Albemarle Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

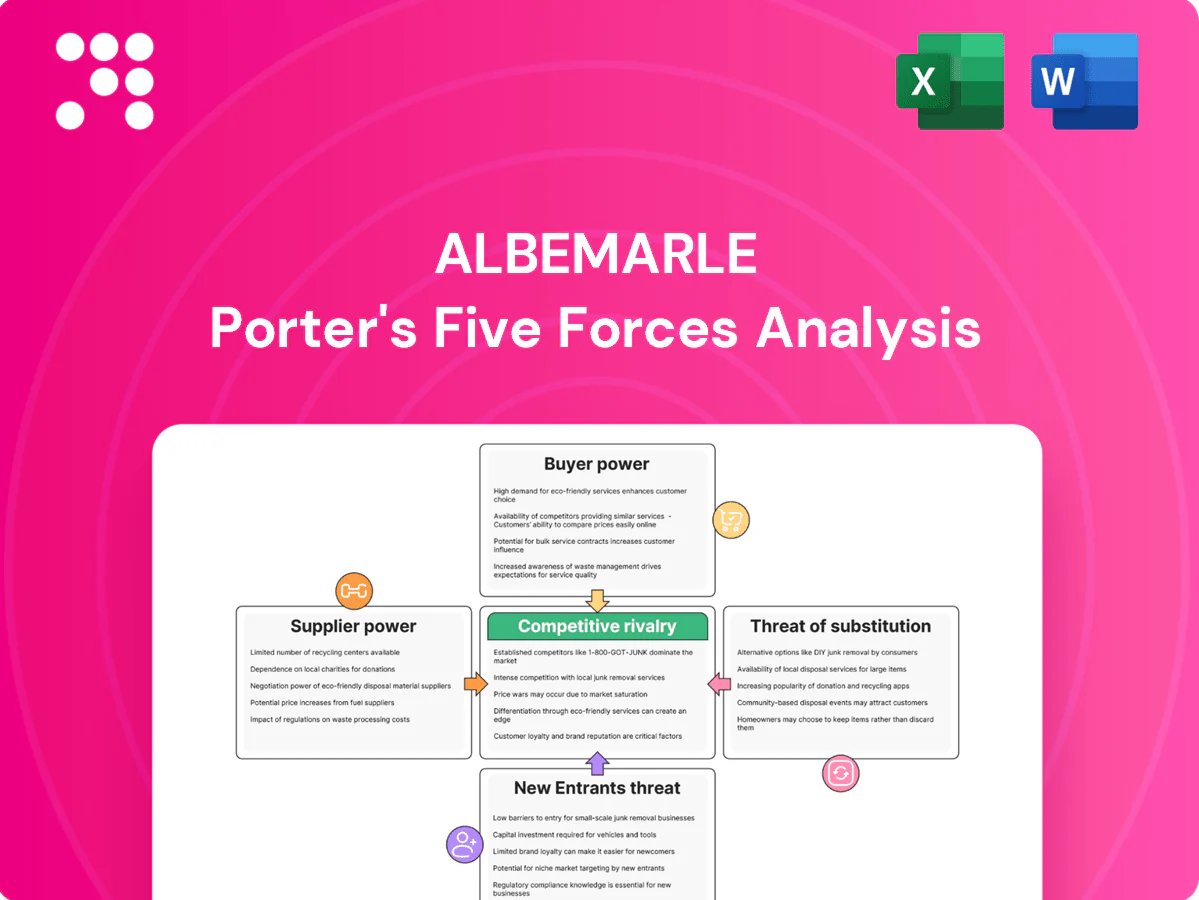

Albemarle's Porter's Five Forces Analysis highlights intense supplier power, moderate buyer leverage, high industry rivalry, limited substitute threats, and entry barriers driven by scale and regulation. This snapshot shows where margin pressure and strategic opportunity intersect. Unlock the full report for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Resource concession and royalty gatekeepers

Access to brine fields and hard‑rock deposits is controlled by governments and a handful of leaseholders (top 3 operators dominate key basins), giving them leverage over royalties, water rights and operating terms. Policy shifts in 2024 in Chile, the U.S. or Australia can alter cost structures rapidly and materially. Albemarle’s own material resource ownership tempers but does not eliminate exposure. Negotiation outcomes directly affect margins and expansion timing.

Critical reagents and energy inputs

Lithium conversion relies on sulfuric acid, soda ash, lime and large electricity/steam inputs, creating exposure to chemical and power suppliers; reagents and energy have been reported to represent up to 30% of conversion operating costs. Regional energy price spikes have raised unit costs materially, keeping power price volatility a key input risk. Long-term supply contracts and on-site utilities reduce but do not fully hedge volatility; renewables sourcing improves resilience but requires upfront capital.

Specialized equipment and EPC capacity

Conversion plants, bromine assets and catalyst lines require custom equipment, EPC services and specialized maintenance expertise, concentrating supplier power. Tight vendor capacity and long lead times can delay projects and inflate capex, while Albemarle’s scale and long-term relationships help secure procurement slots. Ongoing global buildouts strain supply chains, and OEM reliability directly shapes production ramp profiles and timing risk.

Third‑party spodumene feedstock dependence

Even with owned mines Albemarle supplements feedstock with third‑party spodumene, exposing it to miners’ pricing and quality terms; spodumene prices eased from peaks >US$4,500/t in 2022 to roughly US$1,500/t in 2024, prompting miners to seek price floors while buyers face rising premiums and index‑linking when markets tighten.

- Qualification constraints reduce switching flexibility

- Contract optionality and diversification balance cost and continuity

- Spot vs long‑term mix drives margin volatility

Skilled labor and local stakeholders

Engineering talent shortages and unionized workforces materially affect Albemarle’s operating continuity and costs; tight 2024 labor markets (US unemployment ~3.9%) and rising ESG mandates boost bargaining power of skilled workers and community stakeholders, who can demand local hiring, supplier sourcing and environmental investments that raise capex and OPEX.

- Engineering talent: constrained supply raises wages and project delays

- Unionized labor: higher negotiation leverage on pay/conditions

- Social license: local spend and environmental mandates increase compliance costs

- Engagement: lowers disruption risk but adds recurring expenses

Supply squeeze lifts unit costs - reagents ~30%, spodumene US$1,500/t, labor tight

Suppliers wield moderate-to-high power: reagents and energy can be ~30% of conversion costs and regional power spikes raise unit costs materially. Spodumene spot fell from >US$4,500/t in 2022 to ~US$1,500/t in 2024, but miners push price floors and indexation. EPC, OEM and skilled labor shortages (US unemployment ~3.9% in 2024) cause lead-time and wage pressure.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reagents/Energy | ~30% conversion cost | Margin sensitivity |

| Spodumene | ~US$1,500/t | Feedstock price risk |

| EPC/OEM/Labor | Long leads; unemployment ~3.9% | Capex delays, higher wages |

What is included in the product

Tailored Porter's Five Forces analysis for Albemarle that uncovers competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market position.

A one-sheet Porter’s Five Forces analysis for Albemarle that distills competitive pressure, supplier/customer leverage, substitution and entry threats into a deck-ready summary—easy to update with fresh lithium-market data or scenario tabs.

Customers Bargaining Power

Concentrated battery and auto OEM buyers

A handful of cathode makers, battery giants and automakers purchase the bulk of lithium, giving them strong negotiating power; CATL alone held about 35% of global EV battery capacity in 2024 (SNE Research). These buyers increasingly push index-linked or floor/ceiling contracts, trading multi-year volume commitments for pricing concessions and supply security. Ongoing consolidation among buyers amplifies their leverage, especially in down cycles.

High qualification and switching costs

Battery-grade lithium and catalysts require stringent qualification cycles often taking 6–12 months, raising switching costs and protecting incumbents; buyers factor in requalification delays and potential performance variance. Spot lithium carbonate prices were down over 60% from 2022 peaks by 2024, which tempers but does not eliminate pricing power for premium specs. In oversupply phases buyers still extract rebates or push mix optimization to reduce costs.

Price transparency and spot exposure

LME launched tradable lithium contracts in 2023 and spot indices such as Fastmarkets and S&P Global increased market transparency, boosting buyer negotiation leverage. During 2023–24 price corrections buyers pressured sellers to reprice toward spot. Albemarle offsets by retaining long-term contracted volumes and quality premiums, structuring contracts to smooth volatility while preserving market share.

Product performance sensitivity

Customers of Albemarle are highly sensitive to product performance—EV range and battery safety hinge on lithium purity and consistent cathode/cell chemistry, with 2024 global EV sales reported at about 13–14 million units, raising demand for high-quality feedstocks.

Reliable delivery of specs drives customer stickiness and allows performance-linked premiums; failures in purity or catalyst yield can trigger rapid volume shifts despite material switching costs.

- EV range sensitivity: impacts purchasing and warranty exposure

- Safety & purity: directly tied to battery performance and recalls

- Specification reliability: increases contract tenure and premium pricing

- Failures: can cause quick customer volume migration despite switching frictions

Portfolio diversification by customers

OEMs in 2024 increasingly qualified multiple suppliers and chemistries (LFP vs high-nickel) to mitigate supply risk and cost, raising their bargaining leverage during sourcing cycles. Albemarle must compete on total cost, ESG credentials and multi-region reliability as customers shift chemistry mixes and suppliers. Multi-year, multi-plant approvals (commonly 3–5 years) remain Albemarle’s primary defense to retain share.

- OEM diversification of chemistries (2024: broader LFP uptake by Tesla/Chinese OEMs)

- Higher bargaining leverage during sourcing cycles

- Albemarle must win on cost, ESG, reliability

- Multi-year/multi-plant approvals = key switching cost

Buyer concentration boosts negotiating power; spot lithium down ~60%

Concentrated buyers (CATL ~35% EV battery capacity in 2024) wield strong price leverage, using index-linked and floor/ceiling deals; spot lithium fell ~60% from 2022 peaks by 2024, strengthening buyer negotiating power. Qualification lags (6–12 months) and multi-year approvals preserve supplier stickiness, but OEMs qualifying multiple chemistries raise sourcing leverage.

| Metric | 2024 value | Implication |

|---|---|---|

| CATL share | ~35% | Buyer concentration |

| Spot price change vs 2022 | −~60% | Buyer pricing power |

| Global EV sales | ~13.5m units | Demand for high-quality lithium |

Preview Before You Purchase

Albemarle Porter's Five Forces Analysis

This preview displays the exact Albemarle Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use the moment you complete payment. What you see is exactly what you get.

A Must-Have Tool for Decision-Makers

Albemarle's Porter's Five Forces Analysis highlights intense supplier power, moderate buyer leverage, high industry rivalry, limited substitute threats, and entry barriers driven by scale and regulation. This snapshot shows where margin pressure and strategic opportunity intersect. Unlock the full report for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Resource concession and royalty gatekeepers

Access to brine fields and hard‑rock deposits is controlled by governments and a handful of leaseholders (top 3 operators dominate key basins), giving them leverage over royalties, water rights and operating terms. Policy shifts in 2024 in Chile, the U.S. or Australia can alter cost structures rapidly and materially. Albemarle’s own material resource ownership tempers but does not eliminate exposure. Negotiation outcomes directly affect margins and expansion timing.

Critical reagents and energy inputs

Lithium conversion relies on sulfuric acid, soda ash, lime and large electricity/steam inputs, creating exposure to chemical and power suppliers; reagents and energy have been reported to represent up to 30% of conversion operating costs. Regional energy price spikes have raised unit costs materially, keeping power price volatility a key input risk. Long-term supply contracts and on-site utilities reduce but do not fully hedge volatility; renewables sourcing improves resilience but requires upfront capital.

Specialized equipment and EPC capacity

Conversion plants, bromine assets and catalyst lines require custom equipment, EPC services and specialized maintenance expertise, concentrating supplier power. Tight vendor capacity and long lead times can delay projects and inflate capex, while Albemarle’s scale and long-term relationships help secure procurement slots. Ongoing global buildouts strain supply chains, and OEM reliability directly shapes production ramp profiles and timing risk.

Third‑party spodumene feedstock dependence

Even with owned mines Albemarle supplements feedstock with third‑party spodumene, exposing it to miners’ pricing and quality terms; spodumene prices eased from peaks >US$4,500/t in 2022 to roughly US$1,500/t in 2024, prompting miners to seek price floors while buyers face rising premiums and index‑linking when markets tighten.

- Qualification constraints reduce switching flexibility

- Contract optionality and diversification balance cost and continuity

- Spot vs long‑term mix drives margin volatility

Skilled labor and local stakeholders

Engineering talent shortages and unionized workforces materially affect Albemarle’s operating continuity and costs; tight 2024 labor markets (US unemployment ~3.9%) and rising ESG mandates boost bargaining power of skilled workers and community stakeholders, who can demand local hiring, supplier sourcing and environmental investments that raise capex and OPEX.

- Engineering talent: constrained supply raises wages and project delays

- Unionized labor: higher negotiation leverage on pay/conditions

- Social license: local spend and environmental mandates increase compliance costs

- Engagement: lowers disruption risk but adds recurring expenses

Supply squeeze lifts unit costs - reagents ~30%, spodumene US$1,500/t, labor tight

Suppliers wield moderate-to-high power: reagents and energy can be ~30% of conversion costs and regional power spikes raise unit costs materially. Spodumene spot fell from >US$4,500/t in 2022 to ~US$1,500/t in 2024, but miners push price floors and indexation. EPC, OEM and skilled labor shortages (US unemployment ~3.9% in 2024) cause lead-time and wage pressure.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reagents/Energy | ~30% conversion cost | Margin sensitivity |

| Spodumene | ~US$1,500/t | Feedstock price risk |

| EPC/OEM/Labor | Long leads; unemployment ~3.9% | Capex delays, higher wages |

What is included in the product

Tailored Porter's Five Forces analysis for Albemarle that uncovers competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market position.

A one-sheet Porter’s Five Forces analysis for Albemarle that distills competitive pressure, supplier/customer leverage, substitution and entry threats into a deck-ready summary—easy to update with fresh lithium-market data or scenario tabs.

Customers Bargaining Power

Concentrated battery and auto OEM buyers

A handful of cathode makers, battery giants and automakers purchase the bulk of lithium, giving them strong negotiating power; CATL alone held about 35% of global EV battery capacity in 2024 (SNE Research). These buyers increasingly push index-linked or floor/ceiling contracts, trading multi-year volume commitments for pricing concessions and supply security. Ongoing consolidation among buyers amplifies their leverage, especially in down cycles.

High qualification and switching costs

Battery-grade lithium and catalysts require stringent qualification cycles often taking 6–12 months, raising switching costs and protecting incumbents; buyers factor in requalification delays and potential performance variance. Spot lithium carbonate prices were down over 60% from 2022 peaks by 2024, which tempers but does not eliminate pricing power for premium specs. In oversupply phases buyers still extract rebates or push mix optimization to reduce costs.

Price transparency and spot exposure

LME launched tradable lithium contracts in 2023 and spot indices such as Fastmarkets and S&P Global increased market transparency, boosting buyer negotiation leverage. During 2023–24 price corrections buyers pressured sellers to reprice toward spot. Albemarle offsets by retaining long-term contracted volumes and quality premiums, structuring contracts to smooth volatility while preserving market share.

Product performance sensitivity

Customers of Albemarle are highly sensitive to product performance—EV range and battery safety hinge on lithium purity and consistent cathode/cell chemistry, with 2024 global EV sales reported at about 13–14 million units, raising demand for high-quality feedstocks.

Reliable delivery of specs drives customer stickiness and allows performance-linked premiums; failures in purity or catalyst yield can trigger rapid volume shifts despite material switching costs.

- EV range sensitivity: impacts purchasing and warranty exposure

- Safety & purity: directly tied to battery performance and recalls

- Specification reliability: increases contract tenure and premium pricing

- Failures: can cause quick customer volume migration despite switching frictions

Portfolio diversification by customers

OEMs in 2024 increasingly qualified multiple suppliers and chemistries (LFP vs high-nickel) to mitigate supply risk and cost, raising their bargaining leverage during sourcing cycles. Albemarle must compete on total cost, ESG credentials and multi-region reliability as customers shift chemistry mixes and suppliers. Multi-year, multi-plant approvals (commonly 3–5 years) remain Albemarle’s primary defense to retain share.

- OEM diversification of chemistries (2024: broader LFP uptake by Tesla/Chinese OEMs)

- Higher bargaining leverage during sourcing cycles

- Albemarle must win on cost, ESG, reliability

- Multi-year/multi-plant approvals = key switching cost

Buyer concentration boosts negotiating power; spot lithium down ~60%

Concentrated buyers (CATL ~35% EV battery capacity in 2024) wield strong price leverage, using index-linked and floor/ceiling deals; spot lithium fell ~60% from 2022 peaks by 2024, strengthening buyer negotiating power. Qualification lags (6–12 months) and multi-year approvals preserve supplier stickiness, but OEMs qualifying multiple chemistries raise sourcing leverage.

| Metric | 2024 value | Implication |

|---|---|---|

| CATL share | ~35% | Buyer concentration |

| Spot price change vs 2022 | −~60% | Buyer pricing power |

| Global EV sales | ~13.5m units | Demand for high-quality lithium |

Preview Before You Purchase

Albemarle Porter's Five Forces Analysis

This preview displays the exact Albemarle Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use the moment you complete payment. What you see is exactly what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Albemarle's Porter's Five Forces Analysis highlights intense supplier power, moderate buyer leverage, high industry rivalry, limited substitute threats, and entry barriers driven by scale and regulation. This snapshot shows where margin pressure and strategic opportunity intersect. Unlock the full report for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Resource concession and royalty gatekeepers

Access to brine fields and hard‑rock deposits is controlled by governments and a handful of leaseholders (top 3 operators dominate key basins), giving them leverage over royalties, water rights and operating terms. Policy shifts in 2024 in Chile, the U.S. or Australia can alter cost structures rapidly and materially. Albemarle’s own material resource ownership tempers but does not eliminate exposure. Negotiation outcomes directly affect margins and expansion timing.

Critical reagents and energy inputs

Lithium conversion relies on sulfuric acid, soda ash, lime and large electricity/steam inputs, creating exposure to chemical and power suppliers; reagents and energy have been reported to represent up to 30% of conversion operating costs. Regional energy price spikes have raised unit costs materially, keeping power price volatility a key input risk. Long-term supply contracts and on-site utilities reduce but do not fully hedge volatility; renewables sourcing improves resilience but requires upfront capital.

Specialized equipment and EPC capacity

Conversion plants, bromine assets and catalyst lines require custom equipment, EPC services and specialized maintenance expertise, concentrating supplier power. Tight vendor capacity and long lead times can delay projects and inflate capex, while Albemarle’s scale and long-term relationships help secure procurement slots. Ongoing global buildouts strain supply chains, and OEM reliability directly shapes production ramp profiles and timing risk.

Third‑party spodumene feedstock dependence

Even with owned mines Albemarle supplements feedstock with third‑party spodumene, exposing it to miners’ pricing and quality terms; spodumene prices eased from peaks >US$4,500/t in 2022 to roughly US$1,500/t in 2024, prompting miners to seek price floors while buyers face rising premiums and index‑linking when markets tighten.

- Qualification constraints reduce switching flexibility

- Contract optionality and diversification balance cost and continuity

- Spot vs long‑term mix drives margin volatility

Skilled labor and local stakeholders

Engineering talent shortages and unionized workforces materially affect Albemarle’s operating continuity and costs; tight 2024 labor markets (US unemployment ~3.9%) and rising ESG mandates boost bargaining power of skilled workers and community stakeholders, who can demand local hiring, supplier sourcing and environmental investments that raise capex and OPEX.

- Engineering talent: constrained supply raises wages and project delays

- Unionized labor: higher negotiation leverage on pay/conditions

- Social license: local spend and environmental mandates increase compliance costs

- Engagement: lowers disruption risk but adds recurring expenses

Supply squeeze lifts unit costs - reagents ~30%, spodumene US$1,500/t, labor tight

Suppliers wield moderate-to-high power: reagents and energy can be ~30% of conversion costs and regional power spikes raise unit costs materially. Spodumene spot fell from >US$4,500/t in 2022 to ~US$1,500/t in 2024, but miners push price floors and indexation. EPC, OEM and skilled labor shortages (US unemployment ~3.9% in 2024) cause lead-time and wage pressure.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Reagents/Energy | ~30% conversion cost | Margin sensitivity |

| Spodumene | ~US$1,500/t | Feedstock price risk |

| EPC/OEM/Labor | Long leads; unemployment ~3.9% | Capex delays, higher wages |

What is included in the product

Tailored Porter's Five Forces analysis for Albemarle that uncovers competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market position.

A one-sheet Porter’s Five Forces analysis for Albemarle that distills competitive pressure, supplier/customer leverage, substitution and entry threats into a deck-ready summary—easy to update with fresh lithium-market data or scenario tabs.

Customers Bargaining Power

Concentrated battery and auto OEM buyers

A handful of cathode makers, battery giants and automakers purchase the bulk of lithium, giving them strong negotiating power; CATL alone held about 35% of global EV battery capacity in 2024 (SNE Research). These buyers increasingly push index-linked or floor/ceiling contracts, trading multi-year volume commitments for pricing concessions and supply security. Ongoing consolidation among buyers amplifies their leverage, especially in down cycles.

High qualification and switching costs

Battery-grade lithium and catalysts require stringent qualification cycles often taking 6–12 months, raising switching costs and protecting incumbents; buyers factor in requalification delays and potential performance variance. Spot lithium carbonate prices were down over 60% from 2022 peaks by 2024, which tempers but does not eliminate pricing power for premium specs. In oversupply phases buyers still extract rebates or push mix optimization to reduce costs.

Price transparency and spot exposure

LME launched tradable lithium contracts in 2023 and spot indices such as Fastmarkets and S&P Global increased market transparency, boosting buyer negotiation leverage. During 2023–24 price corrections buyers pressured sellers to reprice toward spot. Albemarle offsets by retaining long-term contracted volumes and quality premiums, structuring contracts to smooth volatility while preserving market share.

Product performance sensitivity

Customers of Albemarle are highly sensitive to product performance—EV range and battery safety hinge on lithium purity and consistent cathode/cell chemistry, with 2024 global EV sales reported at about 13–14 million units, raising demand for high-quality feedstocks.

Reliable delivery of specs drives customer stickiness and allows performance-linked premiums; failures in purity or catalyst yield can trigger rapid volume shifts despite material switching costs.

- EV range sensitivity: impacts purchasing and warranty exposure

- Safety & purity: directly tied to battery performance and recalls

- Specification reliability: increases contract tenure and premium pricing

- Failures: can cause quick customer volume migration despite switching frictions

Portfolio diversification by customers

OEMs in 2024 increasingly qualified multiple suppliers and chemistries (LFP vs high-nickel) to mitigate supply risk and cost, raising their bargaining leverage during sourcing cycles. Albemarle must compete on total cost, ESG credentials and multi-region reliability as customers shift chemistry mixes and suppliers. Multi-year, multi-plant approvals (commonly 3–5 years) remain Albemarle’s primary defense to retain share.

- OEM diversification of chemistries (2024: broader LFP uptake by Tesla/Chinese OEMs)

- Higher bargaining leverage during sourcing cycles

- Albemarle must win on cost, ESG, reliability

- Multi-year/multi-plant approvals = key switching cost

Buyer concentration boosts negotiating power; spot lithium down ~60%

Concentrated buyers (CATL ~35% EV battery capacity in 2024) wield strong price leverage, using index-linked and floor/ceiling deals; spot lithium fell ~60% from 2022 peaks by 2024, strengthening buyer negotiating power. Qualification lags (6–12 months) and multi-year approvals preserve supplier stickiness, but OEMs qualifying multiple chemistries raise sourcing leverage.

| Metric | 2024 value | Implication |

|---|---|---|

| CATL share | ~35% | Buyer concentration |

| Spot price change vs 2022 | −~60% | Buyer pricing power |

| Global EV sales | ~13.5m units | Demand for high-quality lithium |

Preview Before You Purchase

Albemarle Porter's Five Forces Analysis

This preview displays the exact Albemarle Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The full, professionally formatted document is ready for immediate download and use the moment you complete payment. What you see is exactly what you get.