Albertsons Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

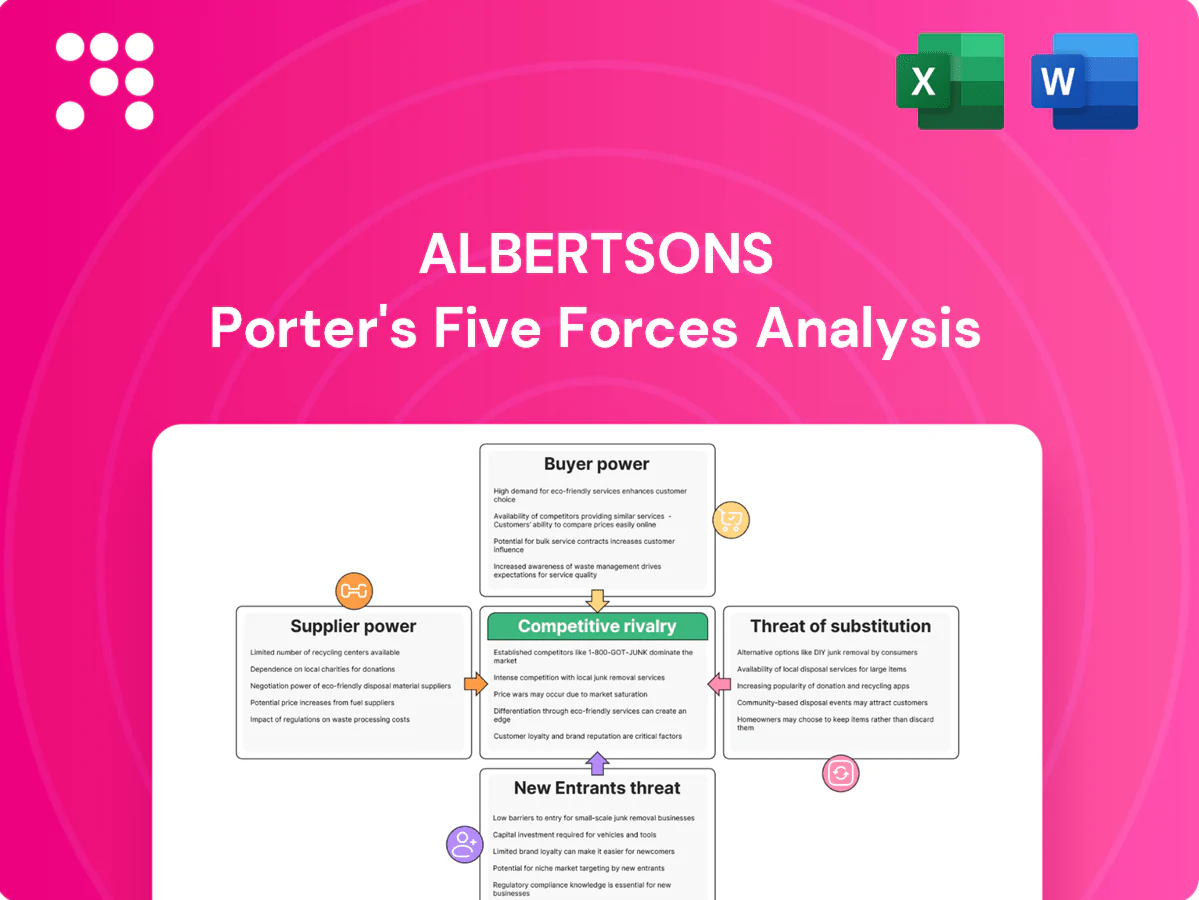

Albertsons faces intense rivalry, growing buyer power, and supplier leverage amid thin margins and low switching costs; new entrants and substitutes pose moderate threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Albertsons’s competitive dynamics in detail.

Suppliers Bargaining Power

Scale vs. branded CPG leverage

Albertsons’ national scale—over 2,000 stores and a national distribution network in 2024—enables volume purchasing and multi‑year contracts that blunt supplier leverage. Top CPGs in beverages, snacks and household goods still wield power through strong brand equity and concentrated shelf share. Promotional funding and slotting fees are reciprocal negotiation levers. Net effect: moderate supplier power, higher in branded staples.

Private label as a counterweight

Albertsons’ private brands—about one-fifth of its portfolio—give the retailer leverage versus national suppliers, supporting margin resilience alongside FY2023 net sales of roughly $69.6 billion; the chain shifts shelf space to in‑house labels when national vendors push prices, and private label penetration cushions commodity shocks, structurally reducing dependency on any single supplier.

Perishables and farm-sourced fragmentation

Produce, meat and seafood supply bases are highly fragmented, enabling competitive bidding and helping Albertsons (net sales ~73 billion in fiscal 2023) contain input costs. Seasonality, weather and biosecurity events can spike supplier power temporarily, as seen in periodic price surges and regional harvest shortfalls. Strict quality and food-safety standards limit substitutability for certain suppliers. Overall fragmentation generally reduces supplier leverage except during disruptions.

Pharmacy and healthcare channel constraints

Top three wholesalers (McKesson, AmerisourceBergen, Cardinal) control about 85% of U.S. drug distribution, raising supplier power for Albertsons' pharmacy inventory. PBM concentration (CVS Caremark, Express Scripts, Optum Rx) managing roughly 80% of prescriptions plus regulatory controls limit pricing flexibility. Periodic generic shortages—over 150 active listings in 2024—can sharply spike procurement costs, giving pharmacy higher upstream leverage than center-store grocery.

- Wholesaler concentration ~85%

- Top PBMs ~80% prescription share

- 2024 active shortages >150

Logistics, fuel, and packaging inputs

National grocery scale and ~20% private-label plus pharmacy concentration boost supplier leverage

Albertsons’ national scale (2,000+ stores in 2024) and ~20% private‑label penetration offset supplier leverage, but top CPGs retain shelf power; FY2023 net sales ~$69.6B. Pharmacy wholesalers ~85% concentrated, PBMs ~80% share and >150 generic shortages in 2024 raise supplier power in pharmacy. Transportation (diesel ~$4.00/gal 2024) and resin tightness intermittently boost supplier leverage.

| Metric | Value (2024/2023) |

|---|---|

| Stores | 2,000+ |

| Private label | ~20% |

| Net sales (FY2023) | $69.6B |

| Wholesaler conc. | ~85% |

| PBM share | ~80% |

| Generic shortages | >150 |

| Diesel | ~$4.00/gal |

What is included in the product

Concise Porter’s Five Forces assessment for Albertsons highlighting competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and regulatory/channel dynamics that shape pricing and margins, with strategic implications for market positioning and defensive moves.

One-sheet Porter's Five Forces for Albertsons—quickly visualize competitive pressures with editable ratings and a radar chart, ready to drop into decks or dashboards.

Customers Bargaining Power

Low switching costs for shoppers

Consumers can switch easily among nearby grocers, warehouse clubs and mass merchants, keeping pricing and service under constant pressure; in 2024 U.S. grocery retail sales were about $820 billion, reflecting intense competition across roughly 60,000 supermarket locations. Proximity and convenience marginally reduce switching but not enough to eliminate the threat, with omnichannel options accelerating churn. Buyer power is structurally high for Albertsons.

Price transparency and digital comparison

Mobile apps, weekly ads and online marketplaces expose prices and promotions widely, and with U.S. online grocery penetration at about 16% in 2024 cross-retailer comparisons via delivery and pickup are easy. This transparency increases customer sensitivity to price and perceived value. Albertsons responds with targeted offers and loyalty pricing through its digital Just for U promotions to retain spend and margin.

Loyalty programs and personalization

Albertsons leverages rewards, fuel points and personalized coupons via its Just for U program to increase stickiness and reduce buyer power, supported by millions of active members and digital promotions that lift basket size and frequency; its 2023 net sales near $72 billion underscore scale for targeted offers. First-party data enables precise promotions and basket optimization, but competitors can replicate tactics, limiting defensibility. Impact: moderating but not eliminating buyer leverage.

Quality, assortment, and fresh expectations

Shoppers demand consistent fresh quality, broad assortment and high in-stock rates; failures prompt rapid store switching, pressuring Albertsons, which operates about 2,200 stores in the US (2024). Superior perishables and local assortment reduce price-driven defections, so service and fulfillment levels materially shape buyer power.

- fresh-quality

- assortment-breadth

- in-stock-rates

- service-as-defence

Macroeconomic sensitivity

High buyer power in omnichannel grocery: $820B, 16% online

Buyer power is high: easy switching across ~60,000 stores and omnichannel options (US grocery sales ~$820B in 2024) keeps pricing pressured. Price transparency and 16% online penetration (2024) raise sensitivity; Albertsons (≈2,200 stores, 2023 sales ~$72B) fights with Just for U, loyalty and private-label (≈18% share) but cannot fully neutralize leverage.

| Metric | Value |

|---|---|

| US grocery sales (2024) | $820B |

| Online penetration (2024) | 16% |

| Albertsons stores | ≈2,200 |

| Albertsons sales (2023) | $72B |

| Private label (2024) | ≈18% |

Preview the Actual Deliverable

Albertsons Porter's Five Forces Analysis

This preview shows the exact Albertsons Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted and ready to download and use immediately upon payment. You're viewing the final deliverable: the same comprehensive competitive forces assessment available instantly to buyers.

A Must-Have Tool for Decision-Makers

Albertsons faces intense rivalry, growing buyer power, and supplier leverage amid thin margins and low switching costs; new entrants and substitutes pose moderate threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Albertsons’s competitive dynamics in detail.

Suppliers Bargaining Power

Scale vs. branded CPG leverage

Albertsons’ national scale—over 2,000 stores and a national distribution network in 2024—enables volume purchasing and multi‑year contracts that blunt supplier leverage. Top CPGs in beverages, snacks and household goods still wield power through strong brand equity and concentrated shelf share. Promotional funding and slotting fees are reciprocal negotiation levers. Net effect: moderate supplier power, higher in branded staples.

Private label as a counterweight

Albertsons’ private brands—about one-fifth of its portfolio—give the retailer leverage versus national suppliers, supporting margin resilience alongside FY2023 net sales of roughly $69.6 billion; the chain shifts shelf space to in‑house labels when national vendors push prices, and private label penetration cushions commodity shocks, structurally reducing dependency on any single supplier.

Perishables and farm-sourced fragmentation

Produce, meat and seafood supply bases are highly fragmented, enabling competitive bidding and helping Albertsons (net sales ~73 billion in fiscal 2023) contain input costs. Seasonality, weather and biosecurity events can spike supplier power temporarily, as seen in periodic price surges and regional harvest shortfalls. Strict quality and food-safety standards limit substitutability for certain suppliers. Overall fragmentation generally reduces supplier leverage except during disruptions.

Pharmacy and healthcare channel constraints

Top three wholesalers (McKesson, AmerisourceBergen, Cardinal) control about 85% of U.S. drug distribution, raising supplier power for Albertsons' pharmacy inventory. PBM concentration (CVS Caremark, Express Scripts, Optum Rx) managing roughly 80% of prescriptions plus regulatory controls limit pricing flexibility. Periodic generic shortages—over 150 active listings in 2024—can sharply spike procurement costs, giving pharmacy higher upstream leverage than center-store grocery.

- Wholesaler concentration ~85%

- Top PBMs ~80% prescription share

- 2024 active shortages >150

Logistics, fuel, and packaging inputs

National grocery scale and ~20% private-label plus pharmacy concentration boost supplier leverage

Albertsons’ national scale (2,000+ stores in 2024) and ~20% private‑label penetration offset supplier leverage, but top CPGs retain shelf power; FY2023 net sales ~$69.6B. Pharmacy wholesalers ~85% concentrated, PBMs ~80% share and >150 generic shortages in 2024 raise supplier power in pharmacy. Transportation (diesel ~$4.00/gal 2024) and resin tightness intermittently boost supplier leverage.

| Metric | Value (2024/2023) |

|---|---|

| Stores | 2,000+ |

| Private label | ~20% |

| Net sales (FY2023) | $69.6B |

| Wholesaler conc. | ~85% |

| PBM share | ~80% |

| Generic shortages | >150 |

| Diesel | ~$4.00/gal |

What is included in the product

Concise Porter’s Five Forces assessment for Albertsons highlighting competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and regulatory/channel dynamics that shape pricing and margins, with strategic implications for market positioning and defensive moves.

One-sheet Porter's Five Forces for Albertsons—quickly visualize competitive pressures with editable ratings and a radar chart, ready to drop into decks or dashboards.

Customers Bargaining Power

Low switching costs for shoppers

Consumers can switch easily among nearby grocers, warehouse clubs and mass merchants, keeping pricing and service under constant pressure; in 2024 U.S. grocery retail sales were about $820 billion, reflecting intense competition across roughly 60,000 supermarket locations. Proximity and convenience marginally reduce switching but not enough to eliminate the threat, with omnichannel options accelerating churn. Buyer power is structurally high for Albertsons.

Price transparency and digital comparison

Mobile apps, weekly ads and online marketplaces expose prices and promotions widely, and with U.S. online grocery penetration at about 16% in 2024 cross-retailer comparisons via delivery and pickup are easy. This transparency increases customer sensitivity to price and perceived value. Albertsons responds with targeted offers and loyalty pricing through its digital Just for U promotions to retain spend and margin.

Loyalty programs and personalization

Albertsons leverages rewards, fuel points and personalized coupons via its Just for U program to increase stickiness and reduce buyer power, supported by millions of active members and digital promotions that lift basket size and frequency; its 2023 net sales near $72 billion underscore scale for targeted offers. First-party data enables precise promotions and basket optimization, but competitors can replicate tactics, limiting defensibility. Impact: moderating but not eliminating buyer leverage.

Quality, assortment, and fresh expectations

Shoppers demand consistent fresh quality, broad assortment and high in-stock rates; failures prompt rapid store switching, pressuring Albertsons, which operates about 2,200 stores in the US (2024). Superior perishables and local assortment reduce price-driven defections, so service and fulfillment levels materially shape buyer power.

- fresh-quality

- assortment-breadth

- in-stock-rates

- service-as-defence

Macroeconomic sensitivity

High buyer power in omnichannel grocery: $820B, 16% online

Buyer power is high: easy switching across ~60,000 stores and omnichannel options (US grocery sales ~$820B in 2024) keeps pricing pressured. Price transparency and 16% online penetration (2024) raise sensitivity; Albertsons (≈2,200 stores, 2023 sales ~$72B) fights with Just for U, loyalty and private-label (≈18% share) but cannot fully neutralize leverage.

| Metric | Value |

|---|---|

| US grocery sales (2024) | $820B |

| Online penetration (2024) | 16% |

| Albertsons stores | ≈2,200 |

| Albertsons sales (2023) | $72B |

| Private label (2024) | ≈18% |

Preview the Actual Deliverable

Albertsons Porter's Five Forces Analysis

This preview shows the exact Albertsons Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted and ready to download and use immediately upon payment. You're viewing the final deliverable: the same comprehensive competitive forces assessment available instantly to buyers.

Description

A Must-Have Tool for Decision-Makers

Albertsons faces intense rivalry, growing buyer power, and supplier leverage amid thin margins and low switching costs; new entrants and substitutes pose moderate threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Albertsons’s competitive dynamics in detail.

Suppliers Bargaining Power

Scale vs. branded CPG leverage

Albertsons’ national scale—over 2,000 stores and a national distribution network in 2024—enables volume purchasing and multi‑year contracts that blunt supplier leverage. Top CPGs in beverages, snacks and household goods still wield power through strong brand equity and concentrated shelf share. Promotional funding and slotting fees are reciprocal negotiation levers. Net effect: moderate supplier power, higher in branded staples.

Private label as a counterweight

Albertsons’ private brands—about one-fifth of its portfolio—give the retailer leverage versus national suppliers, supporting margin resilience alongside FY2023 net sales of roughly $69.6 billion; the chain shifts shelf space to in‑house labels when national vendors push prices, and private label penetration cushions commodity shocks, structurally reducing dependency on any single supplier.

Perishables and farm-sourced fragmentation

Produce, meat and seafood supply bases are highly fragmented, enabling competitive bidding and helping Albertsons (net sales ~73 billion in fiscal 2023) contain input costs. Seasonality, weather and biosecurity events can spike supplier power temporarily, as seen in periodic price surges and regional harvest shortfalls. Strict quality and food-safety standards limit substitutability for certain suppliers. Overall fragmentation generally reduces supplier leverage except during disruptions.

Pharmacy and healthcare channel constraints

Top three wholesalers (McKesson, AmerisourceBergen, Cardinal) control about 85% of U.S. drug distribution, raising supplier power for Albertsons' pharmacy inventory. PBM concentration (CVS Caremark, Express Scripts, Optum Rx) managing roughly 80% of prescriptions plus regulatory controls limit pricing flexibility. Periodic generic shortages—over 150 active listings in 2024—can sharply spike procurement costs, giving pharmacy higher upstream leverage than center-store grocery.

- Wholesaler concentration ~85%

- Top PBMs ~80% prescription share

- 2024 active shortages >150

Logistics, fuel, and packaging inputs

National grocery scale and ~20% private-label plus pharmacy concentration boost supplier leverage

Albertsons’ national scale (2,000+ stores in 2024) and ~20% private‑label penetration offset supplier leverage, but top CPGs retain shelf power; FY2023 net sales ~$69.6B. Pharmacy wholesalers ~85% concentrated, PBMs ~80% share and >150 generic shortages in 2024 raise supplier power in pharmacy. Transportation (diesel ~$4.00/gal 2024) and resin tightness intermittently boost supplier leverage.

| Metric | Value (2024/2023) |

|---|---|

| Stores | 2,000+ |

| Private label | ~20% |

| Net sales (FY2023) | $69.6B |

| Wholesaler conc. | ~85% |

| PBM share | ~80% |

| Generic shortages | >150 |

| Diesel | ~$4.00/gal |

What is included in the product

Concise Porter’s Five Forces assessment for Albertsons highlighting competitive rivalry, buyer and supplier leverage, threat of new entrants and substitutes, and regulatory/channel dynamics that shape pricing and margins, with strategic implications for market positioning and defensive moves.

One-sheet Porter's Five Forces for Albertsons—quickly visualize competitive pressures with editable ratings and a radar chart, ready to drop into decks or dashboards.

Customers Bargaining Power

Low switching costs for shoppers

Consumers can switch easily among nearby grocers, warehouse clubs and mass merchants, keeping pricing and service under constant pressure; in 2024 U.S. grocery retail sales were about $820 billion, reflecting intense competition across roughly 60,000 supermarket locations. Proximity and convenience marginally reduce switching but not enough to eliminate the threat, with omnichannel options accelerating churn. Buyer power is structurally high for Albertsons.

Price transparency and digital comparison

Mobile apps, weekly ads and online marketplaces expose prices and promotions widely, and with U.S. online grocery penetration at about 16% in 2024 cross-retailer comparisons via delivery and pickup are easy. This transparency increases customer sensitivity to price and perceived value. Albertsons responds with targeted offers and loyalty pricing through its digital Just for U promotions to retain spend and margin.

Loyalty programs and personalization

Albertsons leverages rewards, fuel points and personalized coupons via its Just for U program to increase stickiness and reduce buyer power, supported by millions of active members and digital promotions that lift basket size and frequency; its 2023 net sales near $72 billion underscore scale for targeted offers. First-party data enables precise promotions and basket optimization, but competitors can replicate tactics, limiting defensibility. Impact: moderating but not eliminating buyer leverage.

Quality, assortment, and fresh expectations

Shoppers demand consistent fresh quality, broad assortment and high in-stock rates; failures prompt rapid store switching, pressuring Albertsons, which operates about 2,200 stores in the US (2024). Superior perishables and local assortment reduce price-driven defections, so service and fulfillment levels materially shape buyer power.

- fresh-quality

- assortment-breadth

- in-stock-rates

- service-as-defence

Macroeconomic sensitivity

High buyer power in omnichannel grocery: $820B, 16% online

Buyer power is high: easy switching across ~60,000 stores and omnichannel options (US grocery sales ~$820B in 2024) keeps pricing pressured. Price transparency and 16% online penetration (2024) raise sensitivity; Albertsons (≈2,200 stores, 2023 sales ~$72B) fights with Just for U, loyalty and private-label (≈18% share) but cannot fully neutralize leverage.

| Metric | Value |

|---|---|

| US grocery sales (2024) | $820B |

| Online penetration (2024) | 16% |

| Albertsons stores | ≈2,200 |

| Albertsons sales (2023) | $72B |

| Private label (2024) | ≈18% |

Preview the Actual Deliverable

Albertsons Porter's Five Forces Analysis

This preview shows the exact Albertsons Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted and ready to download and use immediately upon payment. You're viewing the final deliverable: the same comprehensive competitive forces assessment available instantly to buyers.