Alex Lee Porter's Five Forces Analysis

From Overview to Strategy Blueprint

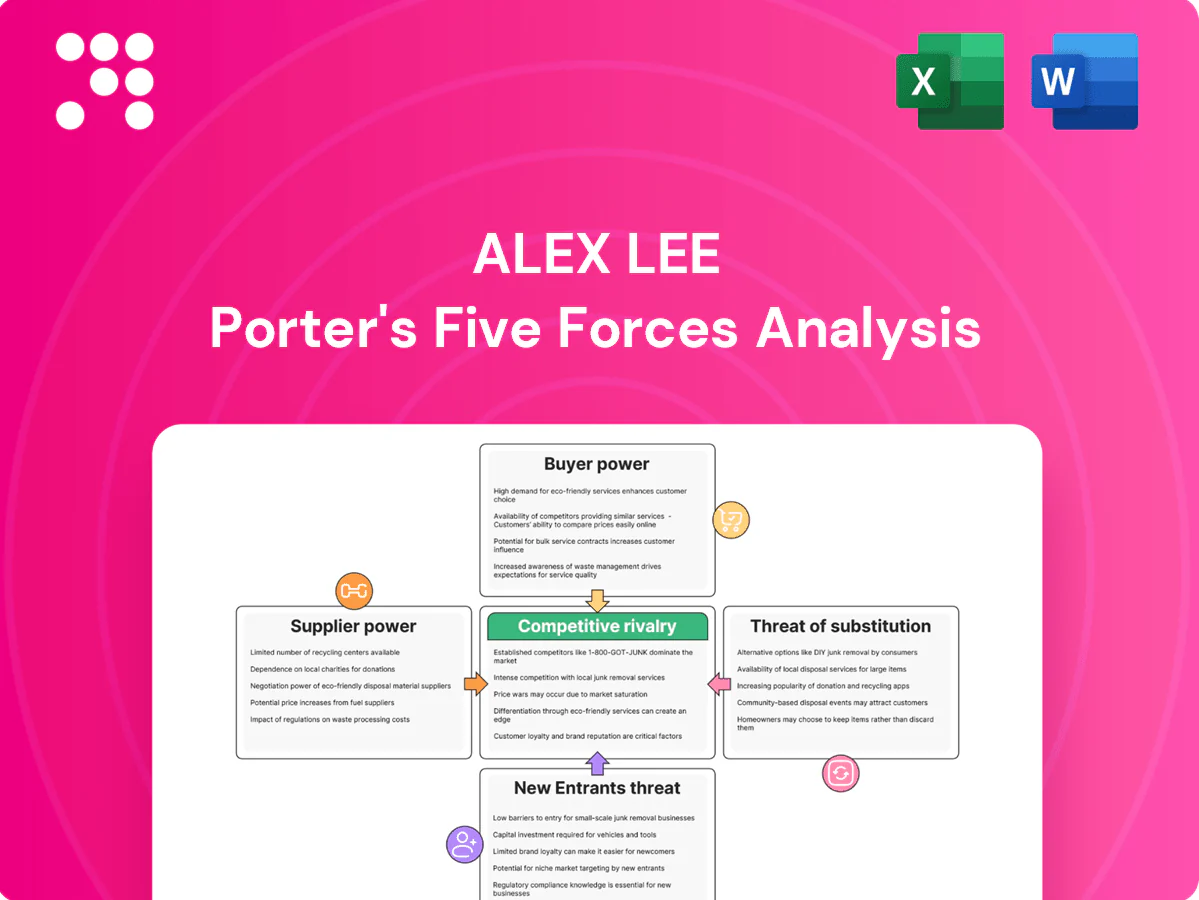

Quick snapshot: Alex Lee’s competitive landscape shows moderate buyer power, concentrated suppliers, manageable entry barriers, substitution risks from online grocers, and intense rivalry among regional chains. This brief overview hints at strategic levers but omits ratings, visuals and tactical recommendations. Unlock the full Porter's Five Forces Analysis to get force-by-force scores, charts and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated CPG brands

Concentrated national CPG brands wield significant leverage via brand equity and limited substitutes; the top 10 CPG firms account for about 40% of US category sales in 2024, enabling price hikes and slotting fees commonly in the $50k–$250k per SKU range that squeeze distributor and retailer margins. Alex Lee mitigates this through multi-category sourcing and an ~18% private-label mix, but must-stock requirements constrain flexibility, while long-term volume commitments reduce price volatility yet increase supplier lock-in.

Perishables and seasonal volatility

Produce, meat and dairy suppliers gain leverage during 2024 supply shocks and seasonal tightness as fresh produce often has shelf-lives under 10 days and meat/dairy stocks cannot be rebuilt quickly, forcing rapid acceptance of supplier terms to avoid out-of-stocks.

Diversified sourcing and cold-chain investments cut risk—FAO notes roughly 14% post-harvest food loss globally—yet freight and yield variability still transmit price and availability shocks to buyers.

Hedging and forward contracts blunt volatility but require capital and forecasting accuracy; margin requirements on commodity contracts commonly range 5–10% of notional value, constraining smaller buyers.

Private label and co-packers

Own-brand manufacturing partners can boost margins but gain leverage when capacity is tight or specs are bespoke; switching co-packers forces requalification, packaging redesign and service disruption risk. Alex Lee’s multi-billion-dollar scale through MDI in 2024 secures longer runs and tougher pricing, while dual-sourcing and standardized specs materially reduce supplier dependence and interruption exposure.

Logistics, fuel, and packaging inputs

Upstream carriers, fuel suppliers, and packaging vendors directly drive delivered cost; tight trucking markets and diesel spikes lifted contract and spot rates in 2024, with U.S. diesel averaging about $3.80/gal and contract linehaul up mid-single digits year-over-year. Alex Lee’s fleet scale, routing tech, and intermodal options trim exposure, but fuel surcharges and pass-through fees still raise inbound/outbound costs.

- Carrier concentration increases supplier leverage

- Diesel ~ $3.80/gal in 2024 raised variable cost share

- Long-term contracts lower volatility

- Fleet scale + routing tech = partial offset

Regulatory and compliance demands

Food safety, traceability and labeling rules shift power to larger, certified suppliers as compliance costs rise; CDC estimates 48 million foodborne illnesses annually in the US, underscoring regulatory pressure. Smaller producers often lack certifications, narrowing the vendor pool and increasing supplier leverage. Alex Lee’s QA and audit programs expand eligible suppliers over time, while digital traceability standardizes expectations and reduces risk.

- compliance-driven supplier consolidation

- certification gap raises supplier leverage

- QA/audits expand supplier base

- digital traceability lowers operational risk

Concentrated CPGs (≈40%) + slotting fees squeeze retail; diesel hits costs

Concentrated CPGs (top 10 ≈40% US sales in 2024) and slotting fees ($50k–$250k/SKU) drive supplier leverage; Alex Lee’s ~18% private-label mix cushions pricing power but must-stock and long-term commitments limit flexibility. Produce/meat/dairy seasonal tightness and short shelf-life force acceptance of terms; hedging requires 5–10% margin capital. Diesel ≈ $3.80/gal in 2024 raised logistics cost exposure despite fleet scale.

| Metric | 2024 |

|---|---|

| Top10 CPG share | ≈40% |

| Slotting fee/SKU | $50k–$250k |

| Diesel (US) | $3.80/gal |

What is included in the product

Comprehensive Five Forces analysis tailored for Alex Lee Porter, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to market share; includes strategic commentary and editable Word format for easy integration into investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter’s Five Forces analysis with customizable pressure sliders and an instant radar chart—perfect for quick strategic decisions, slide-ready and easy to adapt to changing market data.

Customers Bargaining Power

Independent grocers’ price sensitivity

Independent retail customers are highly price-focused due to thin single-digit operating margins, commonly 1–3% in the US independent grocery sector in 2024, and intense local competition. They routinely compare landed cost, promotional allowances, and payment terms across wholesalers, elevating buyer power and squeezing distributor margins. Alex Lee faces this margin pressure, though value-added services like category management and private-label support can partly offset pure price competition.

Switching options among wholesalers

Alternatives like C&S, UNFI and regional specialists give buyers credible outside options; many independents can feasibly switch despite assortment resets because onboarding is commonly 4–12 weeks. Contract structures and service-level agreements, often 6–12 month terms, reduce churn. High fill rates (typically >95%) and tailored assortments materially increase stickiness.

Retail consumers’ omnichannel choices

Lowes Foods shoppers can defect to Walmart (≈25% of US grocery sales in 2024), Kroger (≈10%), Publix, Aldi (≈4%), Lidl or online channels (≈6% of grocery sales in 2024). Price transparency via apps and weekly ads raises customer bargaining power and accelerates switching. Loyalty programs and curated in-store experiences reduce churn. Tiered private labels (≈18% private‑label share in 2024) anchor retention.

Demand for service and data

- Demand: category mgmt, e-comm, analytics

- Win: planograms + content = higher share

- Strategy: trade services for longer terms/preferred placement

Payment terms and credit

Independent retailers, which in 2024 still comprised 99.9% of US firms by count, frequently secure favorable payment terms and credit that ease their working capital needs but shift cash pressure onto wholesalers. Longer terms raise carrying costs and liquidity strain; credit fosters loyalty while concentrating receivable risk; disciplined credit policies limit default exposure and support sustainable growth.

- Payment terms: relieve retailer WC

- Extended terms: increase wholesaler carrying costs

- Credit support: boosts loyalty, concentrates risk

- Policy discipline: balances growth vs defaults

Indy grocers face 1–3% margins as 9.7% e-comm rises

Independent grocers (1–3% operating margins in 2024) are highly price-sensitive, comparing landed cost, promos and terms; credible alternatives (C&S, UNFI, regional) and 9.7% grocery e‑commerce share raise switching risk. Alex Lee offsets pressure via category mgmt, private label (≈18% share) and extended service-for-term trades.

| Metric | 2024 |

|---|---|

| Indy operating margin | 1–3% |

| Grocery e‑comm | 9.7% |

| Private label share | ≈18% |

| Major competitor share (Walmart) | ≈25% |

Same Document Delivered

Alex Lee Porter's Five Forces Analysis

This preview shows the exact Alex Lee Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders or excerpts. The file is fully formatted, professionally written, and ready for download and use the moment you buy. No mockups, no customization required; what you see is what you get.

From Overview to Strategy Blueprint

Quick snapshot: Alex Lee’s competitive landscape shows moderate buyer power, concentrated suppliers, manageable entry barriers, substitution risks from online grocers, and intense rivalry among regional chains. This brief overview hints at strategic levers but omits ratings, visuals and tactical recommendations. Unlock the full Porter's Five Forces Analysis to get force-by-force scores, charts and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated CPG brands

Concentrated national CPG brands wield significant leverage via brand equity and limited substitutes; the top 10 CPG firms account for about 40% of US category sales in 2024, enabling price hikes and slotting fees commonly in the $50k–$250k per SKU range that squeeze distributor and retailer margins. Alex Lee mitigates this through multi-category sourcing and an ~18% private-label mix, but must-stock requirements constrain flexibility, while long-term volume commitments reduce price volatility yet increase supplier lock-in.

Perishables and seasonal volatility

Produce, meat and dairy suppliers gain leverage during 2024 supply shocks and seasonal tightness as fresh produce often has shelf-lives under 10 days and meat/dairy stocks cannot be rebuilt quickly, forcing rapid acceptance of supplier terms to avoid out-of-stocks.

Diversified sourcing and cold-chain investments cut risk—FAO notes roughly 14% post-harvest food loss globally—yet freight and yield variability still transmit price and availability shocks to buyers.

Hedging and forward contracts blunt volatility but require capital and forecasting accuracy; margin requirements on commodity contracts commonly range 5–10% of notional value, constraining smaller buyers.

Private label and co-packers

Own-brand manufacturing partners can boost margins but gain leverage when capacity is tight or specs are bespoke; switching co-packers forces requalification, packaging redesign and service disruption risk. Alex Lee’s multi-billion-dollar scale through MDI in 2024 secures longer runs and tougher pricing, while dual-sourcing and standardized specs materially reduce supplier dependence and interruption exposure.

Logistics, fuel, and packaging inputs

Upstream carriers, fuel suppliers, and packaging vendors directly drive delivered cost; tight trucking markets and diesel spikes lifted contract and spot rates in 2024, with U.S. diesel averaging about $3.80/gal and contract linehaul up mid-single digits year-over-year. Alex Lee’s fleet scale, routing tech, and intermodal options trim exposure, but fuel surcharges and pass-through fees still raise inbound/outbound costs.

- Carrier concentration increases supplier leverage

- Diesel ~ $3.80/gal in 2024 raised variable cost share

- Long-term contracts lower volatility

- Fleet scale + routing tech = partial offset

Regulatory and compliance demands

Food safety, traceability and labeling rules shift power to larger, certified suppliers as compliance costs rise; CDC estimates 48 million foodborne illnesses annually in the US, underscoring regulatory pressure. Smaller producers often lack certifications, narrowing the vendor pool and increasing supplier leverage. Alex Lee’s QA and audit programs expand eligible suppliers over time, while digital traceability standardizes expectations and reduces risk.

- compliance-driven supplier consolidation

- certification gap raises supplier leverage

- QA/audits expand supplier base

- digital traceability lowers operational risk

Concentrated CPGs (≈40%) + slotting fees squeeze retail; diesel hits costs

Concentrated CPGs (top 10 ≈40% US sales in 2024) and slotting fees ($50k–$250k/SKU) drive supplier leverage; Alex Lee’s ~18% private-label mix cushions pricing power but must-stock and long-term commitments limit flexibility. Produce/meat/dairy seasonal tightness and short shelf-life force acceptance of terms; hedging requires 5–10% margin capital. Diesel ≈ $3.80/gal in 2024 raised logistics cost exposure despite fleet scale.

| Metric | 2024 |

|---|---|

| Top10 CPG share | ≈40% |

| Slotting fee/SKU | $50k–$250k |

| Diesel (US) | $3.80/gal |

What is included in the product

Comprehensive Five Forces analysis tailored for Alex Lee Porter, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to market share; includes strategic commentary and editable Word format for easy integration into investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter’s Five Forces analysis with customizable pressure sliders and an instant radar chart—perfect for quick strategic decisions, slide-ready and easy to adapt to changing market data.

Customers Bargaining Power

Independent grocers’ price sensitivity

Independent retail customers are highly price-focused due to thin single-digit operating margins, commonly 1–3% in the US independent grocery sector in 2024, and intense local competition. They routinely compare landed cost, promotional allowances, and payment terms across wholesalers, elevating buyer power and squeezing distributor margins. Alex Lee faces this margin pressure, though value-added services like category management and private-label support can partly offset pure price competition.

Switching options among wholesalers

Alternatives like C&S, UNFI and regional specialists give buyers credible outside options; many independents can feasibly switch despite assortment resets because onboarding is commonly 4–12 weeks. Contract structures and service-level agreements, often 6–12 month terms, reduce churn. High fill rates (typically >95%) and tailored assortments materially increase stickiness.

Retail consumers’ omnichannel choices

Lowes Foods shoppers can defect to Walmart (≈25% of US grocery sales in 2024), Kroger (≈10%), Publix, Aldi (≈4%), Lidl or online channels (≈6% of grocery sales in 2024). Price transparency via apps and weekly ads raises customer bargaining power and accelerates switching. Loyalty programs and curated in-store experiences reduce churn. Tiered private labels (≈18% private‑label share in 2024) anchor retention.

Demand for service and data

- Demand: category mgmt, e-comm, analytics

- Win: planograms + content = higher share

- Strategy: trade services for longer terms/preferred placement

Payment terms and credit

Independent retailers, which in 2024 still comprised 99.9% of US firms by count, frequently secure favorable payment terms and credit that ease their working capital needs but shift cash pressure onto wholesalers. Longer terms raise carrying costs and liquidity strain; credit fosters loyalty while concentrating receivable risk; disciplined credit policies limit default exposure and support sustainable growth.

- Payment terms: relieve retailer WC

- Extended terms: increase wholesaler carrying costs

- Credit support: boosts loyalty, concentrates risk

- Policy discipline: balances growth vs defaults

Indy grocers face 1–3% margins as 9.7% e-comm rises

Independent grocers (1–3% operating margins in 2024) are highly price-sensitive, comparing landed cost, promos and terms; credible alternatives (C&S, UNFI, regional) and 9.7% grocery e‑commerce share raise switching risk. Alex Lee offsets pressure via category mgmt, private label (≈18% share) and extended service-for-term trades.

| Metric | 2024 |

|---|---|

| Indy operating margin | 1–3% |

| Grocery e‑comm | 9.7% |

| Private label share | ≈18% |

| Major competitor share (Walmart) | ≈25% |

Same Document Delivered

Alex Lee Porter's Five Forces Analysis

This preview shows the exact Alex Lee Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders or excerpts. The file is fully formatted, professionally written, and ready for download and use the moment you buy. No mockups, no customization required; what you see is what you get.

Description

From Overview to Strategy Blueprint

Quick snapshot: Alex Lee’s competitive landscape shows moderate buyer power, concentrated suppliers, manageable entry barriers, substitution risks from online grocers, and intense rivalry among regional chains. This brief overview hints at strategic levers but omits ratings, visuals and tactical recommendations. Unlock the full Porter's Five Forces Analysis to get force-by-force scores, charts and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Concentrated CPG brands

Concentrated national CPG brands wield significant leverage via brand equity and limited substitutes; the top 10 CPG firms account for about 40% of US category sales in 2024, enabling price hikes and slotting fees commonly in the $50k–$250k per SKU range that squeeze distributor and retailer margins. Alex Lee mitigates this through multi-category sourcing and an ~18% private-label mix, but must-stock requirements constrain flexibility, while long-term volume commitments reduce price volatility yet increase supplier lock-in.

Perishables and seasonal volatility

Produce, meat and dairy suppliers gain leverage during 2024 supply shocks and seasonal tightness as fresh produce often has shelf-lives under 10 days and meat/dairy stocks cannot be rebuilt quickly, forcing rapid acceptance of supplier terms to avoid out-of-stocks.

Diversified sourcing and cold-chain investments cut risk—FAO notes roughly 14% post-harvest food loss globally—yet freight and yield variability still transmit price and availability shocks to buyers.

Hedging and forward contracts blunt volatility but require capital and forecasting accuracy; margin requirements on commodity contracts commonly range 5–10% of notional value, constraining smaller buyers.

Private label and co-packers

Own-brand manufacturing partners can boost margins but gain leverage when capacity is tight or specs are bespoke; switching co-packers forces requalification, packaging redesign and service disruption risk. Alex Lee’s multi-billion-dollar scale through MDI in 2024 secures longer runs and tougher pricing, while dual-sourcing and standardized specs materially reduce supplier dependence and interruption exposure.

Logistics, fuel, and packaging inputs

Upstream carriers, fuel suppliers, and packaging vendors directly drive delivered cost; tight trucking markets and diesel spikes lifted contract and spot rates in 2024, with U.S. diesel averaging about $3.80/gal and contract linehaul up mid-single digits year-over-year. Alex Lee’s fleet scale, routing tech, and intermodal options trim exposure, but fuel surcharges and pass-through fees still raise inbound/outbound costs.

- Carrier concentration increases supplier leverage

- Diesel ~ $3.80/gal in 2024 raised variable cost share

- Long-term contracts lower volatility

- Fleet scale + routing tech = partial offset

Regulatory and compliance demands

Food safety, traceability and labeling rules shift power to larger, certified suppliers as compliance costs rise; CDC estimates 48 million foodborne illnesses annually in the US, underscoring regulatory pressure. Smaller producers often lack certifications, narrowing the vendor pool and increasing supplier leverage. Alex Lee’s QA and audit programs expand eligible suppliers over time, while digital traceability standardizes expectations and reduces risk.

- compliance-driven supplier consolidation

- certification gap raises supplier leverage

- QA/audits expand supplier base

- digital traceability lowers operational risk

Concentrated CPGs (≈40%) + slotting fees squeeze retail; diesel hits costs

Concentrated CPGs (top 10 ≈40% US sales in 2024) and slotting fees ($50k–$250k/SKU) drive supplier leverage; Alex Lee’s ~18% private-label mix cushions pricing power but must-stock and long-term commitments limit flexibility. Produce/meat/dairy seasonal tightness and short shelf-life force acceptance of terms; hedging requires 5–10% margin capital. Diesel ≈ $3.80/gal in 2024 raised logistics cost exposure despite fleet scale.

| Metric | 2024 |

|---|---|

| Top10 CPG share | ≈40% |

| Slotting fee/SKU | $50k–$250k |

| Diesel (US) | $3.80/gal |

What is included in the product

Comprehensive Five Forces analysis tailored for Alex Lee Porter, uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to market share; includes strategic commentary and editable Word format for easy integration into investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter’s Five Forces analysis with customizable pressure sliders and an instant radar chart—perfect for quick strategic decisions, slide-ready and easy to adapt to changing market data.

Customers Bargaining Power

Independent grocers’ price sensitivity

Independent retail customers are highly price-focused due to thin single-digit operating margins, commonly 1–3% in the US independent grocery sector in 2024, and intense local competition. They routinely compare landed cost, promotional allowances, and payment terms across wholesalers, elevating buyer power and squeezing distributor margins. Alex Lee faces this margin pressure, though value-added services like category management and private-label support can partly offset pure price competition.

Switching options among wholesalers

Alternatives like C&S, UNFI and regional specialists give buyers credible outside options; many independents can feasibly switch despite assortment resets because onboarding is commonly 4–12 weeks. Contract structures and service-level agreements, often 6–12 month terms, reduce churn. High fill rates (typically >95%) and tailored assortments materially increase stickiness.

Retail consumers’ omnichannel choices

Lowes Foods shoppers can defect to Walmart (≈25% of US grocery sales in 2024), Kroger (≈10%), Publix, Aldi (≈4%), Lidl or online channels (≈6% of grocery sales in 2024). Price transparency via apps and weekly ads raises customer bargaining power and accelerates switching. Loyalty programs and curated in-store experiences reduce churn. Tiered private labels (≈18% private‑label share in 2024) anchor retention.

Demand for service and data

- Demand: category mgmt, e-comm, analytics

- Win: planograms + content = higher share

- Strategy: trade services for longer terms/preferred placement

Payment terms and credit

Independent retailers, which in 2024 still comprised 99.9% of US firms by count, frequently secure favorable payment terms and credit that ease their working capital needs but shift cash pressure onto wholesalers. Longer terms raise carrying costs and liquidity strain; credit fosters loyalty while concentrating receivable risk; disciplined credit policies limit default exposure and support sustainable growth.

- Payment terms: relieve retailer WC

- Extended terms: increase wholesaler carrying costs

- Credit support: boosts loyalty, concentrates risk

- Policy discipline: balances growth vs defaults

Indy grocers face 1–3% margins as 9.7% e-comm rises

Independent grocers (1–3% operating margins in 2024) are highly price-sensitive, comparing landed cost, promos and terms; credible alternatives (C&S, UNFI, regional) and 9.7% grocery e‑commerce share raise switching risk. Alex Lee offsets pressure via category mgmt, private label (≈18% share) and extended service-for-term trades.

| Metric | 2024 |

|---|---|

| Indy operating margin | 1–3% |

| Grocery e‑comm | 9.7% |

| Private label share | ≈18% |

| Major competitor share (Walmart) | ≈25% |

Same Document Delivered

Alex Lee Porter's Five Forces Analysis

This preview shows the exact Alex Lee Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders or excerpts. The file is fully formatted, professionally written, and ready for download and use the moment you buy. No mockups, no customization required; what you see is what you get.