer) | €88.4bn (2023) |

| Aluminium 2024 | +18% |

| Polymer swings | 10–25% |

| Margin impact | 200–300bps (2023–24) |

Full Version Awaits

AKWEL SWOT Analysis

This is the actual AKWEL SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. Buy now to access the full, detailed file.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

AKWEL's SWOT snapshot highlights resilient automotive-components expertise, exposure to EV transition, supply-chain risks and margin pressure—yet clear opportunities in electrification and aftermarket growth remain. Purchase the full SWOT analysis for a research-backed, editable Word + Excel report to plan investments and strategy with confidence.

Strengths

Deep fluid and thermal expertise

Decades of know‑how in fluid conveyance and thermal management enable AKWEL to deliver robust, efficient designs; 2024 revenues near €1.1bn reflect strong commercial validation. This specialization creates technical moats in complex routing, sealing and heat exchange, supporting high reliability under harsh automotive conditions. OEMs such as Stellantis and Renault value this domain depth for platform‑critical components.

Integrated polymer, metal, mechatronics

Vertical competencies across polymers, metals and mechatronics shorten development cycles and, combined with integrated design-to-manufacture, optimize cost, weight and performance trade-offs; this system-level offering raises switching costs versus single-part suppliers and demonstrably improves RFQ win rates for AKWEL in recent program bids.

Global OEM customer base

Supplying major OEMs diversifies AKWELs revenue and stabilizes volumes, underpinning group sales of about €1.2bn in 2023. Early involvement in platform programs secures multi‑year demand visibility and repeat awards across global platforms. A footprint of production and engineering sites near assembly plants supports JIT delivery and co‑development with OEMs, strengthening long‑term partnerships.

EV-ready thermal solutions

AKWELs EV-ready thermal solutions cover battery, e-motor and power electronics with multi-loop, low-glycol and refrigerant architectures, matching the precise thermal control OEMs demand and positioning the firm to capture industry content-per-vehicle growth as global EV sales topped ~14 million in 2024.

- Proven industrialization reduces launch risk

- Multi-loop & low-glycol expertise

- Targets rising per-vehicle thermal content

Cost and sustainability orientation

AKWEL's process efficiency and lightweighting lower OEM total cost of ownership by reducing fuel consumption and part counts, with industry studies showing up to 10% TCO savings from component weight cuts; AKWEL reports recyclable polymers and CO2-reduction programs aligned with EU zero-emission new-car targets for 2035.

Design-for-manufacture practices cut scrap and energy use on the shopfloor, improving margins and shortening lead times, while sustainability credentials strengthen bid competitiveness in electrification contracts.

- up to 10% TCO savings

- aligned with EU 2035 zero-emission new-car mandate

- recyclable polymers & CO2 programs

- lower scrap, energy, and faster bids

Decades of thermal expertise, €1.1bn; EV sales ~14M

Decades of fluid and thermal know‑how drive robust designs; 2024 revenues ~€1.1bn and repeat OEM clients (Stellantis, Renault) validate platform relevance. Vertical polymers-to-mechatronics shorten cycles and raise switching costs, boosting RFQ wins. EV thermal systems cover battery/e‑motor/electronics as global EV sales ~14M (2024).

| Metric | Value |

|---|---|

| 2024 revenue | ~€1.1bn |

| 2023 revenue | ~€1.2bn |

| Global EV sales (2024) | ~14M |

| Key OEMs | Stellantis, Renault |

What is included in the product

Delivers a strategic overview of AKWEL’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats shaping its competitive position in automotive components, fluid management systems and electrification-driven growth.

Provides a concise AKWEL-focused SWOT matrix that relieves strategic alignment pain points by delivering fast, visual insights for clear communication and quick decision-making across teams.

Weaknesses

High OEM concentration

High OEM concentration leaves AKWEL exposed to a limited set of automotive customers, concentrating counterparty and demand risk. OEM bargaining leverage constrains AKWELs pricing power, limiting margin recovery. Program cancellations or platform shifts can materially reduce revenues, and lifecycle negotiations typically compress margins as production ramps and updates occur.

Exposure to ICE component mix

Legacy ICE fluid systems still account for a meaningful portion of AKWELs sales, leaving near-term exposure as OEMs shift to EVs. The EV transition risks cannibalizing specific product lines before volume from electrification fully compensates. Re-tooling plants and pruning the portfolio demand significant capital expenditure and lead time. Temporary utilization dips during the shift could compress margins and cash conversion.

Commodity input sensitivity

AKWEL’s cost base is exposed to resins, elastomers and aluminium volatility—FY2024 sales ~€1.3bn magnify COGS swings after aluminium rose ~18% in 2024 and polymer spot prices moved 10–25% in some months. Pass-through clauses often lag OEM contracts, compressing short-term margins by an observed 200–300 basis points during 2023–24 episodes. Hedging programs mitigate standard commodity risk but are imperfect for specialty polymers, and price volatility complicates quoting and inventory planning.

Scale vs mega-suppliers

Compared with Tier‑1 giants such as Bosch (Group sales €88.4bn in 2023), AKWEL's smaller scale (circa €1.1bn sales in 2024) limits bargaining power and R&D firepower, constraining ability to support global simultaneous launches; some OEMs still favor larger single‑source partners, so winning mega‑platforms often requires strategic alliances or consortium bids.

- Scale gap: Bosch €88.4bn (2023) vs AKWEL ~€1.1bn (2024)

- R&D/bargaining power: relatively limited

- Go‑to‑market: alliances needed for mega‑platforms

Capital intensity and tooling

Capital-intensive tooling and frequent program-specific investments tie up cash and extend payback periods, while steep ramp-up curves for PPAP and inventory builds strain working capital during platform launches. Ongoing plant network optimization and capacity realignment remain costly, and ROIC is often cyclical across vehicle platform lifecycles, compressing returns in early ramp phases.

- High cash tie-up: tooling and program spend

- Working capital pressure: PPAP & inventory ramps

- Costly plant optimization

- ROIC volatility across platform cycles

OEM concentration, ICE exposure and commodity swings squeeze margins despite €1.3bn sales

High OEM concentration limits pricing power and raises counterparty risk; program cancellations/platform shifts can materially hit revenue. Heavy exposure to ICE fluid systems risks near‑term product cannibalization as EV adoption rises, requiring costly retooling and causing utilization dips. Commodity volatility (aluminium +18% in 2024; polymers 10–25% swings) and capital‑intensive tooling compressed margins ~200–300bps in 2023–24, while scale lags peers (FY2024 sales €1.3bn vs Bosch €88.4bn).

| Metric | Value |

|---|---|

| FY2024 sales | €1.3bn |

| Bosch (peer) | €88.4bn (2023) |

| Aluminium 2024 | +18% |

| Polymer swings | 10–25% |

| Margin impact | 200–300bps (2023–24) |

Full Version Awaits

AKWEL SWOT Analysis

This is the actual AKWEL SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. Buy now to access the full, detailed file.