Alior Bank Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

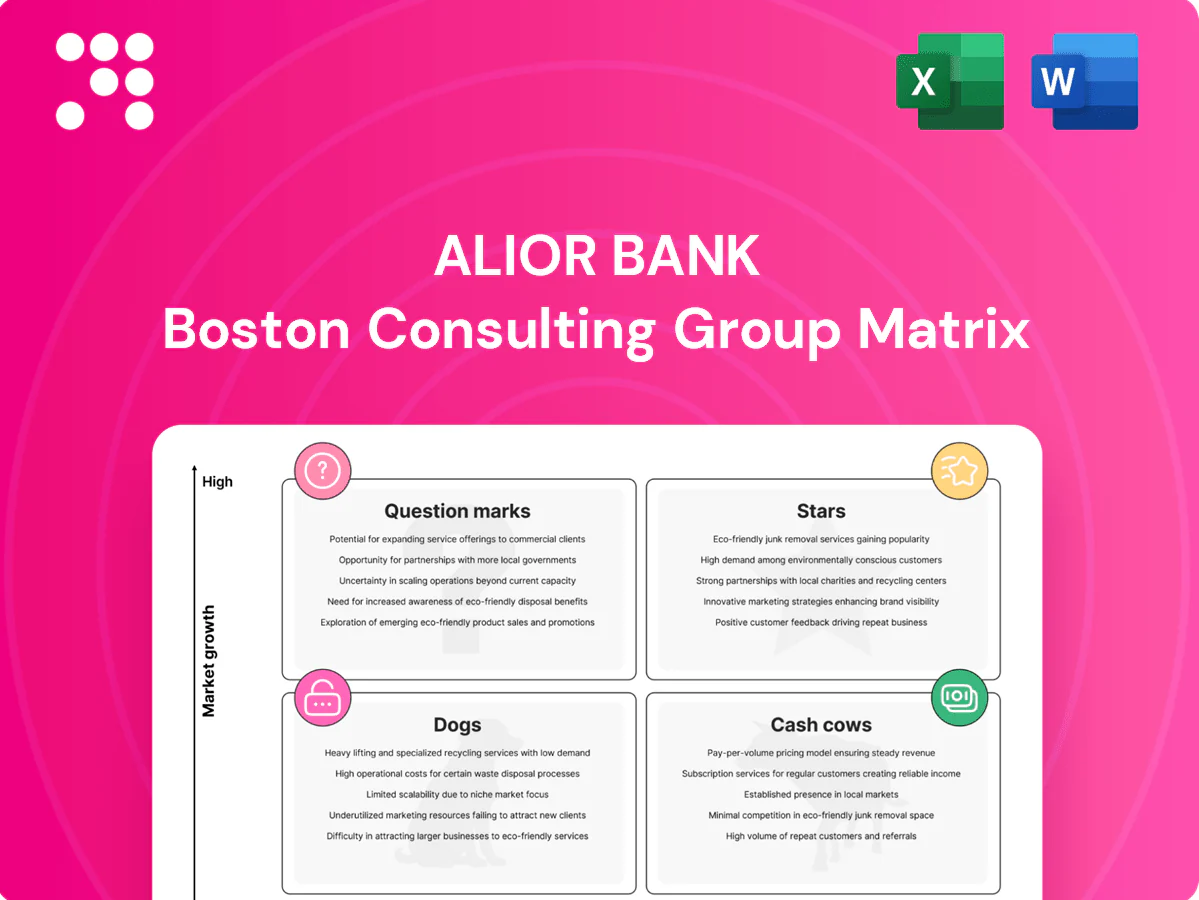

Alior Bank’s BCG Matrix preview shows where key products sit amid growth and market share shifts—some are rising stars, others quietly churning cash or asking hard questions. Want a clear picture of which services to double down on and which to prune? Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-present Word report plus an Excel summary. Skip the guesswork and get strategic clarity you can act on today.

Stars

Mobile & online banking platforms

Mobile and online banking at Alior Bank are Stars: high-growth usage and a dominant share within Alior’s customer base make digital the poster child Star. Engagement metrics climbed through 2024 as new features rolled out and the app increasingly sources deposits and loan originations. The platform requires sustained capex for upgrades and cybersecurity, but the product-to-deposit flywheel justifies continued spend. Maintain investment to cement leadership as Poland’s market matures.

Digital consumer lending (end-to-end onboarding)

Unsecured loans originated fully online are growing ~25% YoY in Poland in 2024 and Alior is strong where it plays, capturing above-market share in digital onboarding. Conversion is solid and unit economics improve as richer data reduces attrition and cost-to-income; marketing spend and model retraining, however, require continuous investment. Cash in equals cash out most months — classic Star behavior. Double down while the window’s open.

SME digital banking suite

SME digital banking suite addresses the 99.8% of Polish businesses that are SMEs, tapping a clear shift to online-first services with accounts, invoicing and instant credit to meet demand. Share looks attractive in chosen niches, but acquisition and support costs remain high. The prize is sticky SME relationships and cross-sell of loans, payments and treasury. Invest now to scale before growth cools and the product slides into Cow territory.

Instant payments and real-time transfers

Instant payments and real-time transfers are a Star for Alior: volume growth remains strong and, as of 2024, the bank processes a large share of instant transfers for its active retail base, reinforcing daily engagement and primary-bank status.

Infrastructure intensity — uptime, rails, fraud controls — keeps capex elevated, but resilience and UX prioritization protect customer habit and enable cross-sell.

- 2024: high volume growth, strong share of active-client instant transfers

- Capex-driven: uptime, rails, fraud prevention

- Strategic: anchors primary-bank status and daily habit

- Monetization: seeds payments, data, embedded-finance revenues

Open banking/API partnerships

Open banking/API partnerships are a Star for Alior: the market is ramping and Alior’s live integrations give it a right-now edge in aggregation and data-led offers, feeding onboarding and lending pipelines.

Partner operations raise costs and returns are building but not fully harvested; stay on offense with more use cases, smarter scoring and tighter consent UX to accelerate monetization.

- Tag: integrations — live aggregation accelerates cross-sell

- Tag: pipeline — APIs feed lending/onboarding

- Tag: returns — positive trajectory, not yet maximized

- Tag: priorities — expand use cases, improve scoring, simplify consent

Unsecured-online loans ~25% growth; SME suite in a 99.8% market, invest in UX & fraud

Alior’s digital channels, unsecured-online loans (~25% YoY growth in 2024) and SME suite (serving needs in a market where 99.8% of firms are SMEs) are Stars: high growth, strong share and requiring sustained capex for UX, rails and fraud. Instant payments drive daily engagement (large share of active-client transfers as of 2024) and open-banking APIs feed onboarding and lending pipelines; keep investing to scale monetization.

| Tag | Metric (2024) | Implication |

|---|---|---|

| Unsecured-online | ~25% YoY growth | Invest: scale & model retrain |

| SME suite | Market: 99.8% SMEs | High cross-sell potential |

| Instant payments | Large share of active transfers | Drives retention |

| APIs | Live integrations (2024) | Feeds pipelines |

What is included in the product

In-depth BCG analysis of Alior Bank’s products with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs

One-page Alior Bank BCG Matrix that clarifies priorities, eases portfolio decisions and speeds C-level alignment.

Cash Cows

Retail current and savings accounts (CASA)

Retail current and savings accounts (CASA) sit in a mature Polish retail market and represent a high share within Alior Bank’s existing client base, serving over 3.2 million customers in 2024 and accounting for roughly 45% of retail deposits. They deliver predictable flows with low promotional spend, a steady fee and NII drip that funds other bets and covers operating costs. Protect via simple perks and functionality rather than costly acquisition campaigns.

Cards and everyday payments

In 2024 Cards and everyday payments deliver stable swipe volumes for Alior Bank, with interchange and fee income reliably recurring. Growth is modest but margins remain healthy thanks to disciplined rewards and cost control. The franchise is a strong lever to finance Stars; optimize pricing and fraud to milk without overfeeding.

Mortgage portfolio

Alior Bank’s mortgage portfolio is a large, slow-growth book that provides a dependable interest spread when credit risk is tight, anchoring net interest income.

Acquisition costs are sunk and incremental cash comes from servicing efficiency and fee capture, making the portfolio a reliable cash cow rather than a headline growth driver.

It functions as a balance-sheet backbone; maintain underwriting quality and avoid rate gimmicks to preserve margins and capital metrics.

Corporate transaction banking

Corporate transaction banking at Alior Bank is a Cash Cow: accounts, transfers and cash management deliver sticky, scale-friendly revenue with low churn and standardized operations; 2024 saw continued deposit stability and strong cash conversion driven by fee and float income. Sales cycles remain long but predictable, and incremental tech investments in 2024 improved margins and operational efficiency.

- Sticky accounts & cash mgmt

- Low churn, long sales cycles

- Standardized ops → strong cash conversion

- 2024 tech upgrades raised margins

Treasury/ALM income

Treasury/ALM income at Alior Bank delivers steady NII/NFI through balance-sheet management and securities positioning; it won’t sprint but reliably covers funding and operating needs. Discipline in duration, liquidity buffers and hedging preserves margins; avoid one-off trading to protect the Cow. Keep capital-light, predictable strategies rather than rate-speculation.

- Focus: steady NII/NFI

- Risk controls: duration, liquidity, hedges

- Strategy: discipline over heroics

3.2m CASA, ~45% deposits: steady funding, recurring fees and predictable NII

Retail CASA serves 3.2 million customers in 2024 and supplies ~45% of retail deposits, providing stable low-cost funding. Cards and payments delivered steady swipe volumes and recurring fees in 2024, supporting margins. Mortgages are a large, slow-growth spread generator; corporate transaction banking showed deposit stability and high cash conversion in 2024. Treasury/ALM supplies predictable NII/NFI via disciplined duration and hedging.

| Product | 2024 metric | Role |

|---|---|---|

| CASA | 3.2m customers; ~45% deposits | Low-cost funding |

| Cards | Stable swipe volumes | Recurring fees |

| Mortgages | Large slow-growth book | Interest spread |

| Corp TB | Deposit stability 2024 | Cash conversion |

| Treasury | Predictable NII/NFI | Balance-sheet support |

Preview = Final Product

Alior Bank BCG Matrix

The Alior Bank BCG Matrix you’re previewing on this page is the exact file you’ll receive after purchase — no watermarks, no placeholders, just the finished strategic report. It’s tailored for Alior Bank’s portfolio, combining market data and clear quadrant recommendations. Once bought, the full document is instantly downloadable and ready to present or edit. You get a professional, analysis-ready deliverable with no surprises.

Visual. Strategic. Downloadable.

Alior Bank’s BCG Matrix preview shows where key products sit amid growth and market share shifts—some are rising stars, others quietly churning cash or asking hard questions. Want a clear picture of which services to double down on and which to prune? Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-present Word report plus an Excel summary. Skip the guesswork and get strategic clarity you can act on today.

Stars

Mobile & online banking platforms

Mobile and online banking at Alior Bank are Stars: high-growth usage and a dominant share within Alior’s customer base make digital the poster child Star. Engagement metrics climbed through 2024 as new features rolled out and the app increasingly sources deposits and loan originations. The platform requires sustained capex for upgrades and cybersecurity, but the product-to-deposit flywheel justifies continued spend. Maintain investment to cement leadership as Poland’s market matures.

Digital consumer lending (end-to-end onboarding)

Unsecured loans originated fully online are growing ~25% YoY in Poland in 2024 and Alior is strong where it plays, capturing above-market share in digital onboarding. Conversion is solid and unit economics improve as richer data reduces attrition and cost-to-income; marketing spend and model retraining, however, require continuous investment. Cash in equals cash out most months — classic Star behavior. Double down while the window’s open.

SME digital banking suite

SME digital banking suite addresses the 99.8% of Polish businesses that are SMEs, tapping a clear shift to online-first services with accounts, invoicing and instant credit to meet demand. Share looks attractive in chosen niches, but acquisition and support costs remain high. The prize is sticky SME relationships and cross-sell of loans, payments and treasury. Invest now to scale before growth cools and the product slides into Cow territory.

Instant payments and real-time transfers

Instant payments and real-time transfers are a Star for Alior: volume growth remains strong and, as of 2024, the bank processes a large share of instant transfers for its active retail base, reinforcing daily engagement and primary-bank status.

Infrastructure intensity — uptime, rails, fraud controls — keeps capex elevated, but resilience and UX prioritization protect customer habit and enable cross-sell.

- 2024: high volume growth, strong share of active-client instant transfers

- Capex-driven: uptime, rails, fraud prevention

- Strategic: anchors primary-bank status and daily habit

- Monetization: seeds payments, data, embedded-finance revenues

Open banking/API partnerships

Open banking/API partnerships are a Star for Alior: the market is ramping and Alior’s live integrations give it a right-now edge in aggregation and data-led offers, feeding onboarding and lending pipelines.

Partner operations raise costs and returns are building but not fully harvested; stay on offense with more use cases, smarter scoring and tighter consent UX to accelerate monetization.

- Tag: integrations — live aggregation accelerates cross-sell

- Tag: pipeline — APIs feed lending/onboarding

- Tag: returns — positive trajectory, not yet maximized

- Tag: priorities — expand use cases, improve scoring, simplify consent

Unsecured-online loans ~25% growth; SME suite in a 99.8% market, invest in UX & fraud

Alior’s digital channels, unsecured-online loans (~25% YoY growth in 2024) and SME suite (serving needs in a market where 99.8% of firms are SMEs) are Stars: high growth, strong share and requiring sustained capex for UX, rails and fraud. Instant payments drive daily engagement (large share of active-client transfers as of 2024) and open-banking APIs feed onboarding and lending pipelines; keep investing to scale monetization.

| Tag | Metric (2024) | Implication |

|---|---|---|

| Unsecured-online | ~25% YoY growth | Invest: scale & model retrain |

| SME suite | Market: 99.8% SMEs | High cross-sell potential |

| Instant payments | Large share of active transfers | Drives retention |

| APIs | Live integrations (2024) | Feeds pipelines |

What is included in the product

In-depth BCG analysis of Alior Bank’s products with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs

One-page Alior Bank BCG Matrix that clarifies priorities, eases portfolio decisions and speeds C-level alignment.

Cash Cows

Retail current and savings accounts (CASA)

Retail current and savings accounts (CASA) sit in a mature Polish retail market and represent a high share within Alior Bank’s existing client base, serving over 3.2 million customers in 2024 and accounting for roughly 45% of retail deposits. They deliver predictable flows with low promotional spend, a steady fee and NII drip that funds other bets and covers operating costs. Protect via simple perks and functionality rather than costly acquisition campaigns.

Cards and everyday payments

In 2024 Cards and everyday payments deliver stable swipe volumes for Alior Bank, with interchange and fee income reliably recurring. Growth is modest but margins remain healthy thanks to disciplined rewards and cost control. The franchise is a strong lever to finance Stars; optimize pricing and fraud to milk without overfeeding.

Mortgage portfolio

Alior Bank’s mortgage portfolio is a large, slow-growth book that provides a dependable interest spread when credit risk is tight, anchoring net interest income.

Acquisition costs are sunk and incremental cash comes from servicing efficiency and fee capture, making the portfolio a reliable cash cow rather than a headline growth driver.

It functions as a balance-sheet backbone; maintain underwriting quality and avoid rate gimmicks to preserve margins and capital metrics.

Corporate transaction banking

Corporate transaction banking at Alior Bank is a Cash Cow: accounts, transfers and cash management deliver sticky, scale-friendly revenue with low churn and standardized operations; 2024 saw continued deposit stability and strong cash conversion driven by fee and float income. Sales cycles remain long but predictable, and incremental tech investments in 2024 improved margins and operational efficiency.

- Sticky accounts & cash mgmt

- Low churn, long sales cycles

- Standardized ops → strong cash conversion

- 2024 tech upgrades raised margins

Treasury/ALM income

Treasury/ALM income at Alior Bank delivers steady NII/NFI through balance-sheet management and securities positioning; it won’t sprint but reliably covers funding and operating needs. Discipline in duration, liquidity buffers and hedging preserves margins; avoid one-off trading to protect the Cow. Keep capital-light, predictable strategies rather than rate-speculation.

- Focus: steady NII/NFI

- Risk controls: duration, liquidity, hedges

- Strategy: discipline over heroics

3.2m CASA, ~45% deposits: steady funding, recurring fees and predictable NII

Retail CASA serves 3.2 million customers in 2024 and supplies ~45% of retail deposits, providing stable low-cost funding. Cards and payments delivered steady swipe volumes and recurring fees in 2024, supporting margins. Mortgages are a large, slow-growth spread generator; corporate transaction banking showed deposit stability and high cash conversion in 2024. Treasury/ALM supplies predictable NII/NFI via disciplined duration and hedging.

| Product | 2024 metric | Role |

|---|---|---|

| CASA | 3.2m customers; ~45% deposits | Low-cost funding |

| Cards | Stable swipe volumes | Recurring fees |

| Mortgages | Large slow-growth book | Interest spread |

| Corp TB | Deposit stability 2024 | Cash conversion |

| Treasury | Predictable NII/NFI | Balance-sheet support |

Preview = Final Product

Alior Bank BCG Matrix

The Alior Bank BCG Matrix you’re previewing on this page is the exact file you’ll receive after purchase — no watermarks, no placeholders, just the finished strategic report. It’s tailored for Alior Bank’s portfolio, combining market data and clear quadrant recommendations. Once bought, the full document is instantly downloadable and ready to present or edit. You get a professional, analysis-ready deliverable with no surprises.

Description

Visual. Strategic. Downloadable.

Alior Bank’s BCG Matrix preview shows where key products sit amid growth and market share shifts—some are rising stars, others quietly churning cash or asking hard questions. Want a clear picture of which services to double down on and which to prune? Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a ready-to-present Word report plus an Excel summary. Skip the guesswork and get strategic clarity you can act on today.

Stars

Mobile & online banking platforms

Mobile and online banking at Alior Bank are Stars: high-growth usage and a dominant share within Alior’s customer base make digital the poster child Star. Engagement metrics climbed through 2024 as new features rolled out and the app increasingly sources deposits and loan originations. The platform requires sustained capex for upgrades and cybersecurity, but the product-to-deposit flywheel justifies continued spend. Maintain investment to cement leadership as Poland’s market matures.

Digital consumer lending (end-to-end onboarding)

Unsecured loans originated fully online are growing ~25% YoY in Poland in 2024 and Alior is strong where it plays, capturing above-market share in digital onboarding. Conversion is solid and unit economics improve as richer data reduces attrition and cost-to-income; marketing spend and model retraining, however, require continuous investment. Cash in equals cash out most months — classic Star behavior. Double down while the window’s open.

SME digital banking suite

SME digital banking suite addresses the 99.8% of Polish businesses that are SMEs, tapping a clear shift to online-first services with accounts, invoicing and instant credit to meet demand. Share looks attractive in chosen niches, but acquisition and support costs remain high. The prize is sticky SME relationships and cross-sell of loans, payments and treasury. Invest now to scale before growth cools and the product slides into Cow territory.

Instant payments and real-time transfers

Instant payments and real-time transfers are a Star for Alior: volume growth remains strong and, as of 2024, the bank processes a large share of instant transfers for its active retail base, reinforcing daily engagement and primary-bank status.

Infrastructure intensity — uptime, rails, fraud controls — keeps capex elevated, but resilience and UX prioritization protect customer habit and enable cross-sell.

- 2024: high volume growth, strong share of active-client instant transfers

- Capex-driven: uptime, rails, fraud prevention

- Strategic: anchors primary-bank status and daily habit

- Monetization: seeds payments, data, embedded-finance revenues

Open banking/API partnerships

Open banking/API partnerships are a Star for Alior: the market is ramping and Alior’s live integrations give it a right-now edge in aggregation and data-led offers, feeding onboarding and lending pipelines.

Partner operations raise costs and returns are building but not fully harvested; stay on offense with more use cases, smarter scoring and tighter consent UX to accelerate monetization.

- Tag: integrations — live aggregation accelerates cross-sell

- Tag: pipeline — APIs feed lending/onboarding

- Tag: returns — positive trajectory, not yet maximized

- Tag: priorities — expand use cases, improve scoring, simplify consent

Unsecured-online loans ~25% growth; SME suite in a 99.8% market, invest in UX & fraud

Alior’s digital channels, unsecured-online loans (~25% YoY growth in 2024) and SME suite (serving needs in a market where 99.8% of firms are SMEs) are Stars: high growth, strong share and requiring sustained capex for UX, rails and fraud. Instant payments drive daily engagement (large share of active-client transfers as of 2024) and open-banking APIs feed onboarding and lending pipelines; keep investing to scale monetization.

| Tag | Metric (2024) | Implication |

|---|---|---|

| Unsecured-online | ~25% YoY growth | Invest: scale & model retrain |

| SME suite | Market: 99.8% SMEs | High cross-sell potential |

| Instant payments | Large share of active transfers | Drives retention |

| APIs | Live integrations (2024) | Feeds pipelines |

What is included in the product

In-depth BCG analysis of Alior Bank’s products with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs

One-page Alior Bank BCG Matrix that clarifies priorities, eases portfolio decisions and speeds C-level alignment.

Cash Cows

Retail current and savings accounts (CASA)

Retail current and savings accounts (CASA) sit in a mature Polish retail market and represent a high share within Alior Bank’s existing client base, serving over 3.2 million customers in 2024 and accounting for roughly 45% of retail deposits. They deliver predictable flows with low promotional spend, a steady fee and NII drip that funds other bets and covers operating costs. Protect via simple perks and functionality rather than costly acquisition campaigns.

Cards and everyday payments

In 2024 Cards and everyday payments deliver stable swipe volumes for Alior Bank, with interchange and fee income reliably recurring. Growth is modest but margins remain healthy thanks to disciplined rewards and cost control. The franchise is a strong lever to finance Stars; optimize pricing and fraud to milk without overfeeding.

Mortgage portfolio

Alior Bank’s mortgage portfolio is a large, slow-growth book that provides a dependable interest spread when credit risk is tight, anchoring net interest income.

Acquisition costs are sunk and incremental cash comes from servicing efficiency and fee capture, making the portfolio a reliable cash cow rather than a headline growth driver.

It functions as a balance-sheet backbone; maintain underwriting quality and avoid rate gimmicks to preserve margins and capital metrics.

Corporate transaction banking

Corporate transaction banking at Alior Bank is a Cash Cow: accounts, transfers and cash management deliver sticky, scale-friendly revenue with low churn and standardized operations; 2024 saw continued deposit stability and strong cash conversion driven by fee and float income. Sales cycles remain long but predictable, and incremental tech investments in 2024 improved margins and operational efficiency.

- Sticky accounts & cash mgmt

- Low churn, long sales cycles

- Standardized ops → strong cash conversion

- 2024 tech upgrades raised margins

Treasury/ALM income

Treasury/ALM income at Alior Bank delivers steady NII/NFI through balance-sheet management and securities positioning; it won’t sprint but reliably covers funding and operating needs. Discipline in duration, liquidity buffers and hedging preserves margins; avoid one-off trading to protect the Cow. Keep capital-light, predictable strategies rather than rate-speculation.

- Focus: steady NII/NFI

- Risk controls: duration, liquidity, hedges

- Strategy: discipline over heroics

3.2m CASA, ~45% deposits: steady funding, recurring fees and predictable NII

Retail CASA serves 3.2 million customers in 2024 and supplies ~45% of retail deposits, providing stable low-cost funding. Cards and payments delivered steady swipe volumes and recurring fees in 2024, supporting margins. Mortgages are a large, slow-growth spread generator; corporate transaction banking showed deposit stability and high cash conversion in 2024. Treasury/ALM supplies predictable NII/NFI via disciplined duration and hedging.

| Product | 2024 metric | Role |

|---|---|---|

| CASA | 3.2m customers; ~45% deposits | Low-cost funding |

| Cards | Stable swipe volumes | Recurring fees |

| Mortgages | Large slow-growth book | Interest spread |

| Corp TB | Deposit stability 2024 | Cash conversion |

| Treasury | Predictable NII/NFI | Balance-sheet support |

Preview = Final Product

Alior Bank BCG Matrix

The Alior Bank BCG Matrix you’re previewing on this page is the exact file you’ll receive after purchase — no watermarks, no placeholders, just the finished strategic report. It’s tailored for Alior Bank’s portfolio, combining market data and clear quadrant recommendations. Once bought, the full document is instantly downloadable and ready to present or edit. You get a professional, analysis-ready deliverable with no surprises.