Alcoa Boston Consulting Group Matrix

Download Your Competitive Advantage

Quick look: Alcoa’s BCG Matrix teases where its aluminum lines sit—fast-growing Stars, steady Cash Cows, and the slower pieces that drain capital. This snapshot shows strategy tensions and where leadership must choose to invest, harvest, or divest. Want the full, actionable map with quadrant-by-quadrant recommendations and editable Word + Excel files? Purchase the complete BCG Matrix and get the roadmap to smarter allocation—fast, clear, and ready to present.

Stars

Low‑carbon primary aluminum

High growth demand from auto, packaging and electronics is chasing lower‑emissions metal as global primary aluminum production reached about 68.6 million tonnes in 2023 (World Aluminium), boosting premiums for low‑carbon supply.

Alcoa’s low‑carbon offerings ride this sustainability wave and hold solid share in premium contracts; the company continues investing in renewable‑tied capacity and third‑party certification.

If momentum in corporate procurement and regulations holds, this line can mature into a cash‑rich engine for Alcoa.

Sustainable smelting tech (inert‑anode/next‑gen processes)

Breakthrough inert‑anode smelting that replaces carbon anodes and emits oxygen rather than CO2 is a category maker: primary aluminium accounts for roughly 1% of global CO2 emissions (IAI) and 2024 industry focus is intense. It sits at the sweet spot—rapid buyer demand for low‑carbon metal plus strong IP moats from pilot patents. It soaks cash today—pilots and scale‑up running into hundreds of millions—but secures strategic leadership and a favorable future cost curve.

Premium alumina for high‑purity uses

Specialty alumina grades feed catalysts, technical ceramics and advanced materials exhibiting healthy growth, with market reports citing roughly a 5% CAGR for high‑purity alumina segments from 2024–2030. Alcoa’s upstream integration from bauxite to refined alumina provides consistent quality and volume that competitors struggle to replicate. Premiums on specialty grades justify ongoing marketing and targeted debottlenecking investments. Hold share aggressively to lock in long‑run margin.

Aerospace and EV‑linked supply programs

Lightweighting demand has rebounded as global air traffic reached about 95% of 2019 levels in 2024 (IATA) and EV adoption climbed to roughly 18% of new car sales in 2024, favoring established metal suppliers; Alcoa’s billets and high‑spec feed position scales with fleet recovery and EV architecture shifts. Winning multi‑year contracts requires dedicated service, alloy qualifications and tech support. The right OEM and tier partnerships convert scale into a durable competitive lead.

- Qualification moat: long lead times, high certification costs

- Scale driver: billet supply tied to fleet & EV growth

- Win factors: service, tech support, OEM partnerships

Hydro‑powered smelter portfolio

Hydro-powered smelter portfolio delivers lower cash costs and 60–80% lower Scope 1/2 emissions versus grid-reliant peers, matching 2024 market demand for low-carbon aluminium; capacity is competitive today and gaining pricing power as certified low-carbon aluminium attracted premiums in 2024 of several hundred dollars per tonne. Continue optimizing load, reliability and certification; as growth normalizes these plants generate strong free cash flow.

- Lower cost & carbon

- Pricing power: 2024 green premiums ~hundreds $/t

- Focus: load, reliability, certification

- Outcome: strong cash generation

Hydro aluminium cuts emissions 60-80% and captures $200-400/t green premiums

Stars: low‑carbon primary (68.6 Mt market 2023) and specialty alumina (~5% CAGR 2024–30) meet EV (18% new sales 2024) and aviation demand (95% of 2019 traffic, 2024).

Hydro smelters cut Scope1/2 emissions 60–80% and captured green premiums ~$200–400/t in 2024, enabling scale‑up into cash generators.

| Metric | Value |

|---|---|

| Primary aluminium market | 68.6 Mt (2023) |

| EV new sales | 18% (2024) |

| Green premium | $200–400/t (2024) |

| Specialty alumina CAGR | ~5% (2024–30) |

| Hydro smelter emissions | -60–80% Scope1/2 |

What is included in the product

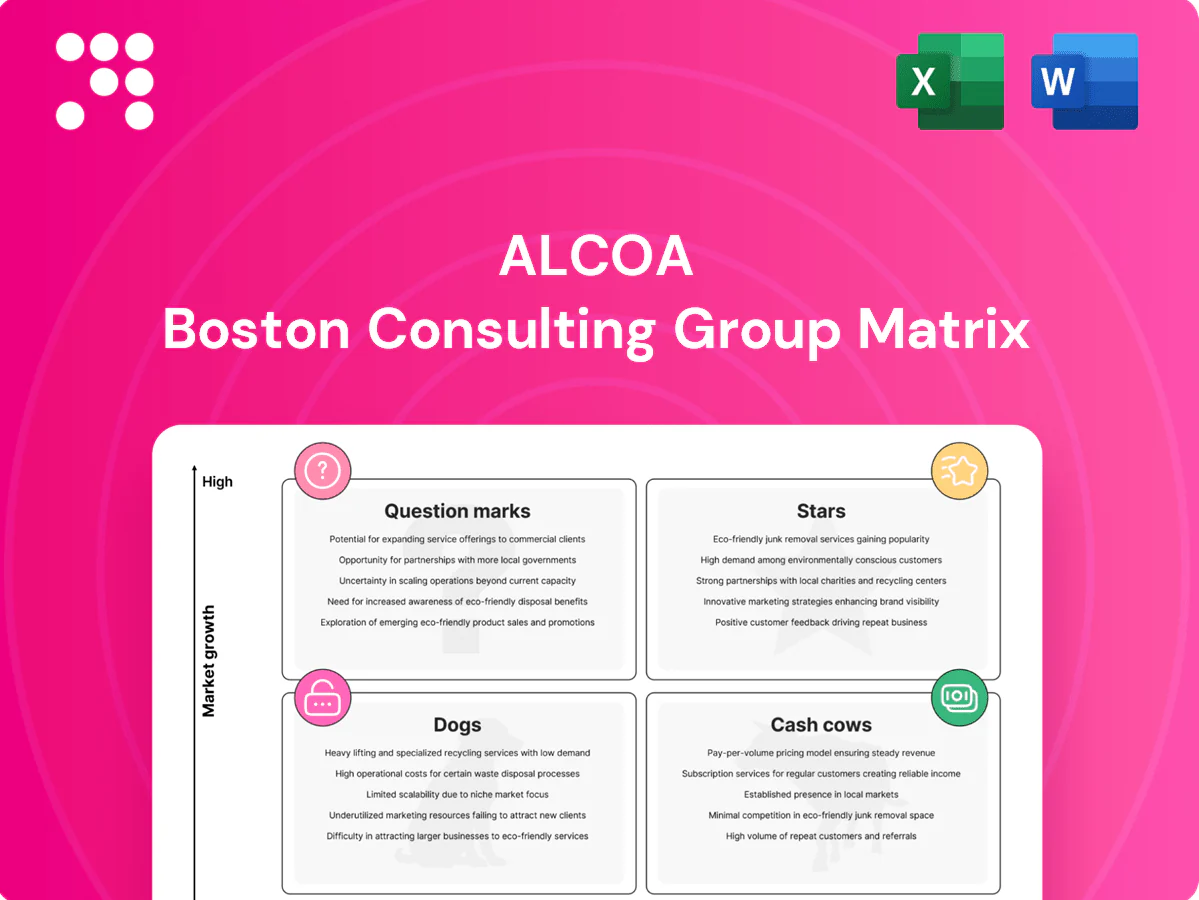

BCG Matrix of Alcoa’s business units highlighting Stars, Cash Cows, Question Marks and Dogs with focused strategic actions.

One-page Alcoa BCG Matrix that clarifies portfolio pain points and guides quick resource moves for C-suite decisions

Cash Cows

Commodity alumina shipments

Commodity alumina shipments sit in a mature market with big volumes and steady offtake—Alcoa shipped about 4.2 million tonnes of alumina in 2024, underpinning predictable revenue. Alcoa’s scale and logistics edge convert throughput into dependable margins and stable cash generation. Capex needs remain modest relative to throughput, supporting a milk-the-position strategy while targeting year-over-year unit-cost reductions.

Tier‑one bauxite mines with advantaged logistics

Tier‑one bauxite mines such as Alcoa’s Weipa complex produce around 20 million tonnes per year, are proven and tightly contracted, and deliver predictable free cash flow. Growth is limited but cash conversion remains strong, with upstream margins supporting >30% cash conversion in recent years. Targeted haulage and processing upgrades typically raise yields and lower unit costs, keeping operations capital‑efficient and low‑risk.

Long‑term industrial aluminum contracts (construction/packaging)

Long-term industrial aluminum contracts in construction and packaging anchor stable end-markets and repeat buyers, supporting steady cash flow; global primary aluminum demand was about 69 million tonnes in 2024, underscoring baseline volume stability. Hedged pricing and pass-through clauses protect margins, making these assets dependable rather than high-growth. Maintain service levels and use proceeds to fund tech bets and debt service, preserving liquidity and strategic optionality.

Operational excellence and energy hedges

Operational excellence, tight process discipline and a disciplined maintenance cadence keep Alcoa’s smelters running at high utilization while smart power contracts lock in spreads; energy typically represents about 30–40% of primary aluminum cash costs, so hedges quietly convert volatility into steady cash flow and incremental margin gains.

- Process discipline: uptime focus

- Maintenance cadence: fewer unplanned outages

- Power hedges: stabilize cash margins

By‑product and residue value recovery

Alcoa’s established by-product and residue recovery programs delivered incremental profit in 2024 by converting intermediates and red mud streams into saleable materials, yielding low-growth, high-return gains from small operational tweaks and recycling flows. Tight material stewardship and asset-light recovery steps increased cash generation with minimal capital risk, so prioritize continual optimization rather than heavy new builds.

- 2024 focus: maximize margin via residues

- Low growth, high ROI from small tweaks

- Tight stewardship = cash up, risk down

- Optimize operations; avoid overbuilding

4.2m alumina, 20m bauxite- >30% conversion; energy 30–40%

Alcoa’s alumina shipments ~4.2m t (2024) and Weipa bauxite ~20m t/year deliver steady, high-conversion cash (~>30%); global primary aluminum demand ~69m t supports baseline volumes. Energy ~30–40% of cash cost—power hedges and uptime drive margin stability. Residue recovery and small capex yield incremental, low-risk returns, funding tech bets and debt service.

| Asset | 2024 metric | Cash role |

|---|---|---|

| Alumina | 4.2m t | Predictable revenue |

| Bauxite | 20m t | High cash conversion |

| Smelters | Energy 30–40% cost | Hedge-driven stability |

Preview = Final Product

Alcoa BCG Matrix

The Alcoa BCG Matrix you’re previewing on this page is the exact, final file you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready matrix tailored to Alcoa’s portfolio. It’s built by strategy pros for clarity and immediate use, editable and print-ready. After purchase the same document is delivered—no surprises, no revisions required.

Download Your Competitive Advantage

Quick look: Alcoa’s BCG Matrix teases where its aluminum lines sit—fast-growing Stars, steady Cash Cows, and the slower pieces that drain capital. This snapshot shows strategy tensions and where leadership must choose to invest, harvest, or divest. Want the full, actionable map with quadrant-by-quadrant recommendations and editable Word + Excel files? Purchase the complete BCG Matrix and get the roadmap to smarter allocation—fast, clear, and ready to present.

Stars

Low‑carbon primary aluminum

High growth demand from auto, packaging and electronics is chasing lower‑emissions metal as global primary aluminum production reached about 68.6 million tonnes in 2023 (World Aluminium), boosting premiums for low‑carbon supply.

Alcoa’s low‑carbon offerings ride this sustainability wave and hold solid share in premium contracts; the company continues investing in renewable‑tied capacity and third‑party certification.

If momentum in corporate procurement and regulations holds, this line can mature into a cash‑rich engine for Alcoa.

Sustainable smelting tech (inert‑anode/next‑gen processes)

Breakthrough inert‑anode smelting that replaces carbon anodes and emits oxygen rather than CO2 is a category maker: primary aluminium accounts for roughly 1% of global CO2 emissions (IAI) and 2024 industry focus is intense. It sits at the sweet spot—rapid buyer demand for low‑carbon metal plus strong IP moats from pilot patents. It soaks cash today—pilots and scale‑up running into hundreds of millions—but secures strategic leadership and a favorable future cost curve.

Premium alumina for high‑purity uses

Specialty alumina grades feed catalysts, technical ceramics and advanced materials exhibiting healthy growth, with market reports citing roughly a 5% CAGR for high‑purity alumina segments from 2024–2030. Alcoa’s upstream integration from bauxite to refined alumina provides consistent quality and volume that competitors struggle to replicate. Premiums on specialty grades justify ongoing marketing and targeted debottlenecking investments. Hold share aggressively to lock in long‑run margin.

Aerospace and EV‑linked supply programs

Lightweighting demand has rebounded as global air traffic reached about 95% of 2019 levels in 2024 (IATA) and EV adoption climbed to roughly 18% of new car sales in 2024, favoring established metal suppliers; Alcoa’s billets and high‑spec feed position scales with fleet recovery and EV architecture shifts. Winning multi‑year contracts requires dedicated service, alloy qualifications and tech support. The right OEM and tier partnerships convert scale into a durable competitive lead.

- Qualification moat: long lead times, high certification costs

- Scale driver: billet supply tied to fleet & EV growth

- Win factors: service, tech support, OEM partnerships

Hydro‑powered smelter portfolio

Hydro-powered smelter portfolio delivers lower cash costs and 60–80% lower Scope 1/2 emissions versus grid-reliant peers, matching 2024 market demand for low-carbon aluminium; capacity is competitive today and gaining pricing power as certified low-carbon aluminium attracted premiums in 2024 of several hundred dollars per tonne. Continue optimizing load, reliability and certification; as growth normalizes these plants generate strong free cash flow.

- Lower cost & carbon

- Pricing power: 2024 green premiums ~hundreds $/t

- Focus: load, reliability, certification

- Outcome: strong cash generation

Hydro aluminium cuts emissions 60-80% and captures $200-400/t green premiums

Stars: low‑carbon primary (68.6 Mt market 2023) and specialty alumina (~5% CAGR 2024–30) meet EV (18% new sales 2024) and aviation demand (95% of 2019 traffic, 2024).

Hydro smelters cut Scope1/2 emissions 60–80% and captured green premiums ~$200–400/t in 2024, enabling scale‑up into cash generators.

| Metric | Value |

|---|---|

| Primary aluminium market | 68.6 Mt (2023) |

| EV new sales | 18% (2024) |

| Green premium | $200–400/t (2024) |

| Specialty alumina CAGR | ~5% (2024–30) |

| Hydro smelter emissions | -60–80% Scope1/2 |

What is included in the product

BCG Matrix of Alcoa’s business units highlighting Stars, Cash Cows, Question Marks and Dogs with focused strategic actions.

One-page Alcoa BCG Matrix that clarifies portfolio pain points and guides quick resource moves for C-suite decisions

Cash Cows

Commodity alumina shipments

Commodity alumina shipments sit in a mature market with big volumes and steady offtake—Alcoa shipped about 4.2 million tonnes of alumina in 2024, underpinning predictable revenue. Alcoa’s scale and logistics edge convert throughput into dependable margins and stable cash generation. Capex needs remain modest relative to throughput, supporting a milk-the-position strategy while targeting year-over-year unit-cost reductions.

Tier‑one bauxite mines with advantaged logistics

Tier‑one bauxite mines such as Alcoa’s Weipa complex produce around 20 million tonnes per year, are proven and tightly contracted, and deliver predictable free cash flow. Growth is limited but cash conversion remains strong, with upstream margins supporting >30% cash conversion in recent years. Targeted haulage and processing upgrades typically raise yields and lower unit costs, keeping operations capital‑efficient and low‑risk.

Long‑term industrial aluminum contracts (construction/packaging)

Long-term industrial aluminum contracts in construction and packaging anchor stable end-markets and repeat buyers, supporting steady cash flow; global primary aluminum demand was about 69 million tonnes in 2024, underscoring baseline volume stability. Hedged pricing and pass-through clauses protect margins, making these assets dependable rather than high-growth. Maintain service levels and use proceeds to fund tech bets and debt service, preserving liquidity and strategic optionality.

Operational excellence and energy hedges

Operational excellence, tight process discipline and a disciplined maintenance cadence keep Alcoa’s smelters running at high utilization while smart power contracts lock in spreads; energy typically represents about 30–40% of primary aluminum cash costs, so hedges quietly convert volatility into steady cash flow and incremental margin gains.

- Process discipline: uptime focus

- Maintenance cadence: fewer unplanned outages

- Power hedges: stabilize cash margins

By‑product and residue value recovery

Alcoa’s established by-product and residue recovery programs delivered incremental profit in 2024 by converting intermediates and red mud streams into saleable materials, yielding low-growth, high-return gains from small operational tweaks and recycling flows. Tight material stewardship and asset-light recovery steps increased cash generation with minimal capital risk, so prioritize continual optimization rather than heavy new builds.

- 2024 focus: maximize margin via residues

- Low growth, high ROI from small tweaks

- Tight stewardship = cash up, risk down

- Optimize operations; avoid overbuilding

4.2m alumina, 20m bauxite- >30% conversion; energy 30–40%

Alcoa’s alumina shipments ~4.2m t (2024) and Weipa bauxite ~20m t/year deliver steady, high-conversion cash (~>30%); global primary aluminum demand ~69m t supports baseline volumes. Energy ~30–40% of cash cost—power hedges and uptime drive margin stability. Residue recovery and small capex yield incremental, low-risk returns, funding tech bets and debt service.

| Asset | 2024 metric | Cash role |

|---|---|---|

| Alumina | 4.2m t | Predictable revenue |

| Bauxite | 20m t | High cash conversion |

| Smelters | Energy 30–40% cost | Hedge-driven stability |

Preview = Final Product

Alcoa BCG Matrix

The Alcoa BCG Matrix you’re previewing on this page is the exact, final file you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready matrix tailored to Alcoa’s portfolio. It’s built by strategy pros for clarity and immediate use, editable and print-ready. After purchase the same document is delivered—no surprises, no revisions required.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Quick look: Alcoa’s BCG Matrix teases where its aluminum lines sit—fast-growing Stars, steady Cash Cows, and the slower pieces that drain capital. This snapshot shows strategy tensions and where leadership must choose to invest, harvest, or divest. Want the full, actionable map with quadrant-by-quadrant recommendations and editable Word + Excel files? Purchase the complete BCG Matrix and get the roadmap to smarter allocation—fast, clear, and ready to present.

Stars

Low‑carbon primary aluminum

High growth demand from auto, packaging and electronics is chasing lower‑emissions metal as global primary aluminum production reached about 68.6 million tonnes in 2023 (World Aluminium), boosting premiums for low‑carbon supply.

Alcoa’s low‑carbon offerings ride this sustainability wave and hold solid share in premium contracts; the company continues investing in renewable‑tied capacity and third‑party certification.

If momentum in corporate procurement and regulations holds, this line can mature into a cash‑rich engine for Alcoa.

Sustainable smelting tech (inert‑anode/next‑gen processes)

Breakthrough inert‑anode smelting that replaces carbon anodes and emits oxygen rather than CO2 is a category maker: primary aluminium accounts for roughly 1% of global CO2 emissions (IAI) and 2024 industry focus is intense. It sits at the sweet spot—rapid buyer demand for low‑carbon metal plus strong IP moats from pilot patents. It soaks cash today—pilots and scale‑up running into hundreds of millions—but secures strategic leadership and a favorable future cost curve.

Premium alumina for high‑purity uses

Specialty alumina grades feed catalysts, technical ceramics and advanced materials exhibiting healthy growth, with market reports citing roughly a 5% CAGR for high‑purity alumina segments from 2024–2030. Alcoa’s upstream integration from bauxite to refined alumina provides consistent quality and volume that competitors struggle to replicate. Premiums on specialty grades justify ongoing marketing and targeted debottlenecking investments. Hold share aggressively to lock in long‑run margin.

Aerospace and EV‑linked supply programs

Lightweighting demand has rebounded as global air traffic reached about 95% of 2019 levels in 2024 (IATA) and EV adoption climbed to roughly 18% of new car sales in 2024, favoring established metal suppliers; Alcoa’s billets and high‑spec feed position scales with fleet recovery and EV architecture shifts. Winning multi‑year contracts requires dedicated service, alloy qualifications and tech support. The right OEM and tier partnerships convert scale into a durable competitive lead.

- Qualification moat: long lead times, high certification costs

- Scale driver: billet supply tied to fleet & EV growth

- Win factors: service, tech support, OEM partnerships

Hydro‑powered smelter portfolio

Hydro-powered smelter portfolio delivers lower cash costs and 60–80% lower Scope 1/2 emissions versus grid-reliant peers, matching 2024 market demand for low-carbon aluminium; capacity is competitive today and gaining pricing power as certified low-carbon aluminium attracted premiums in 2024 of several hundred dollars per tonne. Continue optimizing load, reliability and certification; as growth normalizes these plants generate strong free cash flow.

- Lower cost & carbon

- Pricing power: 2024 green premiums ~hundreds $/t

- Focus: load, reliability, certification

- Outcome: strong cash generation

Hydro aluminium cuts emissions 60-80% and captures $200-400/t green premiums

Stars: low‑carbon primary (68.6 Mt market 2023) and specialty alumina (~5% CAGR 2024–30) meet EV (18% new sales 2024) and aviation demand (95% of 2019 traffic, 2024).

Hydro smelters cut Scope1/2 emissions 60–80% and captured green premiums ~$200–400/t in 2024, enabling scale‑up into cash generators.

| Metric | Value |

|---|---|

| Primary aluminium market | 68.6 Mt (2023) |

| EV new sales | 18% (2024) |

| Green premium | $200–400/t (2024) |

| Specialty alumina CAGR | ~5% (2024–30) |

| Hydro smelter emissions | -60–80% Scope1/2 |

What is included in the product

BCG Matrix of Alcoa’s business units highlighting Stars, Cash Cows, Question Marks and Dogs with focused strategic actions.

One-page Alcoa BCG Matrix that clarifies portfolio pain points and guides quick resource moves for C-suite decisions

Cash Cows

Commodity alumina shipments

Commodity alumina shipments sit in a mature market with big volumes and steady offtake—Alcoa shipped about 4.2 million tonnes of alumina in 2024, underpinning predictable revenue. Alcoa’s scale and logistics edge convert throughput into dependable margins and stable cash generation. Capex needs remain modest relative to throughput, supporting a milk-the-position strategy while targeting year-over-year unit-cost reductions.

Tier‑one bauxite mines with advantaged logistics

Tier‑one bauxite mines such as Alcoa’s Weipa complex produce around 20 million tonnes per year, are proven and tightly contracted, and deliver predictable free cash flow. Growth is limited but cash conversion remains strong, with upstream margins supporting >30% cash conversion in recent years. Targeted haulage and processing upgrades typically raise yields and lower unit costs, keeping operations capital‑efficient and low‑risk.

Long‑term industrial aluminum contracts (construction/packaging)

Long-term industrial aluminum contracts in construction and packaging anchor stable end-markets and repeat buyers, supporting steady cash flow; global primary aluminum demand was about 69 million tonnes in 2024, underscoring baseline volume stability. Hedged pricing and pass-through clauses protect margins, making these assets dependable rather than high-growth. Maintain service levels and use proceeds to fund tech bets and debt service, preserving liquidity and strategic optionality.

Operational excellence and energy hedges

Operational excellence, tight process discipline and a disciplined maintenance cadence keep Alcoa’s smelters running at high utilization while smart power contracts lock in spreads; energy typically represents about 30–40% of primary aluminum cash costs, so hedges quietly convert volatility into steady cash flow and incremental margin gains.

- Process discipline: uptime focus

- Maintenance cadence: fewer unplanned outages

- Power hedges: stabilize cash margins

By‑product and residue value recovery

Alcoa’s established by-product and residue recovery programs delivered incremental profit in 2024 by converting intermediates and red mud streams into saleable materials, yielding low-growth, high-return gains from small operational tweaks and recycling flows. Tight material stewardship and asset-light recovery steps increased cash generation with minimal capital risk, so prioritize continual optimization rather than heavy new builds.

- 2024 focus: maximize margin via residues

- Low growth, high ROI from small tweaks

- Tight stewardship = cash up, risk down

- Optimize operations; avoid overbuilding

4.2m alumina, 20m bauxite- >30% conversion; energy 30–40%

Alcoa’s alumina shipments ~4.2m t (2024) and Weipa bauxite ~20m t/year deliver steady, high-conversion cash (~>30%); global primary aluminum demand ~69m t supports baseline volumes. Energy ~30–40% of cash cost—power hedges and uptime drive margin stability. Residue recovery and small capex yield incremental, low-risk returns, funding tech bets and debt service.

| Asset | 2024 metric | Cash role |

|---|---|---|

| Alumina | 4.2m t | Predictable revenue |

| Bauxite | 20m t | High cash conversion |

| Smelters | Energy 30–40% cost | Hedge-driven stability |

Preview = Final Product

Alcoa BCG Matrix

The Alcoa BCG Matrix you’re previewing on this page is the exact, final file you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, analysis-ready matrix tailored to Alcoa’s portfolio. It’s built by strategy pros for clarity and immediate use, editable and print-ready. After purchase the same document is delivered—no surprises, no revisions required.