Albemarle Boston Consulting Group Matrix

Actionable Strategy Starts Here

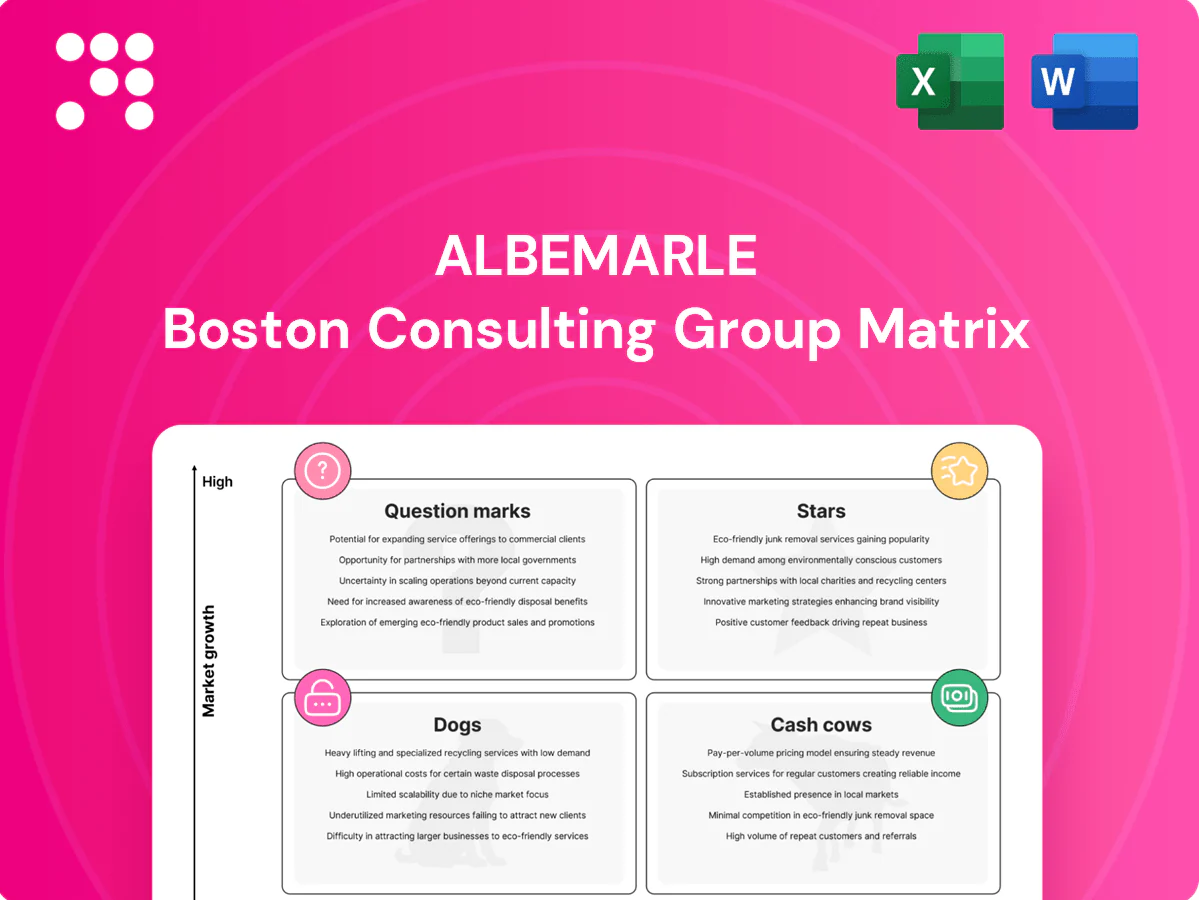

Curious where Albemarle’s products sit — Stars, Cash Cows, Dogs or Question Marks? This snapshot teases the story; the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed recommendations, and tactical moves you can act on now. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary and start reallocating capital smarter today.

Stars

Lithium hydroxide for EV batteries

Albemarle leads the battery-grade lithium hydroxide market, supplying top EV cell makers and capturing high market share amid surging EV demand. High-growth positioning with locked long-term offtakes supports rapid capacity expansion, requiring heavy capital deployment. The business is capital-intensive but generates a reinforcing supply-of-molecules flywheel; continued investment is necessary as the lithium hydroxide market tightens.

Integrated spodumene-to-chemicals network

Owning spodumene mines plus conversion plants gives Albemarle cost and supply security in a fast-growing market, with lithium demand projected at roughly 25% CAGR to 2030 (BNEF 2024). Vertical integration is a defensible edge as competitors focus downstream on molecules, preserving margin capture. Capacity ramps are cash-hungry but strategic, requiring multi-hundred-million-dollar investments to scale. Hold share through reliability and speed to qualify customers.

OEM and cell-maker long-term contracts

Multi‑year OEM and cell‑maker contracts anchor volume for Albemarle, reinforcing its position as the world’s largest lithium producer in 2024 while the EV battery market continues expanding. Pricing formulas and index links in these deals smooth short‑term volatility yet preserve upside participation as spot prices rise. Such long‑standing relationships cement leadership status and market access. Protect them through on‑time delivery and continual quality wins.

High-purity lithium for energy storage

In 2024 grid-scale storage deployments rose sharply alongside EV growth, and Albemarle’s high-purity lithium—holding roughly 20% global lithium share in 2024—travels well between both markets due to identical chemistry and tight purity specs. Adjacent use-case adoption is faster, share is strong where reliability matters, and continued product qualification will lock in the surge.

- Market tag: 20% global lithium share (2024)

- Demand tag: grid + EV convergence accelerates adoption

- Strategy tag: qualify products fast to secure customers

Premium technical support and qualification moat

Qualification cycles in batteries often run 12–24 months, and Albemarle’s lab-to-line technical support materially shortens OEM validation time and lowers program risk, creating customer stickiness and higher share in a fast-growing EV battery market. Maintaining on-site labs and engineering teams costs millions annually but preserves long-term contracts and premium pricing.

- 12–24 months qualification cycle

- Reduces OEM validation risk

- Creates customer stickiness

- Costs millions to maintain

Leading lithium producer, ~20% share; ~25% CAGR to 2030

Albemarle is a Star: #1 global lithium producer in 2024 with ~20% share, high-growth market exposure (BNEF 2024 ~25% CAGR to 2030) and long-term offtakes driving rapid capacity buildouts that require multi-hundred-million-dollar capex and sustain premium pricing via tight supply. Fast qualification (12–24 months) and vertical integration secure customers and margins.

| Metric | Value |

|---|---|

| Global lithium share (2024) | ~20% |

| Demand CAGR to 2030 (BNEF 2024) | ~25% |

| Qualification cycle | 12–24 months |

| Capex scale | Multi-hundred-million $ |

What is included in the product

In-depth BCG Matrix review of Albemarle's portfolio, spotlighting Stars, Cash Cows, Question Marks, Dogs and recommended investment moves.

One-page Albemarle BCG matrix highlighting cash cows and stars to simplify portfolio decisions for execs.

Cash Cows

Bromine flame retardants portfolio

Bromine flame retardants sit in Albemarle’s Cash Cows: serving large, mature end markets—construction, electronics and auto interiors—within a global flame retardants market estimated at $4.2 billion in 2024. High share and stable EBITDA margins near 20% produced steady cash flow, with the segment contributing roughly $1.2 billion in 2024 revenue. Modest capex keeps assets productive, so focus is on milking cash while incrementally optimizing plants and product mix.

Clear brine fluids and bromine specialties

Oilfield and industrial uses of clear brine fluids and bromine specialties are not hyper-growth but provide steady, low-single-digit volume growth and predictable demand. Albemarle’s process know-how and secure brine access keep unit costs low, supporting >20% EBITDA margins and cash generation that exceeded reinvestment needs; these lines contributed roughly 15% of 2024 revenue (~$1.1B). Management focuses on yield, uptime, and contract renewals to preserve cash flow.

Aftermarket catalysts services and licensing

Aftermarket services, tech support, and licensing generated steady cash flows for Albemarle, representing a single-digit percent of revenue in 2024 and smoothing earnings in a slow market. High switching costs from technical integration and proprietary formulations bolster customer retention and recurring income. Growth is limited but margins remain stable, so management should maintain capabilities and avoid heavy expansion capex.

Legacy consumer and industrial additives

Legacy consumer and industrial additives are entrenched SKUs with predictable reorders and high repeat purchase rates, delivering steady, cash-positive margins for Albemarle (ticker ALB). Low promotional spend and minimal commercial complexity translate to low drama, enabling focus on lean operations and strict price discipline to protect margins amid volatility in specialty chemical markets.

- Entrenched SKUs

- Predictable reorders

- Low promotion, high repeat

- Cash-positive & low drama

- Focus: operational efficiency

- Focus: price discipline

Supply chain and logistics advantages

Albemarle leverages a global footprint across Chile, the US and Australia to drive sourcing scale and lower per-unit logistics in mature chemicals and bromine lines, delivering steady margin and cash generation even as lithium markets cycle. Not glamorous but highly effective, the integrated network cut supplier disruption days in recent 2024 reporting periods and improved working-capital terms, supporting free cash flow. Continuous network fine-tuning—warehouses, long-term contracts, modal mix—yields incremental cost wins that sustain cash-cow performance.

Cash cows: bromine FR and clear brines driving ~20% EBITDA on $2.3B revenue

Cash cows: bromine flame retardants, clear brines, services and legacy additives generated stable cash; 2024 revenue ~ $2.3B (flame retardants $1.2B; brines $1.1B), EBITDA ~20%+, low capex and improved working capital supporting recurring cash generation.

| Segment | 2024 Rev | EBITDA |

|---|---|---|

| Bromine FR | $1.2B | ~20% |

| Clear brines | $1.1B | ≥20% |

| Services/legacy | Single-digit % of rev | Stable |

Delivered as Shown

Albemarle BCG Matrix

The file you're previewing on this page is the final Albemarle BCG Matrix you'll receive after purchase. No watermarks, no demo notes—just a fully formatted, analysis-ready report designed for strategic clarity. This exact document is ready for editing, printing, or presenting to investors and your team. Delivered instantly after purchase, it’s crafted to plug straight into your planning with no surprises.

Actionable Strategy Starts Here

Curious where Albemarle’s products sit — Stars, Cash Cows, Dogs or Question Marks? This snapshot teases the story; the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed recommendations, and tactical moves you can act on now. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary and start reallocating capital smarter today.

Stars

Lithium hydroxide for EV batteries

Albemarle leads the battery-grade lithium hydroxide market, supplying top EV cell makers and capturing high market share amid surging EV demand. High-growth positioning with locked long-term offtakes supports rapid capacity expansion, requiring heavy capital deployment. The business is capital-intensive but generates a reinforcing supply-of-molecules flywheel; continued investment is necessary as the lithium hydroxide market tightens.

Integrated spodumene-to-chemicals network

Owning spodumene mines plus conversion plants gives Albemarle cost and supply security in a fast-growing market, with lithium demand projected at roughly 25% CAGR to 2030 (BNEF 2024). Vertical integration is a defensible edge as competitors focus downstream on molecules, preserving margin capture. Capacity ramps are cash-hungry but strategic, requiring multi-hundred-million-dollar investments to scale. Hold share through reliability and speed to qualify customers.

OEM and cell-maker long-term contracts

Multi‑year OEM and cell‑maker contracts anchor volume for Albemarle, reinforcing its position as the world’s largest lithium producer in 2024 while the EV battery market continues expanding. Pricing formulas and index links in these deals smooth short‑term volatility yet preserve upside participation as spot prices rise. Such long‑standing relationships cement leadership status and market access. Protect them through on‑time delivery and continual quality wins.

High-purity lithium for energy storage

In 2024 grid-scale storage deployments rose sharply alongside EV growth, and Albemarle’s high-purity lithium—holding roughly 20% global lithium share in 2024—travels well between both markets due to identical chemistry and tight purity specs. Adjacent use-case adoption is faster, share is strong where reliability matters, and continued product qualification will lock in the surge.

- Market tag: 20% global lithium share (2024)

- Demand tag: grid + EV convergence accelerates adoption

- Strategy tag: qualify products fast to secure customers

Premium technical support and qualification moat

Qualification cycles in batteries often run 12–24 months, and Albemarle’s lab-to-line technical support materially shortens OEM validation time and lowers program risk, creating customer stickiness and higher share in a fast-growing EV battery market. Maintaining on-site labs and engineering teams costs millions annually but preserves long-term contracts and premium pricing.

- 12–24 months qualification cycle

- Reduces OEM validation risk

- Creates customer stickiness

- Costs millions to maintain

Leading lithium producer, ~20% share; ~25% CAGR to 2030

Albemarle is a Star: #1 global lithium producer in 2024 with ~20% share, high-growth market exposure (BNEF 2024 ~25% CAGR to 2030) and long-term offtakes driving rapid capacity buildouts that require multi-hundred-million-dollar capex and sustain premium pricing via tight supply. Fast qualification (12–24 months) and vertical integration secure customers and margins.

| Metric | Value |

|---|---|

| Global lithium share (2024) | ~20% |

| Demand CAGR to 2030 (BNEF 2024) | ~25% |

| Qualification cycle | 12–24 months |

| Capex scale | Multi-hundred-million $ |

What is included in the product

In-depth BCG Matrix review of Albemarle's portfolio, spotlighting Stars, Cash Cows, Question Marks, Dogs and recommended investment moves.

One-page Albemarle BCG matrix highlighting cash cows and stars to simplify portfolio decisions for execs.

Cash Cows

Bromine flame retardants portfolio

Bromine flame retardants sit in Albemarle’s Cash Cows: serving large, mature end markets—construction, electronics and auto interiors—within a global flame retardants market estimated at $4.2 billion in 2024. High share and stable EBITDA margins near 20% produced steady cash flow, with the segment contributing roughly $1.2 billion in 2024 revenue. Modest capex keeps assets productive, so focus is on milking cash while incrementally optimizing plants and product mix.

Clear brine fluids and bromine specialties

Oilfield and industrial uses of clear brine fluids and bromine specialties are not hyper-growth but provide steady, low-single-digit volume growth and predictable demand. Albemarle’s process know-how and secure brine access keep unit costs low, supporting >20% EBITDA margins and cash generation that exceeded reinvestment needs; these lines contributed roughly 15% of 2024 revenue (~$1.1B). Management focuses on yield, uptime, and contract renewals to preserve cash flow.

Aftermarket catalysts services and licensing

Aftermarket services, tech support, and licensing generated steady cash flows for Albemarle, representing a single-digit percent of revenue in 2024 and smoothing earnings in a slow market. High switching costs from technical integration and proprietary formulations bolster customer retention and recurring income. Growth is limited but margins remain stable, so management should maintain capabilities and avoid heavy expansion capex.

Legacy consumer and industrial additives

Legacy consumer and industrial additives are entrenched SKUs with predictable reorders and high repeat purchase rates, delivering steady, cash-positive margins for Albemarle (ticker ALB). Low promotional spend and minimal commercial complexity translate to low drama, enabling focus on lean operations and strict price discipline to protect margins amid volatility in specialty chemical markets.

- Entrenched SKUs

- Predictable reorders

- Low promotion, high repeat

- Cash-positive & low drama

- Focus: operational efficiency

- Focus: price discipline

Supply chain and logistics advantages

Albemarle leverages a global footprint across Chile, the US and Australia to drive sourcing scale and lower per-unit logistics in mature chemicals and bromine lines, delivering steady margin and cash generation even as lithium markets cycle. Not glamorous but highly effective, the integrated network cut supplier disruption days in recent 2024 reporting periods and improved working-capital terms, supporting free cash flow. Continuous network fine-tuning—warehouses, long-term contracts, modal mix—yields incremental cost wins that sustain cash-cow performance.

Cash cows: bromine FR and clear brines driving ~20% EBITDA on $2.3B revenue

Cash cows: bromine flame retardants, clear brines, services and legacy additives generated stable cash; 2024 revenue ~ $2.3B (flame retardants $1.2B; brines $1.1B), EBITDA ~20%+, low capex and improved working capital supporting recurring cash generation.

| Segment | 2024 Rev | EBITDA |

|---|---|---|

| Bromine FR | $1.2B | ~20% |

| Clear brines | $1.1B | ≥20% |

| Services/legacy | Single-digit % of rev | Stable |

Delivered as Shown

Albemarle BCG Matrix

The file you're previewing on this page is the final Albemarle BCG Matrix you'll receive after purchase. No watermarks, no demo notes—just a fully formatted, analysis-ready report designed for strategic clarity. This exact document is ready for editing, printing, or presenting to investors and your team. Delivered instantly after purchase, it’s crafted to plug straight into your planning with no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Curious where Albemarle’s products sit — Stars, Cash Cows, Dogs or Question Marks? This snapshot teases the story; the full BCG Matrix gives quadrant-by-quadrant clarity, data-backed recommendations, and tactical moves you can act on now. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary and start reallocating capital smarter today.

Stars

Lithium hydroxide for EV batteries

Albemarle leads the battery-grade lithium hydroxide market, supplying top EV cell makers and capturing high market share amid surging EV demand. High-growth positioning with locked long-term offtakes supports rapid capacity expansion, requiring heavy capital deployment. The business is capital-intensive but generates a reinforcing supply-of-molecules flywheel; continued investment is necessary as the lithium hydroxide market tightens.

Integrated spodumene-to-chemicals network

Owning spodumene mines plus conversion plants gives Albemarle cost and supply security in a fast-growing market, with lithium demand projected at roughly 25% CAGR to 2030 (BNEF 2024). Vertical integration is a defensible edge as competitors focus downstream on molecules, preserving margin capture. Capacity ramps are cash-hungry but strategic, requiring multi-hundred-million-dollar investments to scale. Hold share through reliability and speed to qualify customers.

OEM and cell-maker long-term contracts

Multi‑year OEM and cell‑maker contracts anchor volume for Albemarle, reinforcing its position as the world’s largest lithium producer in 2024 while the EV battery market continues expanding. Pricing formulas and index links in these deals smooth short‑term volatility yet preserve upside participation as spot prices rise. Such long‑standing relationships cement leadership status and market access. Protect them through on‑time delivery and continual quality wins.

High-purity lithium for energy storage

In 2024 grid-scale storage deployments rose sharply alongside EV growth, and Albemarle’s high-purity lithium—holding roughly 20% global lithium share in 2024—travels well between both markets due to identical chemistry and tight purity specs. Adjacent use-case adoption is faster, share is strong where reliability matters, and continued product qualification will lock in the surge.

- Market tag: 20% global lithium share (2024)

- Demand tag: grid + EV convergence accelerates adoption

- Strategy tag: qualify products fast to secure customers

Premium technical support and qualification moat

Qualification cycles in batteries often run 12–24 months, and Albemarle’s lab-to-line technical support materially shortens OEM validation time and lowers program risk, creating customer stickiness and higher share in a fast-growing EV battery market. Maintaining on-site labs and engineering teams costs millions annually but preserves long-term contracts and premium pricing.

- 12–24 months qualification cycle

- Reduces OEM validation risk

- Creates customer stickiness

- Costs millions to maintain

Leading lithium producer, ~20% share; ~25% CAGR to 2030

Albemarle is a Star: #1 global lithium producer in 2024 with ~20% share, high-growth market exposure (BNEF 2024 ~25% CAGR to 2030) and long-term offtakes driving rapid capacity buildouts that require multi-hundred-million-dollar capex and sustain premium pricing via tight supply. Fast qualification (12–24 months) and vertical integration secure customers and margins.

| Metric | Value |

|---|---|

| Global lithium share (2024) | ~20% |

| Demand CAGR to 2030 (BNEF 2024) | ~25% |

| Qualification cycle | 12–24 months |

| Capex scale | Multi-hundred-million $ |

What is included in the product

In-depth BCG Matrix review of Albemarle's portfolio, spotlighting Stars, Cash Cows, Question Marks, Dogs and recommended investment moves.

One-page Albemarle BCG matrix highlighting cash cows and stars to simplify portfolio decisions for execs.

Cash Cows

Bromine flame retardants portfolio

Bromine flame retardants sit in Albemarle’s Cash Cows: serving large, mature end markets—construction, electronics and auto interiors—within a global flame retardants market estimated at $4.2 billion in 2024. High share and stable EBITDA margins near 20% produced steady cash flow, with the segment contributing roughly $1.2 billion in 2024 revenue. Modest capex keeps assets productive, so focus is on milking cash while incrementally optimizing plants and product mix.

Clear brine fluids and bromine specialties

Oilfield and industrial uses of clear brine fluids and bromine specialties are not hyper-growth but provide steady, low-single-digit volume growth and predictable demand. Albemarle’s process know-how and secure brine access keep unit costs low, supporting >20% EBITDA margins and cash generation that exceeded reinvestment needs; these lines contributed roughly 15% of 2024 revenue (~$1.1B). Management focuses on yield, uptime, and contract renewals to preserve cash flow.

Aftermarket catalysts services and licensing

Aftermarket services, tech support, and licensing generated steady cash flows for Albemarle, representing a single-digit percent of revenue in 2024 and smoothing earnings in a slow market. High switching costs from technical integration and proprietary formulations bolster customer retention and recurring income. Growth is limited but margins remain stable, so management should maintain capabilities and avoid heavy expansion capex.

Legacy consumer and industrial additives

Legacy consumer and industrial additives are entrenched SKUs with predictable reorders and high repeat purchase rates, delivering steady, cash-positive margins for Albemarle (ticker ALB). Low promotional spend and minimal commercial complexity translate to low drama, enabling focus on lean operations and strict price discipline to protect margins amid volatility in specialty chemical markets.

- Entrenched SKUs

- Predictable reorders

- Low promotion, high repeat

- Cash-positive & low drama

- Focus: operational efficiency

- Focus: price discipline

Supply chain and logistics advantages

Albemarle leverages a global footprint across Chile, the US and Australia to drive sourcing scale and lower per-unit logistics in mature chemicals and bromine lines, delivering steady margin and cash generation even as lithium markets cycle. Not glamorous but highly effective, the integrated network cut supplier disruption days in recent 2024 reporting periods and improved working-capital terms, supporting free cash flow. Continuous network fine-tuning—warehouses, long-term contracts, modal mix—yields incremental cost wins that sustain cash-cow performance.

Cash cows: bromine FR and clear brines driving ~20% EBITDA on $2.3B revenue

Cash cows: bromine flame retardants, clear brines, services and legacy additives generated stable cash; 2024 revenue ~ $2.3B (flame retardants $1.2B; brines $1.1B), EBITDA ~20%+, low capex and improved working capital supporting recurring cash generation.

| Segment | 2024 Rev | EBITDA |

|---|---|---|

| Bromine FR | $1.2B | ~20% |

| Clear brines | $1.1B | ≥20% |

| Services/legacy | Single-digit % of rev | Stable |

Delivered as Shown

Albemarle BCG Matrix

The file you're previewing on this page is the final Albemarle BCG Matrix you'll receive after purchase. No watermarks, no demo notes—just a fully formatted, analysis-ready report designed for strategic clarity. This exact document is ready for editing, printing, or presenting to investors and your team. Delivered instantly after purchase, it’s crafted to plug straight into your planning with no surprises.