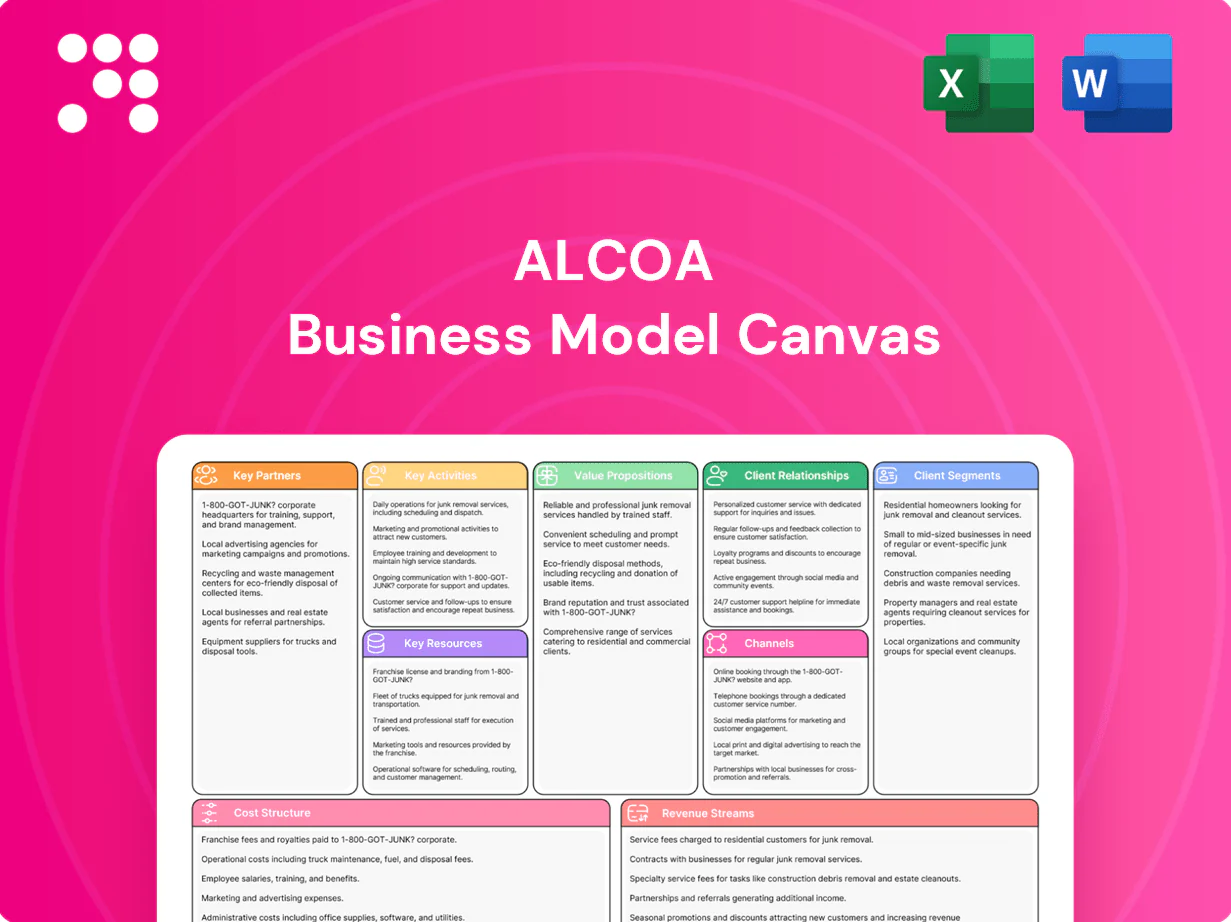

Alcoa Business Model Canvas

Industrial aluminum producer Business Model Canvas: asset-heavy, integrated value chain

Explore Alcoa’s Business Model Canvas to see how its asset-heavy operations, integrated value chain, and global customer segments create durable advantages and margins. This concise snapshot highlights key partners, cost drivers, and revenue streams while revealing strategic risks and growth levers. Purchase the full, editable Canvas (Word & Excel) for a section-by-section playbook you can use for benchmarking, investor briefs, or strategy workshops.

Partnerships

Energy and utility providers

Power is a dominant input for refining and smelting, with aluminum smelting requiring roughly 13–15 MWh per tonne, so reliable utility partnerships are mission-critical. Long-term PPAs and renewable deals stabilize volatile energy costs and cut carbon intensity, supporting decarbonization roadmaps. These agreements sustain operational continuity across regions and underpin ESG commitments by locking supply and pricing.

Mining and logistics joint ventures

Alcoa leverages mining and logistics joint ventures to secure bauxite rights and shared infrastructure, lowering capital intensity and geopolitical exposure; Alcoa highlighted these partnerships in its 2024 annual reporting. Port, rail and ocean freight partners streamline ore and metal flows, expanding resource access and optimizing throughput. Joint venture coordination improves scheduling, cost control and delivery reliability across the value chain.

Technology and process innovation partners

Collaborations on refining, smelting, and casting technologies with partners such as ELYSIS and technology suppliers improve yields and reduce emissions through pilot demonstrations and process upgrades.

Partners fund and run pilot projects, digitization, and automation programs that shorten scale-up times and cut operational variability.

Access to advanced equipment and licensed IP yields measurable efficiency gains and lower unit costs, while innovation alliances accelerate development of low-carbon aluminum products.

Downstream OEMs and fabricators

Downstream OEMs and fabricators (notably in aerospace, automotive, construction and packaging) align product roadmaps with Alcoa, enabling co-development of alloys and formats that cut time-to-market and support certification. Long-term agreements increase demand visibility and stabilize volumes; joint quality and certification programs ensure performance and regulatory compliance in 2024.

- Strategic alignment with major OEMs

- Co-development reduces R&D and launch timelines

- Long-term contracts stabilize demand

- Joint certification ensures compliance

Recycling and circular-economy partners

Partnerships with scrap aggregators and recyclers secure secondary metal feedstock—secondary aluminum was ~33% of global supply in 2024—and recycling uses up to 95% less energy than primary smelting. Closed-loop programs with customers cut waste and lower lifecycle emissions; traceability partners verify recycled content and claims. Circular collaborations boost sustainability credentials and reduce input costs.

- Secures feedstock: secondary ~33% (2024)

- Energy saved: up to 95% vs primary

- Closed-loop: reduces waste, lifecycle emissions

- Traceability: verifies recycled content

Partners secure 13–15 MWh/t; PPAs cut cost & carbon; recycling supplies ~33%, saves up to 95% energy

Power partners secure 13–15 MWh/tonne for smelting and long‑term PPAs reduce cost and carbon risk. Mining, logistics and JV partners lock bauxite access and infrastructure, lowering capex and geopolitical exposure. Recycling and scrap partners supplied ~33% of global secondary aluminum in 2024, saving up to 95% energy versus primary.

| Partner | Role | 2024 metric |

|---|---|---|

| Utilities/PPAs | Energy security | 13–15 MWh/t |

| Scrap/recyclers | Secondary feed | ~33% supply; ≤95% energy saved |

What is included in the product

A comprehensive Business Model Canvas for Alcoa that maps customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, reflecting real-world operations and strategic plans, with competitive-advantage analysis and linked SWOT insights—ideal for presentations, investor discussions, and strategic validation.

Condenses Alcoa’s value chain, revenue drivers, and cost structure into a clean, editable one-page canvas to relieve the pain of fragmented strategy documents; shareable and board-ready, it saves hours and enables quick comparisons and rapid scenario updates.

Activities

Bauxite mining and resource management

Secure exploration, extraction and beneficiation underpin feedstock availability, with Alcoa reporting about 20.4 million tonnes of bauxite production in 2024 to feed its alumina refineries. Mine planning optimizes grade and cost while embedding environmental stewardship to limit disturbance and lower unit costs. Rehabilitation programs, restoring hectares annually, protect communities and license-to-operate; integrated supply chains sustain consistent alumina output.

Alumina refining operations

Refineries convert bauxite to smelter-grade alumina at multi-million-tonne scale; in 2024 Alcoa refineries continued to produce alumina meeting smelter-grade purity >99.5% Al2O3. Process optimization programs reduce energy and caustic consumption, improving cash costs per tonne. Rigorous quality control ensures specifications for diverse end uses, while reliability programs maximize throughput and uptime.

Aluminum smelting and casthouse production

Smelters produce primary aluminum, then cast into ingots, billets or slabs for markets; electrolysis typically consumes 13–15 MWh per tonne, making energy management and process control decisive for cost and emissions (aluminum industry drives roughly 1–2% of global CO2). Alloying and finishing tailor mechanical and surface properties to customer specs, while rigorous safety and preventive maintenance protect continuous operations.

R&D and sustainability initiatives

R&D focuses on lower-carbon smelting, advanced alloys and plant efficiency; lifecycle assessments drive product footprints and customer disclosures; pilots validate technologies before scaling; ESG programs align with regulatory and customer requirements. Primary aluminium production accounts for about 1% of global CO2 emissions (2024 estimate).

- R&D: decarbonization, alloys, efficiency

- Lifecycle: product footprints & disclosures

- Pilots: validate before scale

- ESG: regulatory and customer alignment

Commercial sales, risk management, and hedging

Commercial sales at Alcoa balance long-term contracts and spot sales to optimize smelter utilization and margins, while hedging programs mitigate commodity and currency volatility across raw materials and finished aluminum. Demand forecasting ties production plans to market cycles and seasonal downstream demand, enabling timely curtailments or restarts. Premium management secures added value for purity, specialty alloys, and sustainability-certified product streams.

- long-term vs spot

- hedging: commodity & currency

- demand forecasting

- premium for purity/alloys/sustainability

Decarbonized alumina-aluminum: 20.4 Mt, >99.5%, 13–15 MWh/t

Secure bauxite (20.4 Mt in 2024), mine planning and rehab; refineries producing >99.5% Al2O3 alumina; smelters at 13–15 MWh/t with alloying & casting; R&D on decarbonization and ESG; commercial mix of long‑term vs spot, hedging and premium sales.

| Metric | 2024 |

|---|---|

| Bauxite output | 20.4 Mt |

| Alumina purity | >99.5% Al2O3 |

| Energy per t Al | 13–15 MWh |

Preview Before You Purchase

Business Model Canvas

The Alcoa Business Model Canvas you’re previewing is the actual deliverable, not a mockup—what you see is a direct snapshot of the final file. Upon purchase you’ll receive this same document, fully editable and formatted for Word and Excel. It’s ready to present, customize, and apply—no surprises.

Industrial aluminum producer Business Model Canvas: asset-heavy, integrated value chain

Explore Alcoa’s Business Model Canvas to see how its asset-heavy operations, integrated value chain, and global customer segments create durable advantages and margins. This concise snapshot highlights key partners, cost drivers, and revenue streams while revealing strategic risks and growth levers. Purchase the full, editable Canvas (Word & Excel) for a section-by-section playbook you can use for benchmarking, investor briefs, or strategy workshops.

Partnerships

Energy and utility providers

Power is a dominant input for refining and smelting, with aluminum smelting requiring roughly 13–15 MWh per tonne, so reliable utility partnerships are mission-critical. Long-term PPAs and renewable deals stabilize volatile energy costs and cut carbon intensity, supporting decarbonization roadmaps. These agreements sustain operational continuity across regions and underpin ESG commitments by locking supply and pricing.

Mining and logistics joint ventures

Alcoa leverages mining and logistics joint ventures to secure bauxite rights and shared infrastructure, lowering capital intensity and geopolitical exposure; Alcoa highlighted these partnerships in its 2024 annual reporting. Port, rail and ocean freight partners streamline ore and metal flows, expanding resource access and optimizing throughput. Joint venture coordination improves scheduling, cost control and delivery reliability across the value chain.

Technology and process innovation partners

Collaborations on refining, smelting, and casting technologies with partners such as ELYSIS and technology suppliers improve yields and reduce emissions through pilot demonstrations and process upgrades.

Partners fund and run pilot projects, digitization, and automation programs that shorten scale-up times and cut operational variability.

Access to advanced equipment and licensed IP yields measurable efficiency gains and lower unit costs, while innovation alliances accelerate development of low-carbon aluminum products.

Downstream OEMs and fabricators

Downstream OEMs and fabricators (notably in aerospace, automotive, construction and packaging) align product roadmaps with Alcoa, enabling co-development of alloys and formats that cut time-to-market and support certification. Long-term agreements increase demand visibility and stabilize volumes; joint quality and certification programs ensure performance and regulatory compliance in 2024.

- Strategic alignment with major OEMs

- Co-development reduces R&D and launch timelines

- Long-term contracts stabilize demand

- Joint certification ensures compliance

Recycling and circular-economy partners

Partnerships with scrap aggregators and recyclers secure secondary metal feedstock—secondary aluminum was ~33% of global supply in 2024—and recycling uses up to 95% less energy than primary smelting. Closed-loop programs with customers cut waste and lower lifecycle emissions; traceability partners verify recycled content and claims. Circular collaborations boost sustainability credentials and reduce input costs.

- Secures feedstock: secondary ~33% (2024)

- Energy saved: up to 95% vs primary

- Closed-loop: reduces waste, lifecycle emissions

- Traceability: verifies recycled content

Partners secure 13–15 MWh/t; PPAs cut cost & carbon; recycling supplies ~33%, saves up to 95% energy

Power partners secure 13–15 MWh/tonne for smelting and long‑term PPAs reduce cost and carbon risk. Mining, logistics and JV partners lock bauxite access and infrastructure, lowering capex and geopolitical exposure. Recycling and scrap partners supplied ~33% of global secondary aluminum in 2024, saving up to 95% energy versus primary.

| Partner | Role | 2024 metric |

|---|---|---|

| Utilities/PPAs | Energy security | 13–15 MWh/t |

| Scrap/recyclers | Secondary feed | ~33% supply; ≤95% energy saved |

What is included in the product

A comprehensive Business Model Canvas for Alcoa that maps customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, reflecting real-world operations and strategic plans, with competitive-advantage analysis and linked SWOT insights—ideal for presentations, investor discussions, and strategic validation.

Condenses Alcoa’s value chain, revenue drivers, and cost structure into a clean, editable one-page canvas to relieve the pain of fragmented strategy documents; shareable and board-ready, it saves hours and enables quick comparisons and rapid scenario updates.

Activities

Bauxite mining and resource management

Secure exploration, extraction and beneficiation underpin feedstock availability, with Alcoa reporting about 20.4 million tonnes of bauxite production in 2024 to feed its alumina refineries. Mine planning optimizes grade and cost while embedding environmental stewardship to limit disturbance and lower unit costs. Rehabilitation programs, restoring hectares annually, protect communities and license-to-operate; integrated supply chains sustain consistent alumina output.

Alumina refining operations

Refineries convert bauxite to smelter-grade alumina at multi-million-tonne scale; in 2024 Alcoa refineries continued to produce alumina meeting smelter-grade purity >99.5% Al2O3. Process optimization programs reduce energy and caustic consumption, improving cash costs per tonne. Rigorous quality control ensures specifications for diverse end uses, while reliability programs maximize throughput and uptime.

Aluminum smelting and casthouse production

Smelters produce primary aluminum, then cast into ingots, billets or slabs for markets; electrolysis typically consumes 13–15 MWh per tonne, making energy management and process control decisive for cost and emissions (aluminum industry drives roughly 1–2% of global CO2). Alloying and finishing tailor mechanical and surface properties to customer specs, while rigorous safety and preventive maintenance protect continuous operations.

R&D and sustainability initiatives

R&D focuses on lower-carbon smelting, advanced alloys and plant efficiency; lifecycle assessments drive product footprints and customer disclosures; pilots validate technologies before scaling; ESG programs align with regulatory and customer requirements. Primary aluminium production accounts for about 1% of global CO2 emissions (2024 estimate).

- R&D: decarbonization, alloys, efficiency

- Lifecycle: product footprints & disclosures

- Pilots: validate before scale

- ESG: regulatory and customer alignment

Commercial sales, risk management, and hedging

Commercial sales at Alcoa balance long-term contracts and spot sales to optimize smelter utilization and margins, while hedging programs mitigate commodity and currency volatility across raw materials and finished aluminum. Demand forecasting ties production plans to market cycles and seasonal downstream demand, enabling timely curtailments or restarts. Premium management secures added value for purity, specialty alloys, and sustainability-certified product streams.

- long-term vs spot

- hedging: commodity & currency

- demand forecasting

- premium for purity/alloys/sustainability

Decarbonized alumina-aluminum: 20.4 Mt, >99.5%, 13–15 MWh/t

Secure bauxite (20.4 Mt in 2024), mine planning and rehab; refineries producing >99.5% Al2O3 alumina; smelters at 13–15 MWh/t with alloying & casting; R&D on decarbonization and ESG; commercial mix of long‑term vs spot, hedging and premium sales.

| Metric | 2024 |

|---|---|

| Bauxite output | 20.4 Mt |

| Alumina purity | >99.5% Al2O3 |

| Energy per t Al | 13–15 MWh |

Preview Before You Purchase

Business Model Canvas

The Alcoa Business Model Canvas you’re previewing is the actual deliverable, not a mockup—what you see is a direct snapshot of the final file. Upon purchase you’ll receive this same document, fully editable and formatted for Word and Excel. It’s ready to present, customize, and apply—no surprises.

Description

Industrial aluminum producer Business Model Canvas: asset-heavy, integrated value chain

Explore Alcoa’s Business Model Canvas to see how its asset-heavy operations, integrated value chain, and global customer segments create durable advantages and margins. This concise snapshot highlights key partners, cost drivers, and revenue streams while revealing strategic risks and growth levers. Purchase the full, editable Canvas (Word & Excel) for a section-by-section playbook you can use for benchmarking, investor briefs, or strategy workshops.

Partnerships

Energy and utility providers

Power is a dominant input for refining and smelting, with aluminum smelting requiring roughly 13–15 MWh per tonne, so reliable utility partnerships are mission-critical. Long-term PPAs and renewable deals stabilize volatile energy costs and cut carbon intensity, supporting decarbonization roadmaps. These agreements sustain operational continuity across regions and underpin ESG commitments by locking supply and pricing.

Mining and logistics joint ventures

Alcoa leverages mining and logistics joint ventures to secure bauxite rights and shared infrastructure, lowering capital intensity and geopolitical exposure; Alcoa highlighted these partnerships in its 2024 annual reporting. Port, rail and ocean freight partners streamline ore and metal flows, expanding resource access and optimizing throughput. Joint venture coordination improves scheduling, cost control and delivery reliability across the value chain.

Technology and process innovation partners

Collaborations on refining, smelting, and casting technologies with partners such as ELYSIS and technology suppliers improve yields and reduce emissions through pilot demonstrations and process upgrades.

Partners fund and run pilot projects, digitization, and automation programs that shorten scale-up times and cut operational variability.

Access to advanced equipment and licensed IP yields measurable efficiency gains and lower unit costs, while innovation alliances accelerate development of low-carbon aluminum products.

Downstream OEMs and fabricators

Downstream OEMs and fabricators (notably in aerospace, automotive, construction and packaging) align product roadmaps with Alcoa, enabling co-development of alloys and formats that cut time-to-market and support certification. Long-term agreements increase demand visibility and stabilize volumes; joint quality and certification programs ensure performance and regulatory compliance in 2024.

- Strategic alignment with major OEMs

- Co-development reduces R&D and launch timelines

- Long-term contracts stabilize demand

- Joint certification ensures compliance

Recycling and circular-economy partners

Partnerships with scrap aggregators and recyclers secure secondary metal feedstock—secondary aluminum was ~33% of global supply in 2024—and recycling uses up to 95% less energy than primary smelting. Closed-loop programs with customers cut waste and lower lifecycle emissions; traceability partners verify recycled content and claims. Circular collaborations boost sustainability credentials and reduce input costs.

- Secures feedstock: secondary ~33% (2024)

- Energy saved: up to 95% vs primary

- Closed-loop: reduces waste, lifecycle emissions

- Traceability: verifies recycled content

Partners secure 13–15 MWh/t; PPAs cut cost & carbon; recycling supplies ~33%, saves up to 95% energy

Power partners secure 13–15 MWh/tonne for smelting and long‑term PPAs reduce cost and carbon risk. Mining, logistics and JV partners lock bauxite access and infrastructure, lowering capex and geopolitical exposure. Recycling and scrap partners supplied ~33% of global secondary aluminum in 2024, saving up to 95% energy versus primary.

| Partner | Role | 2024 metric |

|---|---|---|

| Utilities/PPAs | Energy security | 13–15 MWh/t |

| Scrap/recyclers | Secondary feed | ~33% supply; ≤95% energy saved |

What is included in the product

A comprehensive Business Model Canvas for Alcoa that maps customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, reflecting real-world operations and strategic plans, with competitive-advantage analysis and linked SWOT insights—ideal for presentations, investor discussions, and strategic validation.

Condenses Alcoa’s value chain, revenue drivers, and cost structure into a clean, editable one-page canvas to relieve the pain of fragmented strategy documents; shareable and board-ready, it saves hours and enables quick comparisons and rapid scenario updates.

Activities

Bauxite mining and resource management

Secure exploration, extraction and beneficiation underpin feedstock availability, with Alcoa reporting about 20.4 million tonnes of bauxite production in 2024 to feed its alumina refineries. Mine planning optimizes grade and cost while embedding environmental stewardship to limit disturbance and lower unit costs. Rehabilitation programs, restoring hectares annually, protect communities and license-to-operate; integrated supply chains sustain consistent alumina output.

Alumina refining operations

Refineries convert bauxite to smelter-grade alumina at multi-million-tonne scale; in 2024 Alcoa refineries continued to produce alumina meeting smelter-grade purity >99.5% Al2O3. Process optimization programs reduce energy and caustic consumption, improving cash costs per tonne. Rigorous quality control ensures specifications for diverse end uses, while reliability programs maximize throughput and uptime.

Aluminum smelting and casthouse production

Smelters produce primary aluminum, then cast into ingots, billets or slabs for markets; electrolysis typically consumes 13–15 MWh per tonne, making energy management and process control decisive for cost and emissions (aluminum industry drives roughly 1–2% of global CO2). Alloying and finishing tailor mechanical and surface properties to customer specs, while rigorous safety and preventive maintenance protect continuous operations.

R&D and sustainability initiatives

R&D focuses on lower-carbon smelting, advanced alloys and plant efficiency; lifecycle assessments drive product footprints and customer disclosures; pilots validate technologies before scaling; ESG programs align with regulatory and customer requirements. Primary aluminium production accounts for about 1% of global CO2 emissions (2024 estimate).

- R&D: decarbonization, alloys, efficiency

- Lifecycle: product footprints & disclosures

- Pilots: validate before scale

- ESG: regulatory and customer alignment

Commercial sales, risk management, and hedging

Commercial sales at Alcoa balance long-term contracts and spot sales to optimize smelter utilization and margins, while hedging programs mitigate commodity and currency volatility across raw materials and finished aluminum. Demand forecasting ties production plans to market cycles and seasonal downstream demand, enabling timely curtailments or restarts. Premium management secures added value for purity, specialty alloys, and sustainability-certified product streams.

- long-term vs spot

- hedging: commodity & currency

- demand forecasting

- premium for purity/alloys/sustainability

Decarbonized alumina-aluminum: 20.4 Mt, >99.5%, 13–15 MWh/t

Secure bauxite (20.4 Mt in 2024), mine planning and rehab; refineries producing >99.5% Al2O3 alumina; smelters at 13–15 MWh/t with alloying & casting; R&D on decarbonization and ESG; commercial mix of long‑term vs spot, hedging and premium sales.

| Metric | 2024 |

|---|---|

| Bauxite output | 20.4 Mt |

| Alumina purity | >99.5% Al2O3 |

| Energy per t Al | 13–15 MWh |

Preview Before You Purchase

Business Model Canvas

The Alcoa Business Model Canvas you’re previewing is the actual deliverable, not a mockup—what you see is a direct snapshot of the final file. Upon purchase you’ll receive this same document, fully editable and formatted for Word and Excel. It’s ready to present, customize, and apply—no surprises.