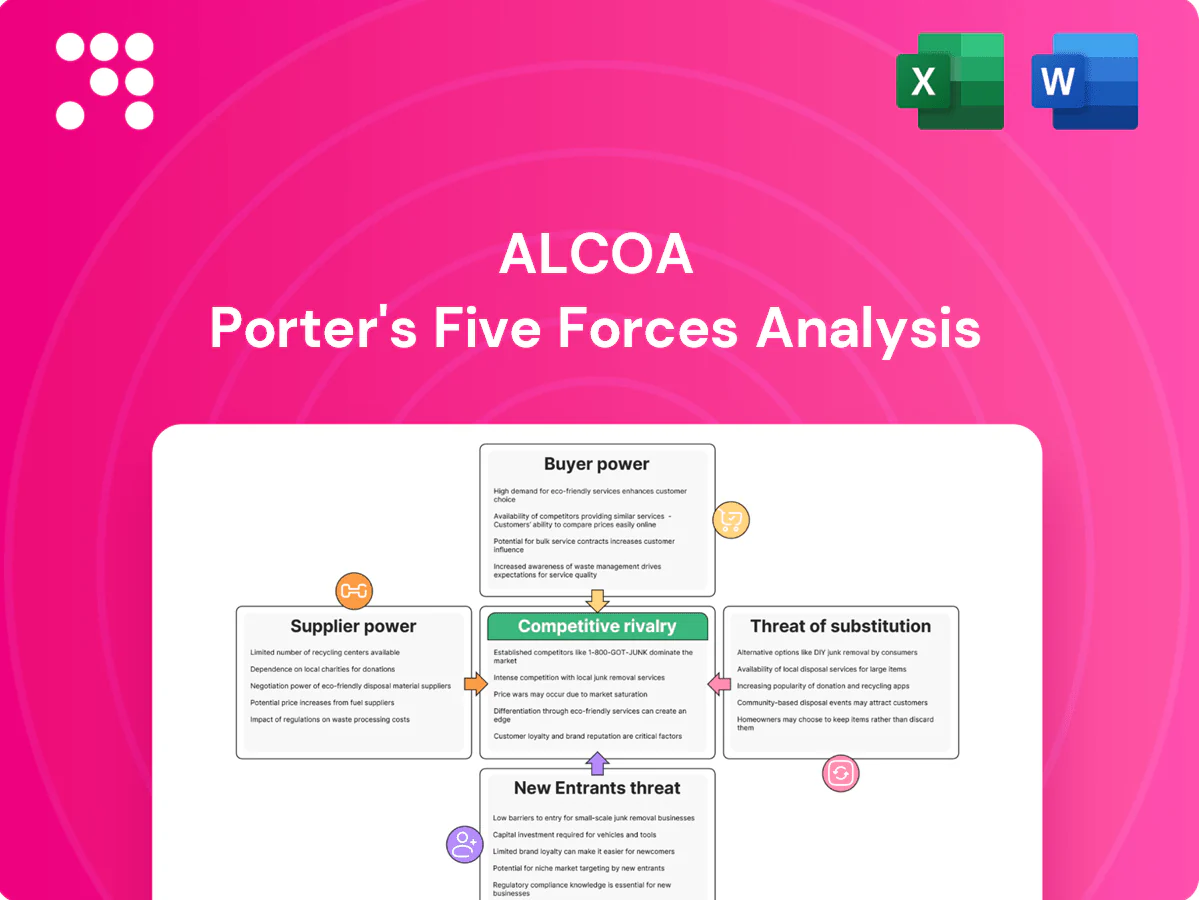

Alcoa Porter's Five Forces Analysis

Don't Miss the Bigger Picture

This concise Porter's Five Forces snapshot highlights Alcoa's bargaining power, competitive rivalry, and external threats in a nutshell. It surfaces supplier and buyer dynamics plus substitution risks that shape margins. For data-driven strategy and investment clarity, the full report unpacks force-by-force ratings and implications. Unlock the complete analysis to act with confidence.

Suppliers Bargaining Power

Energy input concentration

Aluminum smelting consumes about 13–15 MWh per tonne, giving utilities outsized leverage over pricing and reliability; Alcoa offsets this via long-term power contracts and siting near low-cost sources but remains materially exposed. Rapid shifts in hydropower availability and gas markets can move cost curves swiftly, while 2024 carbon prices such as the EU ETS (~€100/t in 2024) and decarbonization premiums increase supplier influence.

Critical consumables

Critical consumables such as carbon anodes, caustic soda and refractories are supplied by relatively concentrated global players; availability constraints or 2024 price spikes (caustic soda and refractory shocks) can compress alumina and smelting margins quickly. Qualification and quality consistency limit Alcoa’s switching flexibility. Alcoa’s 2024 revenue of about $6.1 billion gives negotiating leverage but does not fully neutralize supplier concentration risk.

Logistics and bulk shipping

Bauxite, alumina and aluminum move in bulk ocean freight via Capesize (≈150,000 dwt) and Panamax/Handy terminals, so port access and vessel availability materially boost logistics providers’ leverage. Canal constraints (Panama drought-related draft limits in 2023–24) and weather/geopolitics ripple through timing and costs. Long-term charters and route diversification reduce volatility but do not remove supplier bargaining power.

Equipment and technology vendors

Smelting technology, cell components and automation for Alcoa are supplied by a narrow set of specialized OEMs, and in 2024 top-tier vendors remain concentrated, giving suppliers pricing and upgrade leverage; switching costs are high due to integration and downtime risk. Proprietary upgrades (efficiency/emissions) enhance vendor bargaining power despite Alcoa framework agreements and in-house engineering.

- High vendor concentration: 3-5 major OEMs in 2024

- Switching costs: costly downtime and integration

- Proprietary upgrades drive leverage (efficiency/emissions)

- Frameworks and in-house R&D mitigate but do not commoditize

Labor and permitting dependencies

Aluminum margins under pressure: power 13–15 MWh/t, EU ETS €100/t

Alcoa faces strong supplier power: power (13–15 MWh/t) and EU ETS ~€100/t in 2024 drive cost exposure despite long-term contracts; consumables (carbon anodes, caustic, refractories) are concentrated with price/availability shocks; OEMs (3–5 major vendors) and skilled labor (US unemployment ~3.9% in 2024) create high switching costs and regional permitting leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Power | 13–15 MWh/t; EU ETS ~€100/t | High cost exposure |

| Consumables | Concentrated suppliers | Margin volatility |

| OEMs/labor | 3–5 OEMs; unemployment 3.9% | High switching cost |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and rivalry tailored to Alcoa’s aluminum value chain, highlighting disruptive threats, pricing pressures, and strategic levers to defend market share and profitability.

Clear one-sheet Porter's Five Forces for Alcoa—instantly visualize supplier, buyer, competitive, threat, and substitute pressures with an editable radar and slide-ready layout.

Customers Bargaining Power

Large industrial customers

Large aerospace, automotive, construction and packaging buyers are sizable, sophisticated and price-aware; in 2024 global primary aluminum demand reached about 67 million tonnes, concentrating negotiating power among major OEMs and converters. Their scale forces tough talks on price, quality and delivery, while technical specs create supplier stickiness but impose rigorous qualification hurdles. Framework contracts stabilize volumes yet embed strict pricing discipline and penalty clauses.

LME-linked pricing

Many of Alcoa’s contracts reference LME aluminium (2024 average ~2,300 USD/tonne) plus regional premiums, passing commodity volatility into sales. Buyers lean on spot LME benchmarks to extract discounts or demand surcharges tied to short-term spreads. That linkage limits Alcoa’s ability to set prices unilaterally and increases customer bargaining power. Alcoa counters with value-add and low-carbon premiums to reduce pure commodity exposure.

Alternative sourcing options

Global rivals and abundant Chinese capacity—roughly 60% of world primary aluminum capacity—give buyers multiple sources, while secondary (recycled) metal, about 20–25% of supply, offers an alternative for standard grades. Switching costs are moderate once qualification (specs, supply security) is cleared, and widespread dual-sourcing keeps buyer leverage and price pressure high.

Spec-driven lock-in

High-spec aerospace and auto applications demand NADCAP and AS9100 certifications, creating spec-driven lock-in that lowers buyer power for niche, performance-critical alloys; qualification cycles typically last 12–36 months, which limits immediate switching. Over time certification windows open bids to competitors, so Alcoa’s reliability and QA (NADCAP pass rates, on-time delivery) are vital to retain incumbency.

- Spec certifications: NADCAP, AS9100

- Qualification cycle: 12–36 months

- Buyer power: reduced for niche products

- Key retention factors: reliability, QA performance

Sustainability demands

Customers increasingly demand lower-carbon, traceable aluminium, giving buyers leverage through procurement standards and supplier scorecards; by 2024 Alcoa promoted hydro-powered and decarbonized product lines that aim to capture premiums in disclosed contracts. Alcoa can command higher prices for certified low-carbon metal but must meet stringent disclosures and chain-of-custody audits; failure risks disqualification from strategic OEM and infrastructure tenders.

- traceability-driven procurement

- hydro/decarbonized premium capture

- stringent disclosures required

- risk: disqualification from key segments

OEMs control aluminium trade - 67 Mt, China ~60% capacity

Large OEMs concentrate negotiating power (global primary aluminium demand ~67 Mt in 2024), forcing price, quality and delivery pressure. Sales often reference LME (~2,300 USD/t 2024 avg) plus premiums, limiting unilateral pricing. Chinese capacity (~60%) and secondary supply (20–25%) keep buyer leverage high; certifications (12–36 months) reduce power for niche alloys.

| Metric | 2024 value | Impact |

|---|---|---|

| Global demand | 67 Mt | Concentrated buyers |

| LME avg | ~2,300 USD/t | Price benchmarking |

| Chinese capacity | ~60% | Multiple suppliers |

| Secondary supply | 20–25% | Alternative sourcing |

| Qualification | 12–36 months | Lock-in for niche |

Preview the Actual Deliverable

Alcoa Porter's Five Forces Analysis

This preview shows the exact Alcoa Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full, professionally formatted document is ready for immediate download after purchase. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes. What you see is what you get.

Don't Miss the Bigger Picture

This concise Porter's Five Forces snapshot highlights Alcoa's bargaining power, competitive rivalry, and external threats in a nutshell. It surfaces supplier and buyer dynamics plus substitution risks that shape margins. For data-driven strategy and investment clarity, the full report unpacks force-by-force ratings and implications. Unlock the complete analysis to act with confidence.

Suppliers Bargaining Power

Energy input concentration

Aluminum smelting consumes about 13–15 MWh per tonne, giving utilities outsized leverage over pricing and reliability; Alcoa offsets this via long-term power contracts and siting near low-cost sources but remains materially exposed. Rapid shifts in hydropower availability and gas markets can move cost curves swiftly, while 2024 carbon prices such as the EU ETS (~€100/t in 2024) and decarbonization premiums increase supplier influence.

Critical consumables

Critical consumables such as carbon anodes, caustic soda and refractories are supplied by relatively concentrated global players; availability constraints or 2024 price spikes (caustic soda and refractory shocks) can compress alumina and smelting margins quickly. Qualification and quality consistency limit Alcoa’s switching flexibility. Alcoa’s 2024 revenue of about $6.1 billion gives negotiating leverage but does not fully neutralize supplier concentration risk.

Logistics and bulk shipping

Bauxite, alumina and aluminum move in bulk ocean freight via Capesize (≈150,000 dwt) and Panamax/Handy terminals, so port access and vessel availability materially boost logistics providers’ leverage. Canal constraints (Panama drought-related draft limits in 2023–24) and weather/geopolitics ripple through timing and costs. Long-term charters and route diversification reduce volatility but do not remove supplier bargaining power.

Equipment and technology vendors

Smelting technology, cell components and automation for Alcoa are supplied by a narrow set of specialized OEMs, and in 2024 top-tier vendors remain concentrated, giving suppliers pricing and upgrade leverage; switching costs are high due to integration and downtime risk. Proprietary upgrades (efficiency/emissions) enhance vendor bargaining power despite Alcoa framework agreements and in-house engineering.

- High vendor concentration: 3-5 major OEMs in 2024

- Switching costs: costly downtime and integration

- Proprietary upgrades drive leverage (efficiency/emissions)

- Frameworks and in-house R&D mitigate but do not commoditize

Labor and permitting dependencies

Aluminum margins under pressure: power 13–15 MWh/t, EU ETS €100/t

Alcoa faces strong supplier power: power (13–15 MWh/t) and EU ETS ~€100/t in 2024 drive cost exposure despite long-term contracts; consumables (carbon anodes, caustic, refractories) are concentrated with price/availability shocks; OEMs (3–5 major vendors) and skilled labor (US unemployment ~3.9% in 2024) create high switching costs and regional permitting leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Power | 13–15 MWh/t; EU ETS ~€100/t | High cost exposure |

| Consumables | Concentrated suppliers | Margin volatility |

| OEMs/labor | 3–5 OEMs; unemployment 3.9% | High switching cost |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and rivalry tailored to Alcoa’s aluminum value chain, highlighting disruptive threats, pricing pressures, and strategic levers to defend market share and profitability.

Clear one-sheet Porter's Five Forces for Alcoa—instantly visualize supplier, buyer, competitive, threat, and substitute pressures with an editable radar and slide-ready layout.

Customers Bargaining Power

Large industrial customers

Large aerospace, automotive, construction and packaging buyers are sizable, sophisticated and price-aware; in 2024 global primary aluminum demand reached about 67 million tonnes, concentrating negotiating power among major OEMs and converters. Their scale forces tough talks on price, quality and delivery, while technical specs create supplier stickiness but impose rigorous qualification hurdles. Framework contracts stabilize volumes yet embed strict pricing discipline and penalty clauses.

LME-linked pricing

Many of Alcoa’s contracts reference LME aluminium (2024 average ~2,300 USD/tonne) plus regional premiums, passing commodity volatility into sales. Buyers lean on spot LME benchmarks to extract discounts or demand surcharges tied to short-term spreads. That linkage limits Alcoa’s ability to set prices unilaterally and increases customer bargaining power. Alcoa counters with value-add and low-carbon premiums to reduce pure commodity exposure.

Alternative sourcing options

Global rivals and abundant Chinese capacity—roughly 60% of world primary aluminum capacity—give buyers multiple sources, while secondary (recycled) metal, about 20–25% of supply, offers an alternative for standard grades. Switching costs are moderate once qualification (specs, supply security) is cleared, and widespread dual-sourcing keeps buyer leverage and price pressure high.

Spec-driven lock-in

High-spec aerospace and auto applications demand NADCAP and AS9100 certifications, creating spec-driven lock-in that lowers buyer power for niche, performance-critical alloys; qualification cycles typically last 12–36 months, which limits immediate switching. Over time certification windows open bids to competitors, so Alcoa’s reliability and QA (NADCAP pass rates, on-time delivery) are vital to retain incumbency.

- Spec certifications: NADCAP, AS9100

- Qualification cycle: 12–36 months

- Buyer power: reduced for niche products

- Key retention factors: reliability, QA performance

Sustainability demands

Customers increasingly demand lower-carbon, traceable aluminium, giving buyers leverage through procurement standards and supplier scorecards; by 2024 Alcoa promoted hydro-powered and decarbonized product lines that aim to capture premiums in disclosed contracts. Alcoa can command higher prices for certified low-carbon metal but must meet stringent disclosures and chain-of-custody audits; failure risks disqualification from strategic OEM and infrastructure tenders.

- traceability-driven procurement

- hydro/decarbonized premium capture

- stringent disclosures required

- risk: disqualification from key segments

OEMs control aluminium trade - 67 Mt, China ~60% capacity

Large OEMs concentrate negotiating power (global primary aluminium demand ~67 Mt in 2024), forcing price, quality and delivery pressure. Sales often reference LME (~2,300 USD/t 2024 avg) plus premiums, limiting unilateral pricing. Chinese capacity (~60%) and secondary supply (20–25%) keep buyer leverage high; certifications (12–36 months) reduce power for niche alloys.

| Metric | 2024 value | Impact |

|---|---|---|

| Global demand | 67 Mt | Concentrated buyers |

| LME avg | ~2,300 USD/t | Price benchmarking |

| Chinese capacity | ~60% | Multiple suppliers |

| Secondary supply | 20–25% | Alternative sourcing |

| Qualification | 12–36 months | Lock-in for niche |

Preview the Actual Deliverable

Alcoa Porter's Five Forces Analysis

This preview shows the exact Alcoa Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full, professionally formatted document is ready for immediate download after purchase. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes. What you see is what you get.

Description

Don't Miss the Bigger Picture

This concise Porter's Five Forces snapshot highlights Alcoa's bargaining power, competitive rivalry, and external threats in a nutshell. It surfaces supplier and buyer dynamics plus substitution risks that shape margins. For data-driven strategy and investment clarity, the full report unpacks force-by-force ratings and implications. Unlock the complete analysis to act with confidence.

Suppliers Bargaining Power

Energy input concentration

Aluminum smelting consumes about 13–15 MWh per tonne, giving utilities outsized leverage over pricing and reliability; Alcoa offsets this via long-term power contracts and siting near low-cost sources but remains materially exposed. Rapid shifts in hydropower availability and gas markets can move cost curves swiftly, while 2024 carbon prices such as the EU ETS (~€100/t in 2024) and decarbonization premiums increase supplier influence.

Critical consumables

Critical consumables such as carbon anodes, caustic soda and refractories are supplied by relatively concentrated global players; availability constraints or 2024 price spikes (caustic soda and refractory shocks) can compress alumina and smelting margins quickly. Qualification and quality consistency limit Alcoa’s switching flexibility. Alcoa’s 2024 revenue of about $6.1 billion gives negotiating leverage but does not fully neutralize supplier concentration risk.

Logistics and bulk shipping

Bauxite, alumina and aluminum move in bulk ocean freight via Capesize (≈150,000 dwt) and Panamax/Handy terminals, so port access and vessel availability materially boost logistics providers’ leverage. Canal constraints (Panama drought-related draft limits in 2023–24) and weather/geopolitics ripple through timing and costs. Long-term charters and route diversification reduce volatility but do not remove supplier bargaining power.

Equipment and technology vendors

Smelting technology, cell components and automation for Alcoa are supplied by a narrow set of specialized OEMs, and in 2024 top-tier vendors remain concentrated, giving suppliers pricing and upgrade leverage; switching costs are high due to integration and downtime risk. Proprietary upgrades (efficiency/emissions) enhance vendor bargaining power despite Alcoa framework agreements and in-house engineering.

- High vendor concentration: 3-5 major OEMs in 2024

- Switching costs: costly downtime and integration

- Proprietary upgrades drive leverage (efficiency/emissions)

- Frameworks and in-house R&D mitigate but do not commoditize

Labor and permitting dependencies

Aluminum margins under pressure: power 13–15 MWh/t, EU ETS €100/t

Alcoa faces strong supplier power: power (13–15 MWh/t) and EU ETS ~€100/t in 2024 drive cost exposure despite long-term contracts; consumables (carbon anodes, caustic, refractories) are concentrated with price/availability shocks; OEMs (3–5 major vendors) and skilled labor (US unemployment ~3.9% in 2024) create high switching costs and regional permitting leverage.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Power | 13–15 MWh/t; EU ETS ~€100/t | High cost exposure |

| Consumables | Concentrated suppliers | Margin volatility |

| OEMs/labor | 3–5 OEMs; unemployment 3.9% | High switching cost |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and rivalry tailored to Alcoa’s aluminum value chain, highlighting disruptive threats, pricing pressures, and strategic levers to defend market share and profitability.

Clear one-sheet Porter's Five Forces for Alcoa—instantly visualize supplier, buyer, competitive, threat, and substitute pressures with an editable radar and slide-ready layout.

Customers Bargaining Power

Large industrial customers

Large aerospace, automotive, construction and packaging buyers are sizable, sophisticated and price-aware; in 2024 global primary aluminum demand reached about 67 million tonnes, concentrating negotiating power among major OEMs and converters. Their scale forces tough talks on price, quality and delivery, while technical specs create supplier stickiness but impose rigorous qualification hurdles. Framework contracts stabilize volumes yet embed strict pricing discipline and penalty clauses.

LME-linked pricing

Many of Alcoa’s contracts reference LME aluminium (2024 average ~2,300 USD/tonne) plus regional premiums, passing commodity volatility into sales. Buyers lean on spot LME benchmarks to extract discounts or demand surcharges tied to short-term spreads. That linkage limits Alcoa’s ability to set prices unilaterally and increases customer bargaining power. Alcoa counters with value-add and low-carbon premiums to reduce pure commodity exposure.

Alternative sourcing options

Global rivals and abundant Chinese capacity—roughly 60% of world primary aluminum capacity—give buyers multiple sources, while secondary (recycled) metal, about 20–25% of supply, offers an alternative for standard grades. Switching costs are moderate once qualification (specs, supply security) is cleared, and widespread dual-sourcing keeps buyer leverage and price pressure high.

Spec-driven lock-in

High-spec aerospace and auto applications demand NADCAP and AS9100 certifications, creating spec-driven lock-in that lowers buyer power for niche, performance-critical alloys; qualification cycles typically last 12–36 months, which limits immediate switching. Over time certification windows open bids to competitors, so Alcoa’s reliability and QA (NADCAP pass rates, on-time delivery) are vital to retain incumbency.

- Spec certifications: NADCAP, AS9100

- Qualification cycle: 12–36 months

- Buyer power: reduced for niche products

- Key retention factors: reliability, QA performance

Sustainability demands

Customers increasingly demand lower-carbon, traceable aluminium, giving buyers leverage through procurement standards and supplier scorecards; by 2024 Alcoa promoted hydro-powered and decarbonized product lines that aim to capture premiums in disclosed contracts. Alcoa can command higher prices for certified low-carbon metal but must meet stringent disclosures and chain-of-custody audits; failure risks disqualification from strategic OEM and infrastructure tenders.

- traceability-driven procurement

- hydro/decarbonized premium capture

- stringent disclosures required

- risk: disqualification from key segments

OEMs control aluminium trade - 67 Mt, China ~60% capacity

Large OEMs concentrate negotiating power (global primary aluminium demand ~67 Mt in 2024), forcing price, quality and delivery pressure. Sales often reference LME (~2,300 USD/t 2024 avg) plus premiums, limiting unilateral pricing. Chinese capacity (~60%) and secondary supply (20–25%) keep buyer leverage high; certifications (12–36 months) reduce power for niche alloys.

| Metric | 2024 value | Impact |

|---|---|---|

| Global demand | 67 Mt | Concentrated buyers |

| LME avg | ~2,300 USD/t | Price benchmarking |

| Chinese capacity | ~60% | Multiple suppliers |

| Secondary supply | 20–25% | Alternative sourcing |

| Qualification | 12–36 months | Lock-in for niche |

Preview the Actual Deliverable

Alcoa Porter's Five Forces Analysis

This preview shows the exact Alcoa Porter's Five Forces Analysis you'll receive—no placeholders or mockups. The full, professionally formatted document is ready for immediate download after purchase. It covers competitive rivalry, supplier and buyer power, threats of entry and substitutes. What you see is what you get.