Alan Allman Associates PESTLE Analysis

Your Shortcut to Market Insight Starts Here

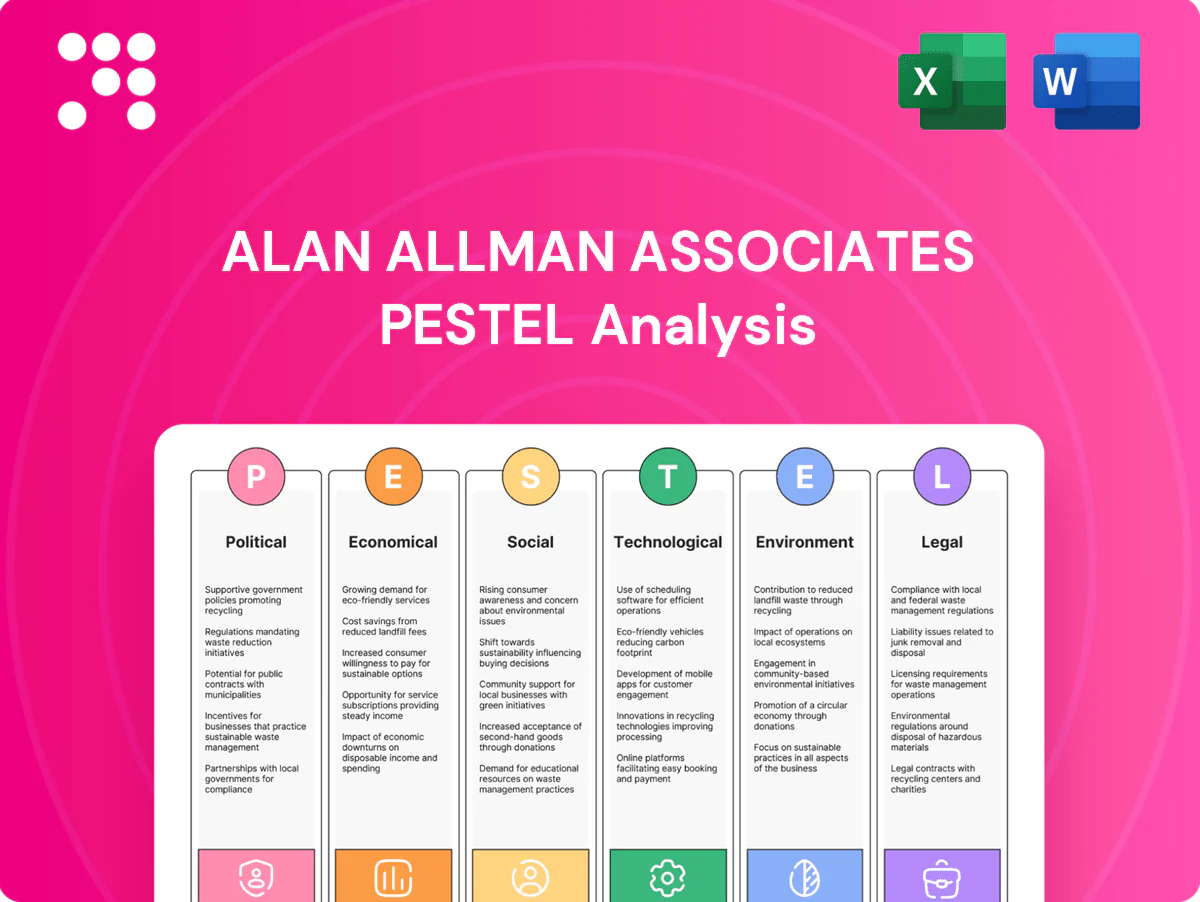

Discover how political, economic, social, technological, legal, and environmental forces shape Alan Allman Associates’ strategy and risk profile. This PESTLE pinpoints key trends, threats, and opportunities to inform smarter decisions. Buy the full, editable analysis for a complete, actionable roadmap you can use immediately.

Political factors

EU and national digital policy influence

Shifts in EU digital strategies and national industrial policies are reshaping client demand for transformation programs, increasing emphasis on cloud, AI and cybersecurity investments. Funding and public tenders — notably NextGenerationEU €806.9bn and the Digital Europe Programme €7.5bn — can accelerate cross‑sector projects; public procurement equals roughly 14% of EU GDP. Alignment with policy priorities like data sovereignty and digital skills boosts win rates, so monitoring policy cycles is essential for pipeline planning.

Public procurement and oversight

Stricter procurement rules in government and regulated sectors lengthen sales cycles and can compress margins; the World Bank notes public procurement represents roughly 15% of global GDP, increasing scrutiny. Transparency and local-content requirements advantage networked firms with in-country presence. Framework agreements commonly span 2–5 years, unlocking multi-year revenue visibility. Robust compliance capability reduces bid disqualification and is a clear competitive differentiator.

Geopolitical tensions and supply-chain resilience

Geopolitical risks are driving clients to re-shore, diversify vendors and redesign operating models; a 2024 McKinsey survey found about 60% of companies accelerating supplier diversification, creating advisory demand in risk, compliance and performance improvement. Scenario-planning services rose 35% in advisory RFPs in 2024. Board-level decision delays often elongate deal cycles by 3–6 months, slowing closures.

Talent mobility and visa regimes

Consulting delivery depends on cross-border teams and expert mobility; tightening visa rules and work-permit delays raise project staffing risk and can push utilization from typical industry levels around 75% toward greater volatility. Local partnerships within Alan Allman Associates network mitigate bottlenecks, while proactive workforce planning and bench management reduce utilization swings and resourcing lead times.

- Cross-border dependency: high

- Visa delays: increase staffing risk

- Local partners: mitigate bottlenecks

- Proactive planning: stabilizes utilization (~75%)

Cyber and critical infrastructure priorities

Government emphasis on cybersecurity and critical infrastructure protection drives steady demand for Alan Allman Associates, with NIS2 (EU, adopted 2023) and US federal directives pushing compliance timelines through 2024–2025 and beyond; global cybersecurity spending topped 200 billion USD in 2024, sustaining multi-year investment in resilience projects.

- Funding and mandates accelerate compliance and resilience projects

- Participation in certified programs pre-qualifies group for sensitive engagements

- Political emphasis sustains multi-year contracts and recurring revenue

EU policy and funding lengthen cycles and create multi-year advisory opportunities

Policy shifts (EU industrial/digital, NIS2), large public funding and stricter procurement lengthen cycles but create multi‑year opportunities; geopolitical reshoring raises advisory demand; visa rules heighten staffing risk, mitigated by local partners and proactive planning.

| Factor | Impact | Key data |

|---|---|---|

| EU funding | drives projects | NextGenerationEU €806.9bn; Digital Europe €7.5bn |

| Public procurement | longer cycles | ~14% EU GDP; ~15% global GDP |

| Cybersecurity | recurring demand | $200bn global spend 2024; NIS2 (2023) |

| Workforce mobility | staffing risk | utilization ~75% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Alan Allman Associates, combining data-driven trends and regional specifics to reveal risks, opportunities and actionable, forward-looking insights for executives, consultants and investors to support strategy, funding and scenario planning.

Alan Allman Associates' PESTLE Analysis delivers a concise, visually segmented summary that’s easy to drop into presentations or share across teams, and includes editable notes so users can quickly adapt insights to their region, business line, or planning sessions.

Economic factors

IT and consulting spend cycles

Macro growth and corporate profitability drive transformation budgets; IMF estimates world GDP growth of about 3.0% in 2024 and 3.3% in 2025, constraining discretionary spend when GDP slows. Gartner projects global IT spend near $5.6 trillion in 2024, but downturns shift demand to cost-takeout and operational-excellence projects while innovation slows. Counter-cyclical offerings (automation, managed services) stabilize utilization, so portfolio mix should flex with the cycle.

Interest rates and capital costs

Higher rates (US federal funds 5.25–5.50% in late 2024) tighten client hurdle rates for transformation ROI, making shorter payback periods essential. Payback-focused business cases and disciplined value-tracking become decisive in project approval. For the group, higher financing costs compress M&A appetite among network firms, while strong cash conversion preserves deal capacity.

Labor market tightness and wage inflation

Consulting talent remains scarce in data, cloud and cybersecurity, with ISC2 reporting a global cybersecurity workforce shortfall of about 3.4 million in 2023. Wage inflation is compressing margins unless Alan Allman Associates can increase pricing power and realize higher bill rates. Nearshore and hub-and-spoke delivery models can protect unit economics by lowering labor cost differentials. Strategic upskilling reduces dependence on expensive external hires and improves utilization.

Sectoral divergences

Financial services and public sector often sustain spend while cyclical industries defer projects; public-sector ICT budgets rose in many markets in 2024 supporting steady demand. Health and the energy transition are growth pockets (IEA clean energy investment ~1.7 trillion USD in 2023), and vertical-tailored propositions boost hit rates; diversification across sectors smooths revenue.

- Sector: Financial services/public sector — resilient demand

- Growth: Health & energy transition — IEA ~$1.7tn (2023)

- Sales: Vertical propositions — higher conversion

- Risk: Cyclicals — timing delays; diversification mitigates

Currency volatility across geographies

Operating through multiple firms exposes Alan Allman Associates earnings to FX swings across corridors; global FX turnover averaged about 7.5 trillion USD per day in the BIS 2022 Triennial Survey, underscoring market depth and volatility risk. Pricing in client currency and using natural hedges can materially reduce translation and transaction exposure, while central treasury policies align cash flows and costs. Transparent FX management and reporting support investor confidence and creditworthiness.

- FX turnover: BIS 2022 — 7.5 trillion USD/day

- Mitigation: client-currency pricing, natural hedges, central treasury

- Benefit: improved investor confidence via transparent FX policies

EU policy and funding lengthen cycles and create multi-year advisory opportunities

Global GDP ~3.0% (2024) limits discretionary transformation spend while Gartner forecasts global IT spend ~$5.6T (2024), shifting demand to cost-reduction and managed services. Higher rates (US 5.25–5.50% late 2024) raise ROI hurdles; talent gaps (cybersecurity shortfall ~3.4M, 2023) squeeze margins; public sector, financial services and energy transition ($1.7T clean energy invest, 2023) offer resilience.

| Metric | Value |

|---|---|

| World GDP growth | 3.0% (2024), 3.3% (2025 IMF) |

| Global IT spend | $5.6T (2024, Gartner) |

| US policy rate | 5.25–5.50% (late 2024) |

| Cyber workforce gap | ~3.4M (2023, ISC2) |

| Clean energy invest | $1.7T (2023, IEA) |

| FX turnover | $7.5T/day (2022, BIS) |

Same Document Delivered

Alan Allman Associates PESTLE Analysis

The preview shown here is the exact Alan Allman Associates PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the layout, content, and structure are exactly as delivered. After checkout you’ll instantly download this finished, professionally structured file.

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces shape Alan Allman Associates’ strategy and risk profile. This PESTLE pinpoints key trends, threats, and opportunities to inform smarter decisions. Buy the full, editable analysis for a complete, actionable roadmap you can use immediately.

Political factors

EU and national digital policy influence

Shifts in EU digital strategies and national industrial policies are reshaping client demand for transformation programs, increasing emphasis on cloud, AI and cybersecurity investments. Funding and public tenders — notably NextGenerationEU €806.9bn and the Digital Europe Programme €7.5bn — can accelerate cross‑sector projects; public procurement equals roughly 14% of EU GDP. Alignment with policy priorities like data sovereignty and digital skills boosts win rates, so monitoring policy cycles is essential for pipeline planning.

Public procurement and oversight

Stricter procurement rules in government and regulated sectors lengthen sales cycles and can compress margins; the World Bank notes public procurement represents roughly 15% of global GDP, increasing scrutiny. Transparency and local-content requirements advantage networked firms with in-country presence. Framework agreements commonly span 2–5 years, unlocking multi-year revenue visibility. Robust compliance capability reduces bid disqualification and is a clear competitive differentiator.

Geopolitical tensions and supply-chain resilience

Geopolitical risks are driving clients to re-shore, diversify vendors and redesign operating models; a 2024 McKinsey survey found about 60% of companies accelerating supplier diversification, creating advisory demand in risk, compliance and performance improvement. Scenario-planning services rose 35% in advisory RFPs in 2024. Board-level decision delays often elongate deal cycles by 3–6 months, slowing closures.

Talent mobility and visa regimes

Consulting delivery depends on cross-border teams and expert mobility; tightening visa rules and work-permit delays raise project staffing risk and can push utilization from typical industry levels around 75% toward greater volatility. Local partnerships within Alan Allman Associates network mitigate bottlenecks, while proactive workforce planning and bench management reduce utilization swings and resourcing lead times.

- Cross-border dependency: high

- Visa delays: increase staffing risk

- Local partners: mitigate bottlenecks

- Proactive planning: stabilizes utilization (~75%)

Cyber and critical infrastructure priorities

Government emphasis on cybersecurity and critical infrastructure protection drives steady demand for Alan Allman Associates, with NIS2 (EU, adopted 2023) and US federal directives pushing compliance timelines through 2024–2025 and beyond; global cybersecurity spending topped 200 billion USD in 2024, sustaining multi-year investment in resilience projects.

- Funding and mandates accelerate compliance and resilience projects

- Participation in certified programs pre-qualifies group for sensitive engagements

- Political emphasis sustains multi-year contracts and recurring revenue

EU policy and funding lengthen cycles and create multi-year advisory opportunities

Policy shifts (EU industrial/digital, NIS2), large public funding and stricter procurement lengthen cycles but create multi‑year opportunities; geopolitical reshoring raises advisory demand; visa rules heighten staffing risk, mitigated by local partners and proactive planning.

| Factor | Impact | Key data |

|---|---|---|

| EU funding | drives projects | NextGenerationEU €806.9bn; Digital Europe €7.5bn |

| Public procurement | longer cycles | ~14% EU GDP; ~15% global GDP |

| Cybersecurity | recurring demand | $200bn global spend 2024; NIS2 (2023) |

| Workforce mobility | staffing risk | utilization ~75% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Alan Allman Associates, combining data-driven trends and regional specifics to reveal risks, opportunities and actionable, forward-looking insights for executives, consultants and investors to support strategy, funding and scenario planning.

Alan Allman Associates' PESTLE Analysis delivers a concise, visually segmented summary that’s easy to drop into presentations or share across teams, and includes editable notes so users can quickly adapt insights to their region, business line, or planning sessions.

Economic factors

IT and consulting spend cycles

Macro growth and corporate profitability drive transformation budgets; IMF estimates world GDP growth of about 3.0% in 2024 and 3.3% in 2025, constraining discretionary spend when GDP slows. Gartner projects global IT spend near $5.6 trillion in 2024, but downturns shift demand to cost-takeout and operational-excellence projects while innovation slows. Counter-cyclical offerings (automation, managed services) stabilize utilization, so portfolio mix should flex with the cycle.

Interest rates and capital costs

Higher rates (US federal funds 5.25–5.50% in late 2024) tighten client hurdle rates for transformation ROI, making shorter payback periods essential. Payback-focused business cases and disciplined value-tracking become decisive in project approval. For the group, higher financing costs compress M&A appetite among network firms, while strong cash conversion preserves deal capacity.

Labor market tightness and wage inflation

Consulting talent remains scarce in data, cloud and cybersecurity, with ISC2 reporting a global cybersecurity workforce shortfall of about 3.4 million in 2023. Wage inflation is compressing margins unless Alan Allman Associates can increase pricing power and realize higher bill rates. Nearshore and hub-and-spoke delivery models can protect unit economics by lowering labor cost differentials. Strategic upskilling reduces dependence on expensive external hires and improves utilization.

Sectoral divergences

Financial services and public sector often sustain spend while cyclical industries defer projects; public-sector ICT budgets rose in many markets in 2024 supporting steady demand. Health and the energy transition are growth pockets (IEA clean energy investment ~1.7 trillion USD in 2023), and vertical-tailored propositions boost hit rates; diversification across sectors smooths revenue.

- Sector: Financial services/public sector — resilient demand

- Growth: Health & energy transition — IEA ~$1.7tn (2023)

- Sales: Vertical propositions — higher conversion

- Risk: Cyclicals — timing delays; diversification mitigates

Currency volatility across geographies

Operating through multiple firms exposes Alan Allman Associates earnings to FX swings across corridors; global FX turnover averaged about 7.5 trillion USD per day in the BIS 2022 Triennial Survey, underscoring market depth and volatility risk. Pricing in client currency and using natural hedges can materially reduce translation and transaction exposure, while central treasury policies align cash flows and costs. Transparent FX management and reporting support investor confidence and creditworthiness.

- FX turnover: BIS 2022 — 7.5 trillion USD/day

- Mitigation: client-currency pricing, natural hedges, central treasury

- Benefit: improved investor confidence via transparent FX policies

EU policy and funding lengthen cycles and create multi-year advisory opportunities

Global GDP ~3.0% (2024) limits discretionary transformation spend while Gartner forecasts global IT spend ~$5.6T (2024), shifting demand to cost-reduction and managed services. Higher rates (US 5.25–5.50% late 2024) raise ROI hurdles; talent gaps (cybersecurity shortfall ~3.4M, 2023) squeeze margins; public sector, financial services and energy transition ($1.7T clean energy invest, 2023) offer resilience.

| Metric | Value |

|---|---|

| World GDP growth | 3.0% (2024), 3.3% (2025 IMF) |

| Global IT spend | $5.6T (2024, Gartner) |

| US policy rate | 5.25–5.50% (late 2024) |

| Cyber workforce gap | ~3.4M (2023, ISC2) |

| Clean energy invest | $1.7T (2023, IEA) |

| FX turnover | $7.5T/day (2022, BIS) |

Same Document Delivered

Alan Allman Associates PESTLE Analysis

The preview shown here is the exact Alan Allman Associates PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the layout, content, and structure are exactly as delivered. After checkout you’ll instantly download this finished, professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Discover how political, economic, social, technological, legal, and environmental forces shape Alan Allman Associates’ strategy and risk profile. This PESTLE pinpoints key trends, threats, and opportunities to inform smarter decisions. Buy the full, editable analysis for a complete, actionable roadmap you can use immediately.

Political factors

EU and national digital policy influence

Shifts in EU digital strategies and national industrial policies are reshaping client demand for transformation programs, increasing emphasis on cloud, AI and cybersecurity investments. Funding and public tenders — notably NextGenerationEU €806.9bn and the Digital Europe Programme €7.5bn — can accelerate cross‑sector projects; public procurement equals roughly 14% of EU GDP. Alignment with policy priorities like data sovereignty and digital skills boosts win rates, so monitoring policy cycles is essential for pipeline planning.

Public procurement and oversight

Stricter procurement rules in government and regulated sectors lengthen sales cycles and can compress margins; the World Bank notes public procurement represents roughly 15% of global GDP, increasing scrutiny. Transparency and local-content requirements advantage networked firms with in-country presence. Framework agreements commonly span 2–5 years, unlocking multi-year revenue visibility. Robust compliance capability reduces bid disqualification and is a clear competitive differentiator.

Geopolitical tensions and supply-chain resilience

Geopolitical risks are driving clients to re-shore, diversify vendors and redesign operating models; a 2024 McKinsey survey found about 60% of companies accelerating supplier diversification, creating advisory demand in risk, compliance and performance improvement. Scenario-planning services rose 35% in advisory RFPs in 2024. Board-level decision delays often elongate deal cycles by 3–6 months, slowing closures.

Talent mobility and visa regimes

Consulting delivery depends on cross-border teams and expert mobility; tightening visa rules and work-permit delays raise project staffing risk and can push utilization from typical industry levels around 75% toward greater volatility. Local partnerships within Alan Allman Associates network mitigate bottlenecks, while proactive workforce planning and bench management reduce utilization swings and resourcing lead times.

- Cross-border dependency: high

- Visa delays: increase staffing risk

- Local partners: mitigate bottlenecks

- Proactive planning: stabilizes utilization (~75%)

Cyber and critical infrastructure priorities

Government emphasis on cybersecurity and critical infrastructure protection drives steady demand for Alan Allman Associates, with NIS2 (EU, adopted 2023) and US federal directives pushing compliance timelines through 2024–2025 and beyond; global cybersecurity spending topped 200 billion USD in 2024, sustaining multi-year investment in resilience projects.

- Funding and mandates accelerate compliance and resilience projects

- Participation in certified programs pre-qualifies group for sensitive engagements

- Political emphasis sustains multi-year contracts and recurring revenue

EU policy and funding lengthen cycles and create multi-year advisory opportunities

Policy shifts (EU industrial/digital, NIS2), large public funding and stricter procurement lengthen cycles but create multi‑year opportunities; geopolitical reshoring raises advisory demand; visa rules heighten staffing risk, mitigated by local partners and proactive planning.

| Factor | Impact | Key data |

|---|---|---|

| EU funding | drives projects | NextGenerationEU €806.9bn; Digital Europe €7.5bn |

| Public procurement | longer cycles | ~14% EU GDP; ~15% global GDP |

| Cybersecurity | recurring demand | $200bn global spend 2024; NIS2 (2023) |

| Workforce mobility | staffing risk | utilization ~75% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Alan Allman Associates, combining data-driven trends and regional specifics to reveal risks, opportunities and actionable, forward-looking insights for executives, consultants and investors to support strategy, funding and scenario planning.

Alan Allman Associates' PESTLE Analysis delivers a concise, visually segmented summary that’s easy to drop into presentations or share across teams, and includes editable notes so users can quickly adapt insights to their region, business line, or planning sessions.

Economic factors

IT and consulting spend cycles

Macro growth and corporate profitability drive transformation budgets; IMF estimates world GDP growth of about 3.0% in 2024 and 3.3% in 2025, constraining discretionary spend when GDP slows. Gartner projects global IT spend near $5.6 trillion in 2024, but downturns shift demand to cost-takeout and operational-excellence projects while innovation slows. Counter-cyclical offerings (automation, managed services) stabilize utilization, so portfolio mix should flex with the cycle.

Interest rates and capital costs

Higher rates (US federal funds 5.25–5.50% in late 2024) tighten client hurdle rates for transformation ROI, making shorter payback periods essential. Payback-focused business cases and disciplined value-tracking become decisive in project approval. For the group, higher financing costs compress M&A appetite among network firms, while strong cash conversion preserves deal capacity.

Labor market tightness and wage inflation

Consulting talent remains scarce in data, cloud and cybersecurity, with ISC2 reporting a global cybersecurity workforce shortfall of about 3.4 million in 2023. Wage inflation is compressing margins unless Alan Allman Associates can increase pricing power and realize higher bill rates. Nearshore and hub-and-spoke delivery models can protect unit economics by lowering labor cost differentials. Strategic upskilling reduces dependence on expensive external hires and improves utilization.

Sectoral divergences

Financial services and public sector often sustain spend while cyclical industries defer projects; public-sector ICT budgets rose in many markets in 2024 supporting steady demand. Health and the energy transition are growth pockets (IEA clean energy investment ~1.7 trillion USD in 2023), and vertical-tailored propositions boost hit rates; diversification across sectors smooths revenue.

- Sector: Financial services/public sector — resilient demand

- Growth: Health & energy transition — IEA ~$1.7tn (2023)

- Sales: Vertical propositions — higher conversion

- Risk: Cyclicals — timing delays; diversification mitigates

Currency volatility across geographies

Operating through multiple firms exposes Alan Allman Associates earnings to FX swings across corridors; global FX turnover averaged about 7.5 trillion USD per day in the BIS 2022 Triennial Survey, underscoring market depth and volatility risk. Pricing in client currency and using natural hedges can materially reduce translation and transaction exposure, while central treasury policies align cash flows and costs. Transparent FX management and reporting support investor confidence and creditworthiness.

- FX turnover: BIS 2022 — 7.5 trillion USD/day

- Mitigation: client-currency pricing, natural hedges, central treasury

- Benefit: improved investor confidence via transparent FX policies

EU policy and funding lengthen cycles and create multi-year advisory opportunities

Global GDP ~3.0% (2024) limits discretionary transformation spend while Gartner forecasts global IT spend ~$5.6T (2024), shifting demand to cost-reduction and managed services. Higher rates (US 5.25–5.50% late 2024) raise ROI hurdles; talent gaps (cybersecurity shortfall ~3.4M, 2023) squeeze margins; public sector, financial services and energy transition ($1.7T clean energy invest, 2023) offer resilience.

| Metric | Value |

|---|---|

| World GDP growth | 3.0% (2024), 3.3% (2025 IMF) |

| Global IT spend | $5.6T (2024, Gartner) |

| US policy rate | 5.25–5.50% (late 2024) |

| Cyber workforce gap | ~3.4M (2023, ISC2) |

| Clean energy invest | $1.7T (2023, IEA) |

| FX turnover | $7.5T/day (2022, BIS) |

Same Document Delivered

Alan Allman Associates PESTLE Analysis

The preview shown here is the exact Alan Allman Associates PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the layout, content, and structure are exactly as delivered. After checkout you’ll instantly download this finished, professionally structured file.