Albaad Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

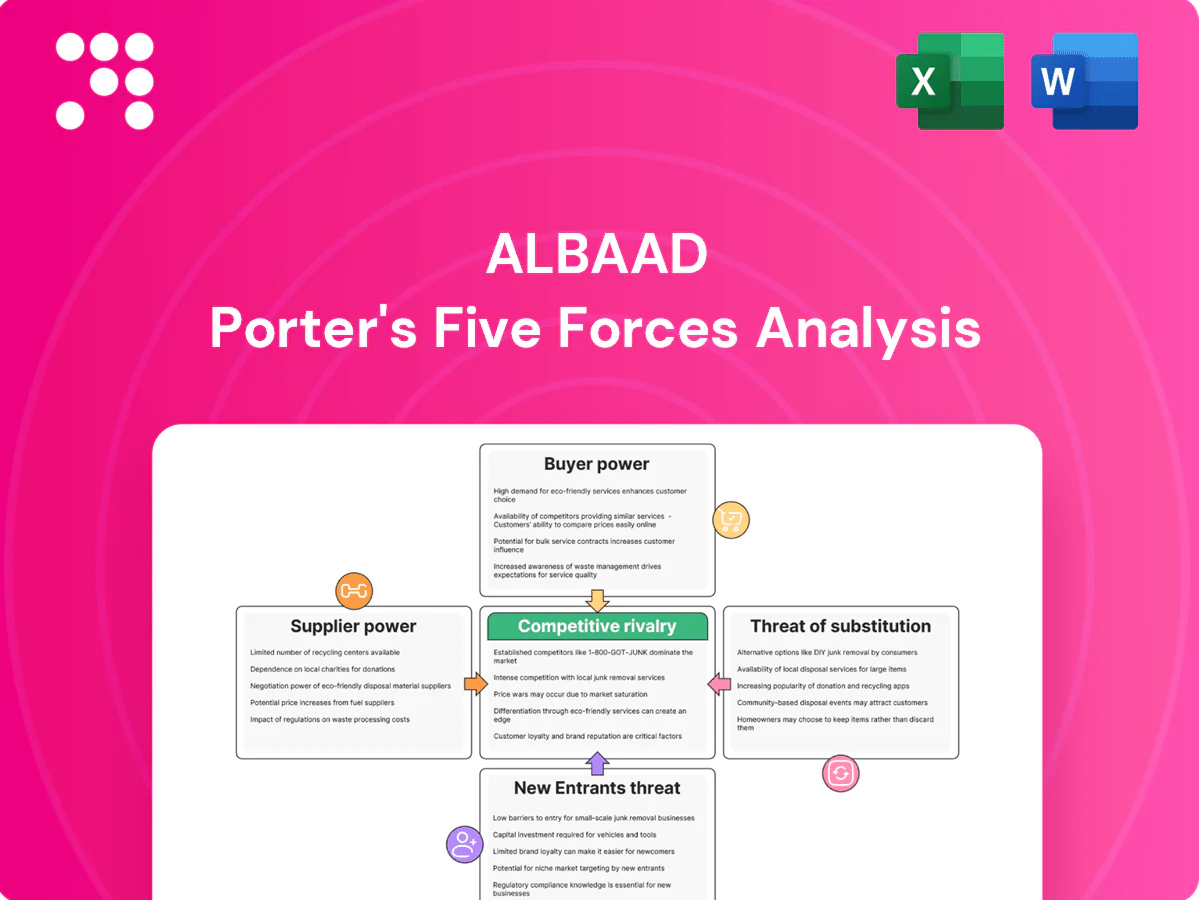

Albaad’s Porter's Five Forces snapshot highlights intense rivalry in personal-care packaging, moderate supplier power, rising buyer sophistication, and manageable substitute threats driven by innovation. These dynamics shape margins and strategic options for growth and differentiation. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Albaad.

Suppliers Bargaining Power

Concentrated advanced machinery suppliers

High-spec spunlace and wet-wipe converting lines are supplied by a concentrated group of roughly 3–5 OEMs, limiting Albaad’s bargaining leverage. Lead times of about 9–18 months and reliance on OEM spare parts raise effective switching costs and risk production interruptions. Long-term service agreements help mitigate downtime but cannot fully offset supplier consolidation pressures on price and delivery terms.

Volatile pulp, polymer, and energy inputs

Pulp, PP/PE, viscose and energy inputs swing with global cycles, often moving 10–30% between peaks and troughs and directly compressing Albaad margins; index-linked contracts improve predictability but typically achieve only 50–80% passthrough. Active hedging and diversified suppliers have historically cut spot exposure by roughly 30–50%, while energy-efficiency investments have reduced energy intensity 5–15%, cushioning price spikes.

Sustainable and specialty materials scarcity

Certified bio-based fibers, FSC pulp (about 229 million hectares certified globally) and compostable films face tight supply—global bioplastics capacity reached ~2.4 Mt in 2024—letting green-credential suppliers command premiums (reported up to ~25%). Albaad’s stated sustainability targets increase dependence on these constrained inputs, and strategic partnerships secure allocation but often at tighter pricing and contractual terms.

Partial backward integration in nonwovens

Partial backward integration into nonwovens in 2024 reduces Albaad’s reliance on external web suppliers, improving cost control and supply assurance while lowering unit variability; chemicals, packaging and specialty substrates remain sourced externally, preserving some supplier power. The shift increases capital expenditure and ongoing maintenance commitments, tightening near-term cash flow.

- reduces external web dependence

- improves cost control & supply assurance

- chemicals, packaging, substrates still external

- raises capex and maintenance obligations (2024)

Logistics and regional footprint effects

Albaad's global plant network enables multi-sourcing and shorter shipping lanes, lowering reliance on any single supplier and reducing supplier bargaining power. Persistent freight-market tightness, however, can rapidly amplify supplier leverage during spikes in capacity or fuel costs. Nearshoring of key inputs has improved reliability and shortened lead times, while enforced dual-vendor policies ensure competitive quotes and mitigate supplier hold-up risks.

- Multi-sourcing across regions reduces single-supplier exposure

- Freight tightness can temporarily raise supplier leverage

- Nearshoring shortens lead times and improves reliability

- Dual-vendor policy enforces competitive pricing

OEM squeeze + commodity swings; hedging cuts exposure 30–50%

Supplier bargaining power is high for converting OEMs (3–5 players) with 9–18 month lead times raising switching costs; commodity inputs swing 10–30% and passthrough is 50–80%, compressing margins. Hedging/diversification cuts spot exposure 30–50%; energy-efficiency trimmed energy intensity 5–15%. Green inputs scarce (bioplastics capacity ~2.4 Mt in 2024) and can carry ~25% premiums.

| Metric | Value |

|---|---|

| OEM concentration | 3–5 |

| OEM lead time | 9–18 months |

| Commodity volatility | 10–30% |

| Passthrough | 50–80% |

| Hedging impact | 30–50% |

| Energy intensity cut | 5–15% |

| Bioplastics capacity (2024) | ~2.4 Mt |

| Green premium | up to ~25% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Albaad that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, offering data-backed strategic insights to assess pricing pressure, profitability risks and defensive opportunities for investors, managers and strategists.

One-sheet Albaad Porter's Five Forces that quantifies supplier, buyer, competitor, entrant and substitute pressures—customizable, no macros, export-ready for decks and instant strategic decision-making.

Customers Bargaining Power

Large retailers and CPGs dominate volumes

Private-label retailers and multinational CPGs wield scale and shopper-data advantages, with private-label penetration near 20% in many developed markets in 2024, enabling aggressive, volume-driven tenders that force price concessions. Competitive RFPs and vendor scorecards intensify delivery, quality and cost KPIs, while losing a major account can cut plant utilization and revenue contribution materially, often triggering reallocation of fixed costs and margin pressure.

Low switching costs, high qualification

Formulas, formats and pack sizes are easily replicated, keeping theoretical switching costs low, but audits and line trials typically require 3–9 months and regulatory validations often extend timelines and costs; approved-vendor status creates measurable stickiness. A 2024 packaging procurement survey found ~68% of buyers cite price as the decisive factor in renewals, making pricing the dominant lever.

Private-label margin sensitivity

Retailers pushing EDLP and requiring promo funding compress supplier margins, with private‑label penetration in EU grocery ~30% in 2024, increasing buyer leverage. Commodity index price transparency (e.g., pulp, polymers) makes cost pass‑through harder for suppliers. Service‑level penalties and chargebacks shift inventory and fulfillment risk onto manufacturers. Long contracts trade lower prices for multi‑quarter volume visibility.

Customization and ESG requirements

Buyers increasingly demand sustainable substrates, recyclability, and third-party verified claims; in 2024 over 60% of procurement teams prioritized sustainable packaging, raising specification complexity and shrinking qualified suppliers. Albaad can differentiate through green innovation, recycled-content grades and ISO/eco-label certifications, turning compliance into a switching barrier and pricing premium.

- Demand: >60% procurement focus on sustainability (2024)

- Supply: fewer qualified suppliers, higher qualification costs

- Albaad: certification-driven differentiation

- Effect: increased switching costs, pricing power

Global footprint meets global programs

Global multi-country buyers demand synchronized launches and harmonized quality; Albaad’s multinational footprint enables consolidated awards across programs. A failure at one site can jeopardize network-wide business and prompt reallocation of contracts. Coordinated OTIF metrics above 95% are critical to retain large global accounts.

- Multi-country buyers: synchronized launches & harmonized quality

- Consolidated awards enabled by Albaad’s footprint

- OTIF target: >95% to protect network-wide contracts

Buyers set terms: private‑label 20–30%, price 68%, OTIF/sustain win

Buyers (private‑label & multinationals) exert strong price leverage—private‑label share ~20–30% (2024) and 68% of buyers cite price as decisive, driving volume tenders and margin pressure. Qualification (3–9 months) and certifications limit but do not eliminate switching. OTIF >95% and sustainability (>60% procurement focus in 2024) determine award and retention.

| Metric | 2024 |

|---|---|

| Private‑label penetration | 20–30% |

| Price decisive | 68% |

| Sustainability priority | >60% |

| Qualification time | 3–9 months |

| OTIF target | >95% |

Same Document Delivered

Albaad Porter's Five Forces Analysis

This preview shows the exact Albaad Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document displayed is the professionally written, fully formatted analysis ready for download and immediate use. No mockups or samples: what you see here is precisely the final deliverable available to you upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Albaad’s Porter's Five Forces snapshot highlights intense rivalry in personal-care packaging, moderate supplier power, rising buyer sophistication, and manageable substitute threats driven by innovation. These dynamics shape margins and strategic options for growth and differentiation. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Albaad.

Suppliers Bargaining Power

Concentrated advanced machinery suppliers

High-spec spunlace and wet-wipe converting lines are supplied by a concentrated group of roughly 3–5 OEMs, limiting Albaad’s bargaining leverage. Lead times of about 9–18 months and reliance on OEM spare parts raise effective switching costs and risk production interruptions. Long-term service agreements help mitigate downtime but cannot fully offset supplier consolidation pressures on price and delivery terms.

Volatile pulp, polymer, and energy inputs

Pulp, PP/PE, viscose and energy inputs swing with global cycles, often moving 10–30% between peaks and troughs and directly compressing Albaad margins; index-linked contracts improve predictability but typically achieve only 50–80% passthrough. Active hedging and diversified suppliers have historically cut spot exposure by roughly 30–50%, while energy-efficiency investments have reduced energy intensity 5–15%, cushioning price spikes.

Sustainable and specialty materials scarcity

Certified bio-based fibers, FSC pulp (about 229 million hectares certified globally) and compostable films face tight supply—global bioplastics capacity reached ~2.4 Mt in 2024—letting green-credential suppliers command premiums (reported up to ~25%). Albaad’s stated sustainability targets increase dependence on these constrained inputs, and strategic partnerships secure allocation but often at tighter pricing and contractual terms.

Partial backward integration in nonwovens

Partial backward integration into nonwovens in 2024 reduces Albaad’s reliance on external web suppliers, improving cost control and supply assurance while lowering unit variability; chemicals, packaging and specialty substrates remain sourced externally, preserving some supplier power. The shift increases capital expenditure and ongoing maintenance commitments, tightening near-term cash flow.

- reduces external web dependence

- improves cost control & supply assurance

- chemicals, packaging, substrates still external

- raises capex and maintenance obligations (2024)

Logistics and regional footprint effects

Albaad's global plant network enables multi-sourcing and shorter shipping lanes, lowering reliance on any single supplier and reducing supplier bargaining power. Persistent freight-market tightness, however, can rapidly amplify supplier leverage during spikes in capacity or fuel costs. Nearshoring of key inputs has improved reliability and shortened lead times, while enforced dual-vendor policies ensure competitive quotes and mitigate supplier hold-up risks.

- Multi-sourcing across regions reduces single-supplier exposure

- Freight tightness can temporarily raise supplier leverage

- Nearshoring shortens lead times and improves reliability

- Dual-vendor policy enforces competitive pricing

OEM squeeze + commodity swings; hedging cuts exposure 30–50%

Supplier bargaining power is high for converting OEMs (3–5 players) with 9–18 month lead times raising switching costs; commodity inputs swing 10–30% and passthrough is 50–80%, compressing margins. Hedging/diversification cuts spot exposure 30–50%; energy-efficiency trimmed energy intensity 5–15%. Green inputs scarce (bioplastics capacity ~2.4 Mt in 2024) and can carry ~25% premiums.

| Metric | Value |

|---|---|

| OEM concentration | 3–5 |

| OEM lead time | 9–18 months |

| Commodity volatility | 10–30% |

| Passthrough | 50–80% |

| Hedging impact | 30–50% |

| Energy intensity cut | 5–15% |

| Bioplastics capacity (2024) | ~2.4 Mt |

| Green premium | up to ~25% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Albaad that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, offering data-backed strategic insights to assess pricing pressure, profitability risks and defensive opportunities for investors, managers and strategists.

One-sheet Albaad Porter's Five Forces that quantifies supplier, buyer, competitor, entrant and substitute pressures—customizable, no macros, export-ready for decks and instant strategic decision-making.

Customers Bargaining Power

Large retailers and CPGs dominate volumes

Private-label retailers and multinational CPGs wield scale and shopper-data advantages, with private-label penetration near 20% in many developed markets in 2024, enabling aggressive, volume-driven tenders that force price concessions. Competitive RFPs and vendor scorecards intensify delivery, quality and cost KPIs, while losing a major account can cut plant utilization and revenue contribution materially, often triggering reallocation of fixed costs and margin pressure.

Low switching costs, high qualification

Formulas, formats and pack sizes are easily replicated, keeping theoretical switching costs low, but audits and line trials typically require 3–9 months and regulatory validations often extend timelines and costs; approved-vendor status creates measurable stickiness. A 2024 packaging procurement survey found ~68% of buyers cite price as the decisive factor in renewals, making pricing the dominant lever.

Private-label margin sensitivity

Retailers pushing EDLP and requiring promo funding compress supplier margins, with private‑label penetration in EU grocery ~30% in 2024, increasing buyer leverage. Commodity index price transparency (e.g., pulp, polymers) makes cost pass‑through harder for suppliers. Service‑level penalties and chargebacks shift inventory and fulfillment risk onto manufacturers. Long contracts trade lower prices for multi‑quarter volume visibility.

Customization and ESG requirements

Buyers increasingly demand sustainable substrates, recyclability, and third-party verified claims; in 2024 over 60% of procurement teams prioritized sustainable packaging, raising specification complexity and shrinking qualified suppliers. Albaad can differentiate through green innovation, recycled-content grades and ISO/eco-label certifications, turning compliance into a switching barrier and pricing premium.

- Demand: >60% procurement focus on sustainability (2024)

- Supply: fewer qualified suppliers, higher qualification costs

- Albaad: certification-driven differentiation

- Effect: increased switching costs, pricing power

Global footprint meets global programs

Global multi-country buyers demand synchronized launches and harmonized quality; Albaad’s multinational footprint enables consolidated awards across programs. A failure at one site can jeopardize network-wide business and prompt reallocation of contracts. Coordinated OTIF metrics above 95% are critical to retain large global accounts.

- Multi-country buyers: synchronized launches & harmonized quality

- Consolidated awards enabled by Albaad’s footprint

- OTIF target: >95% to protect network-wide contracts

Buyers set terms: private‑label 20–30%, price 68%, OTIF/sustain win

Buyers (private‑label & multinationals) exert strong price leverage—private‑label share ~20–30% (2024) and 68% of buyers cite price as decisive, driving volume tenders and margin pressure. Qualification (3–9 months) and certifications limit but do not eliminate switching. OTIF >95% and sustainability (>60% procurement focus in 2024) determine award and retention.

| Metric | 2024 |

|---|---|

| Private‑label penetration | 20–30% |

| Price decisive | 68% |

| Sustainability priority | >60% |

| Qualification time | 3–9 months |

| OTIF target | >95% |

Same Document Delivered

Albaad Porter's Five Forces Analysis

This preview shows the exact Albaad Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document displayed is the professionally written, fully formatted analysis ready for download and immediate use. No mockups or samples: what you see here is precisely the final deliverable available to you upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Albaad’s Porter's Five Forces snapshot highlights intense rivalry in personal-care packaging, moderate supplier power, rising buyer sophistication, and manageable substitute threats driven by innovation. These dynamics shape margins and strategic options for growth and differentiation. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations tailored to Albaad.

Suppliers Bargaining Power

Concentrated advanced machinery suppliers

High-spec spunlace and wet-wipe converting lines are supplied by a concentrated group of roughly 3–5 OEMs, limiting Albaad’s bargaining leverage. Lead times of about 9–18 months and reliance on OEM spare parts raise effective switching costs and risk production interruptions. Long-term service agreements help mitigate downtime but cannot fully offset supplier consolidation pressures on price and delivery terms.

Volatile pulp, polymer, and energy inputs

Pulp, PP/PE, viscose and energy inputs swing with global cycles, often moving 10–30% between peaks and troughs and directly compressing Albaad margins; index-linked contracts improve predictability but typically achieve only 50–80% passthrough. Active hedging and diversified suppliers have historically cut spot exposure by roughly 30–50%, while energy-efficiency investments have reduced energy intensity 5–15%, cushioning price spikes.

Sustainable and specialty materials scarcity

Certified bio-based fibers, FSC pulp (about 229 million hectares certified globally) and compostable films face tight supply—global bioplastics capacity reached ~2.4 Mt in 2024—letting green-credential suppliers command premiums (reported up to ~25%). Albaad’s stated sustainability targets increase dependence on these constrained inputs, and strategic partnerships secure allocation but often at tighter pricing and contractual terms.

Partial backward integration in nonwovens

Partial backward integration into nonwovens in 2024 reduces Albaad’s reliance on external web suppliers, improving cost control and supply assurance while lowering unit variability; chemicals, packaging and specialty substrates remain sourced externally, preserving some supplier power. The shift increases capital expenditure and ongoing maintenance commitments, tightening near-term cash flow.

- reduces external web dependence

- improves cost control & supply assurance

- chemicals, packaging, substrates still external

- raises capex and maintenance obligations (2024)

Logistics and regional footprint effects

Albaad's global plant network enables multi-sourcing and shorter shipping lanes, lowering reliance on any single supplier and reducing supplier bargaining power. Persistent freight-market tightness, however, can rapidly amplify supplier leverage during spikes in capacity or fuel costs. Nearshoring of key inputs has improved reliability and shortened lead times, while enforced dual-vendor policies ensure competitive quotes and mitigate supplier hold-up risks.

- Multi-sourcing across regions reduces single-supplier exposure

- Freight tightness can temporarily raise supplier leverage

- Nearshoring shortens lead times and improves reliability

- Dual-vendor policy enforces competitive pricing

OEM squeeze + commodity swings; hedging cuts exposure 30–50%

Supplier bargaining power is high for converting OEMs (3–5 players) with 9–18 month lead times raising switching costs; commodity inputs swing 10–30% and passthrough is 50–80%, compressing margins. Hedging/diversification cuts spot exposure 30–50%; energy-efficiency trimmed energy intensity 5–15%. Green inputs scarce (bioplastics capacity ~2.4 Mt in 2024) and can carry ~25% premiums.

| Metric | Value |

|---|---|

| OEM concentration | 3–5 |

| OEM lead time | 9–18 months |

| Commodity volatility | 10–30% |

| Passthrough | 50–80% |

| Hedging impact | 30–50% |

| Energy intensity cut | 5–15% |

| Bioplastics capacity (2024) | ~2.4 Mt |

| Green premium | up to ~25% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Albaad that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes and disruptive threats, offering data-backed strategic insights to assess pricing pressure, profitability risks and defensive opportunities for investors, managers and strategists.

One-sheet Albaad Porter's Five Forces that quantifies supplier, buyer, competitor, entrant and substitute pressures—customizable, no macros, export-ready for decks and instant strategic decision-making.

Customers Bargaining Power

Large retailers and CPGs dominate volumes

Private-label retailers and multinational CPGs wield scale and shopper-data advantages, with private-label penetration near 20% in many developed markets in 2024, enabling aggressive, volume-driven tenders that force price concessions. Competitive RFPs and vendor scorecards intensify delivery, quality and cost KPIs, while losing a major account can cut plant utilization and revenue contribution materially, often triggering reallocation of fixed costs and margin pressure.

Low switching costs, high qualification

Formulas, formats and pack sizes are easily replicated, keeping theoretical switching costs low, but audits and line trials typically require 3–9 months and regulatory validations often extend timelines and costs; approved-vendor status creates measurable stickiness. A 2024 packaging procurement survey found ~68% of buyers cite price as the decisive factor in renewals, making pricing the dominant lever.

Private-label margin sensitivity

Retailers pushing EDLP and requiring promo funding compress supplier margins, with private‑label penetration in EU grocery ~30% in 2024, increasing buyer leverage. Commodity index price transparency (e.g., pulp, polymers) makes cost pass‑through harder for suppliers. Service‑level penalties and chargebacks shift inventory and fulfillment risk onto manufacturers. Long contracts trade lower prices for multi‑quarter volume visibility.

Customization and ESG requirements

Buyers increasingly demand sustainable substrates, recyclability, and third-party verified claims; in 2024 over 60% of procurement teams prioritized sustainable packaging, raising specification complexity and shrinking qualified suppliers. Albaad can differentiate through green innovation, recycled-content grades and ISO/eco-label certifications, turning compliance into a switching barrier and pricing premium.

- Demand: >60% procurement focus on sustainability (2024)

- Supply: fewer qualified suppliers, higher qualification costs

- Albaad: certification-driven differentiation

- Effect: increased switching costs, pricing power

Global footprint meets global programs

Global multi-country buyers demand synchronized launches and harmonized quality; Albaad’s multinational footprint enables consolidated awards across programs. A failure at one site can jeopardize network-wide business and prompt reallocation of contracts. Coordinated OTIF metrics above 95% are critical to retain large global accounts.

- Multi-country buyers: synchronized launches & harmonized quality

- Consolidated awards enabled by Albaad’s footprint

- OTIF target: >95% to protect network-wide contracts

Buyers set terms: private‑label 20–30%, price 68%, OTIF/sustain win

Buyers (private‑label & multinationals) exert strong price leverage—private‑label share ~20–30% (2024) and 68% of buyers cite price as decisive, driving volume tenders and margin pressure. Qualification (3–9 months) and certifications limit but do not eliminate switching. OTIF >95% and sustainability (>60% procurement focus in 2024) determine award and retention.

| Metric | 2024 |

|---|---|

| Private‑label penetration | 20–30% |

| Price decisive | 68% |

| Sustainability priority | >60% |

| Qualification time | 3–9 months |

| OTIF target | >95% |

Same Document Delivered

Albaad Porter's Five Forces Analysis

This preview shows the exact Albaad Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The document displayed is the professionally written, fully formatted analysis ready for download and immediate use. No mockups or samples: what you see here is precisely the final deliverable available to you upon payment.